|

시장보고서

상품코드

1871239

자동차 스탬핑 프레스 자동화 시장 : 기회, 성장 요인, 업계 동향 분석, 예측(2025-2034년)Automotive Stamping Press Automation Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

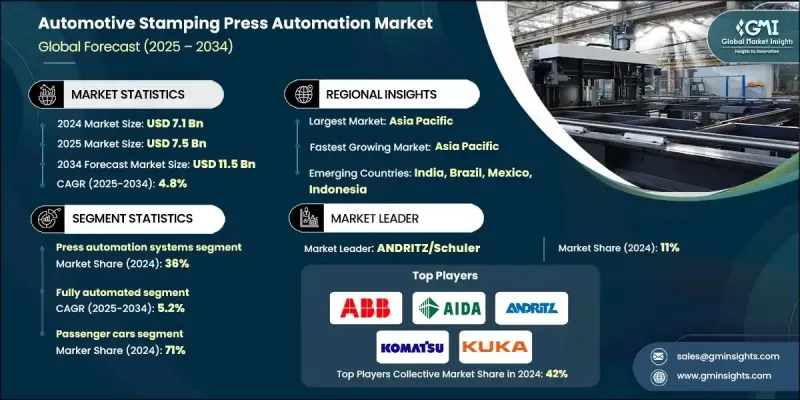

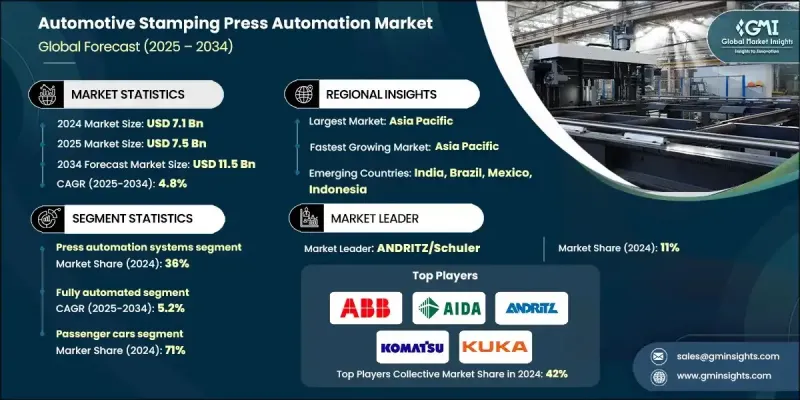

세계 자동차 스탬핑 프레스 자동화 시장은 2024년에 71억 달러로 평가되었으며, 2034년까지 연평균 복합 성장률(CAGR) 4.8%로 성장하고 115억 달러에 이를 것으로 예측됩니다.

본 시장은 금속 자동차 부품의 자동 성형, 성형 및 조립에 초점을 맞추고 있기 때문에 자동차 제조에 있어서 매우 중요한 역할을 담당하고 있습니다. 로봇공학, CNC기계, 자동제어시스템의 활용 확대에 의해 자동차 제조 공정 전체의 생산 정밀도, 속도, 재현성이 향상하고 있습니다. 전기자동차(EV) 부문의 급속한 확대도 프레스 가공의 자동화를 재구성하고 있습니다. EV 생산에는 가볍고 복잡한 구조 부품이 필요하기 때문입니다. 제조업체는 고장력강, 알루미늄 및 복합재료 가공을 지원하기 위해 첨단 자동화 기술에 대한 투자를 증가시키고 있습니다. IoT, 스마트 센서, 예지 보전을 포함한 Industry 4.0 기술의 통합은 이 분야를 더욱 변화시켰습니다. 이러한 혁신 기술은 실시간 모니터링, 자동 품질 검사 및 예측 유지 보수를 가능하게 함으로써 생산 효율을 최적화합니다. 이 통합은 가동 중지 시간을 줄이고 에너지 효율을 높이고 자동차 부품 생산에서 높은 처리량과 정확성을 보장합니다. 세계 경쟁력을 유지하기 위해 자동화가 점점 더 중요해지고 있는 가운데, 승용차, 상용차, 전기차의 제조 분야에서 첨단 프레스 시스템 수요는 계속 증가하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 기간 | 2025-2034년 |

| 시작 금액 | 71억 달러 |

| 예측 금액 | 115억 달러 |

| CAGR | 4.8% |

프레스 자동화 시스템 부문은 2024년에 36%의 점유율을 차지했습니다. 이 부문은 주로 기존의 유압 프레스와 비교하여 우수한 정밀도, 유연성 및 에너지 효율을 제공하는 서보 구동 프레스 기술의 채택에 의해 견인됩니다. 서보 프레스는 작업자가 실시간으로 성형 파라미터를 미세 조정하고 재료 낭비를 줄이고 알루미늄 합금 및 고장력 강철과 같은 다양한 재료를 효율적으로 가공할 수 있도록 합니다. 전기자동차 부품의 제조에 있어서의 사용 증가는 정밀 제조 환경에서의 그 가치를 뒷받침하고 있습니다.

완전 자동화 부문은 2025년부터 2034년까지 연평균 복합 성장률(CAGR)은 5.2%를 보일 것으로 예측됩니다. 이 카테고리는 고속 프레스, 로봇 핸들링 시스템, 지능형 프로세스 제어 솔루션을 통합하여 연속적이고 중단없는 생산을 실현합니다. 이러한 시스템은 수작업 개입을 최소화하여 처리량, 제품 균일성 및 작업 안전성을 향상시키는 동시에 사이클 시간과 생산 비용을 절감합니다. 완전 자동화 프레스 라인은 현재 대규모 자동차 생산 시설 전체에서 린 생산 방식의 목표를 달성하고 균일한 품질 기준을 유지하는 데 필수적인 존재가 되고 있습니다.

미국의 자동차 스탬핑 프레스 자동화 시장은 2024년 10억 9,000만 달러 규모에 이르렀습니다. 미국 시장의 성장은 국내 제조에 대한 재주목과 첨단 자동화 기술의 채택에 의해 견인되고 있습니다. 자동차 제조업체는 차세대 프레스 시스템에 대한 투자를 확대하여 승용차와 상용차 모두에서 유연성, 생산성 및 품질을 향상시킵니다. 제조업무의 국내 회귀와 공급 체인의 탄력성에 대한 주력은 이 지역에서 자동화 솔루션 수요를 더욱 강화하고 있습니다.

세계 자동차 스탬핑 프레스 자동화 시장의 주요 기업으로는 ABB, 코마츠 공업, KUKA, 파낙, 아이다 엔지니어링, 아마다, 세이 기계, 맥주 오브 아메리카, 안드리츠/슈러, 유니버설 로봇 등이 있습니다. 자동차 스탬핑 프레스 자동화 업계의 주요 기업은 기술 혁신, 파트너십, 생산 능력 확대를 중심으로 한 전략을 채택하여 자사의 지위 강화를 도모하고 있습니다. 각 회사는 예측 보전, 에너지 제어 개선, 공정 최적화 강화를 목적으로 AI와 IoT를 통합한 지능형 서보 구동 시스템을 개발하고 있습니다. 자동차 제조업체와 로봇 기업과의 전략적 제휴는 생산 시설 전체에서 자동화 솔루션의 확대에 기여하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

- 시장 범위와 정의

- 조사 설계

- 조사 접근

- 데이터 수집 방법

- 데이터 마이닝의 출처

- 세계

- 지역별/국가별

- 기본 추정치와 계산

- 기준연도 계산

- 시장 추정에서의 주요 동향

- 1차 조사 및 검증

- 1차 정보

- 예측

- 조사의 전제조건과 제한 사항

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률 분석

- 비용 구조

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 전기자동차(EV) 및 경량 소재의 보급 확대

- 인더스트리 4.0 및 스마트 팩토리 기술의 통합

- 신흥 시장에서의 자동차 생산 증가

- 고품질의 균일한 금속 부품에 대한 수요

- 업계의 잠재적 위험 및 과제

- 고도의 자동화를 위한 고자본 투자

- 복합재료 프레스 가공 공정의 통합에 있어서의 복잡성

- 시장 기회

- 전기자동차(EV) 및 경량 차량 프로그램 확대

- AI 구동형 예지 보전 및 프로세스 최적화 채택

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 기술과 혁신의 상황

- 현재의 기술 동향

- 신규기술

- 가격 동향

- 지역별

- 제품별

- 코스트 내역 분석

- 특허 분석

- 지속가능성과 환경면

- 탄소발자국 평가

- 순환형 경제에의 통합

- 전자폐기물 관리 요건

- 친환경 이니셔티브

- 이용 사례와 응용 분야

- 최상의 시나리오

- 투자 상황

- 프레스 가공 자동화에 있어서의 설비 투자 동향

- 사모펀드 및 벤처 투자 활동

- 합병, 인수 및 전략적 제휴

- 투자이익률(ROI)과 회수기간 분석

- 시장 도입 동향

- 차종별 자동화 도입률

- 자동화 레벨별 도입 상황 : 반자동화 vs 완전 자동화

- IoT 및 AI 기술의 통합

- 도입 장벽과 촉진요인

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

- 주요 발전

- 합병 및 인수

- 제휴 및 협업

- 신제품 발매

- 사업 확대 계획과 자금 조달

제5장 시장 추정 및 예측 : 제품별, 2021년-2034년

- 주요 동향

- 프레스 자동화 시스템

- 로봇에 의한 자재 운반

- 프로세스 제어·감시

- 통합 및 서비스

제6장 시장 추정 및 예측 : 자동화 레벨별, 2021년-2034년

- 주요 동향

- 반자동화

- 완전 자동화

- 스마트/커넥티드

제7장 시장 추정 및 예측 : 차량별, 2021년-2034년

- 주요 동향

- 승용차

- 해치백

- 세단

- SUV

- 상용차

- 소형 상용차(LCV)

- 중형 상용차(MCV)

- 대형 상용차(HCV)

제8장 시장 추정 및 예측 : 용도별, 2021년-2034년

- 주요 동향

- 바디 인 화이트(BIW)

- 파워트레인

- 안전 및 구조

- 기타

제9장 시장 추정 및 예측 : 지역별, 2021년-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 북유럽 국가

- 러시아

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 동남아시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제10장 기업 프로파일

- 세계 기업

- ABB

- AIDA Engineering

- AMADA

- ANDRITZ/Schuler

- Bihler of America

- FANUC

- Komatsu Industries

- KUKA

- SEYI Machinery

- Universal Robots

- 지역 기업

- Acro Metal Stamping

- American Axle &Manufacturing

- ArtiFlex Manufacturing

- Challenge Manufacturing

- 신규기업/디스럽터

- AmeriStar

- Arcade Metal Stamping

- Automation Tool &Die(ATD)

- Eagle Press &Equipment

The Global Automotive Stamping Press Automation Market was valued at USD 7.1 Billion in 2024 and is estimated to grow at a CAGR of 4.8% to reach USD 11.5 Billion by 2034.

The market holds a crucial role in automotive manufacturing, as it focuses on the automated forming, shaping, and assembly of metal vehicle components. The growing use of robotics, CNC machinery, and automated control systems is enhancing production precision, speed, and repeatability across vehicle manufacturing processes. The rapid expansion of the electric vehicle segment is also reshaping stamping automation, as EV production requires lightweight and complex structural parts. Manufacturers are increasingly investing in advanced automation to support the processing of high-strength steel, aluminum, and composite materials. The integration of Industry 4.0 technologies including IoT, smart sensors, and predictive maintenance has further transformed the sector. These innovations optimize production efficiency by enabling real-time monitoring, automated quality checks, and predictive equipment maintenance. This integration reduces downtime, improves energy efficiency, and ensures high throughput and accuracy in automotive component production. With automation increasingly essential to maintain global competitiveness, demand for advanced stamping systems continues to rise across passenger, commercial, and electric vehicle manufacturing.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $7.1 Billion |

| Forecast Value | $11.5 Billion |

| CAGR | 4.8% |

The press automation systems segment accounted for a 36% share in 2024. This segment is primarily driven by the adoption of servo-driven press technology, which offers superior accuracy, flexibility, and energy efficiency compared to traditional hydraulic presses. Servo presses enable operators to fine-tune forming parameters in real time, reduce material waste, and efficiently process diverse materials such as aluminum alloys and high-strength steel. Their growing use in the production of electric vehicle components underscores their value in precision manufacturing environments.

The fully automated segment is expected to grow at a CAGR of 5.2% from 2025 to 2034. This category integrates high-speed presses, robotic handling systems, and intelligent process control solutions that enable continuous, uninterrupted production. By minimizing manual intervention, these systems enhance throughput, product consistency, and operational safety while reducing cycle times and production costs. Fully automated stamping lines are now central to achieving lean manufacturing objectives and maintaining uniform quality standards across large-scale automotive production facilities.

United States Automotive Stamping Press Automation Market generated USD 1.09 Billion in 2024. Growth in the U.S. market is being driven by a renewed focus on domestic manufacturing and the adoption of advanced automation technologies. Automotive producers are increasingly investing in next-generation stamping systems to improve flexibility, productivity, and quality across both passenger and commercial vehicle production. The reshoring of manufacturing operations and the focus on supply chain resilience continue to strengthen demand for automated solutions in the region.

Key companies operating in the Global Automotive Stamping Press Automation Market include ABB, Komatsu Industries, KUKA, FANUC, AIDA Engineering, AMADA, SEYI Machinery, Bihler of America, ANDRITZ/Schuler, and Universal Robots. To reinforce their position, leading players in the automotive stamping press automation industry are adopting strategies centered on technological innovation, partnerships, and capacity expansion. Companies are developing intelligent servo-driven systems that integrate AI and IoT for predictive maintenance, improved energy control, and enhanced process optimization. Strategic alliances with automakers and robotics firms are helping expand automation solutions across production facilities.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Automation Level

- 2.2.4 Vehicle

- 2.2.5 Application

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing adoption of EVs and lightweight materials

- 3.2.1.2 Integration of Industry 4.0 and smart factory technologies

- 3.2.1.3 Rising vehicle production in emerging markets

- 3.2.1.4 Demand for high-quality, consistent metal components

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High capital investment for advanced automation

- 3.2.2.2 Complexity in integrating multi-material stamping processes

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of EV and lightweight vehicle programs

- 3.2.3.2 Adoption of AI-driven predictive maintenance and process optimization

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 Pestel analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Cost breakdown analysis

- 3.10 Patent analysis

- 3.11 Sustainability & environmental aspects

- 3.11.1 Carbon Footprint Assessment

- 3.11.2 Circular Economy Integration

- 3.11.3 E-Waste Management Requirements

- 3.11.4 Green Manufacturing Initiatives

- 3.12 Use cases and applications

- 3.13 Best-case scenario

- 3.14 Investment landscape

- 3.14.1 Capital expenditure trends in stamping automation

- 3.14.2 Private equity and venture funding activity

- 3.14.3 Mergers, acquisitions, and strategic partnerships

- 3.14.4 Return on investment and payback period analysis

- 3.15 Market adoption trends

- 3.15.1 Rate of automation adoption across vehicle types

- 3.15.2 Adoption by automation level: semi-automated vs fully automated

- 3.15.3 Integration of IoT and AI technologies

- 3.15.4 Adoption barriers and enablers

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Product, 2021 - 2034 ($Mn)

- 5.1 Key trends

- 5.2 Press Automation systems

- 5.3 Robotic Material Handling

- 5.4 Process Control & Monitoring

- 5.5 Integration & services

Chapter 6 Market Estimates & Forecast, By Automation Level, 2021 - 2034 ($Mn)

- 6.1 Key trends

- 6.2 Semi-Automated

- 6.3 Fully Automated

- 6.4 Smart/Connected

Chapter 7 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Mn)

- 7.1 Key trends

- 7.2 Passenger Cars

- 7.2.1 Hatchback

- 7.2.2 Sedan

- 7.2.3 SUV

- 7.3 Commercial Vehicles

- 7.3.1 Light Commercial Vehicles (LCV)

- 7.3.2 Medium Commercial Vehicles (MCV)

- 7.3.3 Heavy Commercial Vehicles (HCV)

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 ($Mn)

- 8.1 Key trends

- 8.2 Body-in-White (BIW)

- 8.3 Powertrain

- 8.4 Safety/Structural

- 8.5 Other

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Nordics

- 9.3.7 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Players

- 10.1.1 ABB

- 10.1.2 AIDA Engineering

- 10.1.3 AMADA

- 10.1.4 ANDRITZ/Schuler

- 10.1.5 Bihler of America

- 10.1.6 FANUC

- 10.1.7 Komatsu Industries

- 10.1.8 KUKA

- 10.1.9 SEYI Machinery

- 10.1.10 Universal Robots

- 10.2 Regional Players

- 10.2.1 Acro Metal Stamping

- 10.2.2 American Axle & Manufacturing

- 10.2.3 ArtiFlex Manufacturing

- 10.2.4 Challenge Manufacturing

- 10.3 Emerging Players / Disruptors

- 10.3.1 AmeriStar

- 10.3.2 Arcade Metal Stamping

- 10.3.3 Automation Tool & Die (ATD)

- 10.3.4 Eagle Press & Equipment