|

시장보고서

상품코드

1937432

자동차 금속 스탬핑 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Automotive Metal Stamping - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

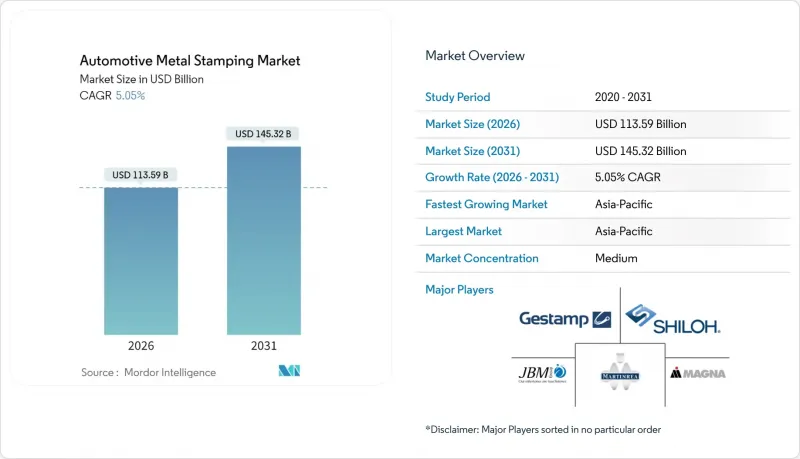

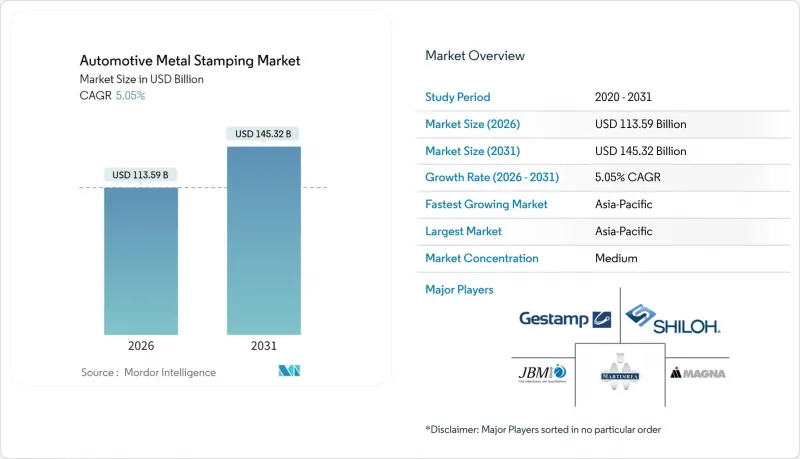

자동차 금속 스탬핑 시장은 2025년에 1,081억 3,000만 달러로 평가되었으며, 2026년 1,135억 9,000만 달러에서 2031년까지 1,453억 2,000만 달러에 달할 것으로 예측됩니다. 예측 기간(2026-2031년) 동안 CAGR은 5.05%로 전망됩니다.

자동차의 전동화 진전, 경량화 규제 강화, 세계 자동차 생산의 꾸준한 회복으로 승용차 및 상용차 프로그램 전체에서 자동차 금속 스탬핑 시장은 견조한 성장세를 보이고 있습니다. 스탬핑 부품은 현대의 모든 차체 구조, 배터리 인클로저, 섀시 모듈의 기초를 구성하고 있으며, OEM 제조업체가 내연기관, 하이브리드, 배터리 전기자동차의 아키텍처를 병행하여 개발함에 따라 이 기술은 필수 불가결한 존재가 되고 있습니다. 알루미늄과 고급고장력강(AHSS)으로의 소재 전환은 계속되고 있지만, 비용과 공급망 친숙도 측면에서 강재가 우위를 점하고 있으며, 생산이 회복되면 프레스 가공업체가 신속하게 생산량을 확대할 수 있도록 하고 있습니다. 동시에 열간 프레스 가공과 서보 프레스의 도입으로 공급업체는 치수 정확도를 잃지 않고 더 얇은 판 두께와 높은 강도를 실현하고 있습니다. 자동차 제조업체들이 무결점 납품과 차량 소프트웨어의 무선 업데이트(OTA)를 지원하는 추적성을 요구함에 따라, 통합 디지털 트윈, 인라인 비전 시스템, 폐쇄형 루프 제어는 테스트 라인에서 주류 생산 라인으로 이동하고 있습니다.

세계 자동차 금속 스탬핑 시장 동향 및 인사이트

자동차 생산 회복 가속화(2025년 이후)

전 세계 자동차 조립량은 팬데믹 이전 최고 수준으로 회복되고 있으며, 프레스 업체들은 휴업 중이던 프레스기를 재가동하고 금형 제작에 박차를 가하고 있습니다. 현대제철이 계획하고 있는 루이지애나 복합단지는 2029년부터 연간 수백만 톤의 자동차 강재를 공급하고, 전기 아크 제강 공정을 통해 탄소강도를 3분의 1로 줄입니다. 지역 라인의 전기자동차(EV) 생산 확대를 가능하게 합니다. 이번 생산능력 확대는 자동차 금속 프레스 시장이 OEM의 신규 모델 출시와 자본 지출을 연동하는 현실을 보여주고 있습니다. 공급업체는 동일한 서보프레스로 고장력강판(AHSS), 기존 강종, 알루미늄 블랭크를 유연하게 생산할 수 있으며, 플랫폼의 다양화에 따라 수주 확대가 예상됩니다. 이러한 유연성은 OEM이 소프트웨어 정의 차량에 대한 소량, 고빈도 생산의 파일럿 로트를 요구할 경우, 새로운 차량의 리드타임을 단축할 수 있습니다.

연비 향상과 EV 항속거리 확대를 위한 경량화 추진

차량에서 1kg이 가벼워질 때마다 차종 전체의 연비 목표가 향상되고, EV의 주행거리가 연장됩니다. 이 때문에 현재 프레스 가공 업체들은 냉간 성형성을 유지하면서 1.2 GPa 이상의 고장력강(AHSS) 제품군을 시험적으로 도입하고 있습니다. ArcelorMittal과 Kirchhoff Automotive는 이중상 강재의 굽힘 특성을 능가하는 포티폼 강종을 입증하여 추가적인 드로우비드 가공 없이도 얇은 두께를 구현할 수 있음을 입증했습니다. 이러한 강종으로 제조된 얇은 두께의 뚜껑, 폐쇄부, 보강 브래킷을 통해 자동차 금속 스탬핑 부품 시장은 보다 가볍고 고강도의 부품을 지속적으로 공급하고 있습니다. 이러한 전환에 따라 공장에서는 고톤수 서보 프레스 및 동일 패널 내에서 서로 다른 두께를 결합하는 맞춤형 용접 블랭크용 레이저를 구매해야 합니다. 알루미늄의 채용도 병행하여 진행되기 때문에 티어1 공급업체는 AHSS 시트의 산세 및 아연도금 처리와 병행하여 열처리 가능한 6xxx계 합금의 용광로 라인의 균형 조정이 필요합니다.

변동하는 철강 및 알루미늄 가격

원자재 가격의 변동은 프레스 가공 비용의 5분의 3 이상을 차지하는 금속 비용으로 인해 약간의 이익을 앗아갈 수 있습니다. 알루미늄 빌릿에 대한 관세 인상(미국의 제안은 세율의 급격한 상승을 의미)은 블랭크 공급업체 전체에 파급되어 1등급 공급업체가 연간 가격 조항을 재협상하도록 강요할 것입니다. 대기업들은 상품거래소에서 헤지를 하거나 제철소와의 다년 계약을 통해 조달량을 고정하여 변동 리스크를 완화하고 있습니다. 자동차 금속 스탬핑 시장의 중소 제조업체들은 운전자금 압박에 직면해 있으며, 공동 조달 풀이나 컨소시엄을 통한 협상력 강화가 요구되고 있습니다.

부문 분석

블랭킹은 2025년 매출의 26.64%를 차지했으며, 이는 다운스트림 성형 전 시트 소재를 그물 모양의 블랭크로 절단하는 핵심 역할을 뒷받침합니다. 이 점유율은 자동차용 금속 스탬핑 가공 시장 규모가 여전히 평면 패턴 준비에 고속 기계 프레스에 의존하고 있는 현실을 보여줍니다. 연속 코일 라인과 인라인 표면 검사는 외판에 필요한 치수 정밀도를 유지합니다. 엠보싱은 규모는 작지만, 디자인 스튜디오가 2차 장식 공정을 생략할 수 있는 텍스처를 요구하고 있어 5.11%의 가장 빠른 CAGR을 기록하고 있습니다.

OEM의 NVH(소음-진동-진동-허쉬네스) 대책용 댐핑 리브와 보강 비드 수요가 엠보싱 가공 라인의 수주를 늘리고 있습니다. 높은 톤수 프레스와 프로그램 가능한 슬라이딩 동작으로 기판을 얇게 만들지 않고도 깊은 패턴을 형성하여 충돌 안전 기준을 충족합니다. 구조 부품의 감소가 진행되는 가운데, 엠보싱 가공은 국부적인 강성을 높이고 판 두께를 줄일 수 있습니다. 그 결과, 서보 구동 프레스에 대한 설비 투자로 공급업체는 블랭킹, 동전 가공, 라이트 엠보싱 가공을 전환할 수 있게 되어, 핵심인 블랭킹 생산량을 유지하면서 서비스 메뉴를 확장할 수 있게 되었습니다. 이러한 접근 방식을 통해 자동차 금속 스탬핑 시장은 다양성을 유지하면서 강인함을 유지하고 있습니다.

판금 성형은 2025년 매출의 42.62%를 차지했으며, 대량 생산되는 인테리어 패널 및 서브 어셈블리에서 전통적인 순송금형이 여전히 자동차 금속 스탬핑 시장의 기반이 되고 있음을 보여줍니다. 자동 코일 공급 장치와 빠른 다이 교환 카트를 통해 가동 시간을 극대화하고, 공급업체는 단축된 모델 사이클을 대응할 수 있습니다. 핫스탬핑은 매출은 뒤처지지만, 1.5GPa 전후의 마르텐사이트계 강도를 필요로 하는 EV용 크래쉬 레일 용도에 힘입어 5.17%의 가장 높은 CAGR을 보이고 있습니다.

다구역 담금질 제어가 가능한 신형 용광로는 수소 취성을 방지하고, 로봇에 의한 진공 이송은 스케일 침착을 억제합니다. Tier 1 공급업체는 기존 프레스와 열간 프레스를 결합한 플랫폼 번들을 제공하여 공급업체 수를 합리화하려는 OEM 구매 부문의 수요를 확보하고 있습니다. 프로그레시브 몰드 및 트랜스퍼 몰드 시스템은 여전히 브래킷과 보강판에서 필수 불가결한 요소입니다. 그러나 서보 프레스의 개조는 AHSS 강판의 성형 한계를 높여 자동차 금속 프레스 시장을 뒷받침하는 점진적인 기술 전환을 입증하고 있습니다.

지역별 분석

아시아태평양은 2025년 세계 매출의 37.89%를 차지했으며, 중국의 조립 라인 재가동과 인도의 정책적 지원으로 인한 현지화 추진에 힘입어 2031년까지 CAGR 5.13%의 견조한 성장이 예상됩니다. 상하이, 광저우, 푸네, 첸나이 주변 클러스터에서는 서보프레스 도입이 진행되어 국내 EV 모델용 고장력 강판 루프 레일과 열간 성형 사이드 실을 생산하고 있습니다. 정부의 신에너지 자동차에 대한 우대정책으로 금형공장의 수주잔고가 금세기 말까지 지속되고 있으며, 이 지역의 자동차 금속 프레스 시장에서의 입지를 강화하고 있습니다.

북미는 스마트 공장에 대한 투자와 한국-일본 철강 대기업의 니어쇼어링으로 기술 우위를 유지합니다. 현대제철 루이지애나 공장은 남부 조립 회랑에 코일 소재를 공급하여 물류 거리 단축과 스탬핑 부품의 탄소발자국 감소를 실현합니다. 미국과 멕시코의 Tier 1 공급업체는 클라우드형 MES 플랫폼을 도입하여 프레스 가동률과 OEM 생산 계획을 동기화했습니다. 페널티를 피함으로써 보너스 획득과 자동차 금속 스탬핑 시장에서의 서비스 수준 향상을 도모합니다.

유럽은 높은 인건비에도 불구하고 혁신 우위를 유지하고 있습니다. 티센크루프 머티리얼즈 프로세싱 유럽의 슈투트가르트 공장 리노베이션 프로젝트에서는 IoT 센서를 AI 기반 공정 제어와 연계하여 스크랩을 줄이고 예지보전의 정확도를 향상시키고 있습니다. EU의 차량 배기가스 규제에 따른 경량화 지침은 다재료 접합 기술에 대한 연구개발을 촉진하고, 공급업체의 기술 지식을 강화하고 있습니다. 남미, 중동 및 아프리카는 여전히 기여도가 낮은 편이나, CKD 조립거점 증가와 함께 특히 픽업 트럭 및 소형 SUV용 그린필드 프레스가 도입되면서 향후 성장기반이 마련되고 있습니다.

기타 특전:

- 엑셀 형식의 시장 예측(ME) 시트

- 애널리스트 지원(3개월)

자주 묻는 질문

목차

제1장 소개

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측(금액(달러))

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KSM 26.03.05The Automotive Metal Stamping Market was valued at USD 108.13 billion in 2025 and estimated to grow from USD 113.59 billion in 2026 to reach USD 145.32 billion by 2031, at a CAGR of 5.05% during the forecast period (2026-2031).

Rising vehicle electrification, lightweighting mandates, and a steady rebound in global automobile output keep the automotive metal stamping market resilient across passenger and commercial vehicle programs. Stamped parts underpin every modern body structure, battery enclosure, and chassis module, making the technology indispensable as OEMs juggle internal-combustion, hybrid, and battery-electric architectures. Material migration toward aluminum and advanced high-strength steel (AHSS) continues, but steel dominates in cost and supply-chain familiarity, allowing stampers to scale volumes quickly whenever production rebounds. Simultaneously, hot-stamping and servo-press upgrades let suppliers achieve thinner gauges and higher strengths without sacrificing dimensional integrity. Integrated digital twins, inline vision systems, and closed-loop controls are moving from pilot lines to mainstream operations as automakers demand zero-defect delivery and traceability to support over-the-air vehicle software updates.

Global Automotive Metal Stamping Market Trends and Insights

Increasing Automobile Production Rebound (Post-2025)

Global vehicle assemblies are climbing pre-pandemic peaks, prompting stampers to reopen idled presses and accelerate tool builds. Hyundai Steel's planned Louisiana complex will deliver numerous automotive steel annually from 2029, cutting carbon intensity by three-fifths via electric-arc routes and positioning regional lines for higher electric-vehicle (EV) output . Capacity expansions illustrate how the automotive metal stamping market aligns capital spending with renewed OEM model launches. Suppliers can juggle AHSS, conventional grades, and aluminum blanks on the same servo press and win incremental orders as platforms diversify. Their flexibility shortens new-model lead times when OEMs request pilot lots for software-defined vehicles in smaller, more frequent batches.

Lightweighting Push for Better Fuel Economy & EV Range

Each kilogram removed from a vehicle lifts fleet fuel economy targets and lengthens EV range, so stampers now trial AHSS families that exceed 1.2 GPa while remaining cold-formable. ArcelorMittal and KIRCHHOFF Automotive validated Fortiform grades that surpass dual-phase steel bending metrics, enabling thinner gauges without extra draw-bead complexity . Down-gauged lids, closures, and reinforcement brackets created through such grades keep the automotive metal stamping market on course to supply lighter yet stronger parts. The transition forces shops to buy higher-tonnage servo presses and tailor-welded-blank lasers that marry dissimilar thicknesses inside one panel. Aluminum uptake runs parallel, so tier-ones must balance furnace lines for heat-treatable 6xxx alloys alongside pickling and galvanizing for AHSS sheets.

Volatile Steel & Aluminum Prices

Raw material swings can erase thin margins because metal outlays exceed three-fifths of stamping cost. Tariff hikes on aluminum billet-US proposals indicate rates climbing exponentially-would ripple across blank suppliers and push tier-ones to renegotiate annual price clauses. Larger players hedge on commodity exchanges or lock multi-year offtake with mills, cushioning volatility. Smaller shops within the automotive metal stamping market face working-capital strain, prompting joint-procurement pools or consortia to gain leverage.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Recovery of Chinese & Indian Auto Supply Chains

- OEM Adoption of Mega-Stamp Body Structures

- Shortage of Skilled Tool-and-Die Makers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Blanking captured 26.64% of 2025 revenue, underscoring its integral role in cutting sheet stock to net-shape blanks before downstream forming. This share illustrates how the automotive metal stamping market size still relies on high-speed mechanical presses for flat-pattern preparation. Continuous coil lines with inline surface inspection uphold the dimensional accuracy needed for outer panels. Embossing, although smaller, is registering the fastest 5.11% CAGR as design studios request textures that remove secondary decorative steps.

OEM requests for NVH damping ribs and stiffening beads lift embossing line orders. High-tonnage presses with programmable slide motions create deep patterns without thinning the base metal, meeting crashworthiness standards. As structures evolve toward fewer parts, embossing raises local stiffness, allowing gauge reduction. Consequently, capital outlays in servo-driven presses ensure suppliers can toggle among blanking, coining, and light embossing, expanding service menus while retaining core blanking volumes. This approach keeps the automotive metal stamping market diversified but resilient.

Sheet-metal forming contributed 42.62% of 2025 turnover, proving that traditional progressive dies still anchor the automotive metal stamping market share for high-volume inner panels and sub-assemblies. Automated coil feeds and quick-die-change carts maximize uptime, letting suppliers meet compressed model cycles. Hot-stamping trails in revenue but shows the strongest 5.17% CAGR, driven by EV crash-rail applications that require martensitic strengths near 1.5 GPa.

New furnaces with multi-zone quench control help prevent hydrogen embrittlement, and robotic vacuum transfer limits scale build-up. Tier-ones offering conventional and hot-stamping win platform bundles from OEM purchasing teams looking to rationalize supplier counts. Progressive-die and transfer-die systems remain essential for brackets and reinforcement plates. Still, servo-press retrofits lift, forming limits on AHSS sheets and illustrating the incremental technology migration sustaining the automotive metal stamping market.

The Automotive Metal Stamping Market Report is Segmented by Technology (Blanking, Embossing, and More), Process (Roll Forming, Hot Stamping, and More), Vehicle Type (Passenger Cars, Light Commercial Vehicles, and More), Material (Steel and More), Application (Body Panels, Transmission & Structural Components, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific commanded 37.89% of global revenue in 2025 and is growing at a robust CAGR of 5.13% through 2031, aided by China's restart of assembly lines and India's policy-backed localization drives. Clusters around Shanghai, Guangzhou, Pune, and Chennai attract servo-press installations, enabling output of AHSS roof rails and hot-stamped side-sills for domestic EV models. Government incentives for new-energy vehicles ensure sustained tool-shop backlogs through the decade-end, bolstering the region's automotive metal stamping market presence.

North America maintains technology leadership through investments in smart-factory upgrades and near-shoring by Korean and Japanese steel majors. Hyundai Steel's Louisiana plant will supply coil stock for southern assembly corridors, shortening logistics and lowering embodied carbon in stamped parts. U.S. and Mexican tier-ones adopt cloud-MES platforms to synchronize press uptime with OEM production sequencing, capturing penalty-avoidance bonuses while elevating service levels within the automotive metal stamping market.

Europe sustains an innovation edge despite high labor costs. Projects like thyssenkrupp Materials Processing Europe's Stuttgart upgrade link IoT sensors to AI-driven process control, slashing scrap and raising predictive maintenance accuracy. Lightweighting directives under EU fleet targets channel R&D toward multi-material joining, reinforcing supplier know-how. South America, the Middle East, and Africa remain smaller contributors. Still, rising CKD assembly hubs usher in greenfield presses, particularly for pickup trucks and compact SUVs, setting the stage for future gains.

- Magna International

- Gestamp Automocion

- Shiloh Industries

- Martinrea International

- JBM Group

- Aisin Seiki

- G-TEKT

- Tower International

- D&H Industries

- PDQ Tool & Stamping

- Alcoa

- American Industrial Company

- Manor Tool & Manufacturing

- Tempco Manufacturing

- Wisconsin Metal Parts

- Lindy Manufacturing

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Automobile Production Rebound

- 4.2.2 Lightweighting Push For Better Fuel Economy & EV Range

- 4.2.3 Growth Of Hot-Stamped Battery Enclosures In EVs

- 4.2.4 Rapid Recovery Of Chinese & Indian Auto Supply Chains

- 4.2.5 OEM Adoption Of Mega-Stamp Body Structures

- 4.2.6 Closed-Loop Digital Twins Enabling Zero-Defect Stamping

- 4.3 Market Restraints

- 4.3.1 Volatile Steel & Aluminum Prices

- 4.3.2 Shortage Of Skilled Tool-And-Die Makers

- 4.3.3 High Cap-Ex For Servo & Hydraulic Presses

- 4.3.4 Regional Metal Supply Disruptions

- 4.4 Value/Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD))

- 5.1 By Technology

- 5.1.1 Blanking

- 5.1.2 Embossing

- 5.1.3 Coining

- 5.1.4 Flanging

- 5.1.5 Bending

- 5.1.6 Deep Drawing

- 5.1.7 Others

- 5.2 By Process

- 5.2.1 Roll Forming

- 5.2.2 Hot Stamping

- 5.2.3 Sheet-Metal Forming

- 5.2.4 Progressive-Die Stamping

- 5.2.5 Transfer-Die Stamping

- 5.2.6 Metal Fabrication

- 5.2.7 Others

- 5.3 By Vehicle Type

- 5.3.1 Passenger Cars

- 5.3.2 Light Commercial Vehicles

- 5.3.3 Medium and Heavy Commercial Vehicles

- 5.4 By Material

- 5.4.1 Steel

- 5.4.2 Aluminum

- 5.4.3 Others

- 5.5 By Application

- 5.5.1 Body Panels

- 5.5.2 Transmission and Structural Components

- 5.5.3 Exhaust Components

- 5.5.4 Chassis and Suspension Parts

- 5.5.5 Others

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Rest of North America

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle-East and Africa

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 Turkey

- 5.6.5.4 Egypt

- 5.6.5.5 South Africa

- 5.6.5.6 Rest of Middle-East and Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Magna International

- 6.4.2 Gestamp Automocion

- 6.4.3 Shiloh Industries

- 6.4.4 Martinrea International

- 6.4.5 JBM Group

- 6.4.6 Aisin Seiki

- 6.4.7 G-TEKT

- 6.4.8 Tower International

- 6.4.9 D&H Industries

- 6.4.10 PDQ Tool & Stamping

- 6.4.11 Alcoa

- 6.4.12 American Industrial Company

- 6.4.13 Manor Tool & Manufacturing

- 6.4.14 Tempco Manufacturing

- 6.4.15 Wisconsin Metal Parts

- 6.4.16 Lindy Manufacturing

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment