|

시장보고서

상품코드

1858869

브랜드화된 주식(Branded Food Staple) 시장 : 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Branded Food Staple Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

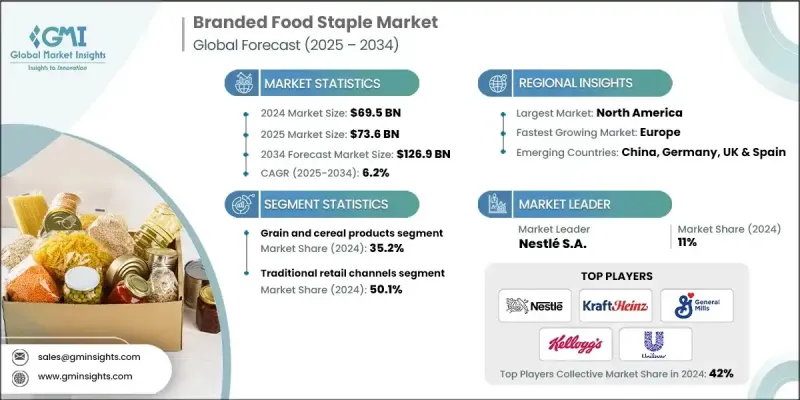

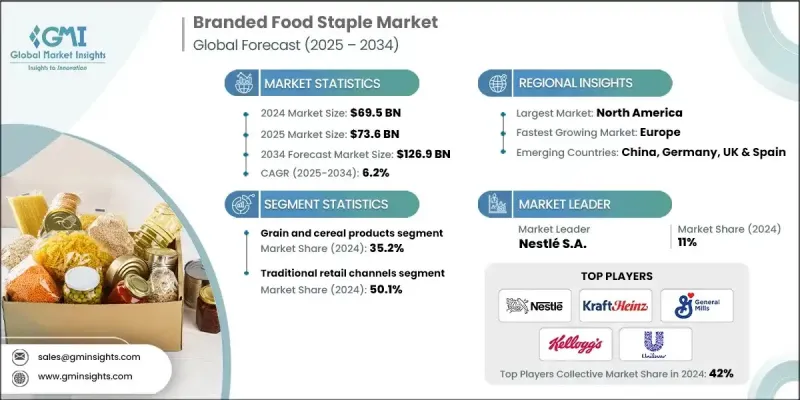

세계의 브랜드화된 주식 시장은 2024년에는 695억 달러로 평가되었고, CAGR 6.2%로 성장할 전망이며, 2034년에는 1,269억 달러에 이를 것으로 추정됩니다.

이 시장은 쌀, 밀가루, 설탕, 식용유, 콩류 등 널리 소비되는 포장된 필수 식품으로 구성되어 있으며, 각각 안정적인 품질과 신뢰할 수 있는 브랜드의 신뢰성을 제공합니다. 세계적인 도시화가 가속화되고 소비자의 습관이 진화함에 따라 식품의 안전성, 추적성, 명확한 영양가를 보장하는 포장된 주식으로의 명확한 변화가 보입니다. 클린 라벨, 영양 강화 식품, 무첨가 식품에 대한 수요 증가는 보다 광범위한 건강 지향의 움직임과 일치하여 브랜드화된 주식의 소비를 더욱 증가시키고 있습니다. 현재 소비자는 대량 생산품이나 포장되지 않은 대체품보다 투명성, 품질 보증 및 편의성을 선호합니다. 브랜드화된 주식은 성숙 시장에서도 신흥 시장에서도 큰 지지를 받고 있는데, 이는 특히 사람들이 보다 바쁜 라이프스타일을 채용해 일상 식생활에 신뢰할 수 있는 브랜드명을 요구하게 되기 때문입니다. 소득 수준의 향상, 식품의 안전성에 대한 의식, 라이프 스타일의 변화가 세계의 소비 동향을 형성하고 있습니다. 시장은 또한 지속 가능한 관행과 환경 친화적인 포장에 대한 수요에 적응하고 있으며, 이는 소비자의 환경 의식 증가를 반영하고 지역 간 제품 선택에 영향을 미칩니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시장 규모 | 695억 달러 |

| 예측 금액 | 1,269억 달러 |

| CAGR | 6.2% |

곡물 및 시리얼 제품 분야는 35.2%의 점유율을 차지했으며, 2034년까지 CAGR 6.5%로 성장이 예측됩니다. 이 부문의 아성은 도시로의 침투, 포장 곡물의 영양 성분에 대한 의식 증가, 건강 지향 증가에 기인합니다. 식용 유지에 대한 수요는 식물 유래의 심장에 좋은 선택에 대한 관심 증가에 의해 뒷받침되어 계속 높습니다. 현재는 오메가3를 강화한 오일과 코코넛, 아마씨, 아보카도 등의 품종이 브랜드 제품으로 제공되고 있으며, 이 제품 카테고리 전체의 확대에 기여하고 있습니다.

전통적인 소매 부문은 2024년에 50.1%의 점유율을 차지했으며, 2034년까지 연평균 복합 성장률(CAGR) 6.3%로 성장할 것으로 예측됩니다. 슈퍼마켓, 현지 식료품점 및 소규모 점포는 세계적으로 주식 식용 식품의 주요 구매 기지로 계속되고 있습니다. 소매업태의 근대화에 따라, 브랜드화된 진열 존, 영양 카운터, 샘플링 스테이션 등 점포내의 업그레이드가 소비자의 관심을 높여, 매장에서의 브랜드 선호를 촉진하고 있습니다.

북미의 브랜드화된 주식 시장은 2024년에 30.3%의 점유율을 차지했으며, 유기농, 클린 라벨, 건강 지향 식품에 대한 기호의 고조가 그 원동력이 되고 있습니다. 이 지역의 동향은 지속 가능한 조달 및 친환경 포장에 대한 관심 증가를 보여 주며, 이는 제품 디자인과 구매 행동 모두에 영향을 미칩니다. 소비자의 건강 의식 및 환경 의식이 높아짐에 따라, 이 지역의 브랜드는 이러한 진화의 기대에 부응하고 장기적인 성장을 보장하기 위해 전략을 조정하고 있습니다.

세계의 브랜드화된 주식 시장을 적극적으로 형성하고 있는 주요 기업은 Coca-Cola Company, Nestle S.A., Mondelez International Inc., PepsiCo Inc., The Hershey Company, McCormick & Company, Inc., Danone S.A., Mars Incorporated, General Mills Inc., The Kellogg's Company, Kraft Heinz Company, Associated British Foods plc (ABF) 및 Unilever 등입니다. 세계 브랜드화된 주식 시장의 발판을 강화하기 위해 주요 기업은 제품 혁신, 지속가능성 및 공급망의 효율성에 중점을 둔 전략적 행동을 수행하고 있습니다. 주요 우선 과제는 유기농, 영양 강화, 식물 유래 주식 등 진화하는 소비자 수요를 충족하는 건강 지향의 선택으로 포트폴리오를 확대하는 것입니다. 브랜드는 또한 환경 친화적인 패키징 솔루션과 환경 목표에 부합하는 책임있는 조달에 투자합니다. 디지털 채널 및 옴니 채널 소매 전략을 활용함으로써 이러한 기업들은 소비자들에게 직접 도달할 수 있도록 노력하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 소비자의 라이프 스타일 및 음식 기호의 변화

- 브랜드 인지 및 신뢰

- 건강 및 웰니스 의식의 고조

- 패키징 및 생산에서 기술의 선진성

- 업계의 잠재적 위험 및 과제

- 원재료 가격 변동

- 프라이빗 브랜드와의 격렬한 경쟁

- 시장 기회

- 건강 지향의 제품 혁신

- 프라이빗 브랜드 파트너십

- 지속 가능한 포장 솔루션

- 신흥 시장에 대한 침투

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 가격 동향

- 지역별

- 제품 카테고리별

- 향후 시장 동향

- 기술 혁신의 전망

- 현재의 기술 동향

- 신흥 기술

- 특허 상황

- 무역 통계(HS코드)(주 : 무역 통계는 주요 국가에 대해서만 제공됨)

- 주요 수입국

- 주요 수출국

- 지속가능성 및 환경 측면

- 지속가능한 실천

- 폐기물 감축 전략

- 생산에서의 에너지 효율

- 환경 친화적인 노력

- 탄소발자국

제4장 경쟁 구도

- 서문

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병 및 인수

- 파트너십

- 신제품 발표

- 확장 계획

제5장 시장 추계 및 예측 : 제품 카테고리별(2021-2034년)

- 주요 동향

- 곡물 및 시리얼 제품

- 쌀 및 쌀 제품

- 밀 및 밀 유래 제품

- 귀리 및 귀리 제품

- 특수 곡물 및 고대 곡물

- 식용 유지

- 식물성 기름

- 올리브 오일 및 고급 오일

- 특수 및 기능성 오일

- 버터 및 마가린 제품

- 설탕 및 감미료

- 정제당 제품

- 천연 및 대체 감미료

- 꿀 및 메이플 제품

- 인공 감미료 시스템

- 소금 및 조미료

- 식탁 소금 및 특수 소금

- 향신료 및 조미료

- 허브 및 천연 조미료

- 민족 및 인터내셔널 조미료

- 통조림 및 보존 식품

- 야채 및 과일 통조림

- 보존 고기 및 해산물

- 피클 및 발효 제품

- 파스타 및 면 제품

- 전통 파스타 제품

- 파스타

- 대체 파스타 및 글루텐 프리 파스타

제6장 시장 추계 및 예측 : 유통 채널별(2021-2034년)

- 주요 동향

- 전통적인 소매 채널

- 슈퍼마켓 및 하이퍼마켓

- 편의점

- 전문 식품점

- 현대적 소매업태

- 할인점

- 유기 및 자연 식품점

- 미식 및 프리미엄 소매

- 전자상거래 및 디지털 채널

- 온라인 식료품 플랫폼

- 소비자 직접 판매

- 정기 구입 서비스

제7장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 기타 라틴아메리카

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

제8장 기업 프로파일

- Associated British Foods plc(ABF)

- Danone SA

- General Mills Inc.

- Kraft Heinz Company

- Mars Incorporated

- McCormick & Company, Inc.

- Mondelez International Inc.

- Nestle SA

- PepsiCo Inc.

- The Coca-Cola Company

- The Hershey Company

- The Kellogg's Company

- Unilever

The Global Branded Food Staple Market was valued at USD 69.5 billion in 2024 and is estimated to grow at a CAGR of 6.2% to reach USD 126.9 billion by 2034.

This market comprises widely consumed, packaged essential food items such as rice, flour, sugar, cooking oils, and pulses, each offering consistent quality and the reliability of trusted brands. As global urbanization accelerates and consumer habits evolve, there's a clear shift toward packaged staples that guarantee food safety, traceability, and defined nutritional value. The rising demand for clean-label, fortified, and additive-free options aligns with the broader health-conscious movement, further amplifying branded staple consumption. Currently, consumers are favoring transparency, quality assurance, and convenience over bulk or unpackaged alternatives. Branded staples are gaining significant traction in both mature and emerging markets, especially as people adopt busier lifestyles and seek trusted names in their everyday diets. Improved income levels, awareness around food safety, and lifestyle changes are shaping consumption trends globally. Markets are also adapting to the demand for sustainable practices and eco-friendly packaging, which reflects growing environmental consciousness among consumers and influences product choices across regions.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $69.5 Billion |

| Forecast Value | $126.9 Billion |

| CAGR | 6.2% |

The grain and cereal products segment held a 35.2% share and is projected to grow at a CAGR of 6.5% through 2034. This segment's stronghold is driven by greater urban penetration, rising awareness of nutritional content in packaged grains, and increasing focus on health-based food selections. Demand for cooking oils and fats remains high, supported by growing interest in plant-based, heart-healthy options. Branded offerings now include oils enriched with omega-3 and varieties such as coconut, flaxseed, and avocado, contributing to the overall expansion of this product category.

The traditional retail segment held a 50.1% share in 2024 and is forecast to grow at a CAGR of 6.3% by 2034. Supermarkets, local grocery stores, and small-scale shops continue to be the primary buying points for staple food items worldwide. With the modernization of retail formats, in-store upgrades like branded display zones, nutrition counters, and sampling stations are elevating consumer engagement and driving brand preference at point-of-sale locations.

North America Branded Food Staple Market held 30.3% share in 2024, driven by the rising preference for organic, clean-label, and health-focused food products. Regional trends show growing interest in sustainable sourcing and eco-friendly packaging, which is influencing both product design and purchasing behavior. As consumers become increasingly health-aware and environmentally conscious, brands in this region are adjusting their strategies to cater to these evolving expectations and ensure long-term growth.

Key players actively shaping the Global Branded Food Staple Market include The Coca-Cola Company, Nestle S.A., Mondelez International Inc., PepsiCo Inc., The Hershey Company, McCormick & Company, Inc., Danone S.A., Mars Incorporated, General Mills Inc., The Kellogg's Company, Kraft Heinz Company, Associated British Foods plc (ABF), and Unilever. To strengthen their foothold in the Global Branded Food Staple Market, leading companies are implementing strategic actions focused on product innovation, sustainability, and supply chain efficiency. A major priority is expanding portfolios with health-forward options such as organic, fortified, or plant-based staples that meet evolving consumer demands. Brands are also investing in eco-friendly packaging solutions and responsible sourcing to align with environmental goals. Leveraging digital channels and omnichannel retail strategies, these companies are enhancing direct-to-consumer reach.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product category

- 2.2.3 Distribution Channel

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Changing Consumer Lifestyles and Dietary Preferences

- 3.2.1.2 Brand Recognition and Trust

- 3.2.1.3 Increasing Health and Wellness Awareness

- 3.2.1.4 Technological Advancements in Packaging and Production

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Price Volatility of Raw Materials

- 3.2.2.2 Intense Competition from Private Labels

- 3.2.3 Market opportunities

- 3.2.3.1 Health-oriented Product Innovation

- 3.2.3.2 Private Label Partnerships

- 3.2.3.3 Sustainable Packaging Solutions

- 3.2.3.4 Emerging Market Penetration

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product category

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) ( Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Product Category, 2021-2034 (USD Million & Units)

- 5.1 Key trends

- 5.2 Grain and cereal products

- 5.2.1 Rice and rice products

- 5.2.2 Wheat and wheat-based products

- 5.2.3 Oats and oat-based products

- 5.2.4 Specialty and ancient grains

- 5.3 Cooking oils and fats

- 5.3.1 Vegetable oils

- 5.3.2 Olive oil and premium oils

- 5.3.3 Specialty and functional oils

- 5.3.4 Butter and margarine products

- 5.4 Sugar and sweeteners

- 5.4.1 Refined sugar products

- 5.4.2 Natural and alternative sweeteners

- 5.4.3 Honey and maple products

- 5.4.4 Artificial sweetener systems

- 5.5 Salt and seasonings

- 5.5.1 Table salt and specialty salts

- 5.5.2 Spice and seasoning blends

- 5.5.3 Herbs and natural seasonings

- 5.5.4 Ethnic and international seasonings

- 5.6 Canned and preserved foods

- 5.6.1 Canned vegetables and fruits

- 5.6.2 Preserved meat and seafood

- 5.6.3 Pickled and fermented products

- 5.7 Pasta and noodle products

- 5.7.1 Traditional pasta products

- 5.7.2 Specialty and artisanal pasta

- 5.7.3 Alternative and gluten-free pasta

Chapter 6 Market Estimates and Forecast, By Distribution Channel, 2021-2034 (USD Million & Units)

- 6.1 Key trends

- 6.2 Traditional retail channels

- 6.2.1 Supermarkets and hypermarkets

- 6.2.2 Convenience stores

- 6.2.3 Specialty food stores

- 6.3 Modern retail formats

- 6.3.1 Discount retailers

- 6.3.2 Organic and natural food stores

- 6.3.3 Gourmet and premium retailers

- 6.4 E-commerce and digital channels

- 6.4.1 Online grocery platforms

- 6.4.2 Direct-to-consumer sales

- 6.4.3 Subscription services

Chapter 7 Market Estimates and Forecast, By Region, 2021-2034 (USD Million & Units)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Rest of Europe

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.4.6 Rest of Asia Pacific

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.5.4 Rest of Latin America

- 7.6 Middle East and Africa

- 7.6.1 Saudi Arabia

- 7.6.2 South Africa

- 7.6.3 UAE

- 7.6.4 Rest of Middle East and Africa

Chapter 8 Company Profiles

- 8.1 Associated British Foods plc (ABF)

- 8.2 Danone S.A.

- 8.3 General Mills Inc.

- 8.4 Kraft Heinz Company

- 8.5 Mars Incorporated

- 8.6 McCormick & Company, Inc.

- 8.7 Mondelez International Inc.

- 8.8 Nestle S.A.

- 8.9 PepsiCo Inc.

- 8.10 The Coca-Cola Company

- 8.11 The Hershey Company

- 8.12 The Kellogg's Company

- 8.13 Unilever