|

시장보고서

상품코드

1844300

오프로드 차량용 브레이크 시스템 시장 : 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Off-road Vehicle Braking System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

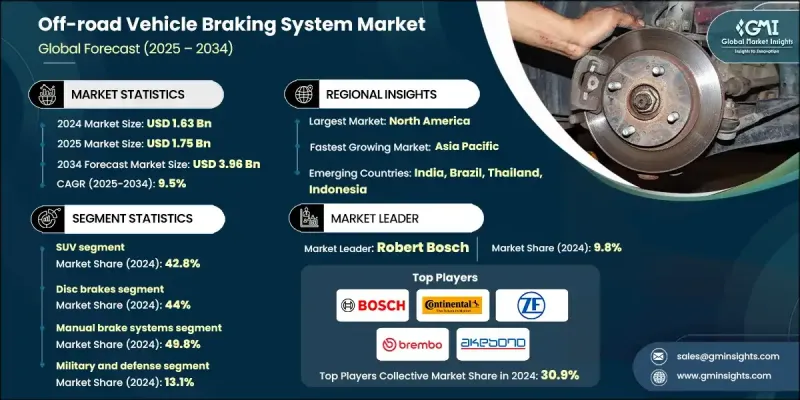

세계의 오프로드 차량용 브레이크 시스템 시장 규모는 2024년에 16억 3,000만 달러로 평가되었고, CAGR 9.5%로 성장할 전망이며, 2034년에는 39억 6,000만 달러에 이를 것으로 예측됩니다.

오프로드 차량이 만나는 가파른 경사, 느슨한 바위, 모래, 진흙과 같은 다양한 지형으로 인해 오프로드 차량의 고성능 브레이크 시스템에 대한 수요가 계속 증가하고 있습니다. 기존의 브레이크 시스템과 달리 오프로드 브레이크 메커니즘은 트랙션과 컨트롤을 유지하면서 다양한 노면 상황에 적응하는 응답성을 제공해야 합니다. 운전자는 특히 어려운 지형을 주파하거나 무거운 적재물을 관리할 때 정확한 모듈레이션을 제공하는 브레이크 시스템에 의존합니다. 오프로드 차량에는 장비 및 탑승자가 자주 추가되므로 브레이크 시스템은 열을 효과적으로 방산하고 액온을 조정하면서 중량 배분의 변화에 대응해야 합니다. 이러한 시스템은 가혹한 조건에서 또는 장기간의 운전에서도 신뢰성을 확보할 수 있도록 브레이크의 페이드를 견뎌야 합니다. 브레이크 기술의 진보는 안정성, 제어성 및 응답성을 향상시키는 데 초점을 맞추고 있으며, 차량이 가득 찼거나 혹독하고 예측 불가능한 환경을 조종하는 경우에도 최적의 제동력을 유지할 수 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시장 규모 | 16억 3,000만 달러 |

| 예측 금액 | 39억 6,000만 달러 |

| CAGR | 9.5% |

SUV 부문은 2024년에 42.8%를 차지하였고, 2034년까지 CAGR 10.3%로 성장이 예측됩니다. 오늘날의 SUV는 변화하는 노면에 적응하는 브레이크 시스템을 탑재하는 것이 늘어나고, 부정지에서의 트랙션과 차량 제어를 강화하고 있습니다. 이러한 기술은 종종 주행 조건 하에서 안전성과 오프로드 조종성을 지원하기 위해 전자 제어식 안정성 제어 시스템 및 트랙션 제어 시스템과 결합되는 경우가 많습니다.

2024년 디스크 브레이크 분야는 44%의 점유율을 차지하였고, 2025-2034년 CAGR 9.9%로 성장할 전망입니다. 디스크 브레이크, 특히 탄소-탄소 복합재료로 구성된 디스크 브레이크는 차량 전체의 무게를 줄이면서 극단적인 온도를 견디는 능력으로 인기를 끌고 있습니다. 뛰어난 강도 대 중량비와 내열성으로 인해 성능과 내구성이 모두 중요한 오프로드 용도에 이상적입니다.

미국의 오프로드 차량용 브레이크 시스템 시장은 2025-2034년 연평균 복합 성장률(CAGR) 10.1%로 성장할 것으로 예측됩니다. 오프로드 트레일, 전용 공원, 딜러, 서비스 인프라의 광범위한 네트워크가 국내 수요를 견인하고 있습니다. 전동 오프로드 자동차의 상승은 시장의 잠재력을 높이고 있습니다. 제조업체 각사는 차량의 견고한 성능을 저하시키지 않으면서 더 큰 토크, 보다 조용한 성능, 저배출 가스를 실현하는 전동 변종을 전개하고 있습니다. 미국 소비자들은 GPS, 텔레매틱스, 온보드 컴퓨터, 전자 파워 스티어링과 같은 고급 기능을 갖춘 오프로드 차량을 선호하고 있으며, 정밀 설계 브레이크 시스템에 대한 수요를 더욱 높입니다.

오프로드 차량용 브레이크 시스템 시장을 독점하고 있는 주요 기업은 ZF Friedrichshafen, Knorr-Bremse, Mando, Advics, Robert Bosch, Continental, Brembo, Akebono Brake Industry 및 Nissin Kogyo 등입니다. 오프로드 차량용 브레이크 시스템 분야의 기업들은 그 지위를 강화하기 위해 기술 혁신과 전략적 제휴에 주력하고 있습니다. 특히 전기자동차와 하이브리드 자동차의 오프로드 플랫폼을 위해 내열성과 내구성을 높이는 경량 고성능 브레이크 재료에 투자하는 기업이 많습니다. 제조업체는 또한 안전성 및 제어성을 높이기 위해 전자 브레이크 솔루션을 고급 운전 지원 기술과 통합합니다. OEM과의 파트너십을 확대하고 지형 특유의 요구에 맞게 브레이크 시스템을 맞춤화함으로써 각 회사는 보다 전문적이고 가치 중심의 솔루션을 제공합니다. 병행하여 제조 능력을 확대하고 차량 텔레매틱스의 데이터를 활용함으로써 제조업체는 예지 보전과 성능 최적화를 제공하여 장기적인 고객 충성도를 확보하고 있습니다.

목차

제1장 조사 방법

- 시장의 범위 및 정의

- 조사 디자인

- 조사 접근

- 데이터 수집 방법

- 데이터 마이닝 소스

- 세계

- 지역 및 국가

- 기본 추정 및 계산

- 기준 연도 계산

- 시장 예측의 주요 동향

- 1차 조사 및 검증

- 1차 정보

- 예보

- 조사의 전제 및 한계

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률 분석

- 비용 구조

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 전동화 및 회생 브레이크

- 안전규제 및 기준

- 가혹한 환경에 대한 노출

- 차량의 적재량 및 중량

- 지형의 변동

- 업계의 잠재적 위험 및 과제

- 높은 개발 및 보수 비용

- 신흥 시장에서의 낮은 인지도

- 시장 기회

- 전기 오프로드 자동차의 성장

- 고급 안전성 통합

- 농업 및 방위 분야 수요

- 스마트 및 커넥티드 브레이크 시스템

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- Porter's Five Forces 분석

- PESTEL 분석

- 기술 및 혁신의 상황

- 현재의 기술 동향

- 신흥 기술

- 코스트 내역 분석

- 특허 분석

- 가격 동향

- 지역별

- 차량별

- 생산 통계

- 생산 거점

- 소비 거점

- 수출 및 수입

- 비용 구조 및 경제 분석

- 제조 비용 내역(재료비, 노무비, 간접비)

- 연구개발 투자 요건 및 감가상각

- 규모의 경제 분석

- 총소유비용(TCO) 모델

- 수요의 가격 탄력성 분석

- 수출입 무역 분석

- 세계 무역 흐름 매핑(HS 코드 분석)

- 주요 수입국 및 수출국

- 지역별 무역수지 분석

- 관세구조 및 무역장벽의 영향

- 공급망의 취약성 평가

- 지속가능성 및 환경 측면

- 지속가능한 관행

- 폐기물 감축 전략

- 생산에 있어서 에너지 효율

- 환경 친화적인 노력

- 탄소발자국의 고려

제4장 경쟁 구도

- 서문

- 기업의 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

- 주요 뉴스와 대처

- 합병 및 인수

- 파트너십 및 협업

- 신제품 발매

- 확장계획 및 자금조달

제5장 시장 추계 및 예측 : 차량별(2021-2034년)

- 주요 동향

- SUV

- UTV

- ATV

- 스노모빌

- 오프로드 오토바이

제6장 시장 추계 및 예측 : 브레이크(2021-2034년)

- 주요 동향

- 디스크 브레이크

- 드럼 브레이크

- 유압 브레이크

- 공압 브레이크

- 전동 브레이크

제7장 시장 추계 및 예측 : 브레이크 시스템 조작별(2021-2034년)

- 주요 동향

- 수동 브레이크 시스템

- 자동 브레이크 시스템

- 안티록 브레이크 시스템(ABS)

- 전자 안정 제어(ESC)

- 트랙션 컨트롤 시스템(TCS)

제8장 시장 추계 및 예측 : 용도별(2021-2034년)

- 주요 동향

- 레크리에이션

- 상업용

- 농업

- 군사 및 방위

- 채굴 및 추출

제9장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 북유럽 국가

- 네덜란드

- 러시아

- 아시아태평양

- 호주

- 중국

- 인도

- 인도네시아

- 일본

- 싱가포르

- 한국

- 태국

- 베트남

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제10장 기업 프로파일

- 세계의 톱 기업

- Brembo

- ZF Friedrichshafen

- Continental

- Robert Bosch

- Akebono Brake Industry

- AISIN

- Tenneco

- Mando

- Nissin Kogyo

- 지역 기업

- Caterpillar

- Komatsu

- KNORR-BREMSE

- Haldex

- Hitachi Astemo

- Technology Specialists

- ADVICS

- Hayes Performance Systems

- Wilwood Engineering

- 신흥 기업 및 교란 기업

- Yamaha

- Rivian Automotive

- OEM Integration Partners

- John Deere

- Volvo Construction Equipment

- Liebherr

- CNH Industrial

The Global Off-road Vehicle Braking System Market was valued at USD 1.63 billion in 2024 and is estimated to grow at a CAGR of 9.5% to reach USD 3.96 billion by 2034.

The demand for high-performance braking systems in off-road vehicles continues to grow due to the diverse terrains these vehicles encounter, including steep inclines, loose rocks, sand, and mud. Unlike conventional braking systems, off-road braking mechanisms must deliver adaptive responsiveness to varying surface conditions while maintaining traction and control. Drivers depend on braking systems to offer precise modulation, particularly when navigating rugged terrain or managing heavy payloads. As off-road vehicles frequently carry added equipment or passengers, their braking systems must handle weight distribution shifts while effectively dissipating heat and regulating fluid temperature. These systems must also resist brake fade, ensuring reliability under extreme conditions and during prolonged operation. Advancements in braking technology continue to focus on improving stability, control, and responsiveness, making it possible to maintain optimal stopping power even when vehicles are fully loaded or maneuvering through harsh, unpredictable environments.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.63 Billion |

| Forecast Value | $3.96 Billion |

| CAGR | 9.5% |

The SUV segment held 42.8% in 2024 and is forecasted to grow at a CAGR of 10.3% through 2034. SUVs today are increasingly equipped with braking systems that adapt to changing surfaces, enhancing traction and vehicle control across uneven terrains. These technologies are often paired with electronic stability and traction control systems to support safety and off-road maneuverability in a wide range of driving conditions.

In 2024, the disc brake segment held a 44% share and will grow at a CAGR of 9.9% from 2025 to 2034. Disc brakes, particularly those constructed from carbon-carbon composites, are gaining popularity due to their ability to withstand extreme temperatures while reducing overall vehicle weight. Their superior strength-to-weight ratio and heat resistance make them ideal for off-road applications where both performance and durability are critical.

U.S. Off-road Vehicle Braking System Market will grow at a CAGR of 10.1% between 2025 and 2034. An extensive network of off-road trails, dedicated parks, dealerships, and service infrastructure is driving domestic demand. The rise of electric off-road vehicles is also boosting market potential. Manufacturers are rolling out electric variants that deliver greater torque, quieter performance, and lower emissions all without compromising the vehicle's rugged capabilities. U.S. consumers are increasingly favoring off-road vehicles equipped with advanced features like GPS, telematics, onboard computers, and electronic power steering, further elevating the demand for precision-engineered braking systems.

Key players dominating the Off-road Vehicle Braking System Market include ZF Friedrichshafen, Knorr-Bremse, Mando, Advics, Robert Bosch, Continental, Brembo, Akebono Brake Industry, and Nissin Kogyo. To strengthen their position, companies in the off-road vehicle braking system sector are focusing on innovation and strategic collaboration. Many are investing in lightweight, high-performance brake materials that enhance thermal resistance and durability, particularly for electric and hybrid off-road platforms. Manufacturers are also integrating electronic braking solutions with advanced driver-assist technologies to enhance safety and control. Expanding partnerships with OEMs and customizing braking systems for terrain-specific needs are helping companies offer more specialized, value-driven solutions. In parallel, expanding manufacturing capabilities and leveraging data from vehicle telematics are helping manufacturers provide predictive maintenance and performance optimization, securing long-term customer loyalty.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Vehicle

- 2.2.3 Brake

- 2.2.4 Brake system operations

- 2.2.5 Application

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook

- 2.6 Strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Electrification & regenerative braking

- 3.2.1.2 Safety regulations & standards

- 3.2.1.3 Harsh environmental exposure

- 3.2.1.4 Vehicle load & weight

- 3.2.1.5 Terrain variability

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High development & maintenance costs

- 3.2.2.2 Limited awareness in emerging markets

- 3.2.3 Market opportunities

- 3.2.3.1 Growth of electric off-road vehicles

- 3.2.3.2 Advanced safety integration

- 3.2.3.3 Demand in agriculture & defense sectors

- 3.2.3.4 Smart & connected braking systems

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology & innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Cost breakdown analysis

- 3.9 Patent analysis

- 3.10 Price trends

- 3.10.1 By region

- 3.10.2 By Vehicle

- 3.11 Production statistics

- 3.11.1 Production hubs

- 3.11.2 Consumption hubs

- 3.11.3 Export and import

- 3.12 Cost Structure & Economics Analysis

- 3.12.1 Manufacturing Cost Breakdown (Materials, Labor, Overhead)

- 3.12.2 R&D Investment Requirements & Amortization

- 3.12.3 Economies of Scale Analysis

- 3.12.4 Total Cost of Ownership (TCO) Models

- 3.12.5 Price Elasticity of Demand Analysis

- 3.13 Import-Export Trade Analysis

- 3.13.1 Global Trade Flow Mapping (HS Code Analysis)

- 3.13.2 Top Importing & Exporting Countries

- 3.13.3 Trade Balance Analysis by Region

- 3.13.4 Tariff Structure & Trade Barriers Impact

- 3.13.5 Supply Chain Vulnerability Assessment

- 3.14 Sustainability and environmental aspects

- 3.14.1 Sustainable practices

- 3.14.2 Waste reduction strategies

- 3.14.3 Energy efficiency in production

- 3.14.4 Eco-friendly initiatives

- 3.14.5 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key news and initiatives

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Mn, Units)

- 5.1 Key trends

- 5.1.1 SUV

- 5.1.2 UTV

- 5.1.3 ATV

- 5.1.4 Snowmobile

- 5.1.5 Off-road Motorcycle

Chapter 6 Market Estimates & Forecast, By Brake, 2021 - 2034 ($Mn, Units)

- 6.1 Key trends

- 6.2 Disc Brakes

- 6.3 Drum Brakes

- 6.4 Hydraulic Brakes

- 6.5 Pneumatic Brakes

- 6.6 Electromechanical Brakes

Chapter 7 Market Estimates & Forecast, By Brake System Operations, 2021 - 2034 ($Mn, Units)

- 7.1 Key trends

- 7.1.1 Manual Brake Systems

- 7.1.2 Automatic Brake Systems

- 7.1.3 Anti-lock Braking Systems (ABS)

- 7.1.4 Electronic Stability Control (ESC)

- 7.1.5 Traction Control Systems (TCS)

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 ($Mn, Units)

- 8.1 Key trends

- 8.2 Recreational

- 8.3 Commercial

- 8.4 Agricultural

- 8.5 Military and Defense

- 8.6 Mining and Extraction

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Nordics

- 9.3.7 Netherlands

- 9.3.8 Russia

- 9.4 Asia Pacific

- 9.4.1 Australia

- 9.4.2 China

- 9.4.3 India

- 9.4.4 Indonesia

- 9.4.5 Japan

- 9.4.6 Singapore

- 9.4.7 South Korea

- 9.4.8 Thailand

- 9.4.9 Vietnam

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1.1.1 Top Global Players

- 10.1.1.1.1 Brembo

- 10.1.1.1.2 ZF Friedrichshafen

- 10.1.1.1.3 Continental

- 10.1.1.1.4 Robert Bosch

- 10.1.1.1.5 Akebono Brake Industry

- 10.1.1.1.6 AISIN

- 10.1.1.1.7 Tenneco

- 10.1.1.1.8 Mando

- 10.1.1.1.9 Nissin Kogyo

- 10.1.1.2 Regional Players

- 10.1.1.2.1 Caterpillar

- 10.1.1.2.2 Komatsu

- 10.1.1.2.3 KNORR-BREMSE

- 10.1.1.2.4 Haldex

- 10.1.1.2.5 Hitachi Astemo

- 10.1.1.2.6 Technology Specialists

- 10.1.1.2.7 ADVICS

- 10.1.1.2.8 Hayes Performance Systems

- 10.1.1.2.9 Wilwood Engineering

- 10.1.1.3 Emerging Players & Disruptors

- 10.1.1.3.1 Yamaha

- 10.1.1.3.2 Rivian Automotive

- 10.1.1.3.3 OEM Integration Partners

- 10.1.1.3.4 John Deere

- 10.1.1.3.5 Volvo Construction Equipment

- 10.1.1.3.6 Liebherr

- 10.1.1.3.7 CNH Industrial