|

시장보고서

상품코드

1844281

카트리지 및 펜 재료 시장 : 시장 기회 및 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Cartridge and Pen Materials Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

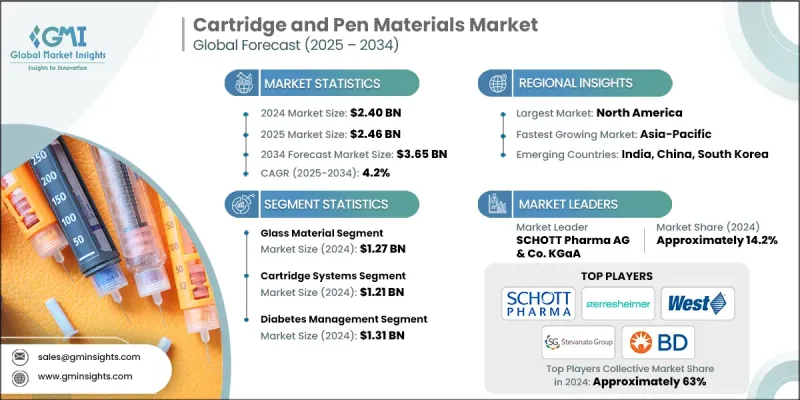

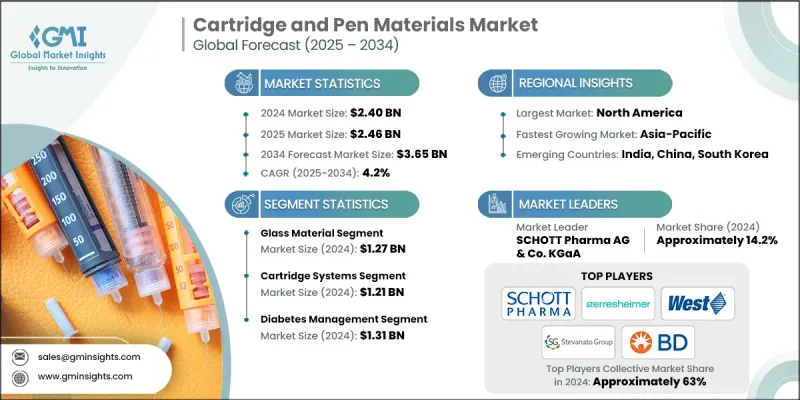

세계의 카트리지 및 펜 재료 시장 규모는 2024년에 24억 달러로 평가되었고, CAGR 4.2%로 성장할 전망이며, 2034년에는 36억 5,000만 달러에 이를 것으로 예측되고 있습니다.

이 진화하는 시장은 대량의 인슐린 전달 시스템에서 환자의 편의성 향상에 초점을 맞춘 더욱 정교한 설계로의 전환이 진행 중입니다. 보다 많은 치료법이 병원에서의 투여에서 가정에서의 주사 형태로 이동함에 따라, 재료의 혁신이 중심적인 우선순위가 되고 있습니다. 장비의 성능과 환자의 편의성을 향상시키는 내구성이 있고 안전하며 규제를 준수하는 재료 개발에 점점 더 집중되고 있습니다. 공급망 전반의 제조업체는 특히 생물학적 제제 및 병용 요법과 같은 복잡한 제형에 맞는 재료에 투자하고 있습니다. 환자 친화적인 자기 투여 시스템 수요가 증가함에 따라 재료는 우수한 적합성, 반응성 감소 및 기계적 특성 향상이 요구되고 있습니다. GLP-1과 다제 병용 요법의 인기 증가는 장기적인 사용성과 컴플라이언스를 지원하는 고급 폴리머와 하이브리드 재료로 시장을 밀어 올리고 있습니다. 또한, 홈 의료 및 디지털 모니터링에 대한 선호도가 높아지면 스마트 납품 장치에 대한 수요가 늘어나 펜 및 카트리지 부품 제조 및 재료 선택에 새로운 복잡성이 생깁니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시장 규모 | 24억 달러 |

| 예측 금액 | 36억 5,000만 달러 |

| CAGR | 4.2% |

2024년 유리 재료 부문의 점유율은 52.4%로 평가되었습니다. 유리는 기존의 주사 요법과 기존의 인슐린 카트리지에 널리 사용됩니다. 유리는 깨지기 쉽고 무거운 무게이며 특히 최신 치료제에서는 민감한 화합물과의 적합성이 낮기 때문에 시장은 유리에서 멀어지고 있습니다. 제조업체 각사는 안전성의 향상, 오염 리스크의 저감, 조립 시 유연성의 향상을 실현하는 첨단 플라스틱의 채용을 진행하고 있습니다.

2024년 펜 컴포넌트 분야의 점유율은 28.5%였습니다. 인체 공학을 기반으로 스마트하고 재사용 가능한 펜 시스템의 사용이 증가하고 있기 때문에 재사용성, 연결성 및 사용자의 편안함을 지원하는 고성능 재료의 요구가 증가하고 있습니다. 특히 만성 치료는 치료의 어드레싱과 편의성을 강조하고 복잡한 전달 메커니즘을 지원하는 펜 설계에 대한 수요가 증가하고 있습니다. GLP-1의 사용, 배합 주사제, 자가 투여 프로토콜의 확대는 펜 부품의 설계 및 제조 방법에 큰 영향을 주고, 정밀도, 촉각 피드백, 고내구성에 중점이 옮겨지고 있습니다.

미국의 카트리지 및 펜 재료 2024년 시장 규모는 6억 7,000만 달러로 평가되었습니다. 미국 시장은 의료용 및 일반 소비자용 이용 사례를 불문하고 리필 및 일회용 펜 제품에 대한 수요가 증가함에 따라 형성되고 있습니다. 겔펜이나 볼펜과 같은 필기구 수요는 견조하게 추이하고 있으며, 소비자는 부드러운 성능과 오래 지속되는 내구성을 중시하고 있습니다. 제조업체 각사는 쾌적성, 디자인, 기능에 있어서 진화하는 기호에 응하기 위해, 고도의 플라스틱 폴리머와 경량 합금을 배합하고 있습니다. 게다가, 판촉용 펜은 특히 브랜딩과 마케팅 활동을 위해 높은 수요가 계속되고 있습니다. 전자상거래 채널이 기세를 늘리면서 개인화와 특수 재료가 구매자들 사이에서 인기를 끌고 있으며, 이 부문 전체 재료 수요의 꾸준한 성장을 지원하고 있습니다.

카트리지 및 펜 재료 시장의 주요 기업으로는 Gerresheimer AG, SCHOTT Pharma AG, West Pharmaceutical Services, Inc., Becton, Dickinson and Company(BD), Stevanato Group SpA 등이 포함됩니다. 카트리지 및 펜 재료 시장의 주요 기업은 내화학성, 저반응성, 진화하는 세계 표준에 대한 규제 대응을 실현하는 첨단 폴리머의 개발로 재료 포트폴리오를 확대하고 있습니다. SCHOTT Pharma AG와 Gerresheimer AG는 차세대 카트리지 및 펜을 위해 기존의 유리와 고품질 폴리머를 결합한 하이브리드 소재 개발을 지원하는 제조 능력에 많은 투자를 하고 있습니다. BD와 Stevanato Group과 같은 기업은 스마트 기술과의 호환성을 펜 플랫폼에 통합하여 디지털 연결을 가능하게 합니다. 공급망의 탄력성과 지역 존재를 향상시키기 위해 많은 기업들이 생산 시설의 현지화를 추진하고 있습니다. 커스텀 메이드 딜리버리 디바이스를 공동 설계하기 위한 의약품 개발 기업과의 공동 개발도 증가하고 있습니다. 재활용 가능하고 환경 친화적인 소재를 선택할 수 있는 등 지속가능성을 중시하는 것도 제품 라인의 장래성을 높이고 경쟁 우위를 획득하기 위해 채용되고 있는 중요한 전술입니다.

목차

제1장 조사 방법

- 시장의 범위 및 정의

- 조사 디자인

- 조사 접근

- 데이터 수집 방법

- 데이터 마이닝 소스

- 세계

- 지역 및 국가

- 기본 추정 및 계산

- 기준 연도 계산

- 시장 예측의 주요 동향

- 1차 조사 및 검증

- 1차 정보

- 예측 모델

- 조사의 전제 및 한계

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 바이오의약품과 바이오시밀러 증가

- 자기 관리와 재택 케어

- 주사기의 안전성에 관한 규제의 추진

- 업계의 잠재적 위험 및 과제

- 유리의 박리와 파손

- 엄격한 규제 테스트

- 공급망의 복잡성

- 시장 기회

- 폴리머 재료의 혁신

- 스마트 및 커넥티드 주사기 시스템

- 아시아태평양 신흥 시장 수요

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 가격 동향

- 지역별

- 제품별

- 장래 시장 동향

- 기술 및 혁신의 상황

- 현재의 기술 동향

- 신흥 기술

- 특허 상황

- 무역 통계(HS코드)(참고 : 무역 통계는 주요 국가에서만 제공됨)

- 주요 수입국

- 주요 수출국

- 지속가능성 및 환경 측면

- 지속가능한 실천

- 폐기물 감축 전략

- 생산에 있어서 에너지 효율

- 환경 친화적인 노력

- 탄소발자국의 고려

제4장 경쟁 구도

- 서문

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병 및 인수

- 파트너십 및 협업

- 신제품 발매

- 확장 계획

제5장 시장 추계 및 예측 : 재질별(2025-2034년)

- 주요 동향

- 유리 재료

- 붕규산 유리

- 소다 석회 유리

- 코팅 유리 솔루션

- 폴리머 재료

- 환상 올레핀 공중합체(COC)

- 환상 올레핀 폴리머(COP)

- 기타 폴리머(폴리프로필렌, 폴리에틸렌)

- 특수 폴리머

- 금속 부품

- 스테인레스 스틸

- 알루미늄 합금

- 코팅 및 도금 금속

- 엘라스토머 부품

- 고무 씰

- 실리콘 엘라스토머

- 열가소성 엘라스토머(TPE)

제6장 시장 추계 및 예측 : 제품 유형별(2025-2034년)

- 주요 동향

- 카트리지 시스템

- 인슐린 카트리지

- 생물 제제 카트리지

- 특수 약제 카트리지

- 펜의 컴포넌트

- 펜 본체

- 주입 메커니즘

- 바늘 조립

- 폐쇄 및 밀봉 시스템

- 플런저 스토퍼

- 바늘 실드

- 캡과 잠금 시스템

제7장 시장 추계 및 예측 : 용도 유형별(2025-2034년)

- 주요 동향

- 당뇨병 관리

- 인슐린 펜

- GLP-1 작용제

- 콤비네이션 인젝터

- 생물제제 및 바이오시밀러

- 단일클론항체

- 성장 호르몬

- 백신 주사기

- 전문 치료제

- 자가면역 질환 치료

- 종양 치료

- 희귀질환 약물 전달

제8장 시장 추계 및 예측 : 지역별(2025-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 기타 라틴아메리카

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

제9장 기업 프로파일

- SCHOTT Pharma AG & Co. KGaA

- Gerresheimer AG

- Stevanato Group SpA

- West Pharmaceutical Services, Inc.

- Becton, Dickinson and Company(BD)

- Ypsomed AG

- Owen Mumford Ltd.

- SHL Medical AG

- Haselmeier GmbH

- Phillips-Medisize(a Molex company)

- Nemera

- Credence MedSystems, Inc.

- Terumo Corporation

- Kraton Corporation

- Datwyler Holding Inc.

The Global Cartridge and Pen Materials Market was valued at USD 2.40 billion in 2024 and is estimated to grow at a CAGR of 4.2% to reach USD 3.65 billion by 2034.

This evolving market is undergoing a shift from high-volume insulin delivery systems to more sophisticated designs focused on improved usability for patients. As more therapies move from hospital-based administration to home-based injectable formats, material innovation has become a core priority. The focus is increasingly on developing durable, safe, and regulatory-compliant materials that enhance device performance and patient experience. Manufacturers across the supply chain are investing in materials tailored for complex drug formulations, particularly in biologics and combination therapies. As demand for patient-friendly, self-administered systems rises, materials must offer superior compatibility, reduced reactivity, and enhanced mechanical properties. The growing popularity of GLP-1s and multi-drug regimens is pushing the market toward advanced polymers and hybrid materials that support long-term usability and compliance. Additionally, the growing preference for at-home care and digital monitoring is driving demand for smart delivery devices, adding another layer of complexity to component manufacturing and material selection in pens and cartridges.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.40 Billion |

| Forecast Value | $3.65 Billion |

| CAGR | 4.2% |

In 2024, the glass materials segment held a 52.4% share. Glasses continue to be widely used in legacy injectable therapies and traditional insulin cartridges. The market is moving away from glass because of its susceptibility to breakage, higher weight, and lower compatibility with sensitive compounds, especially in modern therapies. Manufacturers are progressively adopting advanced plastics that provide improved safety, reduced contamination risk, and greater flexibility during assembly.

The pen components segment held a 28.5% share in 2024. The rising use of ergonomic, smart, and reusable pen systems is driving the need for high-performance materials that support reusability, connectivity, and user comfort. With the increasing focus on therapy adherence and convenience, particularly in chronic treatments, demand is rising for pen designs that support complex delivery mechanisms. The expansion of GLP-1 use, combination injectables, and self-administration protocols has significantly influenced the way pen components are designed and manufactured, shifting emphasis toward precision, tactile feedback, and high durability.

United States Cartridge and Pen Materials Market generated USD 670 million in 2024. The US market is shaped by growing demand for both refillable and disposable pen products across medical and consumer use cases. Demand for writing instruments like gel and ballpoint pens remains steady, with consumers valuing smooth performance and long-lasting durability. Manufacturers are blending advanced plastic polymers and lightweight alloys to meet evolving preferences in comfort, design, and function. Additionally, promotional pens continue to see high demand, especially for branding and marketing activities. As e-commerce channels gain strength, personalization and specialty materials are gaining more traction among buyers, supporting steady growth in material demand across this segment.

Major players in the Global Cartridge and Pen Materials Market include Gerresheimer AG, SCHOTT Pharma AG, West Pharmaceutical Services, Inc., Becton, Dickinson and Company (BD), and Stevanato Group S.p.A. Leading companies in Cartridge and Pen Materials Market are expanding their material portfolios by developing advanced polymers that offer chemical resistance, low reactivity, and regulatory alignment with evolving global standards. SCHOTT Pharma AG and Gerresheimer AG are heavily investing in manufacturing capabilities to support hybrid material development, combining traditional glass and high-grade polymers for next-gen cartridges and pens. Firms like BD and Stevanato Group are integrating smart technology compatibility into their pen platforms, enabling digital connectivity. To improve supply chain resilience and regional presence, many companies are localizing production facilities. Collaborations with drug developers to co-design customized delivery devices are also on the rise. Emphasis on sustainability, with recyclable and eco-friendly material options, is another key tactic adopted to future-proof product lines and gain a competitive advantage.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Material Type

- 2.2.3 Product Type

- 2.2.4 Application

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rise in biologics and biosimilars

- 3.2.1.2 Self-administration & home care

- 3.2.1.3 Regulatory push for syringe safety

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Glass delamination & breakage

- 3.2.2.2 Stringent regulatory testing

- 3.2.2.3 Supply chain complexity

- 3.2.3 Market opportunities

- 3.2.3.1 Polymer material innovation

- 3.2.3.2 Smart/connected syringe systems

- 3.2.3.3 Demand in APAC emerging markets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and Innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and Environmental Aspects

- 3.12.1 Sustainable Practices

- 3.12.2 Waste Reduction Strategies

- 3.12.3 Energy Efficiency in Production

- 3.12.4 Eco-friendly Initiatives

- 3.13 Carbon Footprint Considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Material Type, 2025 - 2034 (USD Million, Units)

- 5.1 Key trends

- 5.2 Glass materials

- 5.2.1 Borosilicate glass

- 5.2.2 Soda-lime glass

- 5.2.3 Coated glass solutions

- 5.3 Polymer materials

- 5.3.1 Cyclic olefin copolymer (COC)

- 5.3.2 Cyclic olefin polymer (COP)

- 5.3.3 Other polymers (polypropylene, polyethylene)

- 5.3.4 Specialty polymers

- 5.4 Metal components

- 5.4.1 Stainless steel

- 5.4.2 Aluminum alloys

- 5.4.3 Coated/plated metals

- 5.5 Elastomer components

- 5.5.1 Rubber seals

- 5.5.2 Silicone elastomers

- 5.5.3 Thermoplastic elastomers (TPEs)

Chapter 6 Market Estimates and Forecast, By Product Type, 2025 - 2034 (USD Million, Units)

- 6.1 Key trends

- 6.2 Cartridge systems

- 6.2.1 Insulin cartridges

- 6.2.2 Biologics cartridges

- 6.2.3 Specialty drug cartridges

- 6.3 Pen components

- 6.3.1 Pen bodies

- 6.3.2 Injection mechanisms

- 6.3.3 Needle assemblies

- 6.4 Closure & sealing systems

- 6.4.1 Plunger stoppers

- 6.4.2 Needle shields

- 6.4.3 Cap and locking systems.

Chapter 7 Market Estimates and Forecast, By Application type, 2025 - 2034 (USD Million, Units)

- 7.1 Key trends

- 7.2 Diabetes management

- 7.2.1 Insulin pens

- 7.2.2 GLP-1 agonists

- 7.2.3 Combination injectors

- 7.3 Biologics and biosimilars

- 7.3.1 Monoclonal antibodies

- 7.3.2 Growth hormones

- 7.3.3 Vaccine injectors

- 7.4 Specialty therapeutics

- 7.4.1 Autoimmune disease therapies

- 7.4.2 Oncology treatments

- 7.4.3 Rare disease drug delivery

Chapter 8 Market Estimates and Forecast, By Region, 2025 - 2034 (USD Million, Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East & Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East & Africa

Chapter 9 Company Profiles

- 9.1 SCHOTT Pharma AG & Co. KGaA

- 9.2 Gerresheimer AG

- 9.3 Stevanato Group S.p.A.

- 9.4 West Pharmaceutical Services, Inc.

- 9.5 Becton, Dickinson and Company (BD)

- 9.6 Ypsomed AG

- 9.7 Owen Mumford Ltd.

- 9.8 SHL Medical AG

- 9.9 Haselmeier GmbH

- 9.10 Phillips-Medisize (a Molex company)

- 9.11 Nemera

- 9.12 Credence MedSystems, Inc.

- 9.13 Terumo Corporation

- 9.14 Kraton Corporation

- 9.15 Datwyler Holding Inc.