|

시장보고서

상품코드

1833654

원격의료 시장 : 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Telehealth Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

세계의 원격의료 시장 규모는 2024년에 1,261억 달러로 평가되었고, CAGR 12.4%로 성장할 전망이며, 2034년에는 4,032억 달러에 이를 것으로 예측됩니다.

급증하는 배경은 특히 도시 지역과 선진 지역에서 원격 헬스케어에 대한 선호도를 높일 수 있으며, 환자는 편의성과 접근성이 뛰어나 가상 관리에 대한 의존성을 강화하고 있습니다. 디지털 헬스 솔루션의 채택은 지속적인 모니터링과 환자와의 참여를 강화할 수 있는 모바일 헬스 용도 및 웨어러블 기술의 혁신에 의해 더욱 강화되고 있습니다. 원격의료 고급 통신 플랫폼을 통해 의료 서비스를 제공하여 원격지에서의 진단, 모니터링, 진단 및 환자 지원을 가능하게 합니다. 이 시장에는 하드웨어, 소프트웨어 및 통합 솔루션이 포함되어 있으며 환자와 헬스케어 제공업체를 모두 지원하는 완벽한 생태계가 구축되었습니다. 성장을 형성하는 주요 동향은 진단 정확도를 향상시키고 개인화된 가상 케어를 강화하는 인공지능과 머신러닝의 이용을 포함합니다. 포도당 수치와 호흡 활동과 같은 환자 데이터를 분석함으로써, 머신러닝 알고리즘은 의사에게 필수적인 의사 결정 지원 시스템으로 작용합니다. 이러한 요인들이 결합되어 헬스케어의 제공 방법과 액세스 방법이 세계적으로 변화되고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시장 규모 | 1,261억 달러 |

| 예측 금액 | 4,032억 달러 |

| CAGR | 12.4% |

서비스 분야는 2024년에 479억 달러를 창출했습니다. 이 범주에는 원격 환자 모니터링, 비디오 또는 음성 컨설팅, 실시간 상호작용, 스토어 앤 포워드 서비스 및 기타 가상 케어 형식이 포함됩니다. 접근성이 뛰어나고 비용 효율적이고 확장 가능한 원격의료 옵션에 대한 수요가 증가함에 따라, 특히 공급업체가 서비스가 미치지 못하는 지역으로 서비스를 확장함에 따라 이 분야의 성장에 박차를 가하고 있습니다. 원격의료 서비스의 편의성과 일상적인 헬스케어 루틴으로의 통합으로 이 분야는 계속 시장 수익의 핵심이 되고 있습니다.

웹 및 클라우드 기반 플랫폼은 2024년에 70%의 점유율을 차지했습니다. 이러한 플랫폼의 매력은 유연성, 인프라 필요성이 낮고 스케일링이 용이합니다. 이러한 플랫폼은 의료 전문가가 효율적으로 원격의료 서비스를 제공할 수 있게 하는 동시에 전자 의료진과 통합하여 협력과 성과를 향상시킵니다. 또한 클라우드 기반 시스템은 기존 서비스를 중단하지 않고도 원활한 업데이트와 고급 기능을 구현할 수 있으므로 기존 온프레미스 솔루션보다 선호되는 모델로 자리매김하고 있습니다.

북미의 원격의료 시장은 2024년에 48%의 점유율을 차지했으며, 원격의료의 세계 리더로서 지위를 굳혔습니다. 견고한 헬스케어 인프라, 인터넷의 보급, 디지털 헬스 도입의 고수준 등의 요인이 동 시장의 존재감을 높이고 있습니다. 정부 지원 조치, 의료 기술에 대한 투자 증가, 주요 원격의료 제공업체의 존재가 이 지역의 성장을 더욱 강화하고 있습니다. 게다가 만성 질환의 유병률 증가와 지속적인 원격 모니터링에 대한 수요 증가는 세계의 원격의료 시장에서 북미의 우위를 강화하고 있습니다.

세계의 원격의료 산업에서 활약하는 주요 기업은 Teladoc Health, Cisco Systems, Doximity, Athenahealth, Medtronic, Amwell, Siemens, McKesson Medical-Surgical, Omnia TeleHealth, AMD, Access TeleCare, Sesame, LifeStance Health, Health Catalyst, Telihealth、Doxy.me、Henry Schein、Apollo TeleHealth、Capsa Healthcare、Koninklijke Philips、Veradigm(Allscripts)、Eagle Telemedicine 등이 있습니다. 원격의료 시장에서 경쟁하는 기업들은 확장성, 접근성, 기존 헬스케어 시스템과의 통합을 강화하는 전략에 주력하고 있습니다. 많은 의료 제공업체는 임상 정확성을 향상시키고, 관리를 개별화하며, 워크플로우 관리를 간소화하기 위해 인공지능 및 예측 분석에 많은 투자를 하고 있습니다. 전자 의료진과의 상호 운용성을 추진하고 기밀성이 높은 의료 데이터를 보호하기 위한 사이버 보안 강화에 주력하고 있습니다.

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 업계에 미치는 영향요인

- 성장 촉진요인

- 만성 질환과 고령화의 만연에 의해 원격 헬스케어 수요 증가

- 디지털 헬스 기술의 진보

- 웨어러블 디바이스 및 커넥티드 디바이스의 보급 증가

- 정부의 대처 및 상환 정책

- 업계의 잠재적 위험 및 과제

- 데이터 프라이버시 및 보안에 대한 우려

- 개발도상 지역에서의 한정된 인터넷 접속

- 시장 기회

- 신흥 시장에서의 디지털 헬스에 대한 액세스 확대

- 하이브리드 헬스케어 모델의 침투

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 투자 및 자금 조달의 상황

- 원격의료 프로젝트 및이니셔티브

- 환급 시나리오

- 기술적 상황

- 신흥 기술

- 현재의 기술

- 장래 시장 동향

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서문

- 기업 매트릭스 분석

- 기업의 시장 점유율 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병 및 인수

- 파트너십 및 협업

- 신제품 발매

- 확장 계획

제5장 시장 추계 및 예측 : 컴포넌트별(2021-2034년)

- 주요 동향

- 하드웨어

- 소프트웨어

- 서비스

- 원격 환자 모니터링

- 실시간 인터랙션

- 저장 및 전송

- 비디오 및오디오 상담

- 기타 서비스 유형

제6장 시장 추계 및 예측 : 배송 방법별(2021-2034년)

- 주요 동향

- 웹 및 클라우드 기반

- 온프레미스

제7장 시장 추계 및 예측 : 전문 분야별(2021-2034년)

- 주요 동향

- 피부과

- 정신 건강

- 심장병학

- 신경학

- 정형외과

- 부인과

- 기타 전문 분야

제8장 시장 추계 및 예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 의료 제공자

- 병원 및 진료소

- 장기 케어 센터

- 기타 의료 제공자

- 지불자

- 환자

제9장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 네덜란드

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제10장 기업 프로파일

- Access TeleCare

- AMD

- American Well

- Apollo TeleHealth

- Athenahealth

- Capsa Healthcare

- Cisco Systems

- Doxy.me

- Doximity

- Eagle Telemedicine

- Health Catalyst

- Henry Schein

- Koninklijke Philips

- LifeStance Health

- McKesson Medical-Surgical

- Medtronic

- Omnia TeleHealth

- Sesame

- Siemens

- Teladoc Health

- Tellihealth

- Veradigm(Allscripts)

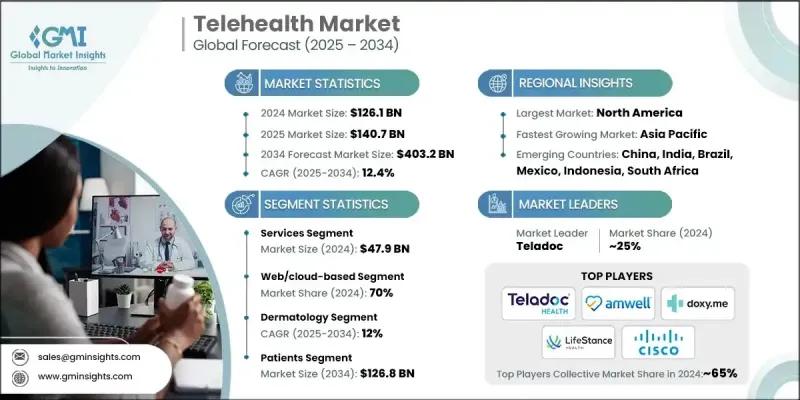

The Global Telehealth Market was valued at USD 126.1 billion in 2024 and is estimated to grow at a CAGR of 12.4% to reach USD 403.2 billion by 2034.

The rapid expansion is attributed to the growing preference for remote healthcare, particularly in urban and developed regions where patients increasingly rely on virtual care for convenience and accessibility. The adoption of digital health solutions is further enhanced by innovations in mobile health applications and wearable technologies, which allow continuous monitoring and stronger patient engagement. Telehealth involves the provision of healthcare services through advanced telecommunication platforms, enabling consultations, monitoring, diagnosis, and patient support remotely. The market encompasses hardware, software, and integrated solutions, creating a complete ecosystem that supports both patients and healthcare providers. Key trends shaping growth include the use of artificial intelligence and machine learning, which improve diagnostic precision and enhance personalized virtual care. By analyzing patient data such as glucose levels or respiratory activity, machine learning algorithms serve as vital decision-support systems for physicians. Together, these factors are transforming the way healthcare is delivered and accessed on a global scale.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $126.1 Billion |

| Forecast Value | $403.2 Billion |

| CAGR | 12.4% |

The services segment generated USD 47.9 billion in 2024. This category includes remote patient monitoring, video or audio consultations, real-time interactions, store-and-forward services, and other virtual care formats. Increasing demand for accessible, cost-efficient, and scalable remote healthcare options is fueling segment growth, particularly as providers expand services into underserved regions. The convenience of telehealth services and their integration into daily healthcare routines ensure this segment remains the backbone of market revenues.

The web and cloud-based platforms held a 70% share in 2024. Their appeal lies in flexibility, lower infrastructure needs, and ease of scaling. These platforms enable healthcare professionals to deliver telehealth services efficiently while integrating with electronic health records for improved coordination and outcomes. Cloud-based systems also allow seamless updates and advanced features without interrupting existing services, positioning them as the preferred model over traditional on-premises solutions.

North America Telehealth Market held a 48% share in 2024, cementing its position as a global leader in telehealth. Factors such as robust healthcare infrastructure, widespread internet penetration, and a high level of digital health adoption have strengthened its market presence. Supportive government measures, rising investments in healthcare technology, and the presence of leading telehealth providers further fuel growth in the region. Additionally, the increasing prevalence of chronic conditions and the rising demand for continuous remote monitoring reinforce North America's dominance in the global telehealth landscape.

Key players active in the Global Telehealth Industry include Teladoc Health, Cisco Systems, Doximity, Athenahealth, Medtronic, Amwell, Siemens, McKesson Medical-Surgical, Omnia TeleHealth, AMD, Access TeleCare, Sesame, LifeStance Health, Health Catalyst, Tellihealth, Doxy.me, Henry Schein, Apollo TeleHealth, Capsa Healthcare, Koninklijke Philips, Veradigm (Allscripts), and Eagle Telemedicine. Companies competing in the telehealth market are focusing on strategies that enhance scalability, accessibility, and integration with existing healthcare systems. Many providers are investing heavily in artificial intelligence and predictive analytics to improve clinical accuracy, personalize care, and streamline workflow management. Advancing interoperability with electronic health records and focusing on cybersecurity enhancements to safeguard sensitive medical data.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Component trends

- 2.2.3 Delivery mode trends

- 2.2.4 Specialty trends

- 2.2.5 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Value addition at each stage

- 3.1.3 Factors affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of chronic disease and geriatric population drives demand for remote healthcare

- 3.2.1.2 Growing advancement in digital health technology

- 3.2.1.3 Rising adoption of wearable and connected devices

- 3.2.1.4 Government initiatives and reimbursement policies

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Data privacy and security concerns

- 3.2.2.2 Limited internet connectivity in developing areas

- 3.2.3 Market opportunities

- 3.2.3.1 Expanding digital health access in emerging markets

- 3.2.3.2 Penetration of hybrid healthcare models

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Investment and funding landscape

- 3.6 Telehealth projects/ initiatives

- 3.7 Reimbursement scenario

- 3.8 Technological landscape

- 3.8.1 Emerging technology

- 3.8.2 Current technology

- 3.9 Future market trends

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Component, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Hardware

- 5.3 Software

- 5.4 Services

- 5.4.1 Remote patient monitoring

- 5.4.2 Real-time interactions

- 5.4.3 Store and forward

- 5.4.4 Video/ audio consultations

- 5.4.5 Other service types

Chapter 6 Market Estimates and Forecast, By Delivery Mode, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Web/ cloud-based

- 6.3 On premises

Chapter 7 Market Estimates and Forecast, By Specialty, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Dermatology

- 7.3 Mental health

- 7.4 Cardiology

- 7.5 Neurology

- 7.6 Orthopedics

- 7.7 Gynecology

- 7.8 Other specialties

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Healthcare providers

- 8.2.1 Hospitals and clinics

- 8.2.2 Long-term care centers

- 8.2.3 Other healthcare providers

- 8.3 Payers

- 8.4 Patients

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Access TeleCare

- 10.2 AMD

- 10.3 American Well

- 10.4 Apollo TeleHealth

- 10.5 Athenahealth

- 10.6 Capsa Healthcare

- 10.7 Cisco Systems

- 10.8 Doxy.me

- 10.9 Doximity

- 10.10 Eagle Telemedicine

- 10.11 Health Catalyst

- 10.12 Henry Schein

- 10.13 Koninklijke Philips

- 10.14 LifeStance Health

- 10.15 McKesson Medical-Surgical

- 10.16 Medtronic

- 10.17 Omnia TeleHealth

- 10.18 Sesame

- 10.19 Siemens

- 10.20 Teladoc Health

- 10.21 Tellihealth

- 10.22 Veradigm (Allscripts)