|

시장보고서

상품코드

1871125

전자 제품용 산화아연 나노 입자 시장 : 기회, 성장 요인, 업계 동향 분석 및 예측(2025-2034년)Zinc Oxide Nanoparticles for Electronics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

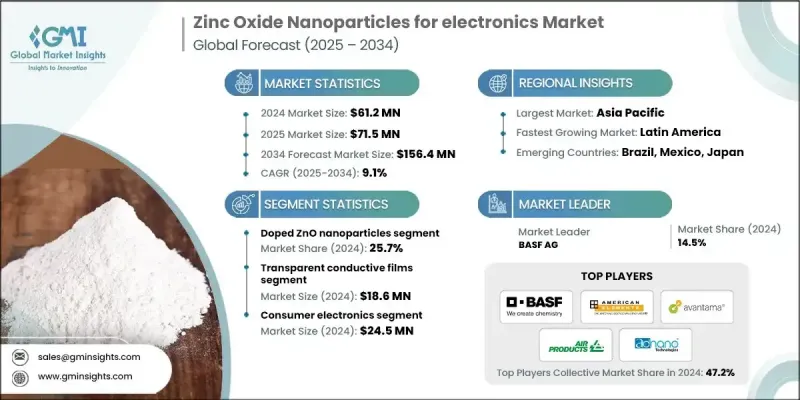

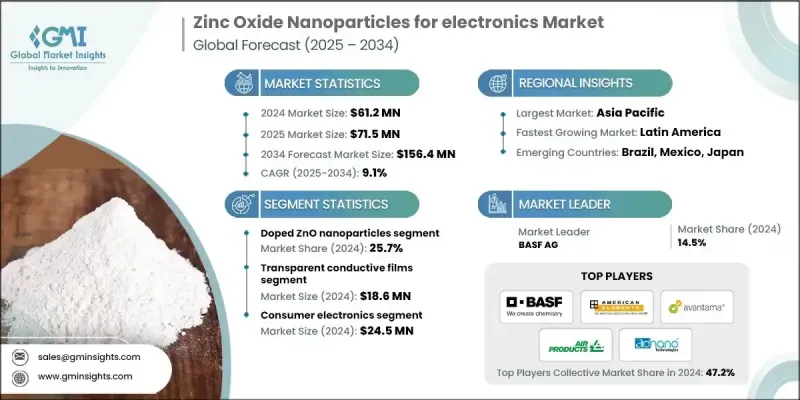

세계의 전자 제품용 산화아연 나노 입자 시장은 2024년 6,120만 달러로 평가되었고, 2034년까지 연평균 복합 성장률(CAGR)은 9.1%를 나타낼 것으로 예측되며 1억 5,640만 달러에 달할 전망입니다.

시장 확장은 소형화된 고성능 전자 부품에 대한 수요 증가에 의해 주도되고 있습니다. 산화아연 나노구조체는 탁월한 전자 이동도, 넓은 밴드갭 특성, 가시광선 스펙트럼에서의 투명성을 보여 투명 전도성 필름 및 고효율 센서를 포함한 첨단 전자기기에 이상적입니다. 높은 표면적, 자외선 차단 능력, 우수한 반도체 특성 등 독특한 특징으로 인해 박막 트랜지스터, 광전자공학, 플렉서블 전자기기 부문에서 광범위하게 채택되고 있습니다. 아시아태평양 지역은 견고한 전자 제조 생태계, 숙련된 노동력 확보, 비용 경쟁력 덕분에 생산 및 소비에서 계속해서 주도적 위치를 차지하고 있습니다. 차세대 전자 제품에 대한 투자 증가와 새로운 나노구조체 연구는 제조업체들이 장치 성능과 에너지 효율성을 높이기 위해 일반 등급 재료에서 특수 도핑된 나노입자, 나노로드, 나노와이어로 초점을 전환함에 따라 성장을 더욱 촉진하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 기간 | 2025-2034년 |

| 시작 금액 | 6,120만 달러 |

| 예측 금액 | 1억 5,640만 달러 |

| CAGR | 9.1% |

도핑된 산화아연 나노입자, 나노로드 및 나노와이어는 전기적 및 광학적 성능 개선으로 주목받으며, 플렉서블 전자기기, 재생 에너지 장치 및 광전자 센서 부문의 혁신을 지원하고 있습니다. 나노로드 및 나노와이어 부문를 포함한 1차원 ZnO 구조물은 20.4%의 점유율을 차지했으며, 2025-2034년 9.7%의 최고 CAGR로 성장할 것으로 예상됩니다. 이들의 이방성 기하 구조는 표면적 증가와 방향성 전자 운송을 제공하여 센서 응용 부문에서 매우 효과적입니다. 그러나 제어된 비율 합성은 여전히 도전 과제로 남아 생산을 제한하는 동시에 지속적인 연구 개발 노력을 촉진하고 있습니다. 초음파 보조 분포와 같은 첨단 제조 방법도 재료 성능 최적화를 위해 연구되고 있습니다.

가스 센서 부문은 2024년 21.6%의 점유율을 기록했으며, IoT 기기 및 환경 모니터링 시스템의 채택 증가에 힘입어 2034년까지 연평균 8.4%의 성장률을 보일 것으로 예상됩니다. 산화아연 나노입자는 다양한 가스에 매우 민감하며 특정 감지 시 6-8초의 빠른 응답 시간을 제공합니다. 자체 전원 공급 능력으로 에너지 효율성 문제를 해결하여 분산형 스마트 센서 네트워크 및 실시간 모니터링 애플리케이션에 적합합니다.

북미의 전자 제품용 산화아연 나노 입자 시장은 2024년 1,490만 달러 규모였습니다. 해당 지역은 강력한 전자 제조 인프라, 선진 연구 기관, 스마트 및 웨어러블 기술에 대한 증가하는 수요의 혜택을 받고 있습니다. 투명 전도성 필름, 자외선 센서, 압전 장치 부문의 응용이 시장을 주도하고 있으며, 상당한 정부 자금 지원과 민간 부문 투자가 이를 뒷받침하고 있습니다. 기술 기업과 대학 간의 전략적 협력은 상용화를 가속화하고 혁신적인 제품 개발을 가능케 하고 있습니다.

세계의 전자 제품용 산화아연 나노 입자 시장에서 사업을 전개하는 주요 기업으로는 American Elements, MSE Supplies LLC, SAT NANO, Techinstro, BASF AG, Noah Chemicals, Shilpa Enterprises, Silox India Pvt Ltd, Avantama AG, AdNano Technologies Pvt Ltd, Ossila Ltd 등이 있습니다. 글로벌 전자용 산화아연 나노입자 시장의 기업들은 ZnO 나노구조체의 전기적 및 광학적 성능 향상을 위한 연구개발에 대규모 투자를 통해 입지를 공고히 하는 전략을 채택하고 있습니다. 플렉서블 전자기기, 센서, 재생에너지 장치 등 특수 응용 부문를 위한 도핑 나노입자, 나노로드, 나노와이어로 제품 포트폴리오를 다각화하고 있습니다. 대학, 연구기관, 산업 파트너와의 전략적 협력이 혁신과 상용화를 가속화하고 있습니다. 기업들은 신흥 시장의 증가하는 수요를 충족시키기 위해 품질 유지와 동시에 생산 규모 확대에 주력하고 있습니다. 우수한 성능, 신뢰성 및 에너지 효율성을 강조하는 마케팅 활동은 브랜드 인지도 제고와 시장 입지 강화에 기여하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 전자 제품의 소형화

- 투명 전도성 필름에 대한 수요 증가

- 플렉서블 전자 기술의 발전

- 자외선 차단 요구 증가

- 업계의 잠재적 억제요인 및 과제

- 규제 준수의 복잡성

- 제조 확장성 문제

- 건강과 안전에 대한 우려 사항

- 시장 기회

- 신흥 양자점 응용 부문

- 차세대 태양전지의 통합

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 가격 동향

- 지역별

- 제품

- 용도

- 최종 이용 산업

- 장래 시장 동향

- 기술과 혁신의 상황

- 현재의 기술 동향

- 신흥기술

- 특허 상황

- 무역 통계(HS코드)(참고 : 무역 통계는 주요 국가에서만 제공됨)

- 주요 수입국

- 주요 수출국

- 지속가능성과 환경면

- 지속가능한 대처

- 폐기물 감축 전략

- 생산에서의 에너지 효율

- 환경에 배려한 대처

- 탄소발자국에 관한 고려 사항

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병 및 인수

- 제휴 및 협업

- 신제품 발매

- 확대 계획

제5장 시장 추계 및 예측 : 제품별(2021-2034년)

- 주요 동향

- 산화아연 나노입자(0d)

- 구형 나노입자(1-50nm)

- 구형 나노입자(50-100nm)

- 구형 나노입자(100-200nm)

- 산화아연 나노로드/나노와이어(1d)

- 단척 나노로드(길이 <1μm)

- 장척 나노와이어(길이>1μm)

- 정렬 나노로드 배열

- 도핑된 산화아연 나노입자

- 알루미늄 도핑 ZnO(AZO)

- 갈륨 도핑 ZnO(GZO)

- 인듐 도핑 ZnO(IZO)

- 기타 금속 도핑 변형체

- 산화아연 양자점

- 초소형 양자점(< 5nm)

- 중형 양자점(5-10 nm)

- 산화아연 나노 복합

- ZnO-그래핀 복합재료

- ZnO-금속 하이브리드 구조

- ZnO-폴리머 나노복합재료

제6장 시장 추계 및 예측 : 용도별(2021-2034년)

- 주요 동향

- 투명 전도성 필름

- 디스플레이

- 터치 패널 통합

- 태양전지 전극

- 스마트 윈도우 기술

- 가스 센서

- 환경 모니터링 센서

- 산업용 공정 제어 센서

- 자동차 배출 가스 센서

- 실내 공기질 센서

- 광검출기 및 자외선 센서

- 자외선 검출 시스템

- UV-b 및 UV-c 검출

- 화염 감지 용도

- 광통신 부품

- 박막 트랜지스터(TFT)

- 디스플레이용 백플레인 TFT

- 플렉서블 전자 TFT

- 고주파 TFT

- 태양전지 부품

- 전자 운송층

- 광양극

- 버퍼층 통합

- 메모리 장치

- 저항성 랜덤 액세스 메모리(ReRAM)

- 일회성 기록 다중 읽기(WORM) 메모리

- 신경모방 컴퓨팅 응용

제7장 시장 추계 및 예측 : 최종 이용 산업별(2021-2034년)

- 주요 동향

- 반도체 제조

- 웨이퍼 가공 용도

- 스퍼터링 타겟의 제조

- 화학 기상 증착법

- 원자층 증착법

- 소비자용 전자 기기

- 스마트폰 및 태블릿 통합

- 웨어러블 디바이스용 용도

- 가전 제품

- 게임 및 엔터테인먼트 시스템

- 자동차용 전자 기기

- 첨단 운전자 보조 시스템(ADAS)

- 전기자동차 부품

- 인포테인먼트 시스템

- 엔진 제어 장치

- 재생에너지

- 태양광 발전 셀 제조

- 에너지 저장 시스템

- 스마트 그리드 기술

- 풍력발전용 전자기기

- 산업용 전자 기기

- 공정 제어 시스템

- 공장 자동화

- 로보틱스 응용

- 전력 관리 시스템

제8장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 기타 라틴아메리카

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

제9장 기업 프로파일

- American Elements

- BASF AG

- Air Products and Chemicals Inc

- SAT NANO

- Techinstro

- MSE Supplies LLC

- Noah Chemicals

- Silox India Pvt Ltd

- Shilpa Enterprises

- Avantama AG

- Ossila Ltd

- AdNano Technologies Pvt Ltd

The Global Zinc Oxide Nanoparticles for Electronics Market was valued at USD 61.2 million in 2024 and is estimated to grow at a CAGR of 9.1% to reach USD 156.4 million by 2034.

The market expansion is driven by rising demand for miniaturized, high-performance electronic components. Zinc oxide nanostructures exhibit exceptional electron mobility, wide bandgap properties, and transparency in the visible light spectrum, making them ideal for advanced electronics, including transparent conductive films and high-efficiency sensors. Their unique features, such as high surface area, UV-blocking capability, and superior semiconducting behavior, have led to widespread adoption in thin-film transistors, optoelectronics, and flexible electronic devices. Asia Pacific continues to dominate production and consumption due to its robust electronics manufacturing ecosystem, availability of skilled labor, and cost advantages. Increasing investment in next-generation electronics and research into novel nanostructures further fuels growth, as manufacturers shift focus from commodity-grade materials to specialized doped nanoparticles, nanorods, and nanowires to enhance device performance and energy efficiency.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $61.2 Million |

| Forecast Value | $156.4 Million |

| CAGR | 9.1% |

Doped zinc oxide nanoparticles, along with nanorods and nanowires, are gaining prominence for their electrical and optical improvements, supporting innovations in flexible electronics, renewable energy devices, and optoelectronic sensors. One-dimensional ZnO structures, including nanorods and nanowires segments, held a 20.4% share and are expected to grow at the highest CAGR of 9.7% from 2025 to 2034. Their anisotropic geometry provides increased surface area and directional electron transport, making them highly effective in sensor applications. However, controlled ratio synthesis remains a challenge, limiting production while driving ongoing research and development efforts. Advanced manufacturing methods, such as ultrasonic-assisted distribution, are also being explored to optimize material performance.

The gas sensors segment held 21.6% share in 2024 and is expected to grow at a CAGR of 8.4% through 2034, driven by increasing adoption of IoT devices and environmental monitoring systems. Zinc oxide nanoparticles are highly sensitive to various gases and provide rapid response times of 6-8 seconds for certain detections. Their self-powered capability addresses energy efficiency concerns, making them suitable for distributed smart sensor networks and real-time monitoring applications.

North America Zinc Oxide Nanoparticles for Electronics Market accounted for USD 14.9 million in 2024. The region benefits from strong electronics manufacturing infrastructure, advanced research institutions, and growing demand for smart and wearable technologies. Applications in transparent conductive films, UV sensors, and piezoelectric devices are leading the market, supported by substantial government funding and private sector investment. Strategic collaborations between technology companies and universities are accelerating commercialization and enabling innovative product development.

Key companies operating in the Global Zinc Oxide Nanoparticles for Electronics Market include American Elements, MSE Supplies LLC, SAT NANO, Techinstro, BASF AG, Noah Chemicals, Shilpa Enterprises, Silox India Pvt Ltd, Avantama AG, AdNano Technologies Pvt Ltd, and Ossila Ltd. Companies in the Global Zinc Oxide Nanoparticles for Electronics Market are adopting strategies to solidify their position by investing heavily in research and development to improve the electrical and optical performance of ZnO nanostructures. They are diversifying their product portfolios with doped nanoparticles, nanorods, and nanowires for specialized applications in flexible electronics, sensors, and renewable energy devices. Strategic collaborations with universities, research institutes, and industrial partners are accelerating innovation and commercialization. Firms are focusing on scaling production while maintaining quality to meet rising demand in emerging markets. Marketing initiatives emphasizing superior performance, reliability, and energy efficiency help enhance brand visibility and strengthen market foothold.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Application

- 2.2.4 End Use Industry

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Miniaturization of electronic devices

- 3.2.1.2 Growing demand for transparent conductive films

- 3.2.1.3 Advancement in flexible electronics

- 3.2.1.4 Increasing uv protection requirement

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Regulatory compliance complexity

- 3.2.2.2 Manufacturing scalability challenges

- 3.2.2.3 Health & safety concerns

- 3.2.3 Market opportunities

- 3.2.3.1 Emerging quantum dot applications

- 3.2.3.2 Next-generation solar cell integration

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and Innovation Landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 Product

- 3.7.3 Application

- 3.7.4 End Use Industry

- 3.8 Future market trends

- 3.9 Technology and Innovation Landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Zno nanoparticles (0d)

- 5.2.1 Spherical nanoparticles (1-50 nm)

- 5.2.2 Spherical nanoparticles (50-100 nm)

- 5.2.3 Spherical nanoparticles (100-200 nm)

- 5.3 Zno nanorods/nanowires (1d)

- 5.3.1 Short nanorods (length <1 μm)

- 5.3.2 Long nanowires (length >1 μm)

- 5.3.3 Aligned nanorod arrays

- 5.4 Doped zno nanoparticles

- 5.4.1 Aluminum-doped zno (AZO)

- 5.4.2 Gallium-doped zno (GZO)

- 5.4.3 Indium-doped zno (IZO)

- 5.4.4 Other metal-doped variants

- 5.5 Zno quantum dots

- 5.5.1 Ultra-small quantum dots (<5 nm)

- 5.5.2 Medium quantum dots (5-10 nm)

- 5.6 Zno nanocomposites

- 5.6.1 Zno-graphene composites

- 5.6.2 Zno-metal hybrid structures

- 5.6.3 Zno-polymer nanocomposites

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Transparent conductive films

- 6.2.1 Display applications

- 6.2.2 Touch panel integration

- 6.2.3 Solar cell electrodes

- 6.2.4 Smart window technologies

- 6.3 Gas sensors

- 6.3.1 Environmental monitoring sensors

- 6.3.2 Industrial process control sensors

- 6.3.3 Automotive emission sensors

- 6.3.4 Indoor air quality sensors

- 6.4 Photodetectors & UV sensors

- 6.4.1 UV-a detection systems

- 6.4.2 UV-b & UV-c detection

- 6.4.3 Flame detection applications

- 6.4.4 Optical communication components

- 6.5 Thin Film Transistors (TFTs)

- 6.5.1 Display Backplane TFTs

- 6.5.2 Flexible Electronics TFTs

- 6.5.3 Radio Frequency TFTs

- 6.6 Solar Cell Components

- 6.6.1 Electron Transport Layers

- 6.6.2 Photoanode Applications

- 6.6.3 Buffer Layer Integration

- 6.7 Memory Devices

- 6.7.1 Resistive Random Access Memory (ReRAM)

- 6.7.2 Write-Once Read-Many (WORM) Memory

- 6.7.3 Neuromorphic Computing Applications

Chapter 7 Market Estimates and Forecast, By End Use Industry, 2021 - 2034 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Semiconductor manufacturing

- 7.2.1 Wafer processing applications

- 7.2.2 Sputtering target production

- 7.2.3 Chemical vapor deposition

- 7.2.4 Atomic layer deposition

- 7.3 Consumer electronics

- 7.3.1 Smartphone & tablet integration

- 7.3.2 Wearable device applications

- 7.3.3 Home appliance electronics

- 7.3.4 Gaming & entertainment systems

- 7.4 Automotive electronics

- 7.4.1 Advanced driver assistance systems (adas)

- 7.4.2 Electric vehicle components

- 7.4.3 Infotainment systems

- 7.4.4 Engine control units

- 7.5 Renewable energy

- 7.5.1 Photovoltaic cell manufacturing

- 7.5.2 Energy storage systems

- 7.5.3 Smart grid technologies

- 7.5.4 Wind power electronics

- 7.6 Industrial electronics

- 7.6.1 Process control systems

- 7.6.2 Factory automation

- 7.6.3 Robotics applications

- 7.6.4 Power management systems

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 American Elements

- 9.2 BASF AG

- 9.3 Air Products and Chemicals Inc

- 9.4 SAT NANO

- 9.5 Techinstro

- 9.6 MSE Supplies LLC

- 9.7 Noah Chemicals

- 9.8 Silox India Pvt Ltd

- 9.9 Shilpa Enterprises

- 9.10 Avantama AG

- 9.11 Ossila Ltd

- 9.12 AdNano Technologies Pvt Ltd