|

시장보고서

상품코드

1871111

첨단 배전관리 시스템(ADMS)시장 : 기회, 성장 요인, 업계 동향 분석 및 예측(2025-2034년)Advanced Distribution Management System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

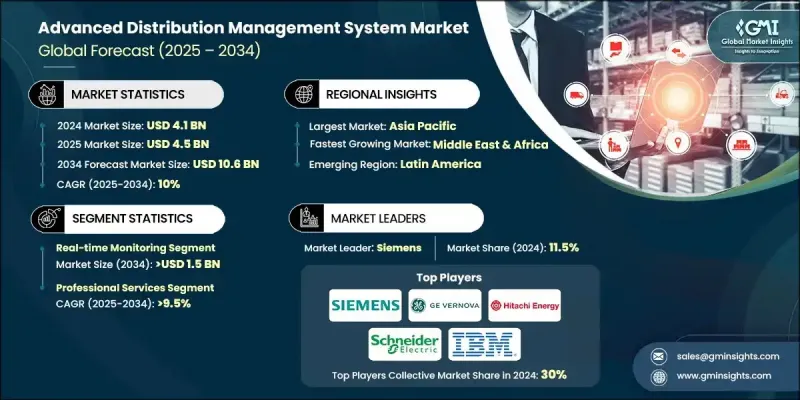

세계의 첨단 배전관리 시스템 시장은 2024년에 41억 달러로 평가되었고, 2034년까지 연평균 복합 성장률(CAGR)은 10%를 나타낼 것으로 예측되며 106억 달러에 달할 전망입니다.

디지털 및 자동화 기술의 급속한 발전은 전력 배전망 관리 방식을 변화시키고 있습니다. 현대적인 ADMS 플랫폼은 이제 인공지능, 엣지 컴퓨팅, 클라우드 네이티브 인프라를 통합하여 확장성, 속도 및 의사 결정 능력을 크게 향상시키고 있습니다. 이러한 발전은 전 세계 유틸리티 기업들 사이에서 광범위한 채택을 주도하고 있습니다. 북미와 유럽은 탄소 중립 달성을 목표로 하는 강력한 규제 프레임워크, 지속 가능성 의무 및 전력망 현대화 프로그램의 지원으로 ADMS 시스템 배포를 주도하고 있습니다. 한편 아시아태평양 지역은 중국과 인도 등 주요 경제권의 급속한 도시화, 증가하는 전력 소비, 인프라 개발에 힘입어 강력한 확장을 보이고 있습니다. ADMS 플랫폼 간 상호 연결성이 높아짐에 따라 사이버 보안에 대한 관심이 증가하며 산업을 형성하고 있습니다. 전력사들은 전력망 안전을 보장하기 위해 안전한 통신 프레임워크, 암호화 시스템, 규정 준수 중심 표준을 구현하고 있습니다. 정전 관리 및 전력망 신뢰성에 대한 규제적 관심이 높아짐에 따라 전력사들은 투명하고 탄력적인 ADMS 구축을 추진하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 기간 | 2025-2034년 |

| 시작 금액 | 41억 달러 |

| 예측 금액 | 106억 달러 |

| CAGR | 10% |

실시간 모니터링 기능 부문은 운영 신뢰성 향상과 정전 최소화에 대한 시급한 필요성에 힘입어 2034년까지 15억 달러 규모에 도달할 것으로 예상됩니다. 에너지 공급업체들은 재생 에너지원, 전기차 통합, 분산형 에너지 자원(DER)으로 인해 점점 더 분산화된 전력망을 관리하고 있습니다. 실시간 모니터링은 전력사가 이상 현상을 신속히 식별하고, 고장을 예측하며, 중단 없는 전력 흐름을 유지하는 데 도움을 줍니다.

전문 서비스 부문은 2034년까지 연평균 9.5% 성장할 것으로 예상됩니다. 이 서비스에는 통합, 컨설팅, 교육 및 지속적인 기술 지원이 포함됩니다. ADMS 시스템이 복잡한 AI, IoT 및 클라우드 통합과 함께 진화함에 따라 유틸리티 기업들은 원활한 구현을 보장하기 위해 전문 서비스 제공업체와 협력하고 있습니다. 배포를 넘어 관리형 서비스 모델은 장기적인 시스템 성능과 신뢰성을 개선하기 위한 지속적인 유지보수, 모니터링 및 최적화를 제공합니다.

미국의 첨단 배전 관리 시스템 시장은 2024년 10억 9,000만 달러 규모에 이르렀습니다. 미국은 전력 송배전 현대화에 지속적으로 대규모 투자를 진행하며 글로벌 ADMS 도입을 가속화하고 있습니다. 미국 기반 전력 회사의 72% 이상이 이미 ADMS 기반 스마트 그리드 시스템을 도입했으며, 이는 전력망 신뢰성, 정전 관리 및 운영 효율성 향상에 대한 국가적 의지를 강조합니다. 대규모 그리드 현대화 사업과 같은 연방 프로그램은 기술 통합을 더욱 촉진하고 있습니다. 미국은 선진적인 에너지 인프라, 적극적인 규제 접근 방식, 높은 기술 혁신 및 도입률로 인해 글로벌 리더 지위를 유지하고 있습니다.

세계의 첨단 배전관리 시스템 시장에서 사업을 전개하는 주요 기업으로는 히타치에너지, GE버노바, IBM, 지멘스, 슈나이더 일렉트릭이 포함되어 있으며, 이들 기업이 글로벌 시장 점유율의 30% 이상을 차지합니다. 고급 배전 관리 시스템 시장에서 경쟁하는 기업들은 입지를 공고히 하기 위해 다양한 전략을 채택하고 있습니다. AI 기반 분석, 자동화 및 실시간 데이터 통합을 강화하기 위해 연구개발(R&D) 투자를 최우선으로 하고 있습니다. 많은 기업들이 전력사 및 정부와의 전략적 제휴를 통해 전력망 현대화를 가속화하고 글로벌 진출을 확대하고 있습니다. 확장성을 개선하고 운영 비용을 절감하기 위해 클라우드 네이티브 및 모듈형 ADMS 플랫폼이 도입되고 있습니다. 기업들은 또한 디지털 인프라를 보호하기 위해 사이버 보안 체계를 강화하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 규제 상황

- 업계에 미치는 영향요인

- 성장 촉진요인

- 업계의 잠재적 억제요인 및 과제

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

- 새로운 기회와 동향

- 디지털화와 IoT 통합

- 신흥 시장 진출

- 투자분석과 전망

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석 : 지역별

- 북미

- 유럽

- 아시아태평양

- 중동 및 아프리카

- 라틴아메리카

- 전략적 노력

- 경쟁 벤치마킹의 도해

- 전략 대시보드

- 혁신과 기술의 정세

제5장 첨단 배전관리 시스템 시장 규모와 예측 : 기능별(2021-2034년)

- 주요 동향

- 실시간 모니터링

- 부하 분산

- 정전 관리

- 전압 최적화

- 수요 반응

- 분산형 에너지 자원(DER) 통합

제6장 첨단 배전관리 시스템 시장 규모와 예측 : 서비스별(2021-2034년)

- 주요 동향

- 전문 서비스

- 관리 서비스

제7장 첨단 배전관리 시스템 시장 규모와 예측 : 도입 형태별(2021-2034년)

- 주요 동향

- 클라우드 기반

- 온프레미스

제8장 첨단 배전관리 시스템 시장 규모와 예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 에너지 및 유틸리티

- IT 및 통신

- 제조업

- 방위 및 정부 기관

- 인프라

- 헬스케어

- 운송 및 물류

- 기타

제9장 첨단 배전관리 시스템 시장 규모와 예측 : 지역별(2021-2034년)

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 영국

- 프랑스

- 네덜란드

- 이탈리아

- 스페인

- 스웨덴

- 덴마크

- 독일

- 러시아

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 중동 및 아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 카타르

- 이집트

- 남아프리카

- 라틴아메리카

- 브라질

- 아르헨티나

- 페루

제10장 기업 프로파일

- Aspen Technology

- Cyient

- DNV

- Eaton

- Elipse Software

- Energyhub

- ETAP

- GE Vernova

- HCL tech

- Hitachi Energy

- IBM Corporation

- Itron Inc.

- Minsait ACS

- Oracle

- Schneider Electric

- Siemens

- Survalent Technology Corporation

- Wipro Ltd.

The Global Advanced Distribution Management System Market was valued at USD 4.1 Billion in 2024 and is estimated to grow at a CAGR of 10% to reach USD 10.6 Billion by 2034.

Rapid advancements in digital and automation technologies are transforming how power distribution networks are managed. Modern ADMS platforms now integrate artificial intelligence, edge computing, and cloud-native infrastructure, significantly improving their scalability, speed, and decision-making capabilities. These advancements are driving widespread adoption among utilities across the globe. North America and Europe are leading the deployment of ADMS systems, supported by strong regulatory frameworks, sustainability mandates, and grid modernization programs aimed at achieving carbon neutrality. Meanwhile, the Asia-Pacific region is witnessing robust expansion, supported by rapid urbanization, rising electricity consumption, and infrastructure development in major economies such as China and India. As ADMS platforms become more interconnected, the growing focus on cybersecurity is shaping the industry. Utilities are implementing secure communication frameworks, encryption systems, and compliance-driven standards to ensure grid safety. Increasing regulatory focus on outage management and grid reliability is also pushing utilities toward transparent and resilient ADMS deployment.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.1 Billion |

| Forecast Value | $10.6 Billion |

| CAGR | 10% |

The real-time monitoring functionality segment is estimated to reach USD 1.5 Billion by 2034, driven by the urgent need to enhance operational reliability and minimize power outages. Energy providers are managing increasingly decentralized grids with renewable power sources, electric vehicle integration, and distributed energy resources (DERs). Real-time monitoring helps utilities quickly identify anomalies, predict faults, and maintain uninterrupted power flow.

The professional services segment is anticipated to grow at a CAGR of 9.5% through 2034. These services include integration, consulting, training, and ongoing technical support. As ADMS systems evolve with complex AI, IoT, and cloud integrations, utilities are partnering with specialized service providers to ensure smooth implementation. Beyond deployment, managed service models offer continuous maintenance, monitoring, and optimization to improve long-term system performance and reliability.

U.S. Advanced Distribution Management System Market generated USD 1.09 Billion in 2024. The country continues to invest heavily in power transmission and distribution modernization, accelerating global ADMS adoption. More than 72% of U.S.-based utility companies have already implemented ADMS-enabled smart grid systems, underscoring the strong national commitment to improving grid reliability, outage management, and operational efficiency. Federal programs, such as large-scale grid modernization initiatives, are further fueling technology integration. The U.S. remains a global leader due to its advanced energy infrastructure, proactive regulatory approach, and high rate of technology innovation and deployment.

Major companies operating in the Global Advanced Distribution Management System Market include Hitachi Energy, GE Vernova, IBM, Siemens, and Schneider Electric, which collectively account for over 30% of the global market share. Companies competing in the Advanced Distribution Management System Market are adopting multiple strategies to solidify their position. They are prioritizing R&D investments to enhance AI-driven analytics, automation, and real-time data integration. Many are forming strategic alliances with utilities and governments to accelerate grid modernization and expand global reach. Cloud-native and modular ADMS platforms are being introduced to improve scalability and lower operational costs. Firms are also strengthening their cybersecurity frameworks to safeguard digital infrastructure.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technological factors

- 3.6.5 Legal factors

- 3.6.6 Environmental factors

- 3.7 Emerging opportunities & trends

- 3.7.1 Digitalization & IoT integration

- 3.7.2 Emerging market penetration

- 3.8 Investment analysis & future outlook

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, by Region, 2024

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Strategic initiatives

- 4.4 Competitive benchmarking depictions

- 4.5 Strategy dashboard

- 4.6 Innovation & technology landscape

Chapter 5 Advanced Distribution Management System Market Size and Forecast, By Functionality, 2021 - 2034 (USD Million)

- 5.1 Key trends

- 5.2 Real-time monitoring

- 5.3 Load balancing

- 5.4 Outage management

- 5.5 Voltage optimization

- 5.6 Demand response

- 5.7 Integration of Distributed Energy Resources (DERs)

Chapter 6 Advanced Distribution Management System Market Size and Forecast, By Service, 2021 - 2034 (USD Million)

- 6.1 Key trends

- 6.2 Professional

- 6.3 Managed

Chapter 7 Advanced Distribution Management System Market Size and Forecast, By Deployment, 2021 - 2034 (USD Million)

- 7.1 Key trends

- 7.2 Cloud based

- 7.3 On premise

Chapter 8 Advanced Distribution Management System Market Size and Forecast, By End Use, 2021 - 2034 (USD Million)

- 8.1 Key trends

- 8.2 Energy and utilities

- 8.3 IT and Telecommunications

- 8.4 Manufacturing

- 8.5 Defence and government

- 8.6 Infrastructure

- 8.7 Healthcare

- 8.8 Transportation and logistics

- 8.9 Others

Chapter 9 Advanced Distribution Management System Market Size and Forecast, By Region, 2021 - 2034 (USD Million)

- 9.1 North America

- 9.1.1 U.S.

- 9.1.2 Canada

- 9.1.3 Mexico

- 9.2 Europe

- 9.2.1 UK

- 9.2.2 France

- 9.2.3 Netherlands

- 9.2.4 Italy

- 9.2.5 Spain

- 9.2.6 Sweden

- 9.2.7 Denmark

- 9.2.8 Germany

- 9.2.9 Russia

- 9.3 Asia Pacific

- 9.3.1 China

- 9.3.2 India

- 9.3.3 Japan

- 9.3.4 South Korea

- 9.3.5 Australia

- 9.4 Middle East & Africa

- 9.4.1 Saudi Arabia

- 9.4.2 UAE

- 9.4.3 Qatar

- 9.4.4 Egypt

- 9.4.5 South Africa

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Argentina

- 9.5.3 Peru

Chapter 10 Company Profiles

- 10.1 Aspen Technology

- 10.2 Cyient

- 10.3 DNV

- 10.4 Eaton

- 10.5 Elipse Software

- 10.6 Energyhub

- 10.7 ETAP

- 10.8 GE Vernova

- 10.9 HCL tech

- 10.10 Hitachi Energy

- 10.11 IBM Corporation

- 10.12 Itron Inc.

- 10.13 Minsait ACS

- 10.14 Oracle

- 10.15 Schneider Electric

- 10.16 Siemens

- 10.17 Survalent Technology Corporation

- 10.18 Wipro Ltd.