|

시장보고서

상품코드

1858885

풍력 터빈 운영 및 유지보수(O&M) 시장 : 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Wind Turbine Operation and Maintenance Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

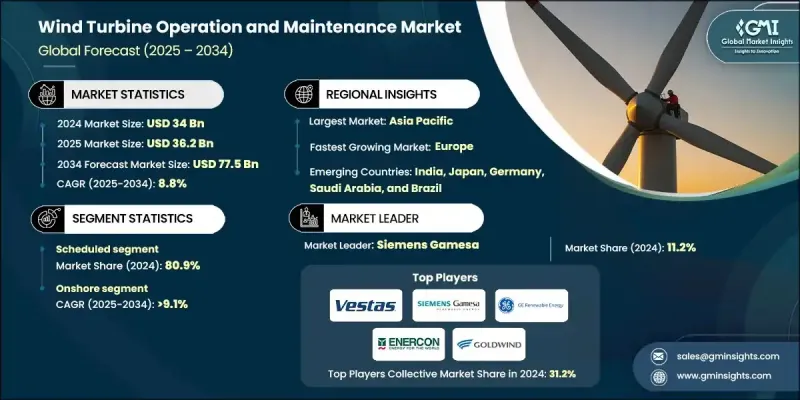

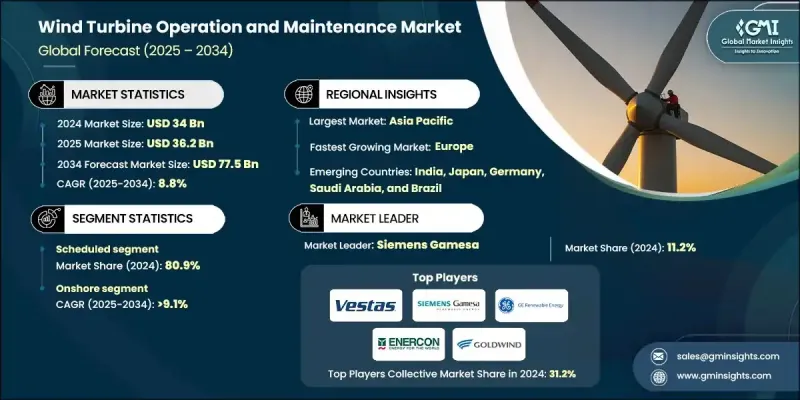

세계의 풍력 터빈 운영 및 유지보수(O&M) 시장은 2024년에는 340억 달러로 평가되었고, CAGR 8.8%로 성장할 전망이며, 2034년에는 775억 달러에 이를 것으로 추정됩니다.

세계의 풍력 발전 인프라는 성숙도를 높이고 있으며 확장 가능하고 비용 효율적인 O&M 서비스 수요가 계속 증가하고 있습니다. 세계의 에너지 포트폴리오 중 풍력 발전이 차지하는 비율이 커짐에 따라 효율적이고 기술적으로 통합된 유지보수의 필요성이 더욱 중요해지고 있습니다. 자동 진단, 머신 러닝, 데이터 구동 시스템의 혁신으로 터빈 효율이 크게 향상되고 운전 휴지 시간이 단축됩니다. 이러한 스마트 툴은 예측 인사이트 및 실시간 모니터링을 제공함으로써 O&M 상황을 재구성합니다. 게다가 에너지 생산자가 지속가능성 및 수명주기 효율성으로 이동함에 따라 사전 활성 유지보수 전략의 역할이 급속히 증가하고 있습니다. 예측 분석 및 원격 액세스 도구는 최소한의 중단과 최적화된 자산 성능을 보장하기 위해 기존의 유지보수 모델을 대체합니다. 드론 기술 및 로봇에 의한 자동화는 특히 손이 닿지 않는 곳에서 터빈을 정비하는 방법을 더욱 바꾸고 있습니다. 이러한 진보는 보다 합리적이고 지속가능한 O&M 생태계를 촉진하고 육상 및 해양 자산 모두에서 시장의 꾸준한 확대를 강화하고 있습니다. 디지털화는 청정 에너지에 대한 정책 지원과 함께 세계 시장 전체에서 풍력 터빈 서비스의 진화를 가속화하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시장 규모 | 340억 달러 |

| 예측 금액 | 775억 달러 |

| CAGR | 8.8% |

2024년에는 정기 유지보수 서비스 분야가 80.9%의 점유율을 차지하였고, 2034년까지 CAGR 9.3%로 성장이 예측됩니다. 이 이점은 디지털 플랫폼에 지원되는 사전 활성 서비스 모델의 보급을 반영합니다. 사업자는 터빈 수명주기를 최적화하고 비용이 많이 드는 고장을 피하기 위해 고급 진단 및 성능 데이터를 활용합니다. 풍력에너지 자산이 노후화되고, 원격지 및 해안에 새로운 설비가 출현함에 따라 복잡한 보수 작업을 지원하는 스마트한 스케줄링, 자산 추적, 예측적 인사이트에 대한 수요가 높아지고 있습니다.

육상 부문은 2024년에 88.5%의 점유율을 차지했으며, 2025-2034년 CAGR 9.1%로 성장할 것으로 예측됩니다. 육상 풍력발전소는 유지보수 비용 절감 및 신뢰성 향상을 위해 디지털 변혁에 주력하고 있습니다. 오래된 풍력발전소에서는 보다 전문적인 케어가 필요하기 때문에 사업자는 AI 주도의 분석, IoT 대응 센서, 고도의 감시 툴을 도입해 부품의 고장을 예측해, 터빈의 수명을 연장하고 있습니다. 이러한 커넥티드의 프로액티브 유지보수 솔루션으로의 전환은 운영자가 워크플로우를 간소화하고, 가동 시간을 향상시키며, 자산으로부터 장기적인 가치를 끌어낼 수 있게 합니다.

유럽의 풍력 터빈 운영 및 유지보수(O&M) 시장은 2034년까지 190억 달러에 달할 전망입니다. 이 성장은 해상 풍력 발전 프로젝트에 대한 투자 증가 및 AI 기반 진단, 로봇 공학, 원격 제어 시스템과 같은 지능형 기술의 통합 증가로 추진됩니다. 이 지역 육상 풍력발전의 대부분은 리파워링(재출력화)을 진행하고 있으며, 요구에 맞춘 O&M 서비스에 대한 새로운 수요가 탄생하고 있습니다. 정부의 정책, 환경 목표, 저배출 에너지원에 대한 규제의 뒷받침이 사업자에게 스마트하고 지속 가능한 유지보수 솔루션에 대한 투자를 촉구하고, 이것이 시장 전체의 성장을 뒷받침하고 있습니다.

세계의 풍력 터빈 운영 및 유지보수(O&M) 시장에서 활약하는 주요 기업은 Vestas Wind Systems A/S, Enercon GmbH, Suzlon Energy Ltd, Fred.Olsen Windcarrier, RTS Wind AG, B9 Energy Group, Moventas Gears Oy, GoldWind, Deutsche Windtechnik, ABB Ltd. Bilfinger Inc., Dana SAC UK Ltd., Global Wind Service company, ZF Friedrichshafen AG, Mistras Group, Mitarsh Energy, NORDEX SE, REETEC, Siemens Gamesa, Blue Water Shipping 등입니다. 세계의 풍력 터빈 운영 및 유지보수(O&M) 시장에서 발판을 굳히기 위해 대기업은 디지털 전환을 도입하여 첨단 기술에 투자하고 있습니다. 각 회사는 AI, 빅데이터, 센서 기반 진단을 활용하여 터빈의 건전성을 실시간으로 모니터링하는 예지보전 플랫폼의 채용을 늘리고 있습니다. 소프트웨어 제공업체 및 혁신 기업과의 전략적 협업은 자동화, 무인 항공기, 로봇 공학을 서비스 제공에 통합하여 비용 절감 및 작업자의 안전성 향상을 지원합니다.

자주 묻는 질문

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

- 업계 에코시스템

- 규제 상황

- 업계에 미치는 영향요인

- 성장 촉진요인

- 업계의 잠재적 위험 및 과제

- 성장 가능성 분석

- 가격 동향 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서문

- 기업의 시장 점유율 분석 : 지역별

- 북미

- 유럽

- 아시아태평양

- 중동 및 아프리카

- 라틴아메리카

- 전략적 대시보드

- 전략적 노력

- 기업 벤치마킹

- 혁신 및 기술 상황

제5장 시장 규모 및 예측 : 유형별(2021-2034년)

- 주요 동향

- 예정

- 예정 외

제6장 시장 규모 및 예측 : 소재지별(2021-2034년)

- 주요 동향

- 온쇼어

- 오프쇼어

제7장 시장 규모 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 프랑스

- 스웨덴

- 영국

- 스페인

- 네덜란드

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 중동 및 아프리카

- 이집트

- 남아프리카

- 모로코

- 사우디아라비아

- 라틴아메리카

- 브라질

- 멕시코

- 칠레

제8장 기업 프로파일

- ABB

- B9 Energy Group

- Bilfinger Inc.

- Dana SAC UK Ltd

- Deutsche Windtechnik

- Enercon GmbH

- Fred. Olsen Windcarrier

- Global Wind Service company

- GoldWind

- Mistras Group,

- Mitarsh Energy

- Moventas Gears Oy

- NORDEX SE

- REETEC

- RTS Wind AG

- Siemens Gamesa

- Suzlon Energy Limited

- Suzlon Energy Ltd

- Vestas Wind Systems A/S

- ZF Friedrichshafen AG

The Global Wind Turbine Operation and Maintenance Market was valued at USD 34 billion in 2024 and is estimated to grow at a CAGR of 8.8% to reach USD 77.5 billion by 2034.

The increasing maturity of global wind energy infrastructure continues to drive demand for scalable and cost-effective O&M services. As wind power claims a larger share of the global energy portfolio, the need for efficient, technology-integrated maintenance becomes more critical. Innovations in automated diagnostics, machine learning, and data-driven systems are significantly enhancing turbine efficiency and reducing operational downtime. These smart tools are reshaping the O&M landscape by offering predictive insights and real-time monitoring. Additionally, with energy producers shifting toward sustainability and lifecycle efficiency, the role of proactive maintenance strategies is growing rapidly. Predictive analytics and remote access tools are replacing traditional maintenance models to ensure minimal disruptions and optimized asset performance. Drone technology and robotic automation are further transforming the way turbines are serviced, especially in hard-to-reach locations. These advancements are fostering a more streamlined and sustainable O&M ecosystem, reinforcing the market's steady expansion across both onshore and offshore assets. Digitalization, combined with policy support for clean energy, continues to accelerate the evolution of wind turbine servicing across global markets.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $34 Billion |

| Forecast Value | $77.5 Billion |

| CAGR | 8.8% |

In 2024, the scheduled maintenance services segment held an 80.9% share and is forecasted to grow at a CAGR of 9.3% through 2034. This dominance reflects the widespread adoption of proactive service models supported by digital platforms. Operators are increasingly using advanced diagnostics and performance data to optimize turbine life cycles and avoid costly breakdowns. As wind energy assets age and new installations emerge in remote or offshore areas, demand is rising for smart scheduling, asset tracking, and predictive insights to support complex maintenance operations.

The onshore segment held an 88.5% share in 2024 and is expected to grow at a CAGR of 9.1% from 2025 to 2034. Onshore wind farms are focusing on digital transformation to reduce maintenance costs and improve reliability. With older wind farms requiring more specialized care, operators are deploying AI-driven analytics, IoT-enabled sensors, and advanced monitoring tools to anticipate component failures and extend turbine life. This shift toward connected, proactive maintenance solutions allows operators to streamline workflows, improve uptime, and drive long-term value from their assets.

Europe Wind Turbine Operation and Maintenance Market will reach USD 19 billion by 2034. This growth is propelled by rising investments in offshore wind projects and increasing integration of intelligent technologies like AI-based diagnostics, robotics, and remote control systems. Many onshore fleets across the region are undergoing repowering, which is creating fresh demand for tailored O&M services. Government policy, environmental targets, and regulatory backing for low-emission energy sources are encouraging operators to invest in smart and sustainable maintenance solutions, which in turn boosts overall market growth.

Leading companies active in the Global Wind Turbine Operation and Maintenance Market include Vestas Wind Systems A/S, Enercon GmbH, Suzlon Energy Ltd, Fred. Olsen Windcarrier, RTS Wind AG, B9 Energy Group, Moventas Gears Oy, GoldWind, Deutsche Windtechnik, ABB Ltd., Bilfinger Inc., Dana SAC UK Ltd, Global Wind Service company, ZF Friedrichshafen AG, Mistras Group, Mitarsh Energy, NORDEX SE, REETEC, Siemens Gamesa, and Blue Water Shipping. To strengthen their foothold in the Global Wind Turbine Operation and Maintenance Market, major players are embracing digital transformation and investing in advanced technologies. Companies are increasingly adopting predictive maintenance platforms that utilize AI, big data, and sensor-based diagnostics to monitor turbine health in real time. Strategic collaborations with software providers and tech innovators help integrate automation, drones, and robotics into their service offerings, reducing costs and improving worker safety.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.1.3 Base estimates and calculations

- 1.1.4 Base year calculation

- 1.1.5 Key trends for market estimates

- 1.2 Forecast model

- 1.3 Primary research & validation

- 1.3.1 Primary sources

- 1.4 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

- 2.2 Business trends

- 2.3 Type trends

- 2.4 Location trends

- 2.5 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Price trend analysis

- 3.6 Porter's analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL analysis

Chapter 4 Competitive landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2024

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Strategic dashboard

- 4.4 Strategic initiatives

- 4.5 Company benchmarking

- 4.6 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Type, 2021 - 2034 (USD Billion)

- 5.1 Key trends

- 5.2 Scheduled

- 5.3 Unscheduled

Chapter 6 Market Size and Forecast, By Location, 2021 - 2034 (USD Billion)

- 6.1 Key trends

- 6.2 Onshore

- 6.3 Offshore

Chapter 7 Market Size and Forecast, By Region, 2021 - 2034 (USD Billion)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 France

- 7.3.3 Sweden

- 7.3.4 UK

- 7.3.5 Spain

- 7.3.6 Netherlands

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 Australia

- 7.5 Middle East & Africa

- 7.5.1 Egypt

- 7.5.2 South Africa

- 7.5.3 Morocco

- 7.5.4 Saudi Arabia

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Mexico

- 7.6.3 Chile

Chapter 8 Company Profiles

- 8.1 ABB

- 8.2 B9 Energy Group

- 8.3 Bilfinger Inc.

- 8.4 Dana SAC UK Ltd

- 8.5 Deutsche Windtechnik

- 8.6 Enercon GmbH

- 8.7 Fred. Olsen Windcarrier

- 8.8 Global Wind Service company

- 8.9 GoldWind

- 8.10 Mistras Group,

- 8.11 Mitarsh Energy

- 8.12 Moventas Gears Oy

- 8.13 NORDEX SE

- 8.14 REETEC

- 8.15 RTS Wind AG

- 8.16 Siemens Gamesa

- 8.17 Suzlon Energy Limited

- 8.18 Suzlon Energy Ltd

- 8.19 Vestas Wind Systems A/S

- 8.20 ZF Friedrichshafen AG