|

시장보고서

상품코드

1859021

여드름 치료제 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Acne Medication Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

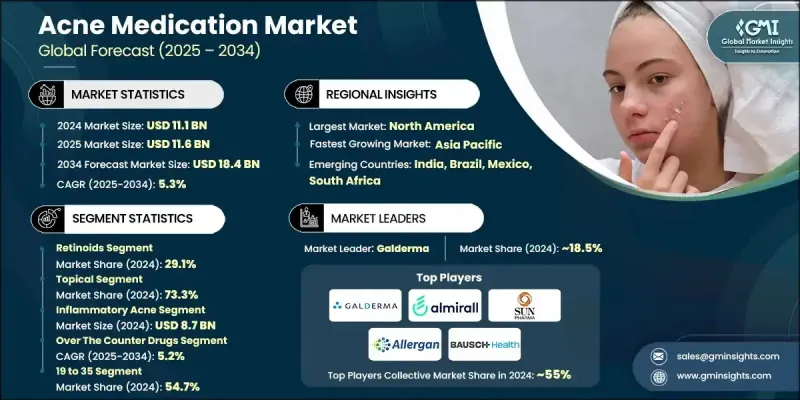

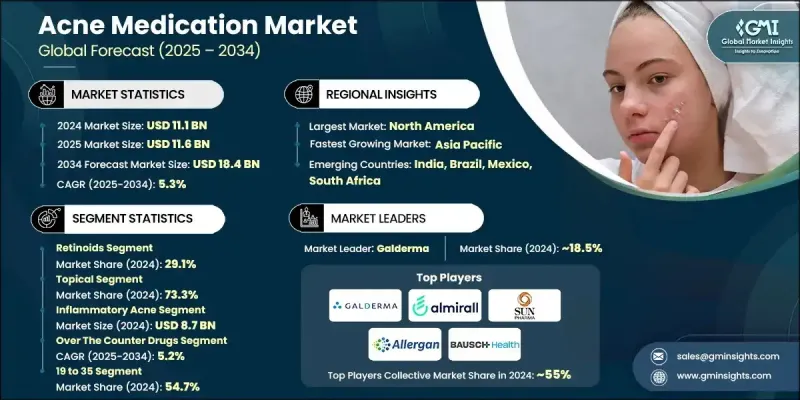

세계의 여드름 치료제 시장은 2024년에는 111억 달러로 평가되었고, CAGR 5.3%를 나타내, 2034년에는 184억 달러에 이를 것으로 추정되고 있습니다.

특히 15-19세의 십대 사이에서 여드름 증례가 증가하고 있으며, 효과적인 여드름 치료에 대한 수요를 부추기는 것이 확대를 견인하고 있습니다. 라이프스타일의 변화, 호르몬 균형의 혼란, 환경적인 스트레스 요인도 여드름 유병률을 높이는 원인이 되어 경구약과 외용약 모두의 필요성이 높아지고 있습니다. 또한 지성 피부와 모낭의 염증으로 인한 백반의 급증이 시장 성장을 더욱 밀어 올리고 있습니다. 여드름 치료제의 부문은 피부과에 속하며 모공 막힘, 화이트헤드, 블랙헤드, 다양한 병변이 있는 만성 염증성 질환 인 심상성 여드름의 관리에 중점을 둡니다. 치료는 염증을 억제하고 피지 분비를 조절하며 박테리아의 증식을 억제하는 것을 목표로합니다. 이 시장은 또한 환자의 컴플라이언스를 높이고 부작용을 줄이는 방부제가 없는 스테로이드 온존 및 클린 라벨 제형에 대한 수요가 증가함에 따라 진화하고 있습니다. 또한 원격 의료 및 전자상거래 플랫폼의 상승으로 여드름 해결책을 요구하는 환자에 대한 접근성과 참여도가 향상되었습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시장 규모 | 111억 달러 |

| 예측 금액 | 184억 달러 |

| CAGR | 5.3% |

2024년, 외용약 부문은 73.3%의 점유율을 차지했으며, 이는 칠하기 쉬움과 경도에서 중등도의 여드름 치료에 있어서 효능 때문입니다. 이 카테고리에는 크림, 로션, 패치, 와이프가 포함되어 있으며, 활성 성분을 환부의 피부에 직접 전달하여 전신 부작용을 최소화하면서 다양한 피부 유형에 대응합니다. 캡슐화된 활성제, 폼 제제, 하이드로콜로이드 패치 등의 기술 혁신이 치료 효과와 사용자의 어드히어런스를 높이고 있습니다. 피부과 의사는 일반적으로 국소 치료제를 제1선택 요법으로 처방하고 있으며, 다단계 스킨케어 루틴에서의 역할은 임상과 소비자 모두 여드름 케어의 중요성을 확고히 합니다.

염증성 여드름 분야는 이 여드름 유형의 중증도 및 표적 치료의 필요성 때문에 2024년에 87억 달러를 창조했습니다. 이 부문은 구진, 농포, 결절, 낭종과 같은 상태를 다루며 종종 국소 요법과 전신 요법의 조합이 필요합니다. 치료는 중등도에서 심한 여드름과 관련된 염증, 발적, 부종, 박테리아 감염의 완화에 중점을 둡니다. 흉터 형성을 예방하기 위해 조기 개입에 대한 의식이 증가함에 따라 염증성 여드름 관리에서 처방약의 사용이 가속화되고 있습니다.

북미의 여드름 치료제 시장은 2024년에 39.7%의 점유율을 차지했습니다. 이 지역의 성장은 강력한 건강 관리 인프라와 효과적인 여드름 관리에 대한 의식이 높아짐에 따라 심상성 여드름의 높은 유병률로 인해 발생합니다. 미국, 캐나다, 멕시코 등의 국가들이 이 지역 수요를 견인하고 있으며, 보다 정확한 치료를 위해 유전체 프로파일링을 도입한 개별화 피부과학과 같은 진보의 혜택을 받고 있습니다. 공중보건 캠페인과 처방약과 일반의약품 모두의 소비 증가는 시장 확대를 더욱 강화하고 있습니다.

세계 여드름 치료제 시장의 주요 기업으로는 Bayer, Stiefel (GSK), Lupin Pharmaceuticals, Teva Pharmaceuticals, Bausch Health, Paratek Pharmaceuticals, Galderma, Dr. Reddy's Laboratories, Akorn, Sun Pharmaceutical, Allergan (AbbVie), Mayne Pharmaceuticals, Almirall, Reckitt Benckiser, Torrent Pharmaceuticals가 포함됩니다. 여드름 치료제 시장의 각 회사는 환자의 결과를 개선하고 부작용을 줄이는 방부제가 없거나 스테로이드를 사용하지 않는 제품과 같은 고급 제제 개발을 통한 혁신에 주력하고 있습니다. 또한 다양한 여드름 유형을 타겟으로 한 경구·국소 요법을 포함한 포트폴리오의 확충도 진행하고 있습니다. 의료 서비스 제공업체와의 전략적 파트너십과 원격 의료 및 전자상거래와 같은 디지털 플랫폼에 대한 투자는 제품 액세스 및 환자 참여를 강화합니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 업계에 미치는 영향요인

- 성장 촉진요인

- 심상성 여드름의 유병률 증가

- 라이프스타일과 환경유인

- 피부과학적 제제의 진보

- 인지도의 향상과 의료에의 액세스

- 업계의 잠재적 위험 및 과제

- 치료 관련 부작용과 내성

- 충분한 서비스를 받지 않은 지역에서의 제한된 접근

- 시장 기회

- 미생물 기반 및 호르몬 표적 치료의 혁신

- AI를 활용한 스킨케어와 개인화 드레지멘의 확대

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 향후 시장 동향

- 기술적 상황

- 현재의 기술

- 신흥기술

- 특허 분석

- 상환 시나리오

- 파이프라인 분석

- 가격 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병과 인수

- 제휴와 협력

- 신제품 발표

- 확장 계획

제5장 시장 추계·예측 : 제품별(2021-2034년)

- 주요 동향

- 레티노이드

- 항생제

- 살리실산

- 벤질 퍼옥사이드

- 아젤라산

- 기타 제품

제6장 시장 추계·예측 : 제형별(2021-2034년)

- 주요 동향

- 국소용

- 크림 및 로션

- 패치 및 닦는 패드

- 경구제

- 정제 및 캡슐

- 분말

- 액제

제7장 시장 추계·예측 : 여드름 유형별(2021-2034년)

- 주요 동향

- 염증성 여드름

- 비염증성 여드름

제8장 시장 추계·예측 : 유형별(2021-2034년)

- 주요 동향

- 처방약

- 일반의약품

제9장 시장 추계·예측 : 연령층별(2021-2034년)

- 주요 동향

- 12세 이상 18세 미만

- 19세 이상 35세 미만

- 35세 이상

제10장 시장 추계·예측 : 유통 채널별(2021-2034년)

- 주요 동향

- 오프라인 채널

- 소매점

- 약국 및 드럭스토어

- 피부과 클리닉/병원

- 온라인 채널

제11장 시장 추계·예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제12장 기업 프로파일

- Akorn

- Allergan(AbbVie)

- Almirall SA

- Bausch Health

- Bayer

- Dr. Reddy’s Laboratories

- Galderma

- Lupin Pharmaceuticals

- Mayne Pharmaceuticals

- Paratek Pharmaceuticals

- Reckitt Benckiser

- Stiefel(GSK)

- Sun Pharmaceutical

- Teva Pharmaceuticals

- Torrent Pharmaceuticals

- Viatris

The Global Acne Medication Market was valued at USD 11.1 billion in 2024 and is estimated to grow at a CAGR of 5.3% to reach USD 18.4 billion by 2034.

The expansion is driven by increasing acne cases, particularly among teenagers aged 15 to 19, which fuels the demand for effective acne treatments. Lifestyle changes, hormonal imbalances, and environmental stressors are also contributing factors that intensify acne prevalence, leading to a higher need for both oral and topical medications. Additionally, the surge in whiteheads caused by oily skin and irritated hair follicles is pushing market growth further. The acne medication segment falls within dermatology, focusing on managing acne vulgaris a chronic inflammatory condition involving clogged pores, whiteheads, blackheads, and various lesions. Treatments aim to reduce inflammation, regulate sebum production, and inhibit bacterial growth. The market is also evolving with the rising demand for preservative-free, steroid-sparing, and clean-label formulations that enhance patient compliance and reduce side effects. Furthermore, the rise of telehealth and e-commerce platforms is improving accessibility and engagement for patients seeking acne solutions.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $11.1 Billion |

| Forecast Value | $18.4 Billion |

| CAGR | 5.3% |

In 2024, the topical medication segment held 73.3% share, owing to its ease of application and effectiveness in treating mild to moderate acne. This category includes creams, lotions, patches, and wipes that deliver active ingredients directly to the affected skin, minimizing systemic side effects while catering to diverse skin types. Innovations such as encapsulated actives, foam formulations, and hydrocolloid patches are boosting treatment effectiveness and user adherence. Dermatologists commonly prescribe topical treatments as first-line therapy, and their role in multi-step skincare routines has cemented their importance in both clinical and consumer acne care.

The inflammatory acne segment generated USD 8.7 billion in 2024, driven by the severity of this acne type and the need for targeted treatment. This segment covers conditions like papules, pustules, nodules, and cysts, which often require a combination of topical and systemic therapies. Treatments focus on alleviating inflammation, redness, swelling, and bacterial infection associated with moderate to severe acne. Growing awareness about early intervention to prevent scarring has also accelerated the use of prescription medications in managing inflammatory acne.

North America Acne Medication Market held a 39.7% share in 2024. The region's growth stems from the high prevalence of acne vulgaris, supported by strong healthcare infrastructure and rising awareness about effective acne management. Countries including the United States, Canada, and Mexico drive regional demand, benefiting from advancements like personalized dermatology, which incorporates genomic profiling for more precise treatments. Public health campaigns and increasing consumption of both prescription and over-the-counter products further bolster market expansion.

Leading players in the Global Acne Medication Market include Bayer, Stiefel (GSK), Lupin Pharmaceuticals, Teva Pharmaceuticals, Bausch Health, Paratek Pharmaceuticals, Galderma, Dr. Reddy's Laboratories, Akorn, Sun Pharmaceutical, Allergan (AbbVie), Mayne Pharmaceuticals, Almirall, Reckitt Benckiser, and Torrent Pharmaceuticals. To strengthen their position, companies in the Acne Medication Market focus on innovation through the development of advanced formulations like preservative-free and steroid-sparing products, which improve patient outcomes and reduce side effects. They are also expanding their portfolios to include oral and topical therapies targeting diverse acne types. Strategic partnerships with healthcare providers and investment in digital platforms such as telehealth and e-commerce enhance product accessibility and patient engagement.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumption and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 Formulation trends

- 2.2.4 Acne type trends

- 2.2.5 Type trends

- 2.2.6 Age group trends

- 2.2.7 Distribution channel trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Value addition at each stage

- 3.1.3 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of acne vulgaris

- 3.2.1.2 Lifestyle and environmental triggers

- 3.2.1.3 Advancements in dermatological formulations

- 3.2.1.4 Growing awareness and access to care

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Treatment-related side effects and resistance

- 3.2.2.2 Limited access in underserved regions

- 3.2.3 Market opportunities

- 3.2.3.1 Innovation in microbiome-based and hormone-targeted therapies

- 3.2.3.2 Expansion of AI-driven skincare and personalized regimens

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Future market trends

- 3.6 Technological landscape

- 3.6.1 Current technologies

- 3.6.2 Emerging technologies

- 3.7 Patent analysis

- 3.8 Reimbursement scenario

- 3.9 Pipeline analysis

- 3.10 Pricing analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Retinoids

- 5.3 Antibiotics

- 5.4 Salicylic acid

- 5.5 Benzyl peroxide

- 5.6 Azelaic acid

- 5.7 Other products

Chapter 6 Market Estimates and Forecast, By Formulation, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Topical

- 6.2.1 Creams and lotions

- 6.2.2 Patches and wiping pads

- 6.3 Oral

- 6.3.1 Tablets and capsules

- 6.3.2 Powders

- 6.3.3 Liquids

Chapter 7 Market Estimates and Forecast, By Acne Type, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Inflammatory acne

- 7.3 Non-inflammatory acne

Chapter 8 Market Estimates and Forecast, By Type, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Prescription drugs

- 8.3 Over the counter drugs

Chapter 9 Market Estimates and Forecast, By Age Group, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 12 to 18

- 9.3 19 to 35

- 9.4 Above 35

Chapter 10 Market Estimates and Forecast, By Distribution Channel, 2021 - 2034 ($ Mn)

- 10.1 Key trends

- 10.2 Offline channels

- 10.2.1 Retail stores

- 10.2.2 Pharmacies and drug stores

- 10.2.3 Dermatology clinics/hospitals

- 10.3 Online channels

Chapter 11 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Netherlands

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 Japan

- 11.4.3 India

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 Middle East and Africa

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Akorn

- 12.2 Allergan (AbbVie)

- 12.3 Almirall S.A.

- 12.4 Bausch Health

- 12.5 Bayer

- 12.6 Dr. Reddy’s Laboratories

- 12.7 Galderma

- 12.8 Lupin Pharmaceuticals

- 12.9 Mayne Pharmaceuticals

- 12.10 Paratek Pharmaceuticals

- 12.11 Reckitt Benckiser

- 12.12 Stiefel (GSK)

- 12.13 Sun Pharmaceutical

- 12.14 Teva Pharmaceuticals

- 12.15 Torrent Pharmaceuticals

- 12.16 Viatris