|

시장보고서

상품코드

2019240

자동차 전력 분배 모듈 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Automotive Power Distribution Modules Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

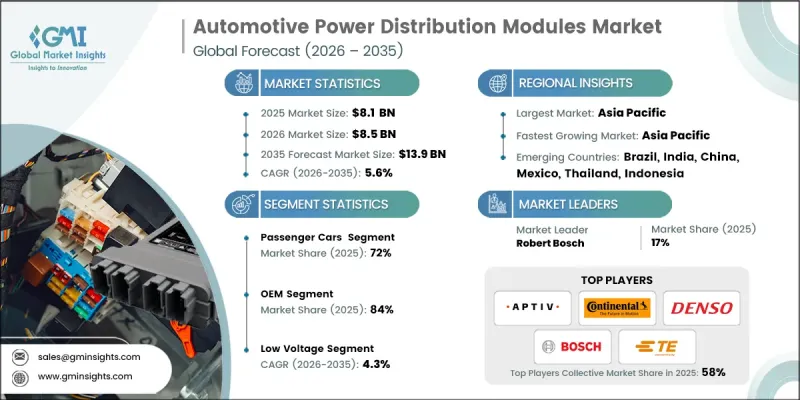

세계의 자동차 전력 분배 모듈 시장은 2025년에 81억 달러로 평가되었고, CAGR 5.6%로 성장하여 2035년까지 139억 달러에 이를 것으로 추정되고 있습니다.

자동차 전기 시스템의 복잡성 증가와 승용차와 상용차 모두에서 전기 파워트레인 채택이 증가하고 있다는 점이 이 시장의 성장을 견인하고 있습니다. PDM(전력 분배 모듈)은 배터리, 발전기 및 여러 전기 부품 간의 전력 흐름을 관리하여 부하가 변동하는 상황에서도 안정적이고 효율적인 작동을 보장하는 데 중요한 역할을 합니다. 기존 릴레이 및 퓨즈 박스에서 진단 기능, 통신 프로토콜, 열 관리 기능을 통합한 스마트하고 가벼운 모듈로 전환하면서 지능형 솔루션에 대한 수요가 증가하고 있습니다. 차량 안전, 배기가스, 전동화 관련 규제 기준과 더불어 커넥티드카 기술, ADAS, 인포테인먼트 시스템의 성장이 시장 확대를 가속화하고 있습니다. 특히 하이브리드 및 배터리 전기자동차의 생산량 증가와 애프터마켓에서의 교체 및 업그레이드가 자동차 PDM 부문의 지속적인 성장에 더욱 기여하고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 연도 시장 규모 | 81억 달러 |

| 예측액 | 139억 달러 |

| CAGR | 5.6% |

승용차 부문은 2025년 72%의 점유율을 차지할 것으로 예상되며, 2026년부터 2035년까지 연평균 복합 성장률(CAGR) 5.1%로 성장할 것으로 전망됩니다. 승용차가 주도적인 위치를 차지하고 있는 것은 전 세계 생산대수가 많을 뿐만 아니라 효율적인 전력관리가 필요한 하이브리드 및 전기자동차의 보급이 진행되고 있기 때문입니다. 현대의 승용차에는 첨단 전자장치, ADAS, 커넥티비티 시스템, 인포테인먼트 플랫폼을 지원하고 최적의 에너지 분배와 시스템 신뢰성 향상을 보장하는 지능형 PDM이 요구됩니다. 기술적으로 정교한 차량에 대한 소비자의 선호도가 높아지면서 이 부문에서 첨단 전력 분배 모듈의 채택이 계속 증가하고 있습니다.

OEM 채널은 2025년 84%의 점유율을 차지할 것으로 예상되며, 2026년부터 2035년까지 연평균 복합 성장률(CAGR) 5.8%를 나타낼 것으로 예측됩니다. 자동차 제조업체는 특정 전기 아키텍처, 성능 기준, 안전 요구 사항에 맞게 맞춤화된 OEM 공급 모듈에 의존하고 있습니다. 이 모듈은 생산 단계에서 승용차, 상용차, 전기자동차에 탑재됩니다. OEM 채널에서는 장기 계약, IATF 16949 인증 준수 및 엄격한 품질 검증을 통해 자동차용 일렉트로닉스의 신뢰성과 안전성을 보장하는 데 중점을 두고 있습니다. 하이브리드 및 배터리 전기자동차의 보급이 증가함에 따라 복잡한 전기 시스템 및 고전압 시스템을 지원하기 위한 고급 PDM 솔루션에 대한 OEM 수요가 더욱 증가하고 있습니다.

중국의 자동차 배전 모듈 시장은 2026년부터 2035년까지 연평균 복합 성장률(CAGR) 5.1%를 나타낼 것으로 예측됩니다. 중국의 방대한 자동차 생산 기지와 탄탄한 전자 부품 공급망은 첨단 배전 시스템에 대한 견고한 수요를 촉진하고 있습니다. 중국에서는 승용차, 상용차, 전기차를 포함하여 연간 3,000만 대 이상의 차량이 생산되고 있으며, 전자 시스템, 디지털 콕핏, ADAS, 커넥티드카 기술을 지원하는 지능형 PDM에 대한 큰 수요가 발생하고 있습니다. 이러한 우위를 바탕으로 중국은 아시아태평양의 자동차 PDM 분야에서 혁신과 보급의 주요 원동력으로 자리매김하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 컴포넌트별, 2022-2035

제6장 시장 추산 및 예측 : 모듈별, 2022-2035

제7장 시장 추산 및 예측 : 차량별, 2022-2035

제8장 시장 추산 및 예측 : 판매채널별, 2022-2035

제9장 시장 추산 및 예측 : 용도별, 2022-2035

제10장 시장 추산 및 예측 : 지역별, 2022-2035

제11장 기업 개요

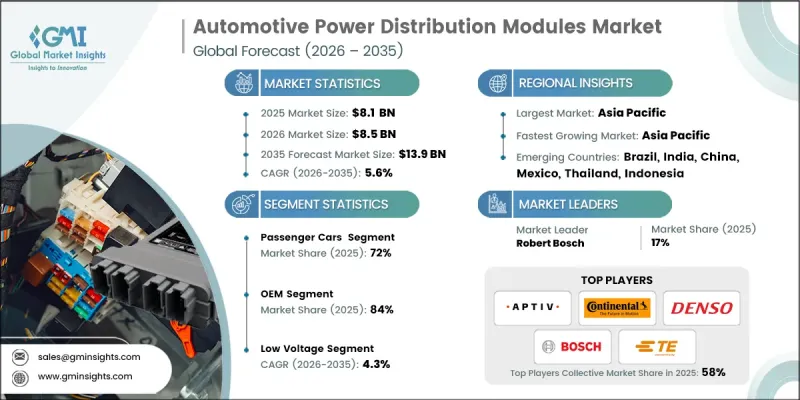

LSH 26.05.08The Global Automotive Power Distribution Modules Market was valued at USD 8.1 billion in 2025 and is estimated to grow at a CAGR of 5.6% to reach USD 13.9 billion by 2035.

The market is fueled by the increasing complexity of vehicle electrical systems and the rising adoption of electrified powertrains in both passenger and commercial vehicles. PDMs play a critical role in managing power flow between the battery, alternator, and multiple electrical components, ensuring stable and efficient operation under varying loads. The transition from conventional relay-fused boxes to smart, lightweight modules with integrated diagnostics, communication protocols, and thermal management is driving the demand for intelligent solutions. Regulatory standards for vehicle safety, emissions, and electrification, coupled with growth in connected car technologies, ADAS, and infotainment systems, are accelerating market expansion. The rise in vehicle production, particularly for hybrid and battery electric vehicles, along with aftermarket replacements and upgrades, further contributes to the sustained growth of the automotive PDM sector.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $8.1 Billion |

| Forecast Value | $13.9 Billion |

| CAGR | 5.6% |

The passenger car segment accounted for 72% share in 2025 and is expected to grow at a CAGR of 5.1% from 2026 to 2035. Passenger cars dominate due to high global production volumes and increasing integration of hybrid and electric vehicles, which require efficient power management. Modern passenger vehicles demand intelligent PDMs to support advanced electronics, ADAS, connectivity systems, and infotainment platforms, ensuring optimized energy distribution and enhanced system reliability. The growing consumer preference for technologically sophisticated vehicles continues to drive the adoption of advanced power distribution modules in this segment.

The OEM channel held an 84% share in 2025, with an expected CAGR of 5.8% during 2026-2035. Automotive manufacturers rely on OEM-supplied modules tailored to specific electrical architectures, performance standards, and safety requirements. These modules are integrated into passenger vehicles, commercial vehicles, and electric vehicles at the production stage. The OEM channel emphasizes long-term contracts, compliance with IATF 16949 certification, and strict quality validation, which ensures the reliability and safety of automotive electronics. Rising hybrid and battery electric vehicle adoption is further reinforcing OEM demand for advanced PDM solutions to support complex electrical and high-voltage systems.

China Automotive Power Distribution Modules Market will grow at a CAGR of 5.1% from 2026 to 2035. The country's vast automotive manufacturing base, combined with a strong electronics supply chain, fuels robust demand for sophisticated power distribution systems. China produces over 30 million vehicles annually, including passenger, commercial, and electric vehicles, creating a significant requirement for intelligent PDMs that support electronic systems, digital cockpits, ADAS, and connected vehicle technologies. This dominance positions China as a key driver for innovation and adoption in the Asia Pacific automotive PDM sector.

Key players operating in the Global Automotive Power Distribution Modules Market include Aptiv, Robert Bosch, Continental, Denso, TE Connectivity, Lear, Eaton, Hitachi Astemo, Yazaki, and Valeo. Companies in the Automotive Power Distribution Modules Market are focusing on technological innovation to strengthen their market position by developing smart, compact, and lightweight modules that support electrified vehicles and high-voltage architectures. They are forming strategic partnerships with OEMs and Tier 1 suppliers to secure long-term contracts and expand their global footprint. Investment in R&D for integrated diagnostics, advanced thermal management, and reliable communication protocols is a key strategy to differentiate products. Companies are also enhancing aftermarket support, offering modular and customizable solutions to meet diverse vehicle architectures. Expansion into emerging markets, especially in Asia Pacific, and collaboration with EV manufacturers are being leveraged to increase market share, improve brand visibility, and capture the growing demand for intelligent power distribution solutions.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.3 Research trail and confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Best estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.8 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Module

- 2.2.4 Vehicle

- 2.2.5 Sales Channel

- 2.2.6 Application

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rapid electrification of vehicle fleets and transition to EVs/HEVs

- 3.2.1.2 Increasing electronic content in modern vehicles (ADAS, infotainment, connectivity)

- 3.2.1.3 Adoption of zone architecture and smart power distribution solutions

- 3.2.1.4 Stringent emission regulations driving high-voltage system integration

- 3.2.1.5 Consumer demand for advanced safety and comfort features

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of advanced power distribution modules

- 3.2.2.2 Complexity in design & integration of multi-voltage systems

- 3.2.2.3 Semiconductor supply chain disruptions & component shortages

- 3.2.2.4 Thermal management challenges in compact vehicle spaces

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of 48V mild hybrid systems in passenger vehicles

- 3.2.3.2 Retrofitting aftermarket smart PDM solutions

- 3.2.3.3 Emerging markets automotive production growth

- 3.2.3.4 Integration with vehicle-to-grid (V2G) infrastructure

- 3.2.3.5 Development of modular & scalable PDM platforms

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 US- EPA GHG phase 3 & CAFE standards

- 3.4.1.2 Canada - Emissions-based regulatory framework

- 3.4.2 Europe

- 3.4.2.1 Germany- Euro 7 Emission Standards

- 3.4.2.2 UK- Post-brexit vehicle type approval

- 3.4.2.3 France- Decarbonization roadmap

- 3.4.2.4 Italy- Low-Emission zone compliance

- 3.4.3 Asia Pacific

- 3.4.3.1 China- China VI-b & Emerging China VII standards

- 3.4.3.2 India- BS-VI Stage II & bharat stage VII transition

- 3.4.3.3 Japan- Fuel efficiency standards (2030 Targets)

- 3.4.3.4 Australia- Fuel quality & ADR 79/05 standards

- 3.4.4 LATAM

- 3.4.4.1 Mexico- NOM-194-SE-2021 & USMCA rules of origin

- 3.4.4.2 Argentina- Law 24.449 & environmental amendments

- 3.4.5 MEA

- 3.4.5.1 South Africa- National road traffic act (1996)

- 3.4.5.2 Saudi Arabia- Traffic law & vision 2030 transport initiatives

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Patent landscape (driven by primary research)

- 3.9 Pricing analysis (Driven by Primary Research)

- 3.9.1 Historical price trend analysis

- 3.9.2 Pricing strategy by player type (premium / value / cost-plus)

- 3.9.3 Total cost of ownership (TCO) analysis

- 3.10 Trade data analysis (driven by paid database)

- 3.10.1 Import/export volume & value trends

- 3.10.2 Key trade corridors & tariff impact

- 3.11 Use cases & success stories

- 3.12 Impact of AI & generative AI on the market

- 3.12.1 AI-driven disruption of existing business models

- 3.12.2 GenAI use cases & adoption roadmap by segment

- 3.12.3 Risks, limitations & regulatory considerations

- 3.13 Capacity & production landscape (driven by primary research)

- 3.13.1 Installed capacity by region & key producer

- 3.13.2 Capacity utilization rates & expansion pipelines

- 3.14 Sustainability and environmental aspects

- 3.14.1 Sustainable practices

- 3.14.2 Waste reduction strategies

- 3.14.3 Energy efficiency in production

- 3.14.4 Eco-friendly Initiatives

- 3.14.5 Carbon footprint considerations

- 3.15 Forecast assumptions & scenario analysis (Driven by primary research)

- 3.15.1 Base Case - key macro & industry variables driving CAGR

- 3.15.2 Optimistic Scenarios - Favorable macro and industry tailwinds

- 3.15.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Company Tier Benchmarking

- 4.5.1 Tier Classification Criteria & Qualifying Thresholds

- 4.5.2 Tier Positioning Matrix by Revenue, Geography & Innovation

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2022 - 2035 ($Bn, Units)

- 5.1 Key trends

- 5.2 Power modules

- 5.3 Fuses and circuit breakers

- 5.4 Connectors and terminals

- 5.5 Relays

- 5.6 Voltage regulators

- 5.7 Others

Chapter 6 Market Estimates & Forecast, By Module, 2022 - 2035 ($Bn, Units)

- 6.1 Key trends

- 6.2 Low voltage

- 6.3 Medium voltage

- 6.4 High voltage

Chapter 7 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Bn, Units)

- 7.1 Key trends

- 7.2 Passenger cars

- 7.2.1 Hatchback

- 7.2.2 Sedan

- 7.2.3 SUV

- 7.3 Commercial vehicles

- 7.3.1 Light commercial vehicles (LCVs)

- 7.3.2 Medium commercial vehicles (MCVs)

- 7.3.3 Heavy commercial vehicles (HCVs)

Chapter 8 Market Estimates & Forecast, By Sales Channel, 2022 - 2035 ($Bn, Units)

- 8.1 Key trends

- 8.2 OEM

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By Application, 2022 - 2035 ($Bn, Units)

- 9.1 Key trends

- 9.2 Lighting systems

- 9.3 Infotainment systems

- 9.4 HVAC systems

- 9.5 Safety and driver assistance systems

- 9.6 Powertrain systems

- 9.7 Battery management systems

- 9.8 Others

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Netherlands

- 10.3.8 Sweden

- 10.3.9 Denmark

- 10.3.10 Poland

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Singapore

- 10.4.7 Thailand

- 10.4.8 Indonesia

- 10.4.9 Vietnam

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Colombia

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

- 10.6.4 Israel

Chapter 11 Company Profiles

- 11.1 Global Players

- 11.1.1 Aptiv

- 11.1.2 Continental

- 11.1.3 Denso

- 11.1.4 Eaton

- 11.1.5 Hitachi Astemo

- 11.1.6 Lear

- 11.1.7 Mitsubishi Electric

- 11.1.8 Robert Bosch

- 11.1.9 TE Connectivity

- 11.1.10 Valeo

- 11.2 Regional Players

- 11.2.1 DRAXLMAIER

- 11.2.2 Furukawa Electric

- 11.2.3 Leoni

- 11.2.4 Panasonic Automotive Systems

- 11.2.5 Sumitomo Electric Industries

- 11.2.6 Yazaki

- 11.3 Emerging Players

- 11.3.1 Infineon Technologies

- 11.3.2 NXP Semiconductors

- 11.3.3 onsemi (ON Semiconductor)

- 11.3.4 STMicroelectronics