|

시장보고서

상품코드

1871319

프리바이오틱스 시장 : 기회, 성장 요인, 업계 동향 분석, 예측(2025-2034년)Prebiotics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

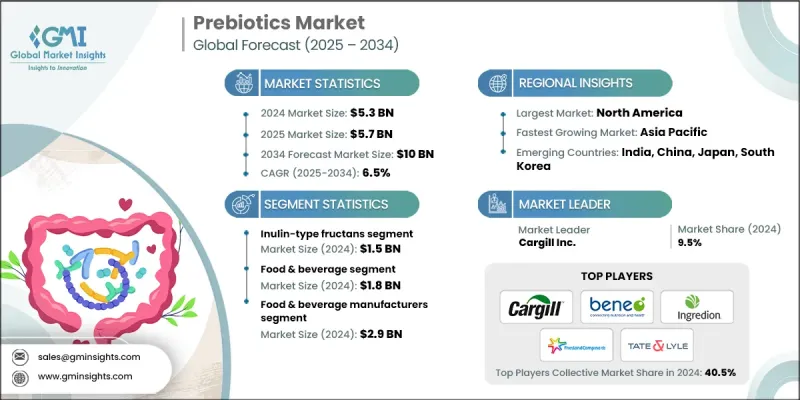

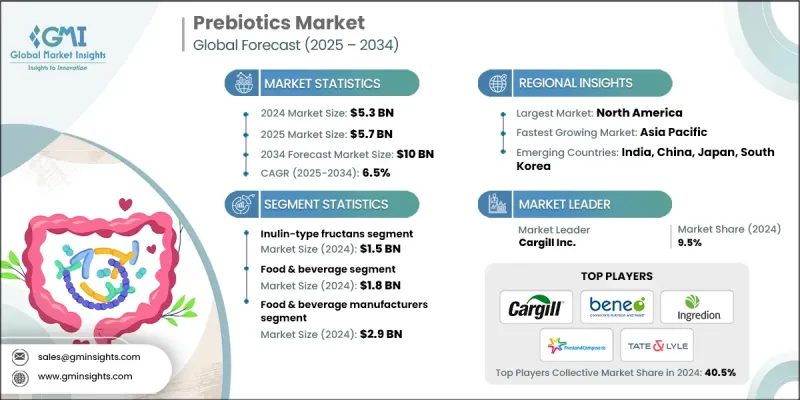

세계 프리바이오틱스 시장은 2024년 53억 달러로 평가되었으며, 2034년까지 연평균 복합 성장률(CAGR) 6.5%로 성장해 100억 달러에 이를 것으로 예측됩니다.

프리바이오틱스는 소화되지 않는 성분이며 유익한 장내 박테리아의 성장을 가속하고 소화기의 건강과 전신 건강을 지원합니다. 이들은 여러 식물성 원료에 자연적으로 포함되어 있으며 기능성 식품, 음료 및 보충제의 배합이 확대되고 있습니다. 장내 환경, 면역력, 예방적 건강 관리에 대한 소비자의 관심이 높아짐에 따라, 프리바이오틱스는 광범위한 건강·영양 산업에서 중요한 구성 요소로서의 지위를 확립하고 있습니다. 추출 기술과 제제 기술의 진보로 프리바이오틱스의 안정성과 효능이 향상되어 보다 폭넓은 용도로 사용할 수 있게 되었습니다. 효소 처리 및 마이크로 캡슐화와 같은 혁신 기술은 프리바이오틱스 원료의 효율성을 높이고 다양한 제품 처방과의 적합성을 향상시키고 있습니다. 천연 유래, 식물성, 클린 라벨 제품에 대한 선호도 증가가 시장 수요를 더욱 뒷받침하고 있습니다. 예방 의료 및 라이프 스타일 주도의 건강 지향으로의 이행에 의해 식품·보충제 제조업체는 소화기의 밸런스와 면역 기능에 대응하는 프리바이오틱스 강화 제품의 개발을 촉진하고 있습니다. 게다가 장과 뇌의 연관성, 그리고 그것이 정신적, 신체적 건강을 이루는 역할에 대한 인식 증가는 특히 도시화 및 선진 경제권에서 세계 시장을 계속 확대하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 기간 | 2025-2034년 |

| 시작 금액 | 53억 달러 |

| 예측 금액 | 100억 달러 |

| CAGR | 6.5% |

2024년 이눌린형 프럭탄 부문은 15억 달러 시장 규모를 창출했습니다. 프락토올리고당과 함께, 이들 프리바이오틱 화합물은 장내 세균총의 균형 유지 및 소화기의 건강 촉진에 중요한 역할을 합니다. 난소화성 전분과 만난 올리고당(MOS)도 대사 기능과 면역력 향상 효과로 수요가 증가하고 있습니다. MOS는 인간 및 동물 영양 분야에서 주목을 받고 있으며 기능성 식품 및 사료 응용 분야에서 기회를 창출하고 있습니다. 이러한 화합물은 진화를 계속하는 기능성 강화 영양 분야에서 유망한 성장 경로를 함께 보여줍니다.

식음료 분야는 2024년 18억 달러 시장 규모를 기록했습니다. 소비자의 관심이 면역기능과 소화기능을 높이는 제품으로 이행하는 동안, 프리바이오틱스의 주요 응용 분야로 계속되고 있습니다. 영양보조식품 분야에서는 개별화·예방영양의 트렌드 확대에 따라 급속한 성장을 이루고 있으며, 소비자가 일상 건강 습관에 프리바이오틱스를 도입하는 경우가 증가하고 있습니다. 유아용 조제 분유나 아기 영양 제품에서는 유아의 건강한 장내 세균총의 촉진과 면역 발달 강화를 목적으로 한 프리바이오틱스의 배합이 계속되어, 세계 시장에서 안정된 수요를 지지하고 있습니다.

미국 프리바이오틱스 시장은 2024년에 82.2%의 점유율을 차지했고, 13억 6,000만 달러로 평가되었습니다. 북미는 소비자의 장내 건강과 면역에 대한 의식 증가를 배경으로 프리바이오틱스 성장의 강력한 거점으로 계속되고 있습니다. 미국에서는 기능성 제품과 클린 라벨 제품에 대한 선호도가 제품 혁신을 형성하여 음식, 음료 및 영양 보조 식품 카테고리 전체에서 채택을 가속화하고 있습니다. 제조업체는 지역 전체의 건강 지향 소비자 증가 기대에 부응하기 위해 배합의 지속적인 개선과 제품 포트폴리오의 다양화를 추진하고 있습니다.

세계의 프리바이오틱스 시장에서 주요 기업으로는 DSM Nutritional Products, Roquette Freres, Beneo GmbH, ADM (Archer Daniels Midland), Cargill Inc., FrieslandCampina Ingredients, Tate & Lyle PLC, Nexira, Ingredion Inc., CJ CheilJedang, Kerry Group plc, Jarrow Formulas, Clasado Biosciences, OptiBiotix Health, Tereos Group, Samyang Holdings, Sensus (Royal Cosun), Quantum Hi-Tech, Tata Chemicals, BAOLINGBAO Biology, Prenexus Health, Meiji Holdings, Cosucra, Yakult Honsha Co., Ltd., Jennewein Biotechnologie 등을 들 수 있습니다. 프리바이오틱스 시장의 기업은 확대하는 소비자 수요에 대응하기 위해, 전략적인 합병, 제휴, 생산 능력의 확대를 통해 글로벌 입지를 강화하고 있습니다. 주요 기업은 다양한 식품 및 보충제 응용 분야에서 소화 효율, 안정성 및 기능 통합을 향상시키는 새로운 프리바이오틱스 제제 개발을 위해 연구 개발에 계속 투자하고 있습니다. 지속가능성과 건강 트렌드에 따른 클린 라벨 및 식물 유래 프리바이오틱스의 생산에 중점을 두고 있습니다. 많은 기업들이 일관된 제품 품질과 조달 투명성을 보장하기 위해 공급망을 강화하기 위해 노력하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 건강과 웰빙에 대한 소비자의 관심 증가

- 기능성 식음료 분야의 확대

- 추출·배합에 있어서의 기술적 진보

- 성장 촉진요인

- 업계의 잠재적 위험 및 과제

- 높은 생산 및 가공 비용

- 규제 및 표시에 관한 과제

- 시장 기회

- 확대하는 비건 및 식물 유래 시장

- 신바이오틱 제품과의 통합

- 유아용 조제 분유 및 노인용 영양 식품에 사용

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 기술과 혁신의 상황

- 현재의 기술 동향

- 신규기술

- 가격 동향

- 지역별

- 제품 유형별

- 장래 시장 동향

- 기술과 혁신의 상황

- 현재의 기술 동향

- 신규기술

- 특허 상황

- 무역 통계(HS코드)(참고 : 무역 통계는 주요 국가에서만 제공됨)

- 주요 수입국

- 주요 수출국

- 지속가능성과 환경적 측면

- 지속가능한 대처

- 폐기물 감축 전략

- 생산에 있어서의 에너지 효율

- 친환경 이니셔티브

- 탄소발자국 고려

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병 및 인수

- 제휴 및 협업

- 신제품 발매

- 확대 계획

제5장 시장 추정 및 예측 : 제품 유형별, 2021-2034

- 주요 동향

- 이눌린형 프럭탄

- 프락토 올리고당(FOS)

- 갈락토 올리고당(GOS)

- 모유 올리고당(HMOs)

- 내성 전분

- 만난 올리고당(MOS)

- 기타

제6장 시장 추정 및 예측 : 용도별, 2021-2034

- 식음료 업계

- 영양보조식품

- 유아용 조제 분유·베이비 푸드

- 사료·동물 영양

- 화장품 및 퍼스널케어

- 의약품 및 의료 용도

제7장 시장 추정 및 예측 : 최종 이용 산업별, 2021-2034

- 주요 동향

- 식음료 제조업체

- 제약회사

- 사료 제조업체

- 화장품 및 퍼스널케어 기업

제8장 시장 추정 및 예측 : 지역별, 2021-2034

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 기타 라틴아메리카

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

제9장 기업 프로파일

- ADM(Archer Daniels Midland)

- BAOLINGBAO Biology

- Beneo GmbH

- Cargill Inc.

- CJ CheilJedang

- Clasado Biosciences

- Cosucra

- DSM Nutritional Products

- FrieslandCampina Ingredients

- Ingredion Inc.

- Jarrow Formulas

- Jennewein Biotechnologie

- Kerry Group plc

- Meiji Holdings

- Nexira

- OptiBiotix Health

- Prenexus Health

- Quantum Hi-Tech

- Roquette Freres

- Samyang Holdings

- Sensus(Royal Cosun)

- Tate &Lyle PLC

- Tereos Group

- Tata Chemicals

- Yakult Honsha Co., Ltd.

The Global Prebiotics Market was valued at USD 5.3 billion in 2024 and is estimated to grow at a CAGR of 6.5% to reach USD 10 billion by 2034.

Prebiotics are non-digestible ingredients that help stimulate the growth of beneficial gut bacteria, supporting digestive wellness and overall health. They are naturally present in several plant-based sources and are increasingly being incorporated into functional foods, beverages, and supplements. Rising consumer interest in gut health, immunity, and preventive wellness has positioned prebiotics as a crucial component in the broader health and nutrition industry. Advances in extraction and formulation technologies have improved the stability and potency of prebiotics, enabling their use in a wider range of applications. Innovations such as enzymatic processing and microencapsulation are enhancing the efficiency of prebiotic ingredients and boosting their compatibility with various product formulations. Growing preferences for natural, plant-based, and clean-label products are further fueling market demand. The shift toward preventive healthcare and lifestyle-driven wellness has encouraged food and supplement manufacturers to introduce prebiotic-enhanced offerings that address digestive balance and immunity. Additionally, increasing awareness of the gut-brain connection and its role in mental and physical health continues to expand the global market, particularly across urbanized and developed economies.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $5.3 Billion |

| Forecast Value | $10 Billion |

| CAGR | 6.5% |

In 2024, the inulin-type fructans segment generated USD 1.5 billion. Along with fructooligosaccharides, these prebiotic compounds play a crucial role in maintaining gut microbiota balance and promoting digestive well-being. Resistant starch and mannan-oligosaccharides (MOS) are also witnessing rising demand due to their metabolic and immune-boosting benefits. MOS is gaining traction in both human and animal nutrition, creating opportunities across functional foods and feed applications. Together, these compounds represent a promising growth avenue in the evolving field of functional and fortified nutrition.

The food & beverage segment generated USD 1.8 billion in 2024. It remains the primary application area for prebiotics, as consumer focus shifts toward products that enhance immunity and digestive function. Dietary supplements are experiencing rapid expansion driven by the rising trend of personalized and preventive nutrition, with consumers increasingly integrating prebiotics into their daily wellness routines. Infant formula and baby nutrition products continue to incorporate prebiotics to promote healthy gut flora and strengthen immune development in infants, fueling consistent demand across global markets.

U.S. Prebiotics Market held 82.2% and generated USD 1.36 billion in 2024. North America remains a strong hub for prebiotics growth, driven by heightened awareness of gut health and immunity among consumers. In the U.S., the preference for functional and clean-label products is shaping product innovation and accelerating adoption across food, beverage, and dietary supplement categories. Manufacturers are continuously improving formulations and diversifying product portfolios to meet the rising expectations of health-conscious consumers throughout the region.

Key companies active in the Global Prebiotics Market include DSM Nutritional Products, Roquette Freres, Beneo GmbH, ADM (Archer Daniels Midland), Cargill Inc., FrieslandCampina Ingredients, Tate & Lyle PLC, Nexira, Ingredion Inc., CJ CheilJedang, Kerry Group plc, Jarrow Formulas, Clasado Biosciences, OptiBiotix Health, Tereos Group, Samyang Holdings, Sensus (Royal Cosun), Quantum Hi-Tech, Tata Chemicals, BAOLINGBAO Biology, Prenexus Health, Meiji Holdings, Cosucra, Yakult Honsha Co., Ltd., and Jennewein Biotechnologie. Companies in the Prebiotics Market are enhancing their global footprint through strategic mergers, collaborations, and capacity expansions to meet growing consumer demand. Leading firms are investing in R&D to develop novel prebiotic formulations that improve digestive efficiency, stability, and functional integration across diverse food and supplement applications. Emphasis is placed on producing clean-label and plant-based prebiotics that align with sustainability and health trends. Many companies are strengthening their supply chains to ensure consistent product quality and sourcing transparency.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Product type

- 2.2.2 Application

- 2.2.3 End use industry

- 2.2.4 Regional

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing consumer focus on health and wellness

- 3.2.1.2 Expansion of functional food & beverage sector

- 3.2.1.3 Technological advancements in extraction & formulation

- 3.2.1 Growth drivers

- 3.3 Industry pitfalls and challenges

- 3.3.1 High production and processing costs

- 3.3.2 Regulatory and labeling challenges

- 3.4 Market opportunities

- 3.4.1 Growing vegan and plant-based market

- 3.4.2 Integration with synbiotic products

- 3.4.3 Use in infant formula and elderly nutrition

- 3.5 Growth potential analysis

- 3.6 Regulatory landscape

- 3.6.1 North America

- 3.6.2 Europe

- 3.6.3 Asia Pacific

- 3.6.4 Latin America

- 3.6.5 Middle East & Africa

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Price trends

- 3.10.1 By region

- 3.10.2 By product type

- 3.11 Future market trends

- 3.12 Technology and innovation landscape

- 3.12.1 Current technological trends

- 3.12.2 Emerging technologies

- 3.13 Patent landscape

- 3.14 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.14.1 Major importing countries

- 3.14.2 Major exporting countries

- 3.15 Sustainability and environmental aspects

- 3.15.1 Sustainable practices

- 3.15.2 Waste reduction strategies

- 3.15.3 Energy efficiency in production

- 3.15.4 Eco-friendly initiatives

- 3.16 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021-2034 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Inulin-Type Fructans

- 5.3 Fructooligosaccharides (FOS)

- 5.4 Galactooligosaccharides (GOS)

- 5.5 Human Milk Oligosaccharides (HMOs)

- 5.6 Resistant starch

- 5.7 Mannan-oligosaccharides (MOS)

- 5.8 Others

Chapter 6 Market Estimates and Forecast, By Application, 2021-2034 (USD Million) (Kilo Tons)

- 6.1 Food & beverage industry

- 6.2 Dietary supplements

- 6.3 Infant formula & baby food

- 6.4 Animal feed & nutrition

- 6.5 Cosmetics & personal care

- 6.6 Pharmaceutical & medical applications

Chapter 7 Market Estimates and Forecast, By End Use Industry, 2021-2034 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Food & beverage manufacturers

- 7.3 Pharmaceutical companies

- 7.4 Animal feed manufacturers

- 7.5 Cosmetics & personal care companies

Chapter 8 Market Estimates and Forecast, By Region, 2021-2034 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 ADM (Archer Daniels Midland)

- 9.2 BAOLINGBAO Biology

- 9.3 Beneo GmbH

- 9.4 Cargill Inc.

- 9.5 CJ CheilJedang

- 9.6 Clasado Biosciences

- 9.7 Cosucra

- 9.8 DSM Nutritional Products

- 9.9 FrieslandCampina Ingredients

- 9.10 Ingredion Inc.

- 9.11 Jarrow Formulas

- 9.12 Jennewein Biotechnologie

- 9.13 Kerry Group plc

- 9.14 Meiji Holdings

- 9.15 Nexira

- 9.16 OptiBiotix Health

- 9.17 Prenexus Health

- 9.18 Quantum Hi-Tech

- 9.19 Roquette Freres

- 9.20 Samyang Holdings

- 9.21 Sensus (Royal Cosun)

- 9.22 Tate & Lyle PLC

- 9.23 Tereos Group

- 9.24 Tata Chemicals

- 9.25 Yakult Honsha Co., Ltd.