|

시장보고서

상품코드

1822650

대체 단백질 시장 : 기회, 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Alternative Proteins Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

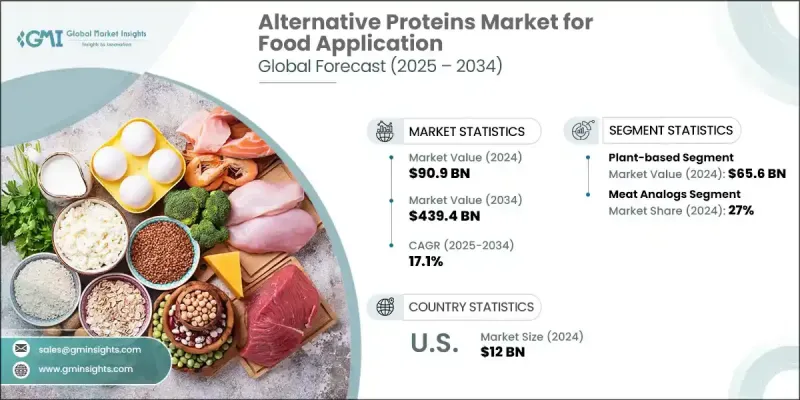

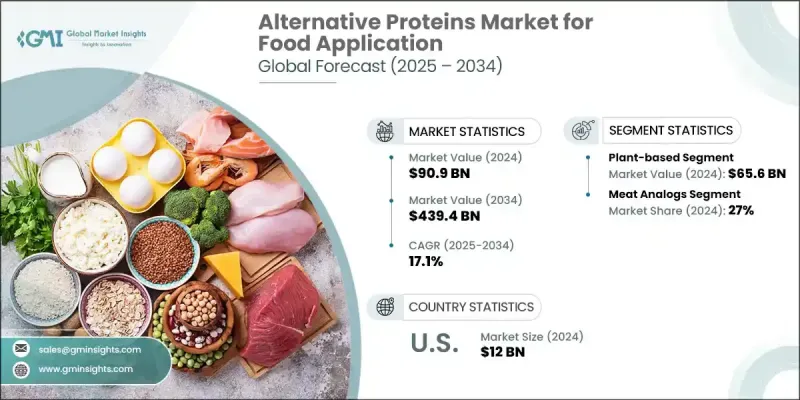

식품 용도의 세계의 대체 단백질 시장은 2024년에 909억 달러로 평가되고 환경 지속가능성에 대한 의식에 힘입어 CAGR은 17.1%를 나타낼 것으로 예측되며 2034년에 4,394억 달러로 성장할 전망입니다. 소비자들이 친환경적인 라이프스타일을 선택함에 따라 생태 발자국이 낮은 단백질 원들을 찾고 있습니다. 또한 건강과 식단에 대한 우려로 인해 더 건강하고 만성 질환을 유발할 가능성이 낮은 것으로 인식되는 식물성 및 실험실 배양 단백질로의 전환이 촉진되고 있습니다. 국제식품정보위원회(IFIC)가 2023년 실시한 설문조사에 따르면, 미국인의 절반 이상(57%)이 대체 단백질을 시도한 경험이 있으며, 식물성 갈은 소고기(31%)가 가장 흔했고, 소고기 대체품(23%), 식물성 소시지(22%), 식물성 닭고기 대체품(22%)이 그 뒤를 이었습니다.

또한 식품 생산 기술의 기술적 발전으로 대체 단백질의 접근성과 비용 효율성이 높아지면서 시장 확대가 가속화되고 있습니다. 대체 단백질 시장은 원, 적용 분야, 지역별로 분류됩니다. 연구 기간 동안 곤충 기반 부문은 자원 활용 효율성에 촉진되어 상당한 성장률을 기록될 것입니다. 곤충은 기존 가축보다 훨씬 적은 토지, 물, 사료가 필요해 매우 지속 가능한 단백질 공급원입니다. 또한 곤충은 사료 전환율이 높고 빠르게 사육할 수 있어 확장 가능하고 회복력 있는 식품 시스템에 대한 증가하는 수요와 부합합니다. 지속가능성에 대한 우려가 커지고 소비자들이 혁신적인 단백질 공급원을 찾는 가운데, 곤충 기반 옵션은 전 세계 식량 안보 문제를 해결할 잠재력으로 환경적 영향을 최소화하면서 주목받고 있습니다. 가축 사료 용도 부문은 축산업 내에서 지속가능한 단백질 공급원의 채택으로 인해 2032년까지 대체 단백질 시장에서 상당한 점유율을 차지할 것입니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시장 규모 | 909억 달러 |

| 예측 금액 | 4,394억 달러 |

| CAGR | 17.1% |

축산물 수요가 증가함에 따라 농가들은 기존 사료를 보완할 수 있는 대체 단백질을 탐구하고 있습니다. 이러한 변화는 사료 효율성을 향상시키고 기존 사료 원료와 관련된 환경적 발자국을 감축하려는 요구에서 비롯됩니다. 대체 단백질을 동물 사료에 통합함으로써 생산자들은 전반적인 자원 활용도를 개선하고 사료 부족 문제를 해결할 수 있습니다. 유럽 대체 단백질 시장은 지속가능하고 윤리적인 식품 선택에 대한 소비자의 강력한 수요에 의해 촉진되어 2032년까지 강력한 성장 동향을 보일 것입니다. 기존 단백질 원료의 환경적 영향에 대한 인식이 높아지면서 유럽 소비자들은 더욱 친환경적인 대안을 찾고 있습니다. 또한 식품 생산의 지속가능성을 촉진하는 엄격한 규제와 정부 인센티브가 시장 성장을 부추기고 있습니다. 건강을 중시하는 식습관의 확산과 식품 기술 혁신은 대체 단백질의 매력을 더욱 강화하여 해당 지역 내 업계 업체들에게 수익성 높은 기회를 창출하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 업계의 잠재적 위험 및 과제

- 시장 기회

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 기술과 혁신 상황

- 현재 기술 동향

- 신흥 기술

- 가격 동향

- 지역별

- 장래 시장 동향

- 기술과 혁신 상황

- 현재 기술 동향

- 신흥 기술

- 특허 상황

- 무역 통계(HS코드)(주 : 무역 통계는 주요 국가만 제공)

- 주요 수입국

- 주요 수출국

- 지속가능성과 환경 측면

- 지속가능한 관행

- 폐기물 감축 전략

- 생산 과정의 에너지 효율성

- 환경 친화적인 노력

- 탄소발자국의 고려

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병과 인수

- 파트너십 및 협업

- 신제품 발매

- 확장 계획

제5장 시장 추계 및 예측 : 출처별(2021-2034년)

- 주요 동향

- 식물 기반

- 대두 단백질 분리물

- 대두 단백질 농축물

- 발효 대두 단백질

- 개구리밥 단백질

- 기타

- 곤충 기반

- 미생물 기반

- 박테리아

- 효모

- 조류

- 기타

제6장 시장 추계 및 예측 : 용도별(2021-2034년)

- 주요 동향

- 육류 대체품

- 베이커리

- 대체 유제품

- 시리얼 및 스낵

- 음료

- 기타

제7장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 기타 라틴아메리카

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

제8장 기업 프로파일

- Archer Daniels Midland Company

- Cargill Inc.

- Ingredion Inc.

- Kerry Group

- Impossible Foods Inc.

- The Scoular Company

- DSM NV

- Lightlife Foods, Inc.

- Impossible Foods Inc.

- International Flavors &Fragrances, Inc.

- Glanbia plc

- Bunge Limited

- Axiom Foods Inc.

Global Alternative Protein Market for food application was valued at USD 90.9 billion in 2024 and is estimated to grow at a CAGR of 17.1% to reach USD 439.4 billion by 2034, driven by the awareness of environmental sustainability. As consumers opt for an eco-friendly lifestyle, they are seeking protein sources with a lower ecological footprint. Additionally, concerns over health and diet are prompting a shift towards plant-based and lab-grown proteins, which are perceived as healthier and less likely to cause chronic diseases. According to a survey conducted by the International Food Information Council in 2023, over half (57%) of Americans have tried alternative proteins, with plant-based ground beef being the most common at 31%, followed by beef alternatives at 23%, plant-based sausage at 22%, and plant-based chicken alternatives at 22%.

Further, technological advancements in food production are making alternative proteins more accessible and cost-effective, accelerating market expansion. The alternative protein market is classified based on source, application, and region. The insect-based segment will record a significant growth rate over the study period, driven by its efficiency in resource utilization. Insects require significantly less land, water, and feed than traditional livestock, making them a highly sustainable protein source. Additionally, insects have a high feed conversion rate and can be cultivated quickly, which aligns with the growing need for scalable and resilient food systems. As sustainability concerns mount and consumers seek innovative protein sources, insect-based options are gaining traction due to their potential to address global food security challenges while minimizing environmental impact. The animal feed application segment will clutch a noticeable alternative protein market share by 2032, owing to the adoption of sustainable protein sources within the livestock industry.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $90.9 Billion |

| Forecast Value | $439.4 Billion |

| CAGR | 17.1% |

As the demand for livestock products increases, farmers are exploring alternative proteins that can supplement traditional feed. This shift is motivated by the desire to enhance feed efficiency and reduce the environmental footprint associated with conventional feed ingredients. By integrating alternative proteins into animal feed, producers can improve overall resource utilization and address the challenges of feed scarcity. Europe alternative protein market will demonstrate a strong growth trend through 2032, driven by robust consumer demand for sustainable and ethical food choices. The increasing awareness of the environmental impact of traditional protein sources has led European consumers to seek more eco-friendly alternatives. Additionally, stringent regulations and government incentives promoting sustainability in food production are fueling market growth. The rise in health-conscious eating and innovations in food technology further bolster the appeal of alternative proteins, creating lucrative opportunities for the industry players across the region.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Source trends

- 2.2.2 Application trends

- 2.2.3 Regional

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.9 Future market trends

- 3.10 Technology and Innovation landscape

- 3.10.1 Current technological trends

- 3.10.2 Emerging technologies

- 3.11 Patent Landscape

- 3.12 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.12.1 Major importing countries

- 3.12.2 Major exporting countries

- 3.13 Sustainability and environmental aspects

- 3.13.1 Sustainable practices

- 3.13.2 Waste reduction strategies

- 3.13.3 Energy efficiency in production

- 3.13.4 Eco-friendly initiatives

- 3.14 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Source, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Plant-based

- 5.2.1 Soy Protein Isolates

- 5.2.2 Soy Protein Concentrates

- 5.2.3 Fermented Soy Protein

- 5.2.4 Duckweed Protein

- 5.2.5 Others

- 5.3 Insect-based

- 5.4 Microbial-based

- 5.4.1 Bacteria

- 5.4.2 Yeast

- 5.4.3 Algae

- 5.4.4 Others

Chapter 6 Market Estimates and Forecast, By Application, 2021-2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Meat analogs

- 6.3 Bakery

- 6.4 Dairy alternatives

- 6.5 Cereals & snacks

- 6.6 Beverages

- 6.7 Others

Chapter 7 Market Estimates and Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Rest of Europe

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.4.6 Rest of Asia Pacific

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.5.4 Rest of Latin America

- 7.6 Middle East and Africa

- 7.6.1 Saudi Arabia

- 7.6.2 South Africa

- 7.6.3 UAE

- 7.6.4 Rest of Middle East and Africa

Chapter 8 Company Profiles

- 8.1 Archer Daniels Midland Company

- 8.2 Cargill Inc.

- 8.3 Ingredion Inc.

- 8.4 Kerry Group

- 8.5 Impossible Foods Inc.

- 8.6 The Scoular Company

- 8.7 DSM NV

- 8.8 Lightlife Foods, Inc.

- 8.9 Impossible Foods Inc.

- 8.10 International Flavors & Fragrances, Inc.

- 8.11 Glanbia plc

- 8.12 Bunge Limited

- 8.13 Axiom Foods Inc.