|

시장보고서

상품코드

1822615

바이알 어댑터 시장 : 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Vial Adaptors Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

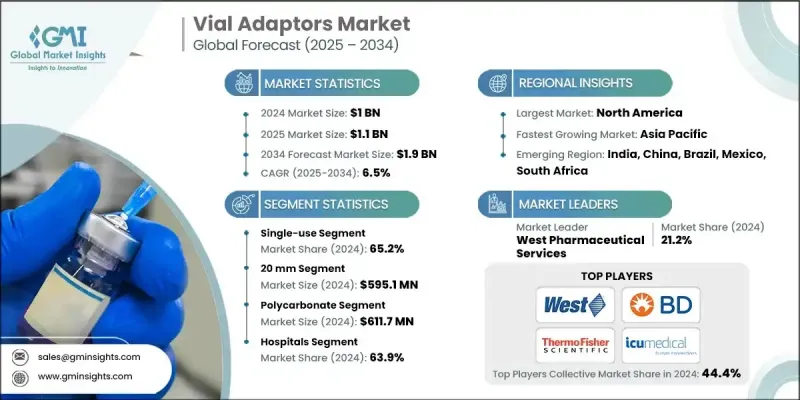

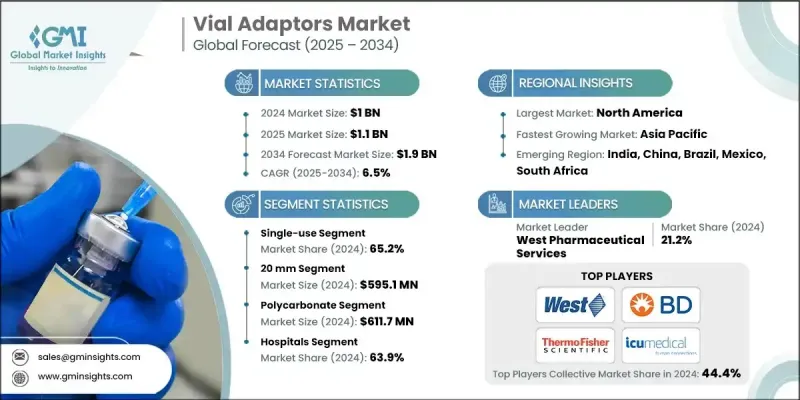

Global Market Insights, Inc.의 최신 보고서에 따르면 세계의 바이알 어댑터 시장은 2024년에 10억 달러로 평가되었으며, 2025년 11억 달러에서 2034년까지 19억 달러로 성장해 CAGR 6.5%를 보일 것으로 예측됩니다.

이 분야의 기세는 안전한 약물의 무균 재구성과 예방 접종, 병원 및 임상 환경에서 오염 위험을 줄이는 시장 요구에 의해 견인되고 있습니다.

바이알 어댑터는 특히 중요한 치료, 종양학, 백신 투여와 같은 중요한 환경에서 주사제의 이송 및 재구성 시 "바늘이 없는" 접근을 가능하게 함으로써 안전성과 효율성 향상에 기여합니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시장 매출 | 10억 달러 |

| 예측 금액 | 19억 달러 |

| CAGR | 6.5% |

주요 촉진요인

1. 생물제제 및 백신 사용 증가 : 생물학적 제제 증가 및 백신접종 프로그램 확대로 안전하고 효율적인 재구성에 대한 수요가 증가하고 있습니다.

2. 감염 예방 및 안전 문제 : 바이알 어댑터는 바늘 찌르기 사고와 미생물 오염을 방지하고 바늘이 없는 폐쇄 시스템으로 약물 전달을 제공합니다.

3. 병원 및 임상 워크플로우의 간소화 : 바이알 어댑터 제품은 약물 준비를 용이하게 하고 시간을 절약하고 약물 실수를 최소화합니다.

4. 폐쇄형 시스템 약물전달 장치(CSTD)에 대한 규제 뒷받침 : 항암제나 위험한 약물을 취급하기 위해 CSTD를 사용하는 것이 세계적으로 권장되며, 바이알 어댑터의 채용이 가속화되고 있습니다.

주요 기업

West Pharmaceutical Services, Thermo Fisher Scientific, Becton, Dickinson and Company, ICU Medical 등 주요 기업이 44.4%의 누적 시장 점유율을 차지하고 있습니다.

West는 국내 바이알 어댑터 공급업체의 톱으로, 2024년 시장 점유율은 21.2%였습니다.

주요 과제

- 확장성 : 일부 바이알 어댑터는 특정 바이알이나 제형에 적합하지 않기 때문에 종종 맞춤형 솔루션은 필연적으로 재고 노력의 복잡성을 초래합니다.

- 규모의 경제성/조달 : 초기 제품에 대한 투자와 현지 공급망이 없기 때문에 특히 자원에 제한이 있는 환경에서는 의료 시스템이 어댑터 솔루션을 채택하고 사용하는 능력이 제한될 수 있습니다.

- 폐기물 및 환경 문제 : 일회용 플라스틱 기반 어댑터는 의료 폐기물의 원인이 되었습니다. 재활용 가능한 재료 기반 어댑터를 개발할 가능성을 조사하는 제조업체도 있습니다.

1. 제품 유형별 - 일회용 바이알 어댑터 리드

일회용 바이알 어댑터는 2024년 시장 리더로 보다 우수한 감염 관리, 규제 준수, 병원 및 연구소의 임상 현장에서의 사용 편의성을 바탕으로 했습니다. 화학요법, 예방접종, 중증 환자용 약제조제에 우선적으로 사용되고 있습니다.

2. 사이즈-20mm 유니버설 용도용

20mm 크기는 종양학, 감염, 소아과 관련 치료 영역에 보편적인 적용 가능성을 제공합니다.

3.소재별 - 폴리카보네이트가 1위에 공헌

2024년에는 내구성, 내약품성, 바이알 어댑터에서 주사기로 약물 주입 시 육안 검사를 가능하게 하는 투명성을 바탕으로 폴리카보네이트 기반 바이알 어댑터가 선도하고 있습니다.

4. 최종 용도별 - 병원이 수요의 중심

병원은 2024년에도 바이알 어댑터의 주요 최종 용도입니다. 왜냐하면, 병원에서는 특히 종양과나 감염증과 등의 고환자수에 대응하기 위해, 무균이고 비용 효율적인 약제 투여 시스템이 필요하기 때문입니다.

5. 지역별-북미가 계속 우세

북미는 헬스케어 인프라와 고급 약물전달 시스템에 대한 왕성한 투자로 바이알 어댑터 세계 시장을 계속 지배하고 있습니다. 폐쇄형 약물 전달 장치(CSTD)의 사용과 감염 예방의 추진은 이 지역의 성장을 더욱 강화하고 있습니다. 북미는 만성 질환 증가, 건강 관리에 대한 고액 지출, 건전한 병원 인프라에 힘입어 2024년 바이알 어댑터 세계 시장을 석권했습니다. 이 지역에는 유명한 제약 회사와 생명 공학 회사도 많아 무균 제제에 바이알 어댑터의 채용을 더욱 뒷받침하고 있습니다. 미국은 백신 접종 증가, 프리필드 주사기 및 밀폐형 약물전달 시스템의 사용 확대로 계속해서 큰 공헌을 하고 있습니다.

주요 바이알 어댑터 시장 기업으로는 B. Braun, Baxter International, Becton, Dickinson and Company, West Pharmaceutical Services, Yukon Medical, Thermo Fisher Scientific, ICU Medical, Helapet, Epic Medical, CODAN Medizinische Gerate, Miltenyi Biotec, EQUASHIELD, VYGON 등이 있습니다.

시장 경쟁력을 유지하기 위해 시장 리더는 제품 혁신, 제휴 및 규제 당국의 허가에 베팅하고 있습니다. Becton, Dickinson and Company 및 Baxter International은 오염을 최소화하기 위해 바이알 어댑터를 주입 및 사전 충전 주사기 플랫폼에 통합합니다. 또한 각 회사는 다양한 병원의 필요와 약제의 형식을 충족하기 위해 지속 가능한 재료와 맞춤형 크기의 어댑터에 자금을 지출합니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 업계 생태계 분석

- 업계에 미치는 영향요인

- 성장 촉진요인

- 만성 질환 증가

- 바이알 어댑터의 장점에 대한 인식 증가

- 고령자 인구 증가

- 업계의 잠재적 리스크 및 과제

- 대체품의 이용가능성

- 시장 기회

- 바이오의약품 및 바이오시밀러의 확대

- 바늘을 사용하지 않는 약물전달 시스템 수요 증가

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 기술의 상황

- 현재의 기술 동향

- 신흥기술

- 가격 분석, 제품 유형별, 2024년

- 세계

- 일회용 바이알 어댑터

- 다목적 바이알 어댑터

- 북미

- 일회용 바이알 어댑터

- 다목적 바이알 어댑터

- 유럽

- 일회용 바이알 어댑터

- 다목적 바이알 어댑터

- 아시아태평양

- 일회용 바이알 어댑터

- 다목적 바이알 어댑터

- 라틴아메리카

- 일회용 바이알 어댑터

- 다목적 바이알 어댑터

- 중동 및 아프리카

- 일회용 바이알 어댑터

- 다목적 바이알 어댑터

- 갭 분석

- Porter's Five Forces 분석

- PESTEL 분석

- 미래 시장 동향

- 밸류체인 분석

제4장 경쟁 구도

- 소개

- 기업 매트릭스 분석

- 기업의 시장 점유율 분석

- 세계

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카, 중동 및 아프리카

- 경쟁 포지셔닝 매트릭스

- 주요 시장 기업의 경쟁 분석

- 주요 발전

- 인수합병

- 파트너십 및 협업

- 신제품 유형의 발매

- 확장 계획

제5장 시장 추계 및 예측 : 제품 유형별, 2021-2034년

- 주요 동향

- 일회용 바이알 어댑터

- 벤트 부착 바이알 어댑터

- 벤트 없음 바이알 어댑터

- 다목적 바이알 어댑터

- 벤트 부착 바이알 어댑터

- 벤트 없음 바이알 어댑터

제6장 시장 추계 및 예측 : 제품 사이즈별, 2021-2034년

- 주요 동향

- 13mm

- 20mm

- 기타 제품 사이즈

제7장 시장 추계 및 예측 : 재료별, 2021-2034년

- 주요 동향

- 폴리카보네이트

- 실리콘

- 폴리에틸렌

- 기타 재료

제8장 시장 추계 및 예측 : 최종 용도별, 2021-2034년

- 주요 동향

- 병원

- 외래수술센터(ASC)

- 기타 용도

제9장 시장 추계 및 예측 : 지역별, 2021-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제10장 기업 프로파일

- B. Braun

- Baxter International

- Becton, Dickinson and Company

- CODAN Medizinische Gerate

- Epic Medical

- EQUASHIELD

- Helapet

- ICU Medical

- Miltenyi Biotec

- Thermo Fisher Scientific

- VYGON

- West Pharmaceutical Services

- Yukon Medical

The global vial adaptors market was valued at USD 1 billion in 2024 and is projected to grow from USD 1.1 billion in 2025 to USD 1.9 billion by 2034, registering a CAGR of 6.5%, according to the latest report by Global Market Insights, Inc. The sector's momentum has been driven by market needs for safe drug sterile reconstitution and vaccinations, as well as a need to mitigate contamination risk in hospitals and clinical environments.

Vial adaptors help improve safety and efficiency by enabling 'needle-free' access when transferring and reconstituting injectable drugs, particularly in critical settings such as critical care, oncology, and vaccine administration.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1 Billion |

| Forecast Value | $1.9 Billion |

| CAGR | 6.5% |

Key Drivers:

1. Increasing use of biologics and vaccines: Increasing numbers of biologic drugs and expanding vaccination programs have increased demand for safe and efficient reconstitution.

2. Infection prevention and safety issues: Vial adaptors provide needle-free, closed-system medication delivery, preventing needlestick accidents and microbial contamination.

3. Streamlining hospital and clinical workflow: These products make drug preparation easier, saving time and minimizing drug errors.

4. Regulatory push to close-system transfer devices (CSTDs): Global recommendations for using CSTDs for cancer and hazardous drug handling are accelerating vial adaptor adoption.

Key Players:

Major players like West Pharmaceutical Services, Thermo Fisher Scientific, Becton, Dickinson and Company, and ICU Medical hold a cumulative market share of 44.4%.

West is the leading domestic vial adaptor supplier with 21.2% market share in 2024.

Key Challenges:

- Scalability:;As some vial adaptors may not fit any particular vial or drug formulation, in many instances, custom solutions would necessarily lead to complexities in inventory efforts.

- Economies of scale/Procurement:;Initial product investments and no local supply chains may limit the medical system's ability to adopt and use adaptor solutions, especially in resource constrained environments.

- Waste and environmental agenda:;The single-use plastic based adaptors contribute to medical waste.;Some manufacturers are investigating the potential to develop recyclable material-based adaptors.;

1. By Product Type - Single-Use Vial Adaptors Lead

Single-use vial adaptors were the market leader in 2024 due to their better infection control, regulatory compliance, and ease of use in hospitals and laboratory clinical settings. They are used in preference in chemotherapy, immunization, and critical care drug preparation.

2. Size - 20mm For Universal Application

A 20mm size offers universal applicability to therapy areas related to oncology, infectious diseases, and pediatrics.

3. Based on Material - Polycarbonate Contributes to 1ST Position

In 2024, polycarbonate based vial adaptors lead the way, based upon durability, chemical resistance, and transparency permitting visual inspection during the transfer of the drug from the vial adapter to the syringe.

4. By End Use - Hospitals Power Core Demand

Hospitals continued to be the major End Uses of vial adaptors in 2024, since such facilities need aseptic, cost-effective drug administration systems to meet high patient loads, particularly in oncology and infectious disease departments.

5. By Region - North America Continues to Dominate

North America continued to dominate the global market for vial adaptors with strong investments in healthcare infrastructure and advanced drug delivery systems. The usage of closed-system transfer devices (CSTDs) and promotion of infection prevention practices additionally enhance regional growth. North America dominated the world vial adaptors market in 2024, aided by increasing numbers of chronic diseases, high expenditure on healthcare, and sound hospital infrastructure. The region is also home to a number of prominent pharmaceutical and biotechnology companies, further driving the adoption of vial adaptors in sterile drug preparation. The US continues to be a dominant contributor because of growing vaccination efforts and extensive use of prefilled syringes and closed drug delivery systems.

Some of the major vial adaptors market players are B. Braun, Baxter International, Becton, Dickinson and Company, West Pharmaceutical Services, Yukon Medical, Thermo Fisher Scientific, ICU Medical, Helapet, Epic Medical, CODAN Medizinische Gerate, Miltenyi Biotec, EQUASHIELD, and VYGON.

Market leaders are placing bets on product innovation, collaborations, and regulatory clearances to remain competitive. An example of this is West Pharmaceutical Services, which continues to expand its portfolio of vial adaptors to facilitate safe reconstitution of biologics.;Becton, Dickinson and Company and Baxter International are incorporating vial adaptors into their infusion and prefilled syringe platforms to minimize contamination. Also, companies are spending money on sustainable materials/ adaptors of custom sizes to satisfy different hospital needs and drug formats.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product type trends

- 2.2.3 Product size trends

- 2.2.4 Material trends

- 2.2.5 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing prevalence of chronic conditions

- 3.2.1.2 Rise in awareness regarding advantages of the vial adaptors

- 3.2.1.3 Increase in geriatric population

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Availability of substitutes

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of biologics and biosimilars

- 3.2.3.2 Growing demand for needle-free drug delivery systems

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 MEA

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Global vial adaptor market, by volume (Units), 2021 - 2034

- 3.6.1 Pricing analysis, By product type, 2024

- 3.6.2 Global

- 3.6.2.1 Single-use vial adaptors

- 3.6.2.2 Multi-use vial adaptors

- 3.6.3 North America

- 3.6.3.1 Single-use vial adaptors

- 3.6.3.2 Multi-use vial adaptors

- 3.6.4 Europe

- 3.6.4.1 Single-use vial adaptors

- 3.6.4.2 Multi-use vial adaptors

- 3.6.5 Asia Pacific

- 3.6.5.1 Single-use vial adaptors

- 3.6.5.2 Multi-use vial adaptors

- 3.6.6 Latin America

- 3.6.6.1 Single-use vial adaptors

- 3.6.6.2 Multi-use vial adaptors

- 3.6.7 MEA

- 3.6.7.1 Single-use vial adaptors

- 3.6.7.2 Multi-use vial adaptors

- 3.7 Gap analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Future market trends

- 3.11 Value chain analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.3.5 LAMEA

- 4.4 Competitive positioning matrix

- 4.5 Competitive analysis of major market players

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product type launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Single-use vial adaptors

- 5.2.1 Vented vial adaptors

- 5.2.2 Non-vented vial adaptors

- 5.3 Multi-use vial adaptors

- 5.3.1 Vented vial adaptors

- 5.3.2 Non-vented vial adaptors

Chapter 6 Market Estimates and Forecast, By Product Size, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 13 mm

- 6.3 20 mm

- 6.4 Other product sizes

Chapter 7 Market Estimates and Forecast, By Material, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Polycarbonate

- 7.3 Silicone

- 7.4 Polyethylene

- 7.5 Other materials

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals

- 8.3 Ambulatory surgical centers

- 8.4 Other end use

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 B. Braun

- 10.2 Baxter International

- 10.3 Becton, Dickinson and Company

- 10.4 CODAN Medizinische Gerate

- 10.5 Epic Medical

- 10.6 EQUASHIELD

- 10.7 Helapet

- 10.8 ICU Medical

- 10.9 Miltenyi Biotec

- 10.10 Thermo Fisher Scientific

- 10.11 VYGON

- 10.12 West Pharmaceutical Services

- 10.13 Yukon Medical