|

시장보고서

상품코드

1871082

포장용 셀룰로오스 나노결정 시장 기회, 성장 요인, 업계 동향 분석 및 예측(2025-2034년)Cellulose Nanocrystals for Packaging Applications Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

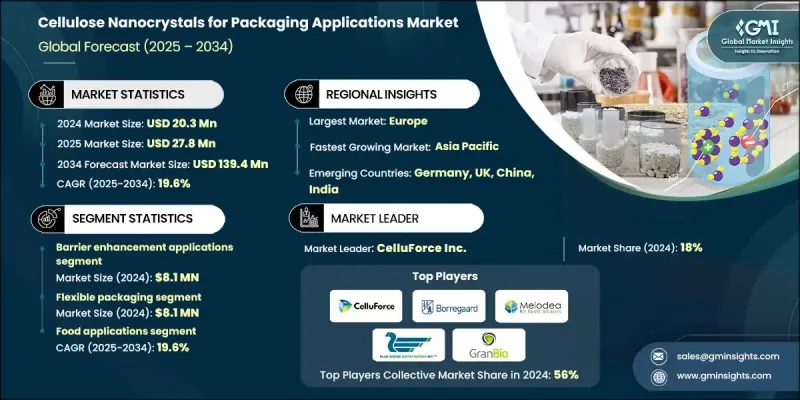

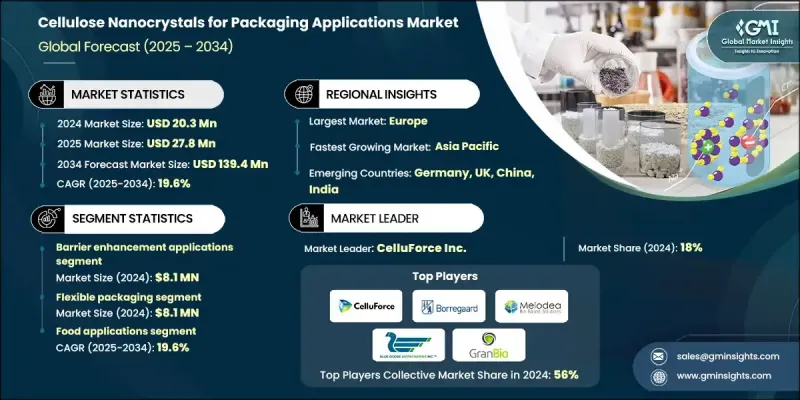

세계의 포장용 셀룰로오스 나노결정 시장 규모는 2024년에 2,030만 달러로 평가되었으며, 2034년까지 연평균 복합 성장률(CAGR) 19.6%를 나타내 1억 3,940만 달러에 달할 것으로 예측되고 있습니다.

포장 산업에서 CNC 수요는 탁월한 기계적 강도, 생분해성 및 고급 장벽 성능으로 빠르게 증가하고 있습니다. 이 나노 재료는 포장 필름의 산소 및 오일에 대한 내성을 크게 향상시키고 석유 유래 코팅의 환경 친화적인 대안을 제공합니다. 포장 및 종이 용도는 마이크로셀룰로오스 및 나노셀룰로오스 제품의 약 60%의 점유율을 차지합니다. 효소처리 및 기계적 가공방법의 기술 혁신은 에너지요건을 약 90% 절감하여 대규모 CNC 생산이 보다 실현가능하고 비용효율이 높아졌습니다. 지속가능하고 순환적인 포장 솔루션으로의 세계 전환은 성장의 주요 추진력이며 소비자와 기업이 친환경 소재를 점점 우선시하고 있습니다. 강화된 배리어 코팅은 측정가능한 성능 향상을 나타내며, 5-10%의 CNC 함량으로 산소 투과율이 21-36% 감소되었습니다. 이러한 지속가능성과 성능의 균형을 통해 CNC 기반 코팅은 제품 수명 연장과 환경 요인으로부터의 보호를 필요로 하는 식품, 의약품, 소비재 포장에서 선호되는 소재로서의 지위를 확립하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 2,030만 달러 |

| 예측 금액 | 1억 3,940만 달러 |

| CAGR | 19.6% |

배리어 강화 용도 부문은 2024년에 39.9%의 점유율을 차지하며 기존 소재에 비해 산소, 습기, 자외선으로부터의 보호 성능에 있어서 CNC의 뛰어난 능력이 두드러졌습니다. 특히 식품, 소비재, 의약품 포장에서 제품의 신선도와 안전성을 유지하기 위해 높은 장벽 특성이 필수적이기 때문에 이 부문은 계속 주도적인 지위를 유지하고 있습니다.

연포장 카테고리는 2024년에 39.9%의 점유율을 차지했으며 필름, 랩, 파우치 및 기타 유연한 용기를 포함합니다. 이 부문은 유연성과 가공성을 유지하면서 장벽 성능을 향상시키는 CNC의 능력에서 혜택을 누리고 있습니다. 식품 포장, 물집 팩, 지속 가능한 소비재 포장 등의 용도는 기능성과 디자인의 다양성을 손상시키지 않으면서 내구성, 보호성 및 환경적 이점을 제공하기 위해 CNC에 의존합니다.

북미의 포장용 셀룰로오스 나노결정 시장은 2024년에 27.6%의 점유율을 차지했으며, 2034년까지 연평균 복합 성장률(CAGR) 19%를 나타낼 것으로 전망되고 있습니다. 이 지역은 강력한 연구 생태계, 성숙한 포장 산업, 지속가능성에 대한 기업 헌신 증가와 같은 이점을 가지고 있습니다. 미국과 캐나다는 주요 도입국이며 대학과 국립 연구소의 활발한 조사 프로그램에 의해 지원됩니다. 규제면의 진전과 나노 재료 응용 분야의 업계 전문 지식이 신흥 시장에서 북미의 주도적 입장을 더욱 강화하고 있습니다.

포장용 셀룰로오스 나노결정 시장에서 주요 기업으로는 FiberLean Technologies, GranBio, Kruger Inc., CelluForce Inc., Anomera Inc., Blue Goose Biorefineries, Melodea Ltd., Reinste Nano Ventures Pvt. Ltd., Borregaard ASA, Nanoverse 등을 들 수 있습니다. 포장용 셀룰로오스 나노결정 시장의 주요 기업은 혁신, 협업, 기술 혁신을 통해 시장 기반을 강화하고 있습니다. 많은 기업들이 확장성 향상, 에너지 비용 절감, 재료 품질 개선을 목적으로 첨단 나노셀룰로오스 가공 기술에 대한 투자를 진행하고 있습니다. 포장 제조업체와 연구기관과의 전략적 제휴는 제품 개발을 가속화함과 동시에 식품, 의약품, 소비재 포장 분야에서의 CNC(셀룰로오스 나노결정)의 응용 범위를 확대하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 파괴적 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 지속 가능한 포장 솔루션에 대한 수요 증가

- 바이오 베이스 식품 접촉 포장 재료에 대한 규제 추진

- 포장 나노기술 조사에 대한 투자 증가

- 업계의 잠재적 위험 및 과제

- 높은 생산 비용과 한정적인 상업 규모

- 소수성 포장 폴리머 통합에 있어서 기술적 과제

- 포장 용도에 있어서 습기 감수성의 제한 사항

- 시장 기회

- 포장 적합성 향상을 위한 표면 개질 기술

- 다층 포장 구조의 개발

- 활성 포장·스마트 포장의 응용 분야에 있어서 성장

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 가격 동향

- 지역별

- 포장 기능

- 포장 형태

- 최종 용도 포장 분야

- 향후 시장 동향

- 특허 상황

- 무역 통계(HS코드)(참고 : 무역 통계는 주요 국가에서만 제공됨)

- 주요 수입국

- 주요 수출국

- 지속가능성과 환경면

- 지속가능한 대처

- 폐기물 감축 전략

- 생산에 있어서 에너지 효율

- 환경에 배려한 대처

- 탄소발자국에 관한 고려 사항

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병 및 인수

- 파트너십 및 협력

- 신제품 발매

- 확대 계획

제5장 시장 추계·예측 : 포장 기능별(2021-2034년)

- 주요 동향

- 차단성 향상

- 산소 차단

- 수분 차단

- 그리스 및 오일 차단

- 가스 차단

- 기계적 보강

- 인장 강도 향상

- 강성 및 치수 안정성

- 인열 저항성 개선

- 코팅

- 표면 차단 코팅

- 기능성 코팅

- 보호 코팅

- 능동적 포장 기능

- 항균 포장

- 항산화 포장

- 제어 방출 시스템

- 스마트 포장 기능

- 센서 통합

- 표시 시스템

- 반응성 포장 재료

제6장 시장 추계·예측 : 포장 형태별(2021-2034년)

- 주요 동향

- 연성 포장

- 필름 및 시트

- 파우치 및 백

- 랩 및 라이너

- 다층 연성 구조

- 경질 포장

- 용기 및 병

- 자 및 캔

- 구조 포장 부품

- 종이 및 판지 포장

- 접이식 카톤

- 식품서비스 포장

- 골판지 포장

- 판지 용기

- 다층 및 라미네이트 포장

- 차단층 적용

- 접착층 통합

- 복합 다층 구조

제7장 시장 추계·예측 : 최종 용도 포장 분야별(2021-2034년)

- 주요 동향

- 식품 포장

- 직접 식품 접촉 용도

- 간접 식품 접촉 용도

- 신선 식품 포장

- 가공 식품 포장

- 냉동 식품 포장

- 음료 포장

- 무알코올 음료 포장

- 알코올 음료 포장

- 유제품 음료 포장

- 의약품 포장

- 1차 의약품 포장

- 2차 의약품 포장

- 의료기기 포장

- 소비재 포장

- 퍼스널케어 포장

- 가정용품 포장

- 전자기기 포장

제8장 시장추계·예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 기타 라틴아메리카

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

제9장 기업 프로파일

- CelluForce Inc.

- Borregaard ASA

- Reinste Nano Ventures Pvt. Ltd.

- Melodea Ltd.

- Blue Goose Biorefineries

- FiberLean Technologies

- Anomera Inc.

- Kruger Inc

- GranBio

- Nanoverse

The Global Cellulose Nanocrystals for Packaging Applications Market was valued at USD 20.3 million in 2024 and is estimated to grow at a CAGR of 19.6% to reach USD 139.4 million by 2034.

The demand for CNCs in the packaging industry is rapidly increasing due to their exceptional mechanical strength, biodegradability, and advanced barrier performance. These nanomaterials significantly improve resistance to oxygen and oil in packaging films, providing an eco-friendly substitute for petroleum-based coatings. Packaging and paper applications represent around 60% share for micro and nanocellulose products. Technological innovations in enzymatic and mechanical processing methods have lowered energy requirements by nearly 90%, making large-scale CNC production more feasible and cost-efficient. The global shift toward sustainable and circular packaging solutions remains the key growth drive, with consumers and corporations increasingly prioritizing environmentally friendly materials. Enhanced barrier coatings have shown measurable performance improvements, with oxygen transmission rates reduced by 21-36% at 5-10% CNC loadings. This balance of sustainability and performance positions CNC-based coatings as a preferred material in food, pharmaceutical, and consumer goods packaging, all requiring extended product life and protection against environmental factors.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $20.3 Million |

| Forecast Value | $139.4 Million |

| CAGR | 19.6% |

The barrier enhancement applications segment held 39.9% share in 2024, highlighting CNC's superior ability to protect against oxygen, moisture, and UV radiation compared to conventional materials. This segment continues to dominate as high-barrier properties are essential for maintaining product freshness and safety, especially in food, consumer goods, and pharmaceutical packaging.

The flexible packaging category held a 39.9% share in 2024, covering films, wraps, pouches, and other flexible containers. This segment benefits from CNC's ability to improve barrier performance while maintaining flexibility and processability. Applications such as food packaging, blister packs, and sustainable consumer goods packaging rely on CNCs to deliver durability, protection, and environmental advantages without compromising functionality or design versatility.

North America Cellulose Nanocrystals for Packaging Applications Market held 27.6% share in 2024 and is expected to grow at a CAGR of 19% through 2034. The region benefits from a strong research ecosystem, a mature packaging sector, and growing corporate commitments to sustainability. The United States and Canada are leading adopters, supported by active research programs across universities and national laboratories. Regulatory advancements and industry expertise in nanomaterial applications have further reinforced North America's leadership in this emerging market.

Key companies operating in the Global Cellulose Nanocrystals for Packaging Applications Market include FiberLean Technologies, GranBio, Kruger Inc., CelluForce Inc., Anomera Inc., Blue Goose Biorefineries, Melodea Ltd., Reinste Nano Ventures Pvt. Ltd., Borregaard ASA, and Nanoverse. Leading companies in the cellulose nanocrystals for packaging applications market are strengthening their market foothold through innovation, collaborations, and technological advancement. Many are investing in advanced nanocellulose processing technologies to enhance scalability, reduce energy costs, and improve material quality. Strategic partnerships between packaging producers and research institutions are accelerating product development and expanding CNC applications across food, pharmaceutical, and consumer goods packaging.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Packaging function

- 2.2.3 Packaging format

- 2.2.4 End use packaging sector

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing Demand for Sustainable Packaging Solutions

- 3.2.1.2 Regulatory Push for Bio-based Food Contact Packaging Materials

- 3.2.1.3 Increasing Investment in Packaging Nanotechnology Research

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High production costs & limited commercial scale

- 3.2.2.2 Technical challenges in hydrophobic packaging polymer integration

- 3.2.2.3 Moisture sensitivity limitations in packaging applications

- 3.2.3 Market opportunities

- 3.2.3.1 Surface modification technologies for enhanced packaging compatibility

- 3.2.3.2 Multilayer packaging architecture development

- 3.2.3.3 Active & smart packaging applications growth

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and Innovation Landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 Packaging Function

- 3.7.3 Packaging Format

- 3.7.4 End use Packaging Sector

- 3.8 Future market trends

- 3.9 Patent Landscape

- 3.10 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.10.1 Major importing countries

- 3.10.2 Major exporting countries

- 3.11 Sustainability and environmental aspects

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly initiatives

- 3.12 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Packaging Function, 2021 - 2034 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Barrier enhancement applications

- 5.2.1 Oxygen barrier applications

- 5.2.2 Moisture barrier applications

- 5.2.3 Grease & oil barrier applications

- 5.2.4 Gas barrier applications

- 5.3 Mechanical reinforcement applications

- 5.3.1 Tensile strength enhancement

- 5.3.2 Stiffness & dimensional stability

- 5.3.3 Tear resistance improvement

- 5.4 Coating applications

- 5.4.1 Surface barrier coatings

- 5.4.2 Functional coatings

- 5.4.3 Protective coatings

- 5.5 Active packaging functions

- 5.5.1 Antimicrobial packaging applications

- 5.5.2 Antioxidant packaging applications

- 5.5.3 Controlled release systems

- 5.6 Smart packaging functions

- 5.6.1 Sensor integration applications

- 5.6.2 Indicator systems

- 5.6.3 Responsive packaging materials

Chapter 6 Market Estimates and Forecast, By Packaging Format, 2021 - 2034 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Flexible packaging

- 6.2.1 Films & sheets

- 6.2.2 Pouches & bags

- 6.2.3 Wraps & liners

- 6.2.4 Multilayer flexible structures

- 6.3 Rigid packaging

- 6.3.1 Containers & bottles

- 6.3.2 Jars & cans

- 6.3.3 Structural packaging components

- 6.4 Paper & paperboard packaging

- 6.4.1 Folding cartons

- 6.4.2 Food service packaging

- 6.4.3 Corrugated packaging

- 6.4.4 Paperboard containers

- 6.5 Multilayer & laminated packaging

- 6.5.1 Barrier layer applications

- 6.5.2 Adhesive layer integration

- 6.5.3 Complex multilayer structures

Chapter 7 Market Estimates and Forecast, By End Use Packaging Sector, 2021 - 2034 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Food packaging

- 7.2.1 Direct food contact applications

- 7.2.2 Indirect food contact applications

- 7.2.3 Fresh food packaging

- 7.2.4 Processed food packaging

- 7.2.5 Frozen food packaging

- 7.3 Beverage packaging

- 7.3.1 Non-alcoholic beverage packaging

- 7.3.2 Alcoholic beverage packaging

- 7.3.3 Dairy beverage packaging

- 7.4 Pharmaceutical packaging

- 7.4.1 Primary pharmaceutical packaging

- 7.4.2 Secondary pharmaceutical packaging

- 7.4.3 Medical device packaging

- 7.5 Consumer goods packaging

- 7.5.1 Personal care packaging

- 7.5.2 Household products packaging

- 7.5.3 Electronics packaging

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 CelluForce Inc.

- 9.2 Borregaard ASA

- 9.3 Reinste Nano Ventures Pvt. Ltd.

- 9.4 Melodea Ltd.

- 9.5 Blue Goose Biorefineries

- 9.6 FiberLean Technologies

- 9.7 Anomera Inc.

- 9.8 Kruger Inc

- 9.9 GranBio

- 9.10 Nanoverse