|

시장보고서

상품코드

1822585

자동차 분야 생성형 AI 시장 : 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Generative AI in Automotive Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

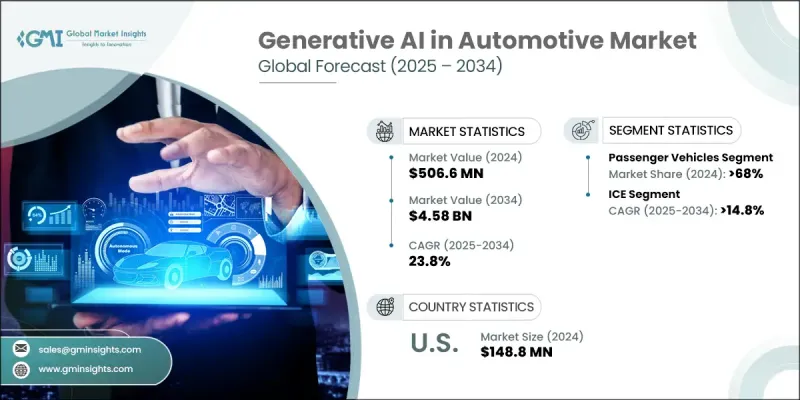

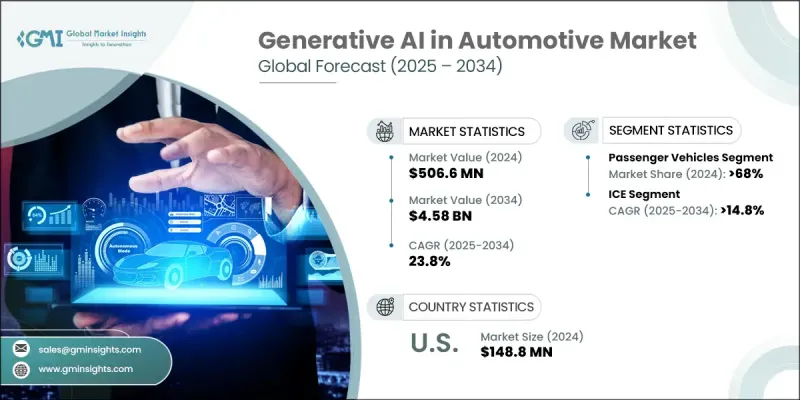

세계의 자동차 분야 생성형 AI 시장 규모는 2024년 5억 660만 달러에 달하고, CAGR 23.8%로 성장하여 2034년까지는 45억 8,000만 달러에 달할 것으로 예측되고 있습니다.

자동차 제조업체가 자율주행 시스템의 합리화, 설계 워크플로우 최적화, 중요한 운전 시나리오 시뮬레이션을 위해 생산적 인공지능의 통합을 진행함에 따라 업계는 급속한 변모를 이루고 있습니다. 규제에 의한 장려와 지원 자금은 자동차 제조업체, 부품 공급자, 모빌리티 기술 혁신자 전체의 개발에 박차를 가하고 있습니다. 디지털화가 깊어지고 자동차가 더 지능적으로 상호 연결됨에 따라 생성형 AI는 자동차 개발의 중심 존재가 되고 있습니다. 이를 통해 자동차 제조업체는 드물거나 복잡한 교통 이벤트를 재현할 수 있어 안전성 검증에 소요되는 시간과 비용을 크게 줄일 수 있습니다. 이 고급 기능은 시뮬레이션 정밀도의 새로운 기준을 만들어 내고 개발 기간 단축에 기여합니다. 자동차 제조업체는 현재 사용자 인터페이스 강화, 유지 보수 요구 사항 예측, 고급 운전 지원 시스템의 미세 조정에 생성형 AI를 활용하고 있습니다. 자동차 산업이 소프트웨어 정의 차량 및 커넥티드 플랫폼으로 전환하는 동안 AI는 더 이상 기능 확장이 아니라 차세대 이동성 에코시스템의 핵심이 되고 있습니다. 소프트웨어 기업과 하드웨어 개발자의 개발은 자동차 환경 전체에서 AI의 원활한 통합을 지원하는 기반 인프라를 구축하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시장 규모 | 5억 660만 달러 |

| 예측 금액 | 45억 8,000만 달러 |

| CAGR | 23.8% |

2024년, 승용차 부문은 차량 전체에 지능형 시스템이 널리 도입됨을 배경으로 68%의 점유율을 획득했습니다. AI 대응 기술은 현재 고급 인포테인먼트, 드라이버 지원 기능, 자동차 안전 시스템 등의 기능에 깊이 통합되어 있습니다. 이러한 도구는 대화형 인터페이스를 통한 상호작용 개선, 개인화된 통찰력 제공, 실시간으로 적응적인 응답 향상 등으로 운전 경험을 크게 향상시킵니다. 자동차 제조업체는 프로액티브 서비스 통지나 컨텍스트를 고려한 운전 제안 등의 기능에 의해 안전성과 기능성을 높이는 AI 툴에 주력하고 있습니다. 센서 기술의 지속적인 강화와 소프트웨어의 원격 업데이트는 이 부문에서 생성형 AI의 적용을 꾸준히 증가할 것으로 예측됩니다.

내연기관차(ICE) 부문은 2025년부터 2034년까지 연평균 복합 성장률(CAGR) 14.8%를 보일 것으로 예측됩니다. 전기자동차 플랫폼이 기술 도입의 최전선에 서는 경우가 많지만, 내연 기관차도 경쟁력을 유지하기 위해 AI 구동 시스템을 통합하고 있습니다. 자동차 제조업체는 기존 ICE 모델을 진단 기능 향상, 원활한 연결성 및 몰입형 디지털 경험을 지원하는 지능형 모듈로 업그레이드하고 있습니다. 이 진화는 프리미엄 ICE 차량의 스마트 기능에 대한 수요가 증가함에 따라 추진되고 있으며, AI 기반 시스템을 통한 개조는 무선 업데이트와 확장 가능한 플랫폼 기술을 통해 더욱 쉽게 액세스할 수 있습니다. 차량 탑재 소프트웨어의 향상으로 하드웨어의 상당한 재설계를 필요로 하지 않고 기존 차량 카테고리가 고급 예측 기능의 혜택을 누릴 수 있게 되었습니다.

미국의 자동차 분야에서 생성형 AI 시장은 2024년에 1억 4,880만 달러를 창출했습니다. 미국은 강력한 혁신 환경, 방대한 연구개발 능력, 학술기관, 기술공급자, 정부기관에 걸친 협력적인 노력으로 계속 주도적인 지위를 차지하고 있습니다. 생성형 AI의 통합은 차량 시스템과 이를 지원하는 디지털 인프라 모두에서 빠르게 진행되고 있습니다. 이러한 요인들로 인해 미국은 특히 실시간 운전 인텔리전스 강화, 차량 설계 프로세스의 간소화, 스마트 모빌리티 솔루션의 촉진에 있어서 생성형 AI 솔루션의 개발과 채용의 주요 거점으로 자리매김하고 있습니다.

세계 자동차 분야에서 생성형 AI 시장을 적극적으로 형성하는 주요 기업으로는 NVIDIA, Amazon Web Services(AWS), Bosch, Microsoft, Qualcomm, Aptiv, IBM, Continental, Intel, Google 등이 있습니다. 자동차 분야에서 생산 AI 시장에서 경쟁력을 유지하기 위해 주요 기업은 전략적 제휴, 기술 혁신, 시장 개척에 주력하고 있습니다. 각 회사는 자동차 제조업체와 Tier 1 공급업체와 장기적인 파트너십을 맺어 차량 시스템 전반에 걸쳐 AI의 원활한 통합을 보장합니다. 고급 시뮬레이션 툴, 실시간 데이터 처리 및 에지 AI 컴퓨팅에 대한 투자는 각 회사의 성장 접근 방식의 핵심이 되었습니다. 또한 주요 기업들은 SDK와 API를 통해 소프트웨어 생태계를 확대하여 개발자가 AI를 탑재한 용도를 신속하게 구축할 수 있도록 하고 있습니다.

목차

제1장 조사 방법

- 시장의 범위와 정의

- 조사 디자인

- 조사 접근

- 데이터 수집 방법

- 데이터 마이닝 소스

- 세계

- 지역/국가

- 기본 추정과 계산

- 기준연도 계산

- 시장 예측의 주요 동향

- 1차 조사와 검증

- 1차 정보

- 예측 모델

- 조사의 전제와 한계

제2장 주요 요약

제3장 업계 인사이트

- 업계 생태계 분석

- 공급자의 상황

- 이익률 분석

- 비용 구조

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 차량 설계와 ADAS에서의 AI 통합

- 전기자동차와 커넥티드카의 보급 확대

- 클라우드와 엣지 AI 도입

- OEM과 기술 기업의 협업

- 멀티모달 AI의 진보

- 업계의 잠재적 리스크 및 과제

- 데이터 프라이버시와 사이버 보안

- 레거시 시스템과의 통합

- 시장 기회

- 소프트웨어 정의 차량과 자율 운전 차량의 확대

- 학술기관 및 연구기관과의 제휴

- 아시아태평양 및 라틴아메리카의 신흥 시장

- 이동성 서비스와의 통합

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 코스트 내역 분석

- 특허 분석

- 지속가능성과 환경 측면

- 지속가능한 관행

- 폐기물 감축 전략

- 생산에서의 에너지 효율

- 환경 친화적인 노력

- 탄소발자국 고려

- 이용 사례와 용도

- 차량 설계 및 엔지니어링 용도

- 제조 및 생산 용도

- 자율주행 및 ADAS 용도

- 고객 경험과 서비스 용도

- 최상의 시나리오

- 기술과 혁신의 상황

- 현재의 기술 동향

- 신흥기술

- 생성형 AI 기술의 기반과 진화

- 생성형 AI 기술의 아키텍처와 기능

- AI 모델 개발 및 트레이닝 인프라

- 자동차용 AI 모델 개발

- 기술의 진화와 미래의 로드맵

- 미래의 기술 로드맵과 혁신의 타임라인

- 생성형 AI 기술의 진화(2024-2034년)

- 자동차용 AI 애플리케이션 개발 타임라인

- 기술의 융합과 통합의 시나리오

- 파괴적 기술의 평가와 시장에 대한 영향

- 자동차 업계의 디지털 변혁의 맥락

- 자동차 업계의 기술 혁신의 상황

- 디지털 트윈과 시뮬레이션 기술의 통합

- 데이터 기반 의사결정 및 분석

- 자동차 소프트웨어 및 플랫폼 에코시스템

- 규제 환경과 표준의 틀

- AI 거버넌스와 규제 상황

- 자동차 안전기준과 AI의 통합

- 국제표준과 조화의 대처

- 윤리적인 AI와 책임있는 개발 프레임워크

- 투자 상황과 자금 조달 분석

- 세계의 AI 투자 동향과 자동차 산업에 대한 주목

- 자동차 업계의 AI 투자 패턴

- 지역의 투자정세와 정부의 지원

- 스타트업 에코시스템과 혁신 허브

- 사이버 보안 및 리스크 관리 프레임워크

- AI 보안 위협 및 취약성 평가

- 자동차 사이버 보안과 AI 통합

- 설계 및 개발 실천에 의한 보안

- 규정 준수 및 규제 보안 요구 사항

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

- 주요 발전

- 인수합병

- 파트너십 및 협업

- 신제품 발매

- 확장계획과 자금조달

제5장 시장 추계 및 예측 : 차량별, 2021-2034년

- 승용차

- 해치백

- 세단

- SUV

- MPV

- 전기승용차

- 상용차

- 소형 상용차

- 대형 상용차

제6장 시장 추계 및 예측 : 추진력별, 2021-2034년

- 주요 동향

- ICE

- BEV

- PHEV

제7장 시장 추계 및 예측 : 기술별, 2021-2034년

- 주요 동향

- 대규모 언어 모델(LLM) 및 NLP

- 컴퓨터 비전 및 이미지 생성

- 멀티모달 AI 및 크로스 도메인 통합

- 생성형 AI 플랫폼 및 툴

- 기타

제8장 시장 추계 및 예측 : 용도별, 2021-2034년

- 주요 동향

- 자율주행 및 ADAS 용도

- 차량 설계 및 엔지니어링

- 제조 및 생산 최적화

- 고객 경험 및 개인화

- 공급망 및 물류 최적화

- 기타

제9장 시장 추계 및 예측 : 최종 용도별, 2021-2034년

- 주요 동향

- OEM

- Tier 1 자동차 부품 공급업체

- 자동차 소프트웨어 및 기술 기업

- 이동성 서비스 제공업체 및 함대 운영자

제10장 시장 추계 및 예측 : 지역별, 2021-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 북유럽 국가

- 러시아

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 동남아시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제11장 기업 프로파일

- Global Technology Leaders

- Amazon Web Services(AWS)

- IBM

- Intel

- Microsoft

- NVIDIA

- OpenAI

- Qualcomm

- Automotive Technology Specialists

- Aptiv

- Bosch

- Continental

- DENSO

- Magna International

- Mobileye

- Valeo

- Waymo

- ZF Friedrichshafen

- Emerging AI Specialists and Startups

- Argo AI

- Aurora Innovation

- Cruise

- DeepRoute.ai

- Einride

- Ghost Autonomy

- Innoviz Technologies

- Motional

- Plus

- Pony.ai

- Scale AI

- WeRide

- Zoox

The Global Generative AI in Automotive Market was valued at USD 506.6 million in 2024 and is estimated to grow at a CAGR of 23.8% to reach USD 4.58 billion by 2034.

The industry is witnessing rapid transformation as automotive manufacturers increasingly integrate generative artificial intelligence to streamline autonomous systems, optimize design workflows, and simulate critical driving scenarios. Regulatory encouragement and supportive funding are fueling development across automakers, component suppliers, and mobility tech innovators. As digitalization deepens and vehicles become more intelligent and interconnected, generative AI is becoming central to vehicle development. It enables automakers to replicate rare or complex traffic events, drastically cutting the time and costs associated with safety verification. This advanced capability is creating new standards in simulation accuracy and contributing to faster development timelines. Automakers are now leveraging generative AI to enhance user interfaces, predict maintenance requirements, and fine-tune advanced driving assistance systems. As the automotive industry transitions to software-defined vehicles and connected platforms, AI is no longer an enhancement but a core enabler of next-gen mobility ecosystems. Collaborations between software firms and hardware developers are creating foundational infrastructure that supports seamless integration of AI across automotive environments.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $506.6 Million |

| Forecast Value | $4.58 Billion |

| CAGR | 23.8% |

In 2024, the passenger vehicle segment generated a 68% share driven by the widespread implementation of intelligent systems across vehicles. AI-enabled technologies are now deeply embedded in functions such as advanced infotainment, driver support features, and in-car safety systems. These tools are significantly elevating the driving experience by improving interaction through conversational interfaces, delivering personalized insights, and powering adaptive responses in real time. Automakers are focusing on AI tools that enhance safety and functionality, with features like proactive service notifications and context-aware driving suggestions. With ongoing enhancements in sensor technology and remote software updates, the application of generative AI in this segment is expected to rise steadily.

The internal combustion engine (ICE) vehicle segment is expected to grow at a CAGR of 14.8% from 2025 to 2034. While electric vehicle platforms are often at the forefront of technological adoption, ICE-powered cars are also integrating AI-driven systems to stay competitive. Automakers are upgrading existing ICE models with intelligent modules that support improved diagnostics, seamless connectivity, and immersive digital experiences. This evolution is being driven by the rising demand for smart functionality in premium ICE vehicles, where retrofitting with AI-based systems is now more accessible through over-the-air updates and scalable platform technologies. Enhanced onboard software allows traditional vehicle categories to benefit from advanced predictive capabilities without requiring major hardware redesigns.

United States Generative AI in Automotive Market generated USD 148.8 million in 2024. The US continues to hold a leadership position due to its strong innovation landscape, vast R&D capabilities, and collaborative efforts spanning academic institutions, technology providers, and government agencies. The integration of generative AI is advancing rapidly across both vehicle systems and the digital infrastructure supporting them. These factors position the US as a primary hub for the development and adoption of generative AI solutions, particularly in enhancing real-time driving intelligence, streamlining vehicle design processes, and facilitating smart mobility solutions.

Key players actively shaping Global Generative AI in Automotive Market include NVIDIA, Amazon Web Services (AWS), Bosch, Microsoft, Qualcomm, Aptiv, IBM, Continental, Intel, and Google. To maintain a competitive edge in the generative AI in automotive market, major players are focusing on strategic alliances, technological innovation, and platform development. Companies are forming long-term partnerships with automakers and tier-one suppliers to ensure seamless AI integration across vehicle systems. Investment in advanced simulation tools, real-time data processing, and edge AI computing is central to their growth approach. Key firms are also expanding their software ecosystems through SDKs and APIs, allowing developers to build AI-powered applications faster.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Vehicle

- 2.2.3 Propulsion

- 2.2.4 Technology

- 2.2.5 Application

- 2.2.6 End Use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 AI integration in vehicle design and ADAS

- 3.2.1.2 Increasing adoption of electric and connected vehicles

- 3.2.1.3 Cloud and edge AI deployment

- 3.2.1.4 OEM-tech company collaborations

- 3.2.1.5 Advancements in multimodal AI

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Data privacy and cybersecurity

- 3.2.2.2 Integration with legacy systems

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of software-defined and autonomous vehicles

- 3.2.3.2 Collaborations with academic and research institutes

- 3.2.3.3 Emerging markets in Asia-Pacific and Latin America

- 3.2.3.4 Integration with mobility services

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Cost breakdown analysis

- 3.8 Patent analysis

- 3.9 Sustainability and environmental aspects

- 3.9.1 Sustainable practices

- 3.9.2 Waste reduction strategies

- 3.9.3 Energy efficiency in production

- 3.9.4 Eco-friendly Initiatives

- 3.9.5 Carbon footprint considerations

- 3.10 Use cases and Applications

- 3.10.1 Vehicle design and engineering applications

- 3.10.2 Manufacturing and production applications

- 3.10.3 Autonomous driving and ADAS applications

- 3.10.4 Customer experience and service applications

- 3.11 Best-case scenario

- 3.12 Technology and Innovation landscape

- 3.12.1 Current technological trends

- 3.12.2 Emerging technologies

- 3.13 Generative AI technology foundation and evolution

- 3.13.1 Generative AI technology architecture and capabilities

- 3.13.2 Ai model development and training infrastructure

- 3.13.3 Automotive-specific AI model development

- 3.13.4 Technology evolution and future roadmap

- 3.14 Future technology roadmap and innovation timeline

- 3.14.1 Generative AI technology evolution (2024-2034)

- 3.14.2 Automotive AI application development timeline

- 3.14.3 Technology convergence and integration scenarios

- 3.14.4 Disruptive technology assessment and market impact

- 3.15 Automotive industry digital transformation context

- 3.15.1 Automotive industry technology disruption landscape

- 3.15.2 Digital twin and simulation technology integration

- 3.15.3 Data-driven decision making and analytics

- 3.15.4 Automotive software and platform ecosystem

- 3.16 Regulatory environment and standards framework

- 3.16.1 AI governance and regulatory landscape

- 3.16.2 Automotive safety standards and AI integration

- 3.16.3 International standards and harmonization efforts

- 3.16.4 Ethical AI and responsible development framework

- 3.17 Investment landscape and funding analysis

- 3.17.1 Global AI investment trends and automotive focus

- 3.17.2 Automotive industry AI investment patterns

- 3.17.3 Regional investment landscape and government support

- 3.17.4 Startup ecosystem and innovation hubs

- 3.18 Cybersecurity and risk management framework

- 3.18.1 AI security threats and vulnerability assessment

- 3.18.2 Automotive cybersecurity and AI integration

- 3.18.3 Security by design and development practices

- 3.18.4 Compliance and regulatory security requirements

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Mn)

- 5.1 Passenger vehicles

- 5.1.1 Hatchback

- 5.1.2 Sedan

- 5.1.3 SUV

- 5.1.4 MPV

- 5.1.5 Electric passenger cars

- 5.2 Commercial vehicles

- 5.2.1 Light commercial vehicles

- 5.2.2 Heavy commercial vehicles

Chapter 6 Market Estimates & Forecast, By Propulsion, 2021 - 2034 ($Mn)

- 6.1 Key trends

- 6.2 ICE

- 6.3 BEV

- 6.4 PHEV

Chapter 7 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Mn)

- 7.1 Key trends

- 7.2 Large language models (LLMs) and NLP

- 7.3 Computer vision and image generation

- 7.4 Multimodal AI and cross-domain integration

- 7.5 Generative AI platforms and tools

- 7.6 Others

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 ($Mn)

- 8.1 Key trends

- 8.2 Autonomous Driving and ADAS Applications

- 8.3 Vehicle Design and Engineering

- 8.4 Manufacturing and production optimization

- 8.5 Customer experience and personalization

- 8.6 Supply chain and logistics optimization

- 8.7 Others

Chapter 9 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Mn)

- 9.1 Key trends

- 9.2 OEM

- 9.3 Tier 1 automotive suppliers

- 9.4 Automotive software and technology companies

- 9.5 Mobility service providers and fleet operators

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Nordics

- 10.3.7 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Technology Leaders

- 11.1.1 Amazon Web Services (AWS)

- 11.1.2 Google

- 11.1.3 IBM

- 11.1.4 Intel

- 11.1.5 Microsoft

- 11.1.6 NVIDIA

- 11.1.7 OpenAI

- 11.1.8 Qualcomm

- 11.2 Automotive Technology Specialists

- 11.2.1 Aptiv

- 11.2.2 Bosch

- 11.2.3 Continental

- 11.2.4 DENSO

- 11.2.5 Magna International

- 11.2.6 Mobileye

- 11.2.7 Valeo

- 11.2.8 Waymo

- 11.2.9 ZF Friedrichshafen

- 11.3 Emerging AI Specialists and Startups

- 11.3.1 Argo AI

- 11.3.2 Aurora Innovation

- 11.3.3 Cruise

- 11.3.4 DeepRoute.ai

- 11.3.5 Einride

- 11.3.6 Ghost Autonomy

- 11.3.7 Innoviz Technologies

- 11.3.8 Motional

- 11.3.9 Plus

- 11.3.10 Pony.ai

- 11.3.11 Scale AI

- 11.3.12 WeRide

- 11.3.13 Zoox