|

시장보고서

상품코드

1858994

특수 의료용 의자 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Specialty Medical Chairs Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

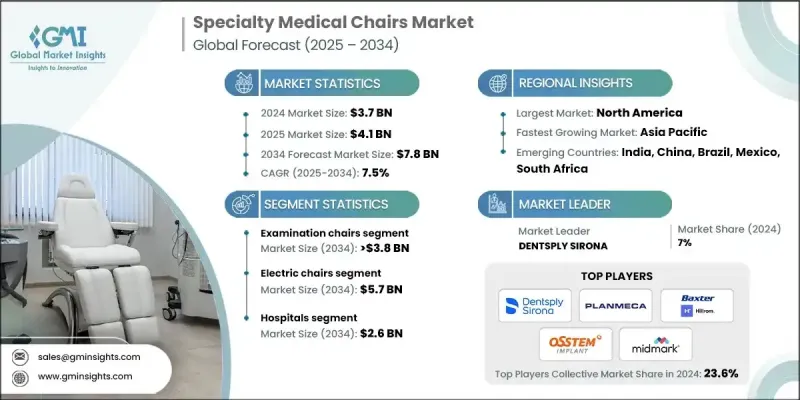

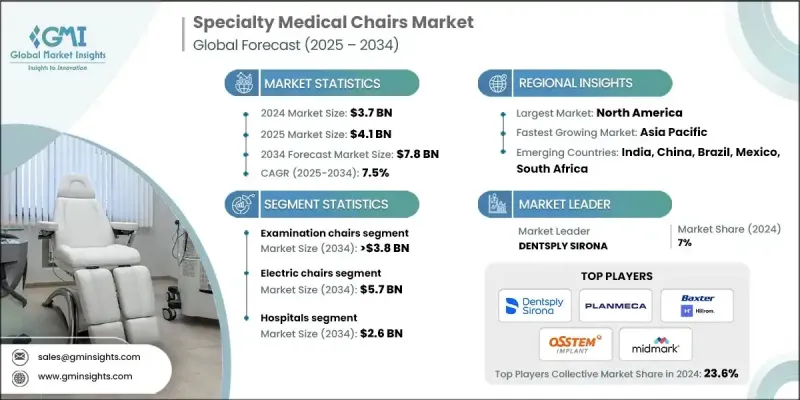

세계의 특수 의료용 의자 시장 규모는 2024년에 37억 달러로 평가되었고, CAGR 7.5%를 나타내 2034년에는 78억 달러에 이를 것으로 예측되고 있습니다.

시장 확대의 원동력은 환자 진료와 임상 효율을 모두 향상시키는 고급 의료 장비에 대한 수요가 증가하고 있습니다. 특수 의료용 의자는 치료 중 편안함, 기능성 및 안전성을 향상시키고 여러 의료 분야에 필수적입니다. 이 의자는 치과, 안과, 이비인후과, 투석 및 재활 치료에 점점 더 통합되어 워크 플로우를 최적화하고 더 나은 치료 결과를 지원합니다. 기술 혁신, 자동화 및 디지털 플랫폼과의 통합을 통해 이러한 의자는 특정 환자의 요구에 적응할 수 있는 스마트 의료기기로 변모하고 있습니다. 의료 서비스 제공업체는 위생 관리, 감염 관리 및 인체공학적 지원에 대한 최신 기준을 준수하는 장비를 선호합니다. 외래 서비스나 재택 치료로의 변화도, 운반이 가능하고 사용하기 편리하고, 다용도에 사용할 수 있는 의자 수요를 밀어 올리고 있습니다. 특히 라틴아메리카와 아시아태평양에서는 건강 관리 인프라에 대한 투자가 시장 보급을 뒷받침하고 있습니다. 한편, 연구개발 노력과 제품개발은 품질 향상과 규제 기대에 부응하기 위한 중심적 존재입니다. 의료 제공업체는 병원, 전문 치료실, 외래 시설에서 환자의 경험을 개선하면서 더 나은 임상 가치를 제공하는 것을 목표로 합니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시장 규모 | 37억 달러 |

| 예측 금액 | 78억 달러 |

| CAGR | 7.5% |

전동 의자 분야는 2024년에 70.4%의 점유율을 차지했고, 2034년까지 57억 달러를 창출할 것으로 예측됩니다. 전동 의자의 이점은 전자 포지셔닝, 리클라이닝, 높이 조절과 같은 전동 보조 기능에 대한 필요성 증가를 반영하여 환자의 안전성과 작동 편의성을 크게 향상시킵니다. 이러한 의자는 수술실, 회복실, 물리치료센터 등 지속적인 사용이 요구되는 의료환경에서 널리 채용되고 있습니다. 환자나 간병인에게 부담을 최소화하면서 장시간의 처치를 서포트할 수 있기 때문에 임상 현장 전체에서 선호되는 솔루션이 되고 있습니다.

병원 분야는 2024년에 35%의 점유율을 차지했으며, 2034년에는 26억 달러에 이를 것으로 예측됩니다. 이 부문의 성장은 특히 급성장 경제권의 건강 관리 인프라 확장과 병원 통합 동향과 밀접하게 관련되어 있습니다. 순환기과, 신경과, 종양과 등의 진료과나 집중 치료실, 응급 서비스 등에서 사용할 수 있는 내구성과 적응성이 뛰어난 의료용 의자 수요가 높아지고 있습니다. 병원에서는 환자 수가 많은 환경에서 진화하는 임상 요구에 대응하는 오래 지속되는 장비를 선호하는 경향이 커지고 있습니다.

북미의 특수 의료용 의자 시장은 2024년 35%의 점유율을 차지했습니다. 심혈관 질환, 관절염, 당뇨병과 같은 만성 질환의 꾸준한 증가는 장기 간호의 필요성을 높이고 첨단 좌석 솔루션에 대한 요구를 높입니다. 미국에서 의료비 증가는 환자 중심 인프라와 서비스로의 광범위한 변화를 반영합니다. 성장을 지원하는 것은 병원에 대한 투자 증가, 특수 장비 채택 확대, 의료 센터 및 클리닉의 치료 능력 확대입니다.

세계의 특수 의료용 의자 시장에서 주요 시장 진출기업은 OSSTEM, Midmark, Hill Laboratories, Baxter, A-dec, MARCO, PLANMECA, CLINTON INDUSTRIES, ActiveAid, Dentsply Sirona, Champion Healthcare Solutions, Lemi MD, FRESENIMOS MEDICAL CARE MedizinTechnik, DENTALEZ, TOPCON 등이 있습니다. 세계 특수 의료용 의자 시장의 주요 기업은 타겟 제품 개발, 합병, 지역 확대를 통해 경쟁력을 강화하고 있습니다. 많은 기업들이 연구 개발에 많은 투자를 하고, 인체공학, 디지털 제어 시스템, 첨단 안전 기능을 갖춘 의자를 설계하고 있습니다. 의료 제공업체 및 의료기관과의 전략적 파트너십을 통해 이들 기업은 제품 능력을 임상 요구사항에 맞출 수 있습니다. 또한 지역 수요에 부응하고 공급망에 대한 의존도를 줄이기 위해 신흥국의 제조 기지를 확대하는 기업도 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 업계 생태계 분석

- 업계에 미치는 영향요인

- 성장 촉진요인

- 전문 클리닉, 혈액 은행, 급환 센터 증가

- 기술의 진보와 전동 의자 수요

- 노년 인구 증가와 재활의 필요성

- 외래 수술 증가

- 업계의 잠재적 리스크 및 과제

- 전문 기기의 고비용

- 한정된 상환정책

- 시장 기회

- 외래·재택 헬스 케어의 확대

- 의료 관광의 성장

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 향후 시장 동향

- 재택 헬스 케어와 외래 환자 확대

- 스마트 기술과 커넥티드 기술의 통합

- 인체공학에 근거한 적응형 디자인에 대한 수요 증가

- 기술 동향

- 현재의 기술 동향

- 휴대형 및 재택형의 특수 의료용 의자의 성장

- 원격 모니터링을 가능하게 하는 디지털 헬스 플랫폼

- 환자 친화적인 조절 가능하고 자동화 된 특수 의자

- 새로운 기술

- AI를 활용한 사용상황 분석과 예지보전

- 커넥티드와 IoT 대응의 특수 의료용 의자

- 개인화된 구성을 가진 적응형 의자와 스마트 의자

- 현재의 기술 동향

- 가격 분석 : 지역별(2024년)

- 업계의 진화

- 밸류체인 분석

- 고객 경험의 변화와 저니 최적화

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서론

- 기업 매트릭스 분석

- 기업의 시장 점유율 분석

- 세계

- 북미

- 유럽

- 아시아태평양

- 경쟁 포지셔닝 매트릭스

- 주요 시장 기업의 경쟁 분석

- 주요 발전

- 합병 및 인수

- 파트너십

- 새로운 서비스 유형의 출시

- 확장 계획

제5장 시장 추계·예측 : 제품별(2021-2034년)

- 주요 동향

- 진찰 의자

- 치과

- 산부인과

- 투석

- 안과

- 피부과

- 채혈

- 유방촬영

- 기타 진찰 의자

- 치료 의자

- 치과

- 안과

- 이비인후과

- 피부과

- 기타 치료 의자

- 재활용 의자

- 노인용 의자

- 소아용 의자

- 비만용 의자

- 기타 재활용 의자

제6장 시장 추계·예측 : 유형별(2021-2034년)

- 주요 동향

- 전동 의자

- 수동 의자

제7장 시장 추계·예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 병원

- 진료소

- 외래 수술 센터(ASC)

- 주입 센터

- 응급 진료

- 재활 센터

- 메디컬 스파

- 재택 치료

- 기타 최종 용도

제8장 시장 추계·예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제9장 기업 프로파일

- ActiveAid

- A-dec

- ATMOS MedizinTechnik

- Baxter

- Champion Healthcare Solutions

- CLINTON INDUSTRIES

- DENTALEZ

- Dentsply Sirona

- FRESENIUS MEDICAL CARE

- Hill Laboratories

- Lemi MD

- MARCO

- Midmark

- OSSTEM

- PLANMECA

- TOPCON

The Global Specialty Medical Chairs Market was valued at USD 3.7 billion in 2024 and is estimated to grow at a CAGR of 7.5% to reach USD 7.8 billion by 2034.

Market expansion is driven by rising demand for advanced healthcare equipment that enhances both patient care and clinical efficiency. Specialty medical chairs are essential across multiple medical disciplines, providing improved comfort, functionality, and safety during treatments. These chairs are increasingly integrated into dental, ophthalmology, ENT, dialysis, and rehabilitation procedures, optimizing workflow and supporting better therapeutic outcomes. Technological innovation, automation, and integration with digital platforms have transformed these chairs into smart medical assets, capable of adjusting to specific patient needs. Healthcare providers are prioritizing equipment that aligns with modern standards for hygiene, infection control, and ergonomic support. The shift toward outpatient services and in-home treatment options is also pushing demand for portable, user-friendly, and multi-use chairs. Investments in healthcare infrastructure, especially across Latin America and Asia-Pacific are fueling broader market adoption. Meanwhile, R&D efforts and product development are central to enhancing quality and compliance with regulatory expectations. Providers aim to deliver better clinical value while improving patient experiences across hospitals, specialty care units, and ambulatory facilities.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.7 Billion |

| Forecast Value | $7.8 Billion |

| CAGR | 7.5% |

The electric chairs segment held a 70.4% share in 2024 and is projected to generate USD 5.7 billion by 2034. Their dominance reflects the rising need for power-assisted features like electronic positioning, recline, and height adjustment, which significantly enhance patient safety and operational convenience. These chairs are widely adopted in healthcare environments that demand continuous usage, including surgical suites, recovery rooms, and physical therapy centers. Their ability to support prolonged procedures with minimal strain on patients and caregivers makes them a preferred solution across clinical settings.

The hospital segment held a 35% share in 2024 and is anticipated to reach USD 2.6 billion by 2034. Growth in this segment is closely tied to the expansion of healthcare infrastructure and hospital consolidation trends, particularly in fast-growing economies. Demand is rising for durable and adaptable medical chairs that can be used across departments such as cardiology, neurology, and oncology, as well as in intensive care units and emergency services. Hospitals increasingly prioritize long-lasting equipment that meets the evolving clinical needs of high-patient-volume environments.

North America Specialty Medical Chairs Market held a 35% share in 2024. A steady rise in chronic conditions such as cardiovascular disease, arthritis, and diabetes is driving long-term care requirements and increasing the need for advanced seating solutions. In the U.S., escalating healthcare expenditures reflect a broader shift toward patient-centered infrastructure and services. Growth is supported by rising investments in hospitals, greater adoption of specialized equipment, and expanded treatment capacity across medical centers and clinics.

Key industry participants in the Global Specialty Medical Chairs Market include OSSTEM, Midmark, Hill Laboratories, Baxter, A-dec, MARCO, PLANMECA, CLINTON INDUSTRIES, ActiveAid, Dentsply Sirona, Champion Healthcare Solutions, Lemi MD, FRESENIUS MEDICAL CARE, ATMOS MedizinTechnik, DENTALEZ, and TOPCON. Major companies in the Global Specialty Medical Chairs Market are enhancing their competitive position through targeted product development, mergers, and regional expansion. Many are investing heavily in R&D to design chairs with enhanced ergonomics, digital control systems, and advanced safety features. Strategic partnerships with healthcare providers and institutions allow these firms to align product capabilities with clinical requirements. Some players are also expanding their manufacturing presence in emerging economies to meet regional demand and reduce supply chain dependencies.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 Type trends

- 2.2.4 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing number of specialty clinics, blood banks, and urgent care centers

- 3.2.1.2 Technological advancements and demand for powered chairs

- 3.2.1.3 Growing geriatric population and need for rehab procedures

- 3.2.1.4 Rising ambulatory surgical procedures

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of specialized equipment

- 3.2.2.2 Limited reimbursement policies

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of outpatient and home healthcare

- 3.2.3.2 Medical tourism growth

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Future market trends

- 3.5.1 Expansion in home healthcare and outpatient settings

- 3.5.2 Integration of smart and connected technologies

- 3.5.3 Rising demand for ergonomic and adaptive designs

- 3.6 Technology landscape

- 3.6.1 Current technological trends

- 3.6.1.1 Growth of portable and home-based specialty medical chairs

- 3.6.1.2 Digital health platforms enabling remote monitoring

- 3.6.1.3 Patient-friendly adjustable and automated specialty chairs

- 3.6.2 Emerging technologies

- 3.6.2.1 AI-powered usage analytics and predictive maintenance

- 3.6.2.2 Connected and IoT-enabled specialty medical chairs

- 3.6.2.3 Adaptive and smart chairs with personalized configurations

- 3.6.1 Current technological trends

- 3.7 Pricing analysis, by region, 2024

- 3.8 Industry evolution

- 3.9 Value chain analysis

- 3.10 Customer experience transformation & journey optimization

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.4 Competitive positioning matrix

- 4.5 Competitive analysis of major market players

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New service type launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Examination chairs

- 5.2.1 Dental

- 5.2.2 OB/GYN

- 5.2.3 Dialysis

- 5.2.4 Ophthalmic

- 5.2.5 Dermatology

- 5.2.6 Blood drawing

- 5.2.7 Mammography

- 5.2.8 Other examination chairs

- 5.3 Treatment chairs

- 5.3.1 Dental

- 5.3.2 Ophthalmic

- 5.3.3 ENT

- 5.3.4 Dermatology

- 5.3.5 Other treatment chairs

- 5.4 Rehabilitation chairs

- 5.4.1 Geriatric chairs

- 5.4.2 Pediatric chairs

- 5.4.3 Bariatric chairs

- 5.4.4 Other rehabilitation chairs

Chapter 6 Market Estimates and Forecast, By Type, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Electric chairs

- 6.3 Manual chairs

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Clinics

- 7.4 Ambulatory surgical centers (ASCs)

- 7.5 Infusion center

- 7.6 Urgent care

- 7.7 Rehabilitation centers

- 7.8 Medical spa

- 7.9 Home care settings

- 7.10 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 ActiveAid

- 9.2 A-dec

- 9.3 ATMOS MedizinTechnik

- 9.4 Baxter

- 9.5 Champion Healthcare Solutions

- 9.6 CLINTON INDUSTRIES

- 9.7 DENTALEZ

- 9.8 Dentsply Sirona

- 9.9 FRESENIUS MEDICAL CARE

- 9.10 Hill Laboratories

- 9.11 Lemi MD

- 9.12 MARCO

- 9.13 Midmark

- 9.14 OSSTEM

- 9.15 PLANMECA

- 9.16 TOPCON