|

시장보고서

상품코드

1871093

콜드체인 물류 장비 시장 : 기회, 성장 요인, 업계 동향 분석 및 예측(2025-2034년)Cold Chain Logistics Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

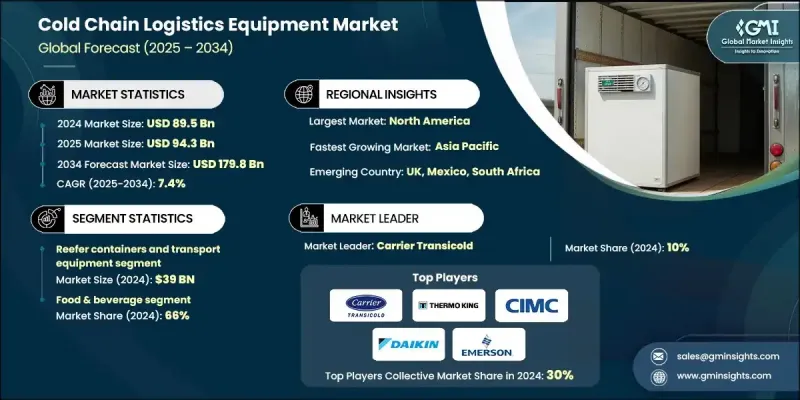

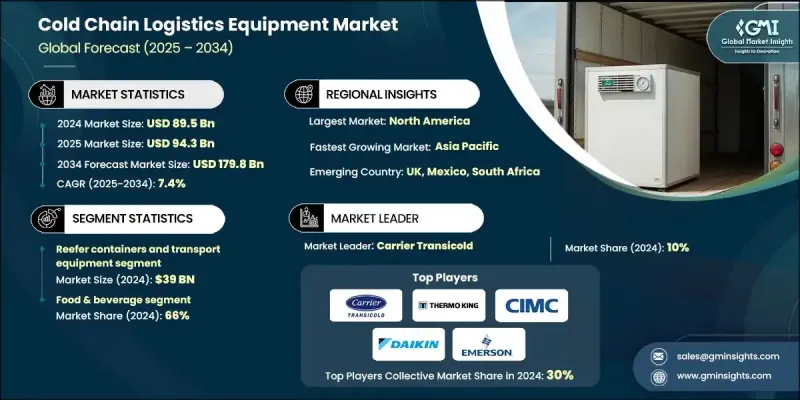

세계의 콜드체인 물류 장비 시장은 2024년 895억 달러로 평가되었고, 2034년까지 연평균 복합 성장률(CAGR)은 7.4%를 나타낼 것으로 예측되며 1,798억 달러에 달할 전망입니다.

시장 성장은 의약품, 생물학적 제제, 백신, 신선 농산물, 해산물, 유제품, 냉동 식품 등 온도에 민감한 제품에 대한 전 세계적 수요 증가에 힘입어 가속화되고 있습니다. 제약 산업은 생물학적 제제 및 mRNA 기반 치료제를 보존하기 위해 극저온 저장 및 운송 시스템에 크게 의존하고 있어 첨단 콜드체인 물류 장비에 대한 수요가 강하게 발생하고 있습니다. 마찬가지로 신선 및 유기농 식품 소비 증가로 공급망 전반에 걸쳐 제품 안전성과 품질을 보장하기 위한 냉장 저장 및 운송 시스템에 대한 투자가 촉진되고 있습니다. 세계화로 인해 대륙 간 부패하기 쉬운 상품의 유통 범위가 확대됨에 따라 물류 업체들은 제품 무결성을 유지하고 손실을 줄이기 위해 온도 제어 솔루션을 점점 더 많이 채택하고 있습니다. 식품 안전성과 지속가능성에 대한 인식 제고 역시 생산부터 최종 배송까지 일관된 온도 조건을 유지하도록 설계된 첨단 콜드 체인 시스템으로의 전환을 가속화하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 895억 달러 |

| 예측 금액 | 1,798억 달러 |

| CAGR | 7.4% |

2024년 리퍼 컨테이너 및 운송 장비 부문은 390억 달러의 매출을 기록했습니다. 이러한 컨테이너는 해상, 철도, 도로를 아우르는 복합 운송 과정에서 효율적인 온도 제어를 제공하여 장거리 운송 중 신선식품의 품질 유지를 보장함으로써 국제 물류에 필수적입니다. 그 적응성과 신뢰성은 글로벌 콜드 체인 운영에 없어서는 안 될 요소입니다.

식품 및 음료 부문은 신선하고 자연스러운 즉석 섭취 제품에 대한 소비자 선호도 증가에 힘입어 2024년 66%의 점유율을 차지했습니다. 부패 및 오염 방지를 위한 정밀한 온도 조절 필요성으로 인해 생산자, 소매업체 및 유통업체는 냉장 저장 시설, 온도 감지 시스템, 냉장 운송 차량을 포함한 첨단 냉장 인프라에 대규모 투자를 진행하고 있습니다. 이러한 투자는 높은 안전성과 신선도 기준을 유지하면서 농장에서 소매점까지 원활한 제품 이동을 지원합니다.

미국의 콜드체인 물류 장비 시장은 2024년 78.2%의 점유율을 차지하며 249억 달러 규모에 달했습니다. 미국의 잘 구축된 인프라, 엄격한 규제 환경, 온도에 민감한 상품에 대한 강력한 수요는 이 나라를 글로벌 콜드체인 운영의 주요 허브로 만듭니다. 스마트 모니터링 기술, 냉장 저장 시설 확장, 효율적인 운송 시스템에 대한 지속적인 투자는 미국의 우위를 더욱 공고히 하고 있습니다. 이 성장은 신뢰할 수 있는 콜드 체인 시스템에 크게 의존하는 전자상거래, 음식 배달, 제약 산업의 번영에 의해 추가로 뒷받침됩니다.

세계의 콜드체인 물류 장비 시장의 주요 기업으로는 캐리어 트랜시콜드(유나이티드 테크놀로지스), 에머슨 일렉트릭(코플랜드), 존슨 컨트롤스, 리버콜드, 댄포스, 오얼비콤, DANA 스틸, 다이킨 산업, 서모킹( 트레인 테크놀로지스), 블레이더 트레이딩 & 리플리제레이션, TSSC, 써모다이나믹스, 차이나 인터내셔널 마린 컨테이너스, 자노티 스파, 정주 개선 콜드체인, 사우디아라비아의 콜드 스토어즈 그룹(CGS) 등이 있습니다. 콜드체인 물류 장비 시장 기업들은 글로벌 입지를 강화하고 경쟁 우위를 유지하기 위해 다양한 전략을 채택하고 있습니다. 선도적 제조사들은 에너지 효율적인 압축기, 스마트 센서, 실시간 모니터링 시스템 등 첨단 냉동 기술에 투자하여 온도 제어 성능을 개선하고 에너지 소비를 줄이고 있습니다. 물류 제공업체 및 식품 생산자와의 전략적 협력 및 파트너십을 통해 유통망을 확장하고 공급망을 최적화하고 있습니다. 지속적인 연구 개발 노력은 글로벌 환경 기준을 충족하기 위한 친환경 냉매 및 지속 가능한 설계 개발에 집중되고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 업계에 미치는 영향요인

- 성장 촉진요인

- 온도에 민감한 제품에 대한 수요 증가

- 전자식료품 및 온라인 식품 배달 성장

- 지속가능성과 친환경 물류

- 업계의 잠재적 억제요인 및 과제

- 온도 제어 실패

- 높은 운영 비용과 에너지 비용

- 기회

- 기술 혁신

- 모듈식 및 이동식 냉장 보관 솔루션

- 성장 촉진요인

- 성장 가능성 분석

- 장래 시장 동향

- 기술과 혁신의 상황

- 현재의 기술 동향

- 신흥기술

- 가격 동향

- 지역별

- 장비별

- 규제 상황

- 규격 및 규정 준수 요건

- 지역별 규제 프레임워크

- 인증기준

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병 및 인수

- 제휴 및 협력관계

- 신제품 발매

- 확대 계획

제5장 시장 추계 및 예측 : 설비 유형별(2021-2034년)

- 주요 동향

- 리퍼 컨테이너 및 운송 장비

- 표준 리퍼 컨테이너(10피트, 20피트, 40피트)

- 냉장 트럭 및 트레일러

- 전용 해상 컨테이너(DNV 인증 취득 완료)

- 이동식 냉동 장비

- 냉장 보관 인프라

- 모듈식 냉장실

- 온도 제어 창고

- 급속 냉동 장치

- 워크인 냉장고 및 냉동고

- 모니터링 및 제어 시스템

- IoT 지원 센서

- 데이터 로거 및 레코더

- SCADA 모니터링 시스템

- 블록체인 추적 플랫폼

- 냉동 설비

- 집중형 냉동 시스템

- 응축기

- 컴프레서 및 증발기

- 열교환기

제6장 시장 추계 및 예측 : 온도 범위별(2021-2034년)

- 주요 동향

- 냉동 저장(-25℃--18℃)

- 냉장 저장(0°C-8°C)

- 상온 저장(15℃-25℃)

- 상온 플러스 저장( 15°C- 25°C)

- 초저온 저장(-70℃--40℃)

제7장 시장 추계 및 예측 : 서비스종별(2021-2034년)

- 주요 동향

- 보관 서비스

- 운송 서비스

- 부가가치 서비스

- 급속 냉동

- 라벨링 및 포장

- 재고 관리

- 품질관리

제8장 시장 추계 및 예측 : 용도별(2021-2034년)

- 주요 동향

- 식품 및 음료

- 신선 식품(과일, 야채)

- 유제품

- 육류 및 수산물

- 냉동식품

- 가공식품

- 의약품 및 헬스케어

- 백신 및 생물학적 제제

- 온도 민감성 의약품

- 혈액제제

- 의료기기

- 화학제품 및 산업 제품

- 특수화학제품

- 산업용 재료

- 전자부품

제9장 시장 추계 및 예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 물류 및 3PL 제공업체

- 식품 제조업체

- 제약회사

- 소매 체인

- 전자상거래 플랫폼

- 정부 및 의료기관

제10장 시장 추계 및 예측 : 유통 채널별(2021-2034년)

- 주요 동향

- 직접

- 간접

제11장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제12장 기업 프로파일

- Bureida Trading &Refrigeration

- Carrier Transicold(United Technologies)

- China International Marine Containers

- Coldstores Group of Saudi Arabia(CGS)

- Daikin Industries

- DANA Steel

- Danfoss

- Emerson Electric(Copeland)

- Johnson Controls

- ORBCOMM

- Rivacold

- Thermo King(Trane Technologies)

- Thermodynamics

- TSSC

- Zanotti spa

- Zhengzhou Kaixue Cold Chain

The Global Cold Chain Logistics Equipment Market was valued at USD 89.5 Billion in 2024 and is estimated to grow at a CAGR of 7.4% to reach USD 179.8 Billion by 2034.

Market growth is fueled by the increasing global demand for temperature-sensitive products such as pharmaceuticals, biologics, vaccines, fresh produce, seafood, dairy, and frozen foods. The pharmaceutical industry relies heavily on ultra-low-temperature storage and transport systems to preserve biologics and mRNA-based therapies, creating strong demand for advanced refrigerated logistics equipment. Similarly, the rising consumption of fresh and organic food products has prompted investments in refrigerated storage and transportation systems to ensure product safety and quality throughout the supply chain. With globalization extending the reach of perishable goods across continents, logistics providers are increasingly adopting temperature-controlled solutions to preserve product integrity and reduce spoilage. Growing awareness about food safety and sustainability is also accelerating the transition toward advanced cold chain systems designed to maintain consistent temperature conditions from production to final delivery.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $89.5 Billion |

| Forecast Value | $179.8 Billion |

| CAGR | 7.4% |

In 2024, the reefer containers and transport equipment segment generated USD 39 Billion. These refrigerated containers are vital for international logistics, offering efficient temperature control during multimodal transportation spanning sea, rail, and road, ensuring perishable goods maintain quality during long-distance shipment. Their adaptability and reliability make them indispensable for global cold chain operations.

The food & beverage sector held a 66% share in 2024, driven by rising consumer preference for fresh, natural, and ready-to-eat products. The need for precise temperature regulation to prevent spoilage and contamination has led producers, retailers, and distributors to invest heavily in advanced refrigeration infrastructure, including cold storage units, temperature-sensing systems, and refrigerated transport vehicles. These investments support seamless product movement from farms to retail outlets while maintaining high safety and freshness standards.

U.S. Cold Chain Logistics Equipment Market held 78.2% share and generated USD 24.9 Billion in 2024. The country's well-established infrastructure, strict regulatory environment, and strong demand for temperature-sensitive goods make it a major global hub for cold chain operations. Continuous investments in smart monitoring technologies, cold storage expansion, and efficient transportation systems are further strengthening the country's dominance. The growth is also supported by the thriving e-commerce, food delivery, and pharmaceutical industries, which rely heavily on reliable cold chain systems.

Key players in the Global Cold Chain Logistics Equipment Market include Carrier Transicold (United Technologies), Emerson Electric (Copeland), Johnson Controls, Rivacold, Danfoss, ORBCOMM, DANA Steel, Daikin Industries, Thermo King (Trane Technologies), Bureida Trading & Refrigeration, TSSC, Thermodynamics, China International Marine Containers, Zanotti Spa, Zhengzhou Kaixue Cold Chain, and Coldstores Group of Saudi Arabia (CGS). Companies in the Cold Chain Logistics Equipment Market are adopting multiple strategies to strengthen their global presence and maintain a competitive advantage. Leading manufacturers are investing in advanced refrigeration technologies, such as energy-efficient compressors, smart sensors, and real-time monitoring systems, to improve temperature control and reduce energy consumption. Strategic collaborations and partnerships with logistics providers and food producers are expanding distribution networks and optimizing supply chains. Continuous R&D efforts are focused on developing eco-friendly refrigerants and sustainable designs to meet global environmental standards.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Equipment type

- 2.2.3 Temperature range

- 2.2.4 Service type

- 2.2.5 Application

- 2.2.6 End use industry

- 2.2.7 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for temperature-sensitive products

- 3.2.1.2 Growth in e-grocery and online food delivery

- 3.2.1.3 Sustainability and green logistics

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Temperature control failures

- 3.2.2.2 High operational and energy costs

- 3.2.3 Opportunities

- 3.2.3.1 Technological innovation

- 3.2.3.2 Modular and mobile cold storage solutions

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By equipment type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Equipment Type, 2021 - 2034 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Reefer containers and transport equipment

- 5.2.1 Standard reefer containers (10ft, 20ft, 40ft)

- 5.2.2 Refrigerated trucks and trailers

- 5.2.3 Specialized offshore containers (DNV certified)

- 5.2.4 Mobile refrigeration units

- 5.3 Cold storage infrastructure

- 5.3.1 Modular cold rooms

- 5.3.2 Temperature-controlled warehouses

- 5.3.3 Blast freezing equipment

- 5.3.4 Walk-in coolers and freezers

- 5.4 Monitoring and control systems

- 5.4.1 IoT-enabled sensors

- 5.4.2 Data loggers and recorders

- 5.4.3 SCADA monitoring systems

- 5.4.4 Blockchain traceability platforms

- 5.5 Refrigeration equipment

- 5.5.1 Centralized refrigeration systems

- 5.5.2 Condensing units

- 5.5.3 Compressors and evaporators

- 5.5.4 Heat exchangers

Chapter 6 Market Estimates and Forecast, By Temperature Range, 2021 - 2034 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Frozen storage (-25°C to -18°C)

- 6.3 Chilled storage (0°C to +8°C)

- 6.4 Cool storage (+8°C to +15°C)

- 6.5 Ambient plus (+15°C to +25°C)

- 6.6 Ultra-low temperature (-70°C to -40°C)

Chapter 7 Market Estimates and Forecast, By Service Type, 2021 - 2034 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Storage services

- 7.3 Transportation services

- 7.4 Value-added services

- 7.4.1 Blast freezing

- 7.4.2 Labeling and packaging

- 7.4.3 Inventory management

- 7.4.4 Quality control

Chapter 8 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Food & beverage

- 8.2.1 Fresh produce (fruits, vegetables)

- 8.2.2 Dairy products

- 8.2.3 Meat and seafood

- 8.2.4 Frozen foods

- 8.2.5 Processed foods

- 8.3 Pharmaceuticals & healthcare

- 8.3.1 Vaccines and biologics

- 8.3.2 Temperature-sensitive medicines

- 8.3.3 Blood products

- 8.3.4 Medical devices

- 8.4 Chemicals & industrial

- 8.4.1 Specialty chemicals

- 8.4.2 Industrial materials

- 8.4.3 Electronics components

Chapter 9 Market Estimates and Forecast, By End Use, 2021 - 2034 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Logistics & 3PL providers

- 9.3 Food manufacturers

- 9.4 Pharmaceutical companies

- 9.5 Retail chains

- 9.6 E-commerce platforms

- 9.7 Government & healthcare institutions

Chapter 10 Market Estimates and Forecast, By Distribution Channel, 2021 - 2034 (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 Direct

- 10.3 Indirect

Chapter 11 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion) (Thousand Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 Japan

- 11.4.3 India

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 Middle East and Africa

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Bureida Trading & Refrigeration

- 12.2 Carrier Transicold (United Technologies)

- 12.3 China International Marine Containers

- 12.4 Coldstores Group of Saudi Arabia (CGS)

- 12.5 Daikin Industries

- 12.6 DANA Steel

- 12.7 Danfoss

- 12.8 Emerson Electric (Copeland)

- 12.9 Johnson Controls

- 12.10 ORBCOMM

- 12.11 Rivacold

- 12.12 Thermo King (Trane Technologies)

- 12.13 Thermodynamics

- 12.14 TSSC

- 12.15 Zanotti spa

- 12.16 Zhengzhou Kaixue Cold Chain