|

시장보고서

상품코드

2007706

산화 아연 시장 예측(-2031년) : 제조 프로세스(간접법, 직접법, 습식 화학법), 등급(표준, 처리, USP, FCC), 용도(고무, 세라믹, 화학제품, 화장품 및 퍼스널케어, 의약품), 지역별Zinc Oxide Market By Process (Indirect, Direct, Wet-Chemical), Grade (Standard, Treated, USP, FCC), Application (Rubber, Ceramics, Chemicals, Cosmetics & Personal Care, Pharmaceuticals), and Region - Global Forecast to 2031 |

||||||

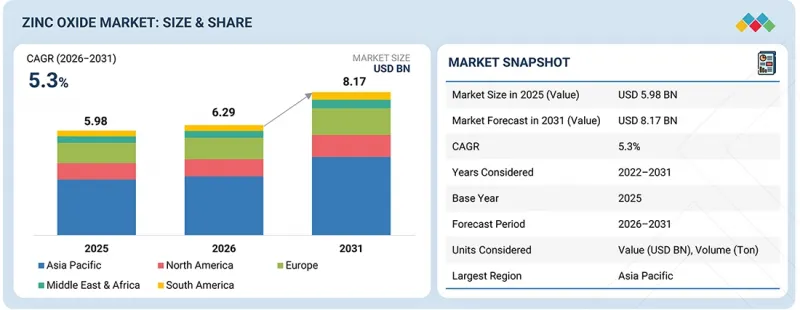

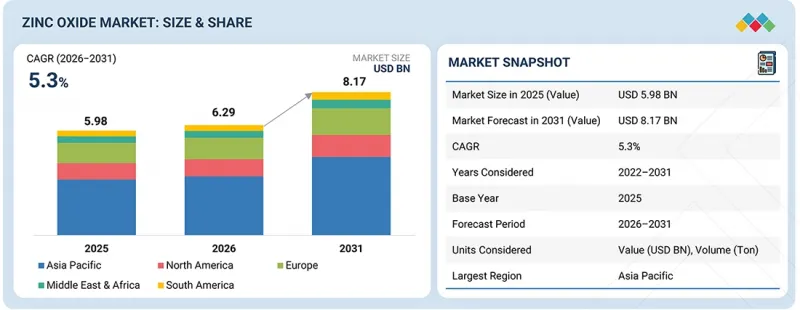

산화 아연 시장 규모는 예측 기간 중 CAGR 5.3%로 확대하며, 2026년 62억 9,000만 달러에서 2031년에는 81억 7,000만 달러에 달할 것으로 전망되고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2022-2031년 |

| 기준연도 | 2025년 |

| 예측 기간 | 2026-2031년 |

| 대상 단위 | 금액(달러)·톤 |

| 부문 | 프로세스, 등급, 용도, 지역 |

| 대상 지역 | 북미, 아시아태평양, 유럽, 중동 및 아프리카, 남미 |

산화아연의 수요는 자동차 고무, 세라믹, 화장품 및 퍼스널 케어, 의약품 등 다양한 분야에서 산화아연에 대한 수요 증가에 기인합니다.

"예측 기간 중 다이렉트 방식이 두 번째로 큰 부문이 될 것으로 예상됩니다. "

프로세스별로 보면 2위는 직접법(미국법)이 차지하고 있습니다. 이는 가장 비용 효율적이고 대량 생산의 산업 공정에 적합하기 때문입니다. 이 공정은 광석, 잔류물, 2차 원료 등의 형태로 아연을 함유한 원료를 사용하여 이루어집니다. 따라서 특히 가격에 민감한 시장에서는 간접(프랑스) 프로세스보다 비용 효율성이 높다고 할 수 있습니다. 생성되는 산화아연(ZnO)의 순도나 입자 크기는 낮지만, 고순도가 필수적이지 않은 고무, 세라믹, 일부 화학제품 등에서는 선호되는 것으로 알려져 있습니다. 재활용 원료와 저급 원료를 사용할 수 있고, 순환 경제의 실천을 촉진한다는 점에서 비용 최적화와 지속가능성을 중시하는 산업에서 이 공정은 매력적입니다. 대량 생산 및 비용 중심의 부문에서 높은 점유율과 원료 조달의 유연성으로 인해 직접법이 계속해서 주요한 역할을 할 것으로 예상됩니다.

"예측 기간 중 처리 등급이 두 번째로 큰 부문이 될 것으로 예상됩니다. "

등급별로는 가공용 산화아연이 2위를 차지할 것으로 예상됩니다. 이는 표준 등급보다 높은 기능성을 가지면서도 USP 등급이나 특수 고순도 등급보다 저렴한 비용으로 생산할 수 있기 때문입니다. 표면 개질 또는 표면 코팅 처리된 산화아연은 분산성이 높고, 폴리머와의 배합이 가능하며, 응집 저항성을 가지고 있으며, 고무, 플라스틱, 표면 가공제에 널리 활용되고 있습니다. 비용과 성능의 균형이 뛰어나며, 표준 등급의 산화아연에 비해 성능이 우수하지만 의약품 및 식품 등급의 재료만큼 비싸지 않습니다. 산업 및 자동차 분야의 강력한 수요로 인해 가공용 산화아연은 중요하고 확고한 시장 부문이 되었습니다.

"세라믹은 예측 기간 중 두 번째로 큰 부문이 될 것으로 예상됩니다. "

용도별로는 세라믹이 두 번째로 큰 용도 부문이 될 것으로 예상됩니다. 이는 세라믹 제품의 물리적 및 외관 특성 향상에 널리 활용되고 있으며, 건설 및 소비재 시장의 안정적인 수요를 배경으로 하고 있습니다. 산화아연은 세라믹 유약, 에나멜, 프릿에 널리 사용되어 밝기, 광택, 열 안정성, 내균열성을 향상시킵니다. 또한 플럭스제 역할을 하여 소성 온도를 낮추고, 제조시 에너지 소비 효율을 높입니다. 건설 산업에서 타일, 위생도기, 장식용 세라믹 제품에 대한 높은 수요도 이 산업에서 산화아연의 대규모 대량 소비를 촉진하고 있습니다. 또한 산화아연은 전기 세라믹 및 특수 세라믹 부품에도 사용되어 그 응용 범위가 확대되고 있습니다. 광범위한 응용 분야와 지속적인 건설 수요, 제품 품질 향상제로서 산화아연의 기능적 중요성으로 인해 세라믹은 항상 가장 중요한 분야 중 하나였습니다.

"유럽이 금액 기준 2위를 차지할 것으로 전망"

산화아연의 두 번째로 큰 시장은 유럽입니다. 이는 탄탄한 산업기반, 건전한 자동차 산업, 의약품, 화장품 등 고부가가치 시장에서의 우위 때문인 것으로 분석됩니다. 이 지역의 자동차 부문은 잘 확립되어 있으며, 타이어 및 고무 생산에서 산화아연의 안정적인 수요에 기여하고 있습니다. 전동화 추세가 더욱 진전됨에 따라 이 소재에 대한 수요는 더욱 확대될 것으로 예상됩니다. 또한 유럽은 개보수 공사, 지속가능성 프로젝트, 인프라 구축에 힘입어 발전된 건설 산업이 있으며, 이는 건축용 페인트, 코팅, 세라믹의 산화아연 소비를 주도하고 있습니다. 유럽의 주요 특징 중 하나는 특히 제약, 퍼스널 케어, 특수 화학 분야에서 고품질의 규제 대상 특수 용도이며, 이러한 분야에서는 고순도 및 USP 등급의 산화아연에 대한 수요가 높습니다. 결론적으로 유럽은 기술력, 고부가가치 용도, 혁신에 의해 주도되는 산업에서 우위를 점하고 있으며, 세계 주요하고 안정적인 산화아연 시장으로 남아있습니다.

세계의 산화아연(Zinc Oxide) 시장을 조사했으며, 시장 개요, 시장 성장에 영향을 미치는 각종 영향요인 분석, 기술-특허 동향, 법-규제 환경, 사례 분석, 시장 규모 추이와 예측, 각종 부문별-지역별-주요 국가별 상세 분석, 경쟁 구도, 주요 기업 개요 등의 정보를 정리하여 전해드립니다.

자주 묻는 질문

목차

제1장 서론

제2장 개요

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술의 진보, AI에 의한 영향, 특허, 혁신, 향후 용도

제7장 지속가능성과 규제 상황

제8장 고객 상황과 구매 행동

제9장 산화 아연 시장 : 제조 프로세스별

제10장 산화 아연 시장 : 등급별

제11장 산화 아연 시장 : 용도별

제12장 산화 아연 시장 : 지역별

제13장 경쟁 구도

제14장 기업 개요

제15장 조사 방법

제16장 부록

KSA 26.04.29The zinc oxide market is projected to grow from USD 6.29 billion in 2026 to USD 8.17 billion by 2031, at a CAGR of 5.3% during the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2022-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | Value (USD Billion) Volume (Ton) |

| Segments | Process, Grade, Application, and Region |

| Regions covered | North America, Asia Pacific, Europe, the Middle East & Africa, and South America |

The demand for zinc oxide is attributed to the growing demand for the product from various applications, including rubber in automotive, ceramics, cosmetics & personal care, and pharmaceutical applications.

"Direct process projected to be the second-largest segment during the forecast period."

The second-largest segment of the zinc oxide market, based on the process, is occupied by the direct (American) process, as it is the most cost-effective and has high suitability in bulk industrial processes. This is carried out with zinc-containing raw materials in the form of ores, residues, or even secondary sources. This process is therefore more cost-effective than the indirect (French) process, particularly in price-sensitive markets. Although it yields ZnO with reduced purity and particle size, these are found to be favorable in products such as rubber, ceramics, and some chemicals, where high purity is not essential. Its capabilities to use recycled or lower-grade feedstock as well as facilitate the practice of circular economy make it appealing in the industries where the focus is on optimization of costs and sustainability. Its high presence in high-volume, cost-oriented segments, along with its flexibility in terms of sourcing raw materials, also ensures that the direct process continues playing a major role, albeit secondary in the global ZnO market.

"Treated segment projected to be the second-largest segment during the forecast period."

The second-largest grade segment is projected to be taken by the treated zinc oxide because it has higher functional characteristics than standard grade, and is less expensive than high-purity USP or specialty grades. Surface modification or surface-coated treated ZnO is able to be dispersed, allowing it to be combined with polymers, and provides agglomeration resistance, thus finding great application in rubber, plastics, and finishes. It has a good compromise between cost and performance, which means that it has better performance compared to standard ZnO, but it is not as expensive as pharmaceutical or food-grade materials. Strong demand from the industrial and automotive sectors makes treated ZnO an important and well-established market segment.

"The ceramics segment is projected to be the second-largest segment during the forecast period."

The second-largest application of zinc oxide is the ceramics segment because of the numerous applications in improving the physical and aesthetic properties of the ceramic products, coupled with the stable demand of construction and consumer goods markets. ZnO finds large applications in ceramic glazes, enamels, and frits, and enhances brightness, gloss, thermal stability, and crack resistance. It works as well as a fluxing agent, which reduces the firing temperature and efficiency in energy consumption during production. The high demand for tiles, sanitary ware, and decorative ceramics in the construction industry facilitates the consumption of ZnO in mass on a large scale in this industry. Besides, ZnO is also used in electroceramics and specialty ceramic parts, and the range of its application is also expanded, which guarantees the fact that the ceramics are still one of the most important, second-largest segments in the ZnO market. The wide scope of the application and constant demand for building results, along with the functional significance of ZnO as the quality enhancer of products, make ceramics always one of the most important ones in the ZnO market.

"In terms of value, Europe is projected to be the second-largest segment."

The second-largest market for zinc oxide is Europe because of its well-established industrial base, good automotive industry, and the dominance of high-value markets in pharmaceuticals and cosmetics. The automotive sector in the region is well established, and it contributes to the constant demand for ZnO in tire and rubber production. As more electrification trends emerge, demand for the material is expected to grow. There is also the developed construction industry in Europe, supported by renovation, sustainability projects, and infrastructure improvements, which drive consumption of ZnO in construction paints, coatings, and ceramics. One of the major distinctions that Europe has is that quality, regulated, and specialty applications, especially in pharmaceuticals, personal care, and specialty chemicals, where the demand for high-purity and USP-grade ZnO is high. In conclusion, it is evident that Europe is well-positioned because of its technological power, high-value applications, and industries driven by innovation, thus it continues to be a major and steady ZnO market in the world.

By Company Type: Tier 1: 25%, Tier 2: 42%, and Tier 3: 33%

By Designation: C-level Executives: 20%, Directors: 30%, and Other Designations: 50%

By Region: North America: 20%, Europe: 10%, Asia Pacific: 40%, South America: 10%, and Middle East & Africa: 20%

Notes: Other designations include sales, marketing, and product managers.

Tier 1: >USD 1 Billion; Tier 2: USD 500 million-1 Billion; and Tier 3: <USD 500 million

Companies Covered: EverZinc (US), Zochem LLC (US), Grupa Boryszew (Poland), Lanxess (Germany), JG Chemicals Limited (India), Akrochem Corporation (US), Pan-Continental Chemical Co., Ltd. (Taiwan), RUBAMIN (India), GRILLO-Werke AG (Germany), Zhiyi Zinc Industry Group (China), and Grupo PROMAX (Mexico), among others, are covered in the report.

The study includes an in-depth competitive analysis of these key players in the zinc oxide market, with their company profiles, recent developments, and key market strategies.

Research Coverage

This research report categorizes the zinc oxide market based on process (indirect, direct, wet-chemical), grade (standard, treated, USP, FCC, others), application (rubber, ceramics, chemicals, agriculture, cosmetics & personal care, pharmaceuticals, others) and region (Asia Pacific, North America, Europe, South America, and Middle East & Africa). The report's scope covers detailed information regarding the drivers, restraints, challenges, and opportunities influencing the growth of the zinc oxide market. A detailed analysis of the key industry players has been done to provide insights into their business overview, products offered, and key strategies, such as partnerships, collaborations, product launches, expansions, and acquisitions, associated with the zinc oxide market. This report covers a competitive analysis of upcoming startups in the zinc oxide market ecosystem.

Reasons to Buy the Report

The report will offer the market leaders/new entrants with information on the closest approximations of the revenue numbers for the overall zinc oxide market and the subsegments. This report will help stakeholders understand the competitive landscape, gain more insights into positioning their businesses better, and plan suitable go-to-market strategies. The report will help stakeholders understand the pulse of the market and provide them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following points:

Analysis of key drivers (growth in automotive production and demand for tires, increasing demand from cosmetics and personal care products), restraints (raw material price volatility, strict environmental regulatory frameworks), opportunities (rapid industrialization and infrastructure development, nanotechnology adoption), and challenges (supply chain dependency on zinc mining and refining, health concerns related to zinc oxide fumes and heavy metal exposure).

- Product Development/Innovation: Detailed insights into upcoming technologies, research & development activities, and product & service launches in the zinc oxide market.

- Market Development: Comprehensive information about profitable markets - the report analyzes the zinc oxide market across varied regions.

Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the zinc oxide market.

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players such as EverZinc (US), Zochem LLC (US), Grupa Boryszew (Poland), Lanxess (Germany), JG Chemicals Limited (India), Akrochem Corporation (US), Pan-Continental Chemical Co., Ltd. (Taiwan), RUBAMIN (India), GRILLO-Werke AG (Germany), Zhiyi Zinc Industry Group (China), and Grupo PROMAX (Mexico).

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.3.5 UNITS CONSIDERED

- 1.4 STAKEHOLDERS

- 1.5 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: SHARE INSIGHTS AND STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING THE MARKET

- 2.4 HIGH-GROWTH SEGMENTS & EMERGING FRONTIERS

- 2.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN ZINC OXIDE MARKET

- 3.2 ASIA PACIFIC: ZINC OXIDE MARKET, BY GRADE AND COUNTRY

- 3.3 ZINC OXIDE MARKET, BY PROCESS

- 3.4 ZINC OXIDE MARKET, BY GRADE

- 3.5 ZINC OXIDE MARKET, BY APPLICATION

- 3.6 ZINC OXIDE MARKET, BY COUNTRY

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Growth in automotive production and demand for tires

- 4.2.1.2 Increasing demand from cosmetics and personal care products

- 4.2.2 RESTRAINTS

- 4.2.2.1 Raw material price volatility

- 4.2.2.2 Stringent environmental regulatory frameworks

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Rapid industrialization and infrastructure development

- 4.2.3.2 Nanotechnology adoption

- 4.2.4 CHALLENGES

- 4.2.4.1 Supply chain dependency on zinc mining and refining

- 4.2.4.2 Health concerns related to zinc oxide fumes and heavy metal exposure

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 UNMET NEEDS IN ZINC OXIDE MARKET

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

- 4.5.1 TIER 1 PLAYERS: GLOBAL LEADERS DRIVING CONSOLIDATION AND INNOVATION

- 4.5.2 TIER 2 PLAYERS: REGIONAL INNOVATORS AND NICHE LEADERS

- 4.5.3 TIER 3 PLAYERS: STRENGTHENS ECO-EFFICIENCY WITH ZERO WASTE MILESTONE

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF SUPPLIERS

- 5.1.4 BARGAINING POWER OF BUYERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC ANALYSIS

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECASTS

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.5.1 AVERAGE SELLING PRICE TREND OF KEY PLAYERS, BY GRADE

- 5.5.2 AVERAGE SELLING PRICE, BY REGION

- 5.6 TRADE ANALYSIS

- 5.6.1 EXPORT SCENARIO (HS CODE 2817)

- 5.6.2 IMPORT SCENARIO (HS CODE 2817)

- 5.7 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.9 INVESTMENT AND FUNDING SCENARIO

- 5.10 CASE STUDY ANALYSIS

- 5.10.1 RUBAMIN - ZYNK (WORKER SAFETY INNOVATION)

- 5.10.2 GRILLO-WERKE AG - ECO ZINC (LOW-CARBON ZINC SOLUTION)

- 5.10.3 RUBAMIN - ZYNK FOR DESULFURIZATION CATALYSTS

- 5.11 IMPACT OF 2025 US TARIFF: ZINC OXIDE MARKET

- 5.11.1 INTRODUCTION

- 5.11.2 KEY TARIFF RATES

- 5.11.3 PRICE IMPACT ANALYSIS

- 5.11.4 IMPACT ON COUNTRIES/REGIONS

- 5.11.4.1 US

- 5.11.4.2 Europe

- 5.11.4.3 Asia Pacific

- 5.11.5 IMPACT ON END-USE INDUSTRIES

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 KEY TECHNOLOGIES

- 6.1.1 INDIRECT PROCESS (FRENCH PROCESS)

- 6.1.2 DIRECT PROCESS (AMERICAN PROCESS)

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 ANALYTICAL TECHNOLOGIES

- 6.2.1.1 Microprilling and palletization of zinc oxide

- 6.2.1 ANALYTICAL TECHNOLOGIES

- 6.3 ADJACENT TECHNOLOGIES

- 6.3.1 NANO ZINC OXIDE MANUFACTURING

- 6.3.2 ADVANCED MUFFLE FURNACE TECHNOLOGY

- 6.4 TECHNOLOGY ROADMAP

- 6.4.1 SHORT-TERM (2026-2028) | EFFICIENCY, COST OPTIMIZATION & INCREMENTAL PERFORMANCE GAINS

- 6.4.2 MID-TERM (2028-2030) | PRODUCT DIFFERENTIATION & SUSTAINABILITY INTEGRATION

- 6.4.3 LONG-TERM (2030-2035+) | DECARBONIZATION, ADVANCED APPLICATIONS & CIRCULAR ECOSYSTEMS

- 6.5 PATENT ANALYSIS

- 6.5.1 INTRODUCTION

- 6.5.2 METHODOLOGY

- 6.5.3 ZINC OXIDE MARKET, PATENT ANALYSIS, 2016-2025

- 6.6 FUTURE APPLICATIONS

- 6.6.1 ZINC OXIDE-DRIVEN NEXT-GENERATION ENERGY STORAGE SYSTEMS

- 6.6.2 BIO-INTERACTIVE ZINC OXIDE NANOMATERIALS FOR ADVANCED MEDICAL THERAPIES

- 6.6.3 SELF-HEALING ZINC OXIDE COATINGS FOR SMART INFRASTRUCTURE

- 6.7 IMPACT OF AI/GEN AI ON ZINC OXIDE MARKET

- 6.7.1 TOP USE CASES AND MARKET POTENTIAL

- 6.7.2 BEST PRACTICES IN ZINC OXIDE PROCESSING

- 6.7.3 CASE STUDIES OF AI IMPLEMENTATION IN ZINC OXIDE MARKET

- 6.7.4 INTERCONNECTED ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.7.5 CLIENTS' READINESS TO ADOPT GENERATIVE AI IN ZINC OXIDE MARKET

7 SUSTAINABILITY AND REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

- 7.2 SUSTAINABILITY INITIATIVES

- 7.2.1 UL 2809

- 7.2.1.1 Low carbon emissions in production

- 7.2.1.2 EcoVadis certification

- 7.2.1 UL 2809

- 7.3 IMPACT OF REGULATORY POLICY ON SUSTAINABILITY INITIATIVES

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOUR

- 8.1 DECISION-MAKING PROCESS

- 8.2 BUYER STAKEHOLDERS AND BUYING EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.4 UNMET NEEDS FROM VARIOUS APPLICATIONS

- 8.5 MARKET PROFITABILITY

- 8.5.1 REVENUE POTENTIAL

- 8.5.2 COST DYNAMICS

- 8.5.3 MARGIN OPPORTUNITIES, BY APPLICATION

9 ZINC OXIDE MARKET, BY PROCESS

- 9.1 INTRODUCTION

- 9.2 INDIRECT PROCESS (FRENCH PROCESS)

- 9.2.1 DEMAND FOR HIGH-PURITY ZINC OXIDE TO DRIVE MARKET GROWTH

- 9.3 DIRECT PROCESS (AMERICAN PROCESS)

- 9.3.1 COST-EFFECTIVE METHOD FOR APPLICATIONS REQUIRING LOWER PURITY ZINC OXIDE

- 9.4 WET-CHEMICAL PROCESS

- 9.4.1 CONTROL OVER PARTICLE DESIGN AND LOW IMPURITY LEVELS TO DRIVE MARKET GROWTH

10 ZINC OXIDE MARKET, BY GRADE

- 10.1 INTRODUCTION

- 10.2 STANDARD GRADE

- 10.2.1 WIDE ADOPTION IN INDUSTRIAL APPLICATIONS TO DRIVE MARKET GROWTH

- 10.3 TREATED GRADE

- 10.3.1 OPTIMUM DISPERSION EFFICIENCY TO DRIVE ADOPTION IN INDUSTRIAL AND COSMETIC APPLICATIONS

- 10.4 UNITED STATES PHARMACOPEIA (USP) GRADE

- 10.4.1 STRINGENT PHARMACEUTICAL STANDARDS TO DRIVE MARKET

- 10.5 FOOD CHEMICALS CODEX (FCC) GRADE

- 10.5.1 INCREASING FOCUS ON MICRONUTRIENT DEFICIENCY TO DRIVE MARKET GROWTH

- 10.6 OTHER GRADES

11 ZINC OXIDE MARKET, BY APPLICATION

- 11.1 INTRODUCTION

- 11.2 RUBBER

- 11.2.1 EXPANSION OF AUTOMOBILE INDUSTRY TO DRIVE GROWTH

- 11.3 CERAMICS

- 11.3.1 EXPANDING CONSTRUCTION INDUSTRY TO DRIVE DEMAND

- 11.4 CHEMICALS

- 11.4.1 ADOPTION OF ZINC OXIDE AS CHEMICAL INTERMEDIATES AND CATALYSTS TO DRIVE GROWTH

- 11.5 AGRICULTURE

- 11.5.1 INCREASING ADOPTION OF SUSTAINABLE ZINC FERTILIZER SOLUTIONS TO FUEL DEMAND

- 11.6 COSMETICS & PERSONAL CARE

- 11.6.1 COMPATIBILITY ADVANTAGES OF ZINC OXIDE OVER TITANIUM DIOXIDE TO SUPPORT MARKET GROWTH

- 11.7 PHARMACEUTICALS

- 11.7.1 INCREASING DEMAND FOR PHARMACEUTICALS TO DRIVE GROWTH

- 11.8 OTHER APPLICATIONS

12 ZINC OXIDE MARKET, BY REGION

- 12.1 INTRODUCTION

- 12.2 ASIA PACIFIC

- 12.2.1 CHINA

- 12.2.1.1 Growth of multiple end-use sectors to drive market growth

- 12.2.2 INDIA

- 12.2.2.1 Automotive production growth, government infrastructure support, and growing agricultural output to propel market

- 12.2.3 JAPAN

- 12.2.3.1 Presence of strong electronics manufacturing sector to support market growth

- 12.2.4 REST OF ASIA PACIFIC

- 12.2.1 CHINA

- 12.3 NORTH AMERICA

- 12.3.1 US

- 12.3.1.1 Expanding automotive industry and tire manufacturing to drive growth

- 12.3.2 CANADA

- 12.3.2.1 LNG production growth plans and new automotive industry strategy to boost market growth

- 12.3.3 MEXICO

- 12.3.3.1 Strong automotive manufacturing, rising construction investments, and expansion of pharmaceutical industry to drive market

- 12.3.1 US

- 12.4 EUROPE

- 12.4.1 GERMANY

- 12.4.1.1 Automotive, cosmetics, and pharmaceutical industries to drive market growth

- 12.4.2 UK

- 12.4.2.1 Rising construction plans to support market growth

- 12.4.3 FRANCE

- 12.4.3.1 Growing EV adoption and construction activities to fuel demand

- 12.4.4 ITALY

- 12.4.4.1 Rising agricultural exports to drive market growth

- 12.4.5 SPAIN

- 12.4.5.1 Rising automobile sales and growth of agriculture sector to increase demand

- 12.4.6 RUSSIA

- 12.4.6.1 Fossil fuel and agricultural exports to support market growth

- 12.4.7 REST OF EUROPE

- 12.4.1 GERMANY

- 12.5 MIDDLE EAST & AFRICA

- 12.5.1 GCC COUNTRIES

- 12.5.1.1 Saudi Arabia

- 12.5.1.1.1 Vision 2030 and PIF projects to support market growth

- 12.5.1.2 UAE

- 12.5.1.2.1 Expanding automotive manufacturing and infrastructure investments to drive market growth

- 12.5.1.3 Rest of GCC Countries

- 12.5.1.1 Saudi Arabia

- 12.5.2 SOUTH AFRICA

- 12.5.2.1 Growing construction activities and automotive exports to drive growth

- 12.5.3 REST OF MIDDLE EAST & AFRICA

- 12.5.1 GCC COUNTRIES

- 12.6 SOUTH AMERICA

- 12.6.1 BRAZIL

- 12.6.1.1 Growing automotive exports and expanding agriculture sector to drive market growth

- 12.6.2 ARGENTINA

- 12.6.2.1 Expansion of automotive and industrial sectors to support market growth

- 12.6.3 REST OF SOUTH AMERICA

- 12.6.1 BRAZIL

13 COMPETITIVE LANDSCAPE

- 13.1 OVERVIEW

- 13.2 KEY PLAYERS' STRATEGIES/RIGHT TO WIN

- 13.3 MARKET SHARE ANALYSIS

- 13.4 REVENUE ANALYSIS

- 13.5 COMPANY VALUATION AND FINANCIAL METRICS

- 13.6 BRAND COMPARISON

- 13.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 13.7.1 STARS

- 13.7.2 EMERGING LEADERS

- 13.7.3 PERVASIVE PLAYERS

- 13.7.4 PARTICIPANTS

- 13.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 13.7.5.1 Company footprint

- 13.7.5.2 Region footprint

- 13.7.5.3 Application footprint

- 13.7.5.4 Process footprint

- 13.7.5.5 Grade footprint

- 13.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 13.8.1 PROGRESSIVE COMPANIES

- 13.8.2 RESPONSIVE COMPANIES

- 13.8.3 DYNAMIC COMPANIES

- 13.8.4 STARTING BLOCKS

- 13.8.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 13.8.5.1 Detailed list of key startups/SMEs

- 13.8.5.2 Competitive benchmarking of key startups/SMEs

- 13.9 COMPETITIVE SCENARIO

- 13.9.1 DEALS

- 13.9.2 EXPANSIONS

- 13.9.3 OTHERS

14 COMPANY PROFILES

- 14.1 KEY PLAYERS

- 14.1.1 EVERZINC

- 14.1.1.1 Business overview

- 14.1.1.2 Products/Solutions/Services offered

- 14.1.1.3 Recent developments

- 14.1.1.3.1 Deals

- 14.1.1.4 MnM view

- 14.1.1.4.1 Right to win

- 14.1.1.4.2 Strategic choices

- 14.1.1.4.3 Weaknesses and competitive threats

- 14.1.2 ZOCHEM LLC

- 14.1.2.1 Business overview

- 14.1.2.2 Products/Solutions/Services offered

- 14.1.2.3 Recent developments

- 14.1.2.3.1 Deals

- 14.1.2.3.2 Expansions

- 14.1.2.4 MnM view

- 14.1.2.4.1 Right to win

- 14.1.2.4.2 Strategic choices

- 14.1.2.4.3 Weaknesses and competitive threats

- 14.1.3 GRUPA BORYSZEW

- 14.1.3.1 Business overview

- 14.1.3.2 Products/Solutions/Services offered

- 14.1.3.3 MnM view

- 14.1.3.3.1 Right to win

- 14.1.3.3.2 Strategic choices

- 14.1.3.3.3 Weaknesses and competitive threats

- 14.1.4 LANXESS

- 14.1.4.1 Business overview

- 14.1.4.2 Products/Solutions/Services offered

- 14.1.4.3 MnM view

- 14.1.4.3.1 Right to win

- 14.1.4.3.2 Strategic choices

- 14.1.4.3.3 Weaknesses and competitive threats

- 14.1.5 JG CHEMICALS LIMITED

- 14.1.5.1 Business overview

- 14.1.5.2 Products/Solutions/Services offered

- 14.1.5.3 Recent developments

- 14.1.5.3.1 Expansions

- 14.1.5.3.2 Others

- 14.1.5.4 MnM view

- 14.1.5.4.1 Right to win

- 14.1.5.4.2 Strategic choices

- 14.1.5.4.3 Weaknesses and competitive threats

- 14.1.6 AKROCHEM CORPORATION

- 14.1.6.1 Business overview

- 14.1.6.2 Products/Solutions/Services offered

- 14.1.6.3 Recent Developments

- 14.1.6.3.1 Deals

- 14.1.6.4 MnM view

- 14.1.7 PAN-CONTINENTAL CHEMICAL CO., LTD.

- 14.1.7.1 Business overview

- 14.1.7.2 Products/Solutions/Services offered

- 14.1.7.3 MnM view

- 14.1.8 RUBAMIN

- 14.1.8.1 Business overview

- 14.1.8.2 Products/Solutions/Services offered

- 14.1.8.3 MnM view

- 14.1.9 GRILLO-WERKE AG

- 14.1.9.1 Business overview

- 14.1.9.2 Products/Solutions/Services offered

- 14.1.9.3 Recent developments

- 14.1.9.3.1 Deals

- 14.1.9.4 MnM view

- 14.1.10 ZHIYI ZINC INDUSTRY GROUP

- 14.1.10.1 Business overview

- 14.1.10.2 Products/Solutions/Services offered

- 14.1.10.3 Recent developments

- 14.1.10.3.1 Deals

- 14.1.10.3.2 Expansions

- 14.1.10.4 MnM view

- 14.1.11 GRUPO PROMAX

- 14.1.11.1 Business overview

- 14.1.11.2 Products/Solutions/Services offered

- 14.1.11.3 MnM view

- 14.1.1 EVERZINC

- 14.2 OTHER PLAYERS

- 14.2.1 BRUGGEMANN

- 14.2.2 SILOX GROUP

- 14.2.3 ARABIAN ZINC

- 14.2.4 ENTEKNO MATERIALS

- 14.2.5 NANOMOX

- 14.2.6 HAKUSUI TECH CO., LTD.

- 14.2.7 NAHAR ZINC OXIDE

- 14.2.8 GLOBAL CHEMICAL CO., LTD.

- 14.2.9 PT INDO LYSAGHT

- 14.2.10 SKYSPRING NANOMATERIALS, INC.

- 14.2.11 MICRONISERS PTY LTD.

- 14.2.12 ZINC-O-INDIA

- 14.2.13 GARG ZINC (INDIA) PVT. LTD.

- 14.2.14 ACE CHEMIE ZYNK ENERGY LIMITED

15 RESEARCH METHODOLOGY

- 15.1 RESEARCH DATA

- 15.1.1 SECONDARY DATA

- 15.1.1.1 Key data from secondary sources

- 15.1.2 PRIMARY DATA

- 15.1.2.1 Key data from primary sources

- 15.1.1 SECONDARY DATA

- 15.2 MARKET SIZE ESTIMATION

- 15.2.1 TOP-DOWN APPROACH & BOTTOM-UP APPROACH

- 15.3 BASE NUMBER CALCULATION

- 15.3.1 SUPPLY-SIDE APPROACH

- 15.4 MARKET FORECAST APPROACH

- 15.4.1 SUPPLY SIDE

- 15.4.2 DEMAND SIDE

- 15.5 DATA TRIANGULATION

- 15.6 RESEARCH ASSUMPTIONS

- 15.7 RISK ASSESSMENT

- 15.8 GROWTH RATE ASSUMPTIONS

16 APPENDIX

- 16.1 DISCUSSION GUIDE

- 16.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 16.3 CUSTOMIZATION OPTIONS

- 16.4 RELATED REPORTS

- 16.5 AUTHOR DETAILS