|

시장보고서

상품코드

1859019

액체생검 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Liquid Biopsy Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

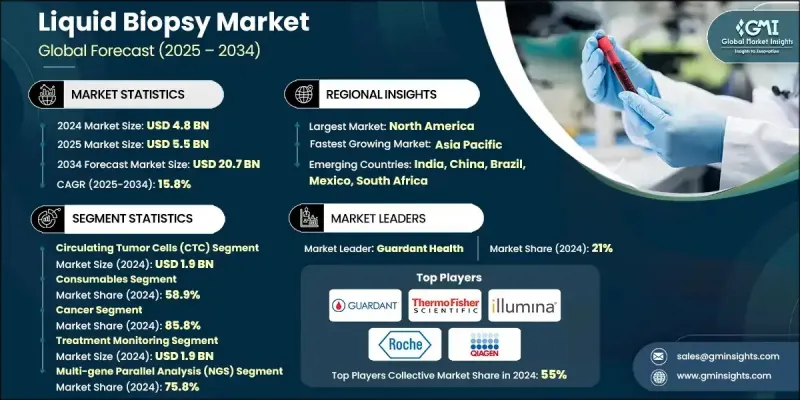

세계의 액체생검 시장은 2024년에는 48억 달러로 평가되었고 CAGR 15.8%를 나타내 2034년에는 207억 달러에 이를 것으로 추정되고 있습니다.

이 성장을 뒷받침하는 것은 암 진단의 진보, 비침습적 수법으로의 변화, 암 이환율 증가, 조기 발견에 대한 의식의 고조입니다. 헬스케어 시스템이 전 세계적으로 인프라에 투자하고 스크리닝에 대한 액세스를 확대함에 따라 액체생검와 같은 확장 가능하고 정확한 도구에 대한 수요는 계속 가속화되고 있습니다. 조기 발견과 정밀의료에 대한 관심 증가는 액체생검를 임상 현장에 통합하기위한 비옥 한 토양을 생산하고 있습니다. 이 검사는 체액으로부터 직접 무세포 DNA, 순환 종양 세포, 세포외 소포 등의 종양 유래의 바이오마커를 검출·분석할 수 있어 기존의 조직 생검을 대신하는 보다 안전하고 신속한 방법을 제공합니다. 액체생검는 암 진단, 돌연변이 추적, 치료 모니터링에 응용되어 특히 고위험 취약한 환자 집단에 있어서 획기적인 솔루션임이 증명되고 있습니다. 수술의 위험을 최소화하면서 실용적인 지식을 얻을 수 있기 때문에 연구 기관, 병원, 진단 실험실에서 채택이 확산되고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시장 규모 | 48억 달러 |

| 예측 금액 | 207억 달러 |

| CAGR | 15.8% |

2024년, 순환 종양 세포 부문은 19억 달러를 창출했습니다. 원발성 종양에서 벗겨지고 혈류를 타고 이동하는 이러한 세포는 종양의 역학을 실시간으로 밝히는 데 중요합니다. 이미징 플랫폼에서 마이크로플루이딕스공학에 이르기까지 CTC를 분리하고 분석하는 데 사용되는 기술은 임상의가 종양의 진화, 내성 메커니즘 및 유전자 프로파일을 이해할 수 있게 합니다. CTC의 비침범성 특성과 실시간 모니터링에서의 역할은 CTC를 액체 생체 생태계의 점점 더 중요한 구성요소로 삼아 임상적 관련성을 넓히고 있습니다.

암 응용 분야는 2024년 85.8%의 점유율을 차지했습니다. 세계적인 암 이환율의 꾸준한 상승에 의해 보다 신속하고 저침습, 고정밀도의 진단 방법에 대한 수요가 계속 증가하고 있습니다. 액체 생검은 악성 종양의 조기 발견, 보다 효과적인 치료법의 조정, 수술적 개입을 필요로 하지 않는 반응 모니터링의 가능성을 제공합니다. 종양학에서 액체생검의 채용이 확대되고 있는 배경에는 진단까지의 시간을 단축하고 치료 결과를 개선하는 보다 개별화된 환자 중심의 치료 전략의 필요성이 있습니다.

2024년 북미의 액체생검 시장 규모는 20억 달러에 달했고, 2034년에는 84억 달러에 이를 것으로 예측됩니다. 이 지역의 리더십은 강력한 생명 공학 연구 생태계, 종양학에 대한 정부의 엄청난 투자, 고급 진단 옵션에 대한 수요 증가로 인한 것입니다. 임상 및 연구 환경에서 높은 채용률, 정기적인 제품 혁신 및 승인은이 지역의 지위를 확고하게합니다. 환자와 의료 제공업체의 의식의 높아짐과 공적·민간 자금에 지지된 견고한 R&D 파이프라인이 이 지역의 성장에 기세를 주고 있습니다.

세계의 액체생검 시장을 형성하는 주요 기업으로는 Myriad Genetics, BIOCEPT, Thermo Fisher Scientific, Guardant Health, F. Hoffmann La Roche, Menarini Silicon Biosystems, Lucene Health, Oncinmune, Illumina, EPIGENOMICS, Freenome Holdings, Laboratories, MDxHealth, Angle 등이 있습니다. 액체생검 시장의 각 회사는 시장에서의 지위를 구축하고 지키기 위한 다면적인 전략을 전개하고 있습니다. 주요 초점은 조기 암 검출 및 모니터링 솔루션의 연구 개발 파이프라인의 확대입니다. 연구기관 및 병원과의 전략적 제휴는 임상 검증을 가속화하고 새로운 기술에 대한 접근을 확대하는 데 도움이 됩니다. 많은 기업들이 바이오마커 검출의 정확성을 향상시키고 해석을 간소화하기 위해 AI 중심 플랫폼을 개발하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 업계에 미치는 영향요인

- 성장 촉진요인

- 암 진단에서 끊임없는 기술 진보

- 비침습적 질환 진단에의 기호의 고조

- 세계의 암 이환율 증가

- 질병의 조기 진단에 관한 의식의 고조

- 업계의 잠재적 위험 및 과제

- 엄격한 규제 프레임워크

- 숙련된 전문가의 부족

- 시장 기회

- 멀티암 조기 발견(MCED) 검사 확대

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 기술적 진보

- 현재의 기술 동향

- 신흥기술

- 공급망 분석

- 상환 시나리오

- 가격 분석(2024년)

- 향후 시장 동향

- 갭 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병과 인수

- 파트너십 및 협업

- 신제품 발표

- 확장 계획

제5장 시장 추계·예측 : 바이오 마커별(2021-2034년)

- 주요 동향

- 순환 종양 세포(CTC)

- 순환 종양 DNA

- 무세포 DNA

- 세포외 소포

- 기타 바이오마커

제6장 시장 추계·예측 : 제품별(2021-2034년)

- 주요 동향

- 소모품

- 키트 및 시약

- 분석 및 패널

- 기기

- 서비스

제7장 시장 추계·예측 : 적응 질환별(2021-2034년)

- 주요 동향

- 암

- 폐암

- 유방암

- 대장암

- 전립선암

- 기타 암

- 비암성 질환

- 비침습적 산전 검사

- 장기 이식

- 감염성 질환 검사

제8장 시장 추계·예측 : 용도별(2021-2034년)

- 주요 동향

- 치료 모니터링

- 예후 및 재발 모니터링

- 치료 선택

- 진단 및 스크리닝

제9장 시장 추계·예측 : 기술별(2021-2034년)

- 주요 동향

- 다중 유전자 병렬 분석(NGS)

- 단일 유전자 분석(PCR 마이크로어레이)

제10장 시장 추계·예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 병원

- 연구 실험실

- 임상 실험실

- 기타 최종 사용

제11장 시장 추계·예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

제12장 기업 프로파일

- Angle

- BIOCEPT

- Bio-Rad Laboratories

- EPIGENOMICS

- F. Hoffmann La Roche

- Freenome Holdings

- Guardant Health

- Illumina

- Lucene Health

- MDxHealth

- Menarini Silicon Biosystems

- Myriad Genetics

- Oncimmune

- QIAGEN

- Thermo Fisher Scientific

The Global Liquid Biopsy Market was valued at USD 4.8 billion in 2024 and is estimated to grow at a CAGR of 15.8% to reach USD 20.7 billion by 2034.

The growth is being fueled by rising advancements in cancer diagnostics, a shift toward non-invasive methods, increasing cancer prevalence, and greater awareness around early detection. As healthcare systems globally invest in infrastructure and expand screening access, demand for scalable, accurate tools like liquid biopsy continues to accelerate. The growing focus on early-stage identification and precision medicine is creating fertile ground for the integration of liquid biopsy into clinical settings. The test allows the detection and analysis of tumor-derived biomarkers such as cell-free DNA, circulating tumor cells, and extracellular vesicles directly from bodily fluids, offering a safer and faster alternative to traditional tissue biopsies. With applications spanning cancer diagnosis, mutation tracking, and treatment monitoring, liquid biopsy is proving to be a transformative solution, especially for high-risk and vulnerable patient populations. Its ability to minimize procedural risks while delivering actionable insights supports broader adoption across research institutions, hospitals, and diagnostic labs.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.8 Billion |

| Forecast Value | $20.7 Billion |

| CAGR | 15.8% |

In 2024, the circulating tumor cells segment generated USD 1.9 billion. These cells, which detach from primary tumors and travel through the bloodstream, are valuable in revealing tumor dynamics in real time. Technologies used to isolate and analyze CTCs, ranging from imaging platforms to microfluidics, are enabling clinicians to understand tumor evolution, resistance mechanisms, and genetic profiles. Their non-invasive nature and role in real-time monitoring make CTCs an increasingly important component of the liquid biopsy ecosystem, broadening its clinical relevance.

The cancer application segment held an 85.8% share in 2024. The steadily rising global burden of cancer continues to elevate the demand for faster, less invasive, and highly precise diagnostic methods. Liquid biopsy offers the potential to detect malignancies earlier, tailor therapies more effectively, and monitor responses without requiring surgical interventions. Its growing adoption in oncology is being driven by the need for more personalized, patient-centric treatment strategies that reduce time-to-diagnosis and improve care outcomes.

North America Liquid Biopsy Market generated USD 2 billion in 2024 and is expected to reach USD 8.4 billion by 2034. The region's leadership stems from its strong biotechnology research ecosystem, significant government investments in oncology, and rising demand for advanced diagnostic options. High adoption rates across clinical and research environments, along with regular product innovation and approvals, are helping solidify the region's position. Rising awareness among patients and providers, along with robust R&D pipelines supported by public and private funding, is adding momentum to regional growth.

Key players shaping the Global Liquid Biopsy Market include Myriad Genetics, BIOCEPT, Thermo Fisher Scientific, Guardant Health, F. Hoffmann La Roche, Menarini Silicon Biosystems, Lucene Health, Oncimmune, Illumina, EPIGENOMICS, Freenome Holdings, QIAGEN, Bio-Rad Laboratories, MDxHealth, and Angle. Companies in the Liquid Biopsy Market are deploying multi-faceted strategies to build and protect their market positions. A primary focus lies in expanding R&D pipelines for early-stage cancer detection and monitoring solutions. Strategic collaborations with research institutes and hospitals help accelerate clinical validation and widen access to emerging technologies. Many firms are developing AI-driven platforms to improve the accuracy of biomarker detection and streamline interpretation.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Biomarkers trends

- 2.2.3 Product trends

- 2.2.4 Disease indication trends

- 2.2.5 Clinical application trends

- 2.2.6 Technology trends

- 2.2.7 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Continuous technological advancements in cancer diagnostics

- 3.2.1.2 Increasing preference for non-invasive disease diagnosis

- 3.2.1.3 Growing prevalence of cancer worldwide

- 3.2.1.4 Rising awareness regarding early disease diagnosis

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Stringent regulatory framework

- 3.2.2.2 Lack of skilled professionals

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of multi-cancer early detection (MCED) tests

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Technological advancements

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Supply chain analysis

- 3.7 Reimbursement scenario

- 3.8 Pricing analysis, 2024

- 3.9 Future market trends

- 3.10 Gap analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Biomarkers, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Circulating tumor cells (CTC)

- 5.3 Circulating tumor DNA

- 5.4 Cell-free DNA

- 5.5 Extracellular vesicles

- 5.6 Other biomarkers

Chapter 6 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Consumables

- 6.2.1 Kits and reagents

- 6.2.2 Assay and panels

- 6.3 Instruments

- 6.4 Services

Chapter 7 Market Estimates and Forecast, By Disease Indication, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Cancer

- 7.2.1 Lung cancer

- 7.2.2 Breast cancer

- 7.2.3 Colorectal cancer

- 7.2.4 Prostate cancer

- 7.2.5 Other cancers

- 7.3 Non-cancer

- 7.3.1 Non-invasive prenatal testing

- 7.3.2 Organ transplantation

- 7.3.3 Infectious disease testing

Chapter 8 Market Estimates and Forecast, By Clinical Application Use, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Treatment monitoring

- 8.3 Prognosis and recurrence monitoring

- 8.4 Treatment selection

- 8.5 Diagnosis and screening

Chapter 9 Market Estimates and Forecast, By Technology, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Multi-gene parallel analysis (NGS)

- 9.3 Single gene analysis (PCR Microarrays)

Chapter 10 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 10.1 Key trends

- 10.2 Hospitals

- 10.3 Research Laboratories

- 10.4 Clinical Laboratories

- 10.5 Other end use

Chapter 11 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Netherlands

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 Middle East and Africa

- 11.6.1 Saudi Arabia

- 11.6.2 South Africa

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Angle

- 12.2 BIOCEPT

- 12.3 Bio-Rad Laboratories

- 12.4 EPIGENOMICS

- 12.5 F. Hoffmann La Roche

- 12.6 Freenome Holdings

- 12.7 Guardant Health

- 12.8 Illumina

- 12.9 Lucene Health

- 12.10 MDxHealth

- 12.11 Menarini Silicon Biosystems

- 12.12 Myriad Genetics

- 12.13 Oncimmune

- 12.14 QIAGEN

- 12.15 Thermo Fisher Scientific