|

시장보고서

상품코드

1844346

비타민 D 검사 시장 : 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Vitamin D Testing Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

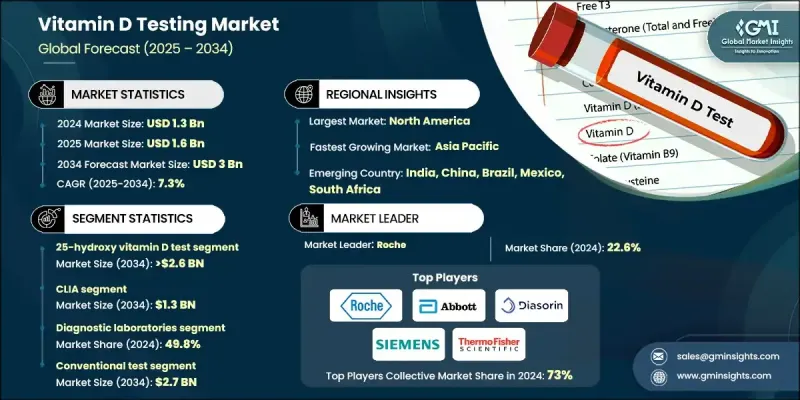

세계의 비타민 D 검사 시장은 2024년 13억 달러로 평가되었으며 CAGR 7.3%로 성장해 2034년까지 30억 달러에 이를 것으로 추정됩니다.

이 성장은 세계적인 비타민 D 결핍증 유병률 증가, 예방 건강 관리에 대한 관심 증가, 진단 검사에 대한 수요 증가가 영향을 받고 있습니다. 건강 관리 시스템에 첨단 기술의 지속적인 통합은 비타민 D 진단 약물의 채택을 가속화하고 있습니다. 당뇨병, 자가면역질환, 심혈관질환, 골다공증 등의 만성질환이 증가하는 가운데 비타민 D 검사는 임상 워크플로우의 중요한 부분이 되고 있습니다. 건강 관리 제공업체는 결핍을 관리하고 보충의 결과를 더 정확하게 모니터링하기 위해 이러한 검사를 일상 진단에 통합합니다. 진단 실험실, 지불자, 디지털 건강 플랫폼은 정확성 향상과 환자 모니터링을 위해 LC-MS/MS, ELISA, 화학발광 면역 측정법 등의 솔루션에 주목하고 있습니다. 이는 조기 발견이 중요한 역할을 하는 개인화된 건강 관리로의 큰 변화를 지원합니다. 비타민 D 검사가 병원, 클리닉, 심지어 가정에서 이용 가능하게 된 것은 접근성 향상에 기여합니다. 만성 질환 예방, 모자 건강, 노인 케어 프로그램에 대한 중점 확대는 시장의 일관된 성장 궤도를 더욱 강화하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시장 규모 | 13억 달러 |

| 예측 금액 | 30억 달러 |

| CAGR | 7.3% |

25-히드록시 비타민 D 검사 분야는 여전히 혈중 비타민 D 농도를 평가하기 위한 표준으로 선호되었기 때문에 2024년 86.2%의 점유율을 차지했습니다. 이 분야는 CAGR 7.6%로 성장하여 2034년에는 26억 달러에 달할 것으로 예측됩니다. 이 검사는 만성 질환 관리, 정기 건강 진단, 노인 관리, 영양 평가 등 여러 임상 응용 분야에 사용됩니다. 이 검사는 햇빛에 대한 노출이 제한적이거나, 식사에 의한 섭취량이 적거나, 비타민 D의 흡수에 영향을 미치는 대사 장애가 있는 사람의 결핍을 평가하기 위해 널리 채택됩니다. 전체 집단의 스크리닝과 표적 진단 모두에서 이 검사의 역할은 시장의 장점을 계속 확고히 합니다.

CLIA 분야는 2024년에 43.5%의 점유율을 차지했으며, 2034년에는 13억 달러에 이를 것으로 예측됩니다. 화학발광 면역측정법 수요가 증가하고 있는 이유는 기존의 면역측정법보다 감도와 정밀도가 우수하기 때문입니다. CLIA는 결핍 관련 위험을 평가하는 데 필수적인 마커인 주요 비타민 D 대사산물의 정확한 정량을 가능하게 합니다. 신뢰성, 스피드, 스케일러블한 처리량에 의해 집중형 랩에서도 포인트 오브 케어에서도 채용이 확대하고 있습니다.

2024년 북미 비타민 D 검사 시장 점유율은 37.7%로 첨단 의료 인프라, 높은 환자 의식, 적극적인 스크리닝 노력이 견인했습니다. 이 지역은 특히 일조 시간이 짧은 지역에서 비타민 D 결핍증이 만연하고 있습니다. 그 결과, 검사가 일상적인 건강 진단에 통합되어 왔습니다. 의사는 장기적인 질병을 가진 환자에게 정기적으로 이러한 검사를 권장하며 수요 증가에 기여합니다. 보험이 널리 적용되고, 정부 건강 캠페인이 실시되고, 재택 진단이 확대됨에 따라 미국과 캐나다 시장 확대가 더욱 가속화되고 있습니다.

세계 비타민 D 검사 시장을 형성하는 주요 기업은 Abbott, Thermo Fisher Scientific, Roche, Danaher(Beckman Coulter), Mindray Medical International, NanoSpeed Diagnostics, Siemens, Diasorin, Randox Laboratories, Bio-Rad Laboratories, Toso, Qu Therapeutics, EUROIMMUN, bioMerieux, NanoEnTek 등이 있습니다. 기반을 강화하기 위해 비타민 D 검사 시장의 선도 기업들은 다양한 전략적 노력을 실시했습니다. 대부분은 보다 빠른 턴어라운드 시간을 제공하는 고감도 차세대 분석 키트를 출시함으로써 진단 포트폴리오의 확대에 주력하고 있습니다. 또한 워크플로우 효율성과 데이터 정확성을 높이기 위해 자동화 및 AI 기반 분석에도 투자하고 있습니다. 고성장 지역으로의 지리적 확대는 유통업체와의 제휴와 현지 생산을 통해 우선적으로 진행되고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 부품 및 기술 공급자

- 진단 장치 및 키트 제조업체

- 각 단계에서의 부가가치

- 업계에 미치는 영향요인

- 성장 촉진요인

- 비타민 D 결핍증의 유병률 증가

- 소비자의 의식 고조

- 공중위생 캠페인과 상환 정책 증가

- 기술의 진보의 가속

- 업계의 잠재적 위험 및 과제

- 첨단 진단 방법의 높은 비용

- 시장 기회

- 포인트 오브 케어와 재택 검사로의 확대

- 신흥 시장으로의 성장

- 성장 촉진요인

- 성장 가능성 분석

- 규제 시나리오

- 북미

- 유럽

- 아시아태평양

- 환급 시나리오

- 기술의 상황

- 현재의 기술 동향

- 신흥기술

- 미래 시장 동향

- 가격 분석, 2024년

- 특허 상황

- 특허권자 분석

- 임상 가이드라인과 표준화

- 투자 및 자금조달 동향

- 역학 시나리오

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업 매트릭스 분석

- 기업의 시장 점유율 분석

- 세계

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 경쟁 포지셔닝 매트릭스

- 주요 시장 기업의 경쟁 분석

- 주요 발전

- 합병과 인수

- 파트너십 및 협업

- 새로운 서비스 유형의 개시

- 확장 계획

제5장 시장 추계 및 예측 : 제품별, 2021-2034년

- 주요 동향

- 25-히드록시비타민 D 검사

- 1,25-디히드록시비타민 D 검사

제6장 시장 추계 및 예측 : 테크닉별, 2021-2034년

- 주요 동향

- CLIA

- ELISA

- LC-MS

- 방사면역검정

- 기타 기술

제7장 시장 추계 및 예측 : 적응증별, 2021-2034년

- 주요 동향

- 비타민 D 결핍증

- 골다공증

- 심혈관계

- 구루병

- 갑상선 질환

- 기타 적응증

제8장 시장 추계 및 예측 : 환자별, 2021-2034년

- 주요 동향

- 성인

- 소아

제9장 시장 추계 및 예측 : 테스트 유형별, 2021-2034년

- 주요 동향

- 기존 검사

- 포인트 오브 케어 검사

제10장 시장 추계 및 예측 : 최종 용도별, 2021-2034년

- 주요 동향

- 진단실험실

- 병원

- 홈케어

- 기타 용도

제11장 시장 추계 및 예측 : 지역별, 2021-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제12장 기업 프로파일

- Abbott

- bioMerieux

- Bio-Rad Laboratories

- Danaher(Beckman Coulter)

- Diasorin

- EUROIMMUN

- Roche

- Mindray Medical International

- NanoEnTek

- NanoSpeed Diagnostics

- Qualigen Therapeutics

- Randox Laboratories

- Siemens

- Thermo Fisher Scientific

- Tosoh

The Global Vitamin D Testing Market was valued at USD 1.3 billion in 2024 and is estimated to grow at a CAGR of 7.3% to reach USD 3 billion by 2034.

The growth is influenced by the increasing prevalence of vitamin D deficiency worldwide, a greater focus on preventive healthcare, and rising demand for diagnostic testing. The continued integration of advanced technologies into healthcare systems is accelerating the adoption of vitamin D diagnostics. With chronic illnesses such as diabetes, autoimmune disorders, cardiovascular diseases, and osteoporosis on the rise, vitamin D testing is becoming a critical part of clinical workflows. Healthcare providers are incorporating these tests into routine diagnostics to manage deficiencies and monitor supplementation outcomes more accurately. Diagnostic labs, payers, and digital health platforms are turning to solutions like LC-MS/MS, ELISA, and chemiluminescence immunoassays for enhanced accuracy and patient monitoring. This is supporting a major shift toward personalized healthcare, where early detection plays a key role. The availability of vitamin D testing in hospitals, clinics, and even at-home setups contributes to increasing accessibility. The expanding focus on chronic disease prevention, maternal and child health, and elderly care programs is further supporting the market's consistent growth trajectory.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.3 Billion |

| Forecast Value | $3 Billion |

| CAGR | 7.3% |

The 25-hydroxy vitamin D test segment held 86.2% share in 2024, as it remains the preferred standard for evaluating vitamin D levels in the blood. This segment is projected to reach USD 2.6 billion by 2034, growing at a CAGR of 7.6%. Its use spans multiple clinical applications, including chronic disease management, routine wellness checkups, elderly care, and nutritional assessments. The test is widely adopted to assess deficiency in individuals with limited sunlight exposure, low dietary intake, or metabolic disorders affecting vitamin D absorption. Its role in both population-wide screenings and targeted diagnostics continues to solidify its market dominance.

The CLIA segment held a 43.5% share in 2024 and is expected to reach USD 1.3 billion by 2034. The growing demand for chemiluminescence immunoassay testing is driven by its superior sensitivity and precision over traditional immunoassay methods. CLIA enables accurate quantification of key vitamin D metabolites, which are essential markers in assessing deficiency-related risks. Its adoption is increasing across both centralized labs and point-of-care testing setups due to its reliability, speed, and scalable throughput.

North America Vitamin D Testing Market held a 37.7% share in 2024, driven by advanced healthcare infrastructure, high patient awareness, and proactive screening initiatives. The region is particularly impacted by widespread vitamin D deficiency, especially in areas with reduced sun exposure. As a result, testing is increasingly integrated into routine health evaluations. Physicians regularly recommend these tests for patients with long-term conditions, contributing to increased demand. Widespread insurance coverage, government health campaigns, and growing home-based diagnostics are further accelerating market expansion across the US and Canada.

Key companies shaping the Global Vitamin D Testing Market include Abbott, Thermo Fisher Scientific, Roche, Danaher (Beckman Coulter), Mindray Medical International, NanoSpeed Diagnostics, Siemens, Diasorin, Randox Laboratories, Bio-Rad Laboratories, Tosoh, Qualigen Therapeutics, EUROIMMUN, bioMerieux, and NanoEnTek. To strengthen their foothold, leading players in the vitamin D testing market are implementing a range of strategic initiatives. Many are focused on expanding their diagnostic portfolios by launching highly sensitive, next-generation assay kits that offer faster turnaround times. Companies are also investing in automation and AI-based analytics for enhanced workflow efficiency and data accuracy. Geographic expansion into high-growth regions is being prioritized through distributor partnerships and local manufacturing.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 Technique trends

- 2.2.4 Indication trends

- 2.2.5 Patient trends

- 2.2.6 Test type trends

- 2.2.7 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Component & technology suppliers

- 3.1.2 Diagnostic device & kit manufacturers

- 3.1.3 Value addition at each stage

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of vitamin D deficiency disorders

- 3.2.1.2 Rising awareness among consumers

- 3.2.1.3 Rise in public health campaigns and reimbursement policies

- 3.2.1.4 Increasing technological advancements

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of advanced diagnostic methods

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion into point-of-care and home testing

- 3.2.3.2 Growth into emerging markets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory scenario

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Reimbursement scenario

- 3.6 Technology landscape

- 3.6.1 Current technological trends

- 3.6.2 Emerging technologies

- 3.7 Future market trends

- 3.8 Pricing analysis, 2024

- 3.9 Patent landscape

- 3.9.1 Patent holder analysis

- 3.10 Clinical guidelines & standardization

- 3.11 Investment & funding trends

- 3.12 Epidemiology scenario

- 3.13 Porter's analysis

- 3.14 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.3.5 Latin America

- 4.3.6 MEA

- 4.4 Competitive positioning matrix

- 4.5 Competitive analysis of major market players

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New service type launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 25-hydroxy vitamin D test

- 5.3 1,25-dihydroxy vitamin D test

Chapter 6 Market Estimates and Forecast, By Technique, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 CLIA

- 6.3 ELISA

- 6.4 LC-MS

- 6.5 Radioimmunoassay

- 6.6 Other techniques

Chapter 7 Market Estimates and Forecast, By Indication, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Vitamin D deficiency

- 7.3 Osteoporosis

- 7.4 Cardiovascular

- 7.5 Rickets

- 7.6 Thyroid disorders

- 7.7 Other indications

Chapter 8 Market Estimates and Forecast, By Patient, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Adult

- 8.3 Pediatric

Chapter 9 Market Estimates and Forecast, By Test Type, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Conventional test

- 9.3 Point-of-care test

Chapter 10 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 10.1 Key trends

- 10.2 Diagnostic laboratories

- 10.3 Hospitals

- 10.4 Homecare

- 10.5 Other end use

Chapter 11 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Netherlands

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 Japan

- 11.4.3 India

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 Middle East and Africa

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Abbott

- 12.2 bioMerieux

- 12.3 Bio-Rad Laboratories

- 12.4 Danaher (Beckman Coulter)

- 12.5 Diasorin

- 12.6 EUROIMMUN

- 12.7 Roche

- 12.8 Mindray Medical International

- 12.9 NanoEnTek

- 12.10 NanoSpeed Diagnostics

- 12.11 Qualigen Therapeutics

- 12.12 Randox Laboratories

- 12.13 Siemens

- 12.14 Thermo Fisher Scientific

- 12.15 Tosoh