|

시장보고서

상품코드

1844305

자동차용 오디오 반도체 시장 : 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Automotive Audio Semiconductor Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

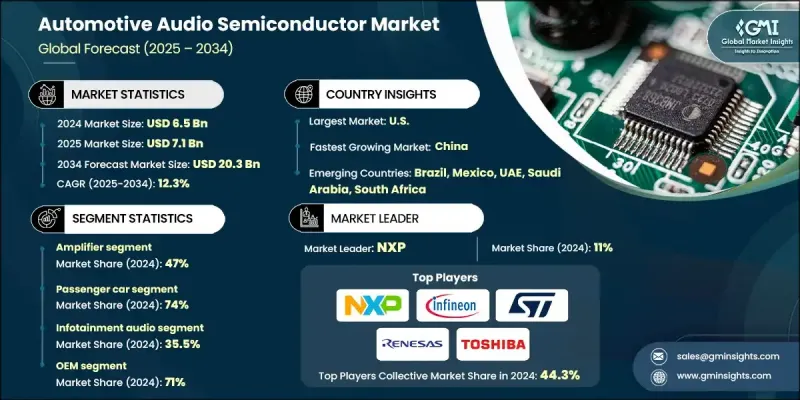

세계의 자동차용 오디오 반도체 시장 규모는 2024년에는 65억 달러로 평가되었고, CAGR 12.3%로 성장할 전망이며, 2034년에는 203억 달러에 달할 것으로 예측되고 있습니다.

이러한 성장은 자동차 제조업체들이 몰입감 있는 사용자 경험을 선호하기 때문에 고급 자동차 인포테인먼트 시스템에 대한 수요가 급증하고 있음을 반영합니다. 현대 소비자는 터치 스크린, 음성 상호작용, 원활한 오디오 연결을 기대하고 있으며, 반도체는 고충실도 사운드 처리 및 효율적인 멀티채널 설정의 전원으로서 중요한 역할을 하고 있습니다. 전기자동차 및 하이브리드 자동차가 차 안의 쾌적성과 고급 전자 기능을 중시하게 되면서, 성능, 에너지 효율, 저잡음 기준을 충족하기 위해 특수한 반도체가 점점 요구되고 있습니다. 음성 명령 시스템과 AI 주도의 인포테인먼트 플랫폼은 명령을 해석하여 실시간 음질을 향상시키는 고급 오디오 칩에 의존합니다. 커넥티드 및 인터랙티브 차량 내 환경으로의 이동은 모든 차량 부문에 걸친 반도체 집적의 상승에 직접적인 영향을 미칩니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시장 규모 | 65억 달러 |

| 예측 금액 | 203억 달러 |

| CAGR | 12.3% |

2024년, 앰프 분야는 47%의 점유율을 차지하였고, 2034년까지 CAGR 13%로 성장이 예측됩니다. 첨단 D급 앰프는 자동차 오디오 아키텍처에 널리 통합되어 전력 효율을 최적화하면서 왜곡을 최소화한 멀티 채널 오디오를 지원합니다. 이 동향은 특히 중급차와 고급차 부문에서 보다 고도의 사운드 체험을 요구하는 소비자 수요가 주인이 되고 있습니다.

승용차 부문은 2024년에 74%의 점유율을 차지하였고, 2025-2034년 CAGR 12.9%로 성장할 것으로 예측됩니다. 이 부문은 음성 인식, 오디오 스트리밍, 인터랙티브 디스플레이와 같은 인포테인먼트 기술의 사용을 증가시키고 있으며, 전력 증폭기, DSP, 커넥티비티 칩과 같은 집적 반도체 솔루션의 요구가 크게 증가하고 있습니다. 향상된 사운드 기능은 이제 엔트리 레벨 모델에서도 필수적이며, 승용차 카테고리 전체에서 오디오에 특화된 반도체 수요를 강화하고 있습니다.

미국의 자동차용 오디오 반도체 시장 점유율은 90%로 2024년에는 16억 달러를 창출했습니다. 이 나라는 프리미엄 자동차와 고급 자동차 판매에서 세계적인 선두 주자이며, 하이 엔드 브랜드 사운드 시스템이 필수적인 기능입니다. 이러한 자동차는 서라운드 사운드 프로세싱, 신호 컨디셔닝 및 앰프 성능을 위해 첨단 반도체를 필요로 합니다. 자동차 제조업체가 몰입감이 있는 오디오 체험으로 차별화를 도모하는 가운데, 미국은 자동차용 오디오 칩 기술의 채용과 개발로 리드를 계속하고 있습니다.

자동차용 오디오 반도체 시장의 주요 기업으로는 Infineon Technologies, ROHM Semiconductor, NXP, Analog Devices, STMicroelectronics, ON Semiconductor, Qualcomm, Toshiba Electronic Devices, Texas Instruments, and Renesas Electronics 등이 있습니다. 경쟁이 치열한 자동차용 오디오 반도체 시장에서 확고한 지위를 유지하기 위해 주요 기업은 스마트 앰프와 AI 통합 DSP 등 차세대 오디오 기술에 많은 투자를 하고 있습니다. 각 회사는 음향 성능을 높이면서 전기자동차 수요에 부응하는 에너지 효율이 높은 칩 설계에 주력하고 있습니다. 자동차 OEM과의 전략적 제휴는 제품 채용을 가속화하는 데 도움이 되며 연구개발 노력은 첨단 연결성 및 음성 인터페이스를 지원하는 작고 다기능 칩 개발을 목표로 합니다.

목차

제1장 조사 방법

- 시장의 범위 및 정의

- 조사 디자인

- 조사 접근

- 데이터 수집 방법

- 데이터 마이닝 소스

- 세계

- 지역 및 국가

- 기본 추정 및 계산

- 기준 연도 계산

- 시장 예측의 주요 동향

- 1차 조사 및 검증

- 1차 정보

- 예측 모델

- 조사의 전제 및 한계

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률 분석

- 비용 구조

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 몰입형 차량용 오디오 수요 증가

- EV 보급 증가

- AI 및 음성 어시스턴트의 통합

- 커넥티드카 및 소프트웨어 정의 차량으로의 전환

- 오디오 브랜드와의 프리미엄 OEM 콜라보레이션

- 업계의 잠재적 위험 및 과제

- 높은 연구 개발비 및 생산 비용

- 반도체 공급망의 불안정성

- 엄격한 자동차 신뢰성 기준

- 급속한 기술 변화

- 시장 기회

- 아시아태평양에서 EV와 하이브리드 자동차의 생산 증가

- 액티브 노이즈 캔슬레이션(ANC)의 채용

- 클라우드 접속형 인포테인먼트 시스템

- 신흥 시장에서의 고급차소유 확대

- 칩 제조업체 및 Tier 1 OEM의 제휴

- 성장 촉진요인

- 성장 가능성 분석

- 주요 시장 동향 및 혼란

- 장래 시장 동향

- 규제 상황

- Porter's Five Forces 분석

- PESTEL 분석

- 기술과 혁신의 상황

- 현재의 기술 동향

- 신흥 기술

- 특허 분석

- 가격 동향

- 지역별

- 제품별

- 코스트 내역 분석

- 생산 통계

- 생산 거점

- 수입 및 수출

- 주요 수입국

- 지속가능성 및 환경 측면

- 지속가능한 관행

- 폐기물 감축 전략

- 생산에서의 에너지 효율

- 환경 친화적인 노력

- 탄소발자국의 고려

- 투자 상황 분석

- 반도체 연구개발 투자

- 차재 오디오 기술에 대한 자금 제공

- 오디오 혁신의 벤처 캐피탈

- 기업의 투자 패턴

- 정부의 조사 자금

- 오디오 반도체에서 M&A 활동

- 차재 오디오 아키텍처의 진화

- ADAS 오디오 통합

- 멀티존 및 개인화된 오디오 시스템

- 소프트웨어 정의 차량(SDV)의 영향

- 오디오 품질 및 성능의 벤치마크

제4장 경쟁 구도

- 서문

- 기업의 시장 점유율 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

- 주요 발전

- 합병 및 인수

- 파트너십 및 협업

- 신제품 발매

- 확장계획 및 자금조달

제5장 시장 추계 및 예측 : 컴포넌트별(2021-2034년)

- 주요 동향

- 증폭기

- DSP

- 마이크

- 튜너

제6장 시장 추계 및 예측 : 추진력별(2021-2034년)

- 주요 동향

- 가솔린

- 디젤

- 전 전기자동차

- 하이브리드 자동차

- PHEV

- 연료 전지 자동차

제7장 시장 추계 및 예측 : 용도별(2021-2034년)

- 주요 동향

- 인포테인먼트 오디오

- 차내 음성

- 액티브 노이즈 캔슬링

- ADAS 오디오 큐

- 텔레매틱스 및 통화 음성

- 기타

제8장 시장 추계 및 예측 : 설비별(2021-2034년)

- 주요 동향

- OEM

- 애프터마켓

제9장 시장 추계 및 예측 : 차량별(2021-2034년)

- 주요 동향

- 승용차

- 해치백

- 세단

- SUV

- 상용차

- 경작

- 중형

- 내구성이 높은

제10장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 북유럽 국가

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주 및 뉴질랜드

- 동남아시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제11장 기업 프로파일

- 세계 기업

- Analog Devices

- Cirrus Logic

- Infineon Technologies

- NXP

- ON Semiconductor

- Qualcomm

- Renesas Electronics

- ROHM Semiconductor

- STMicroelectronics

- Texas Instruments

- Toshiba Electronic Devices

- Regional Champions

- MediaTek

- Realtek

- ESS Technology

- Synaptics

- Dialog Semiconductor

- Wolfson Microelectronics

- AKM Semiconductor

- Yamaha

- Nuvoton Technology

- Silicon Labs

- 신흥 기업 및 서비스 제공업체

- Cadence Design Systems

- CEVA

- Dolby Laboratories

- DSP Group

- DTS

- Fortemedia

- Imagination Technologies

- Knowles

- Tempo Semiconductor

- Waves Audio

The Global Automotive Audio Semiconductor Market was valued at USD 6.5 billion in 2024 and is estimated to grow at a CAGR of 12.3% to reach USD 20.3 billion by 2034.

This growth reflects the surge in demand for advanced in-vehicle infotainment systems, as automakers prioritize immersive user experiences. With modern consumers expecting touchscreens, voice interaction, and seamless audio connectivity, semiconductors play a key role in powering high-fidelity sound processing and efficient multi-channel setups. As electric and hybrid vehicles emphasize cabin comfort and advanced electronic features, specialized semiconductors are increasingly required to meet performance, energy efficiency, and low-noise standards. Voice-command systems and AI-driven infotainment platforms also rely on sophisticated audio chips to interpret commands and enhance real-time sound quality. The shift toward connected, interactive cabin environments is directly influencing the rise in semiconductor integration across all vehicle segments.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $6.5 Billion |

| Forecast Value | $20.3 Billion |

| CAGR | 12.3% |

In 2024, the amplifiers segment held a 47% share and is forecast to grow at a CAGR of 13% through 2034. Advanced Class-D amplifiers are being widely integrated into vehicle audio architectures, supporting multi-channel audio with minimal distortion while optimizing power efficiency. This trend is primarily driven by consumer demand for elevated sound experiences, particularly in mid-range and high-end vehicle segments.

The passenger cars segment held a 74% share in 2024 and is anticipated to grow at a CAGR of 12.9% between 2025 and 2034. The rising use of infotainment technologies in this segment, including voice recognition, audio streaming, and interactive displays, has significantly increased the need for integrated semiconductor solutions like power amplifiers, DSPs, and connectivity chips. Enhanced sound features are now essential even in entry-level models, reinforcing the demand for audio-focused semiconductors throughout the passenger vehicle category.

US Automotive Audio Semiconductor Market held a 90% share and generated USD 1.6 billion in 2024. The country remains a global leader in the sale of premium and luxury vehicles, where high-end branded sound systems are essential features. These vehicles require advanced semiconductors for surround sound processing, signal conditioning, and amplifier performance. As carmakers strive to differentiate with immersive audio experiences, the US continues to lead in the adoption and development of automotive audio chip technologies.

Key players in the Automotive Audio Semiconductor Market include Infineon Technologies, ROHM Semiconductor, NXP, Analog Devices, STMicroelectronics, ON Semiconductor, Qualcomm, Toshiba Electronic Devices, Texas Instruments, and Renesas Electronics. To maintain a strong position in the competitive automotive audio semiconductor market, leading companies are investing heavily in next-gen audio technologies, including smart amplifiers and AI-integrated DSPs. Firms are focusing on energy-efficient chip designs that meet the demands of electric vehicles while enhancing acoustic performance. Strategic alliances with automotive OEMs help accelerate product adoption, while R&D efforts are geared toward developing compact, multifunctional chips that support advanced connectivity and voice interfaces.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Vehicle

- 2.2.4 Propulsion

- 2.2.5 Application

- 2.2.6 Installation

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook

- 2.6 Strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing demand for immersive in-car audio

- 3.2.1.2 Increasing EV adoption

- 3.2.1.3 Integration of AI and voice assistants

- 3.2.1.4 Shift toward connected and software-defined vehicles

- 3.2.1.5 Premium OEM collaborations with audio brands

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High R&D and production costs

- 3.2.2.2 Semiconductor supply chain volatility

- 3.2.2.3 Stringent automotive reliability standards

- 3.2.2.4 Rapid pace of tech change

- 3.2.3 Market opportunities

- 3.2.3.1 Growing EV and hybrid production in APAC

- 3.2.3.2 Adoption of active noise cancellation (ANC)

- 3.2.3.3 Cloud-connected infotainment systems

- 3.2.3.4 Expansion of premium car ownership in emerging markets

- 3.2.3.5 Collaboration between chipmakers and Tier-1 OEMs

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Major market trends and disruptions

- 3.5 Future market trends

- 3.6 Regulatory landscape

- 3.6.1 North America

- 3.6.2 Europe

- 3.6.3 Asia Pacific

- 3.6.4 Latin America

- 3.6.5 MEA

- 3.7 Porter’s analysis

- 3.8 PESTEL analysis

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent analysis

- 3.11 Price trends

- 3.11.1 By region

- 3.11.2 By product

- 3.12 Cost breakdown analysis

- 3.13 Production statistics

- 3.13.1 Production hubs

- 3.13.2 Import and export

- 3.13.3 Major import countries

- 3.14 Sustainability and environmental aspects

- 3.14.1 Sustainable practices

- 3.14.2 Waste reduction strategies

- 3.14.3 Energy efficiency in production

- 3.14.4 Eco-friendly initiatives

- 3.14.5 Carbon footprint considerations

- 3.15 Investment Landscape Analysis

- 3.15.1 Semiconductor R&D Investment

- 3.15.2 Automotive Audio Technology Funding

- 3.15.3 Venture Capital in Audio Innovation

- 3.15.4 Corporate Investment Patterns

- 3.15.5 Government Research Funding

- 3.15.6 M&A Activity in Audio Semiconductors

- 3.16 Automotive Audio Architecture Evolution

- 3.17 ADAS Audio Integration

- 3.18 Multi-Zone and Personalized Audio Systems

- 3.19 Software-Defined Vehicle (SDV) Impact

- 3.20 Audio Quality and Performance Benchmarking

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn) (Units)

- 5.1 Key trends

- 5.2 Amplifier

- 5.3 DSP

- 5.4 Microphone

- 5.5 Tuner

Chapter 6 Market Estimates & Forecast, By Propulsion, 2021 - 2034 ($Bn) (Units)

- 6.1 Key trends

- 6.2 Gasoline

- 6.3 Diesel

- 6.4 All-electric

- 6.5 HEV

- 6.6 PHEV

- 6.7 FCEV

Chapter 7 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn) (Units)

- 7.1 Key trends

- 7.2 Infotainment audio

- 7.3 In-car Voice

- 7.4 Active noise cancellation

- 7.5 ADAS audio cues

- 7.6 Telematics & call audio

- 7.7 Others

Chapter 8 Market Estimates & Forecast, By Installation, 2021 - 2034 ($Bn) (Units)

- 8.1 Key trends

- 8.2 OEM

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn) (Units)

- 9.1 Key trends

- 9.2 Passenger car

- 9.2.1 Hatchback

- 9.2.2 Sedan

- 9.2.3 SUV

- 9.3 Commercial Vehicle

- 9.3.1 Light duty

- 9.3.2 Medium duty

- 9.3.3 Heavy-duty

Chapter 10 Market Estimates & Forecast, By Region, 2021-2034 ($Bn) (Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 ANZ

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Players

- 11.1.1 Analog Devices

- 11.1.2 Cirrus Logic

- 11.1.3 Infineon Technologies

- 11.1.4 NXP

- 11.1.5 ON Semiconductor

- 11.1.6 Qualcomm

- 11.1.7 Renesas Electronics

- 11.1.8 ROHM Semiconductor

- 11.1.9 STMicroelectronics

- 11.1.10 Texas Instruments

- 11.1.11 Toshiba Electronic Devices

- 11.2 Regional Champions

- 11.2.1 MediaTek

- 11.2.2 Realtek

- 11.2.3 ESS Technology

- 11.2.4 Synaptics

- 11.2.5 Dialog Semiconductor

- 11.2.6 Wolfson Microelectronics

- 11.2.7 AKM Semiconductor

- 11.2.8 Yamaha

- 11.2.9 Nuvoton Technology

- 11.2.10 Silicon Labs

- 11.3 Emerging Players & Service Providers

- 11.3.1 Cadence Design Systems

- 11.3.2 CEVA

- 11.3.3 Dolby Laboratories

- 11.3.4 DSP Group

- 11.3.5 DTS

- 11.3.6 Fortemedia

- 11.3.7 Imagination Technologies

- 11.3.8 Knowles

- 11.3.9 Tempo Semiconductor

- 11.3.10 Waves Audio