|

시장보고서

상품코드

1876553

그린케미스트리용 불균일 촉매 시장 : 기회, 성장 촉진요인, 업계 동향 분석, 예측(2025-2034년)Heterogeneous Catalysts for Green Chemistry Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

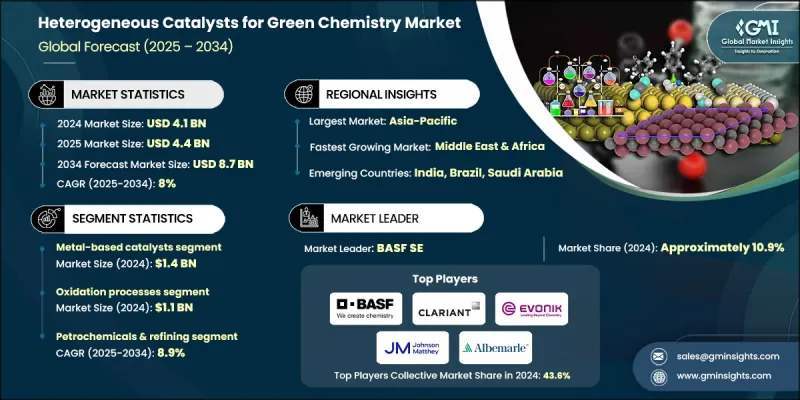

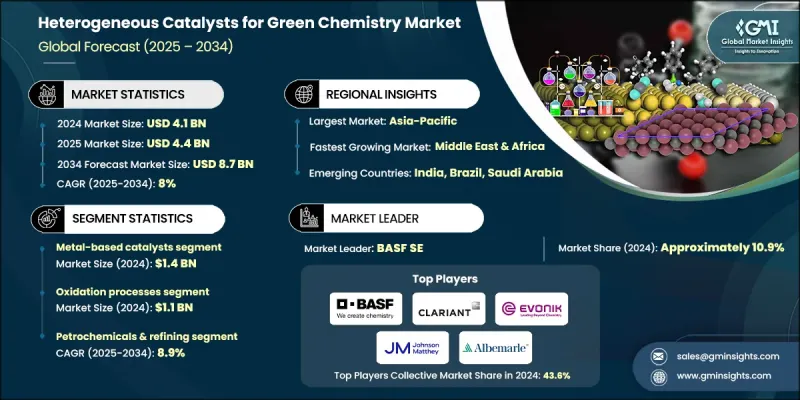

세계의 그린케미스트리용 불균일 촉매 시장은 2024년에 41억 달러로 평가되었으며, 2034년까지 연평균 복합 성장률(CAGR) 8%로 성장하여 87억 달러에 이를 것으로 예측됩니다.

이러한 성장은 기술적 돌파구, 규제 압력, 지속 가능한 화학 공정에 대한 관심 증가에 의해 견인됩니다. 컴퓨팅 모델링, 높은 처리량 스크리닝, 디지털 트윈 시뮬레이션의 발전으로 조사 사이클이 크게 단축되어 고성능 촉매를 신속하게 식별할 수 있습니다. 한편, 유럽연합과 중국 등 주요 지역의 유황 및 CO2 배출량을 대상으로 하는 규제는 경제적인 불확실성의 시기에도 정유소와 화학 플랜트가 차세대 촉매에 투자를 촉구하고 있습니다. 업계는 점점 더 데이터 주도형으로 전환하고 있으며, 현장 분광법과 클라우드 분석을 결합하여 컨셉부터 상품화까지의 타임라인을 가속화하고 있습니다. 이러한 동향은 디지털 퍼스트 방식으로 신규 참가자를 끌어들이는 한편 기존 기업은 진화하는 환경 기준에 적합하기 때문에 지속적으로 프로세스를 업그레이드하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 41억 달러 |

| 예측 금액 | 87억 달러 |

| CAGR | 8% |

산화 프로세스 분야는 2024년에 11억 달러 시장 규모를 기록했으며, 2025년부터 2034년에 걸쳐 CAGR 7%로 성장할 것으로 전망되고 있습니다. 저온전화 플랫폼은 탈탄소화를 가능하게 하고 있으며, 산화 반응과 수소화 반응이 수전해 인프라를 공유하는 경우가 증가하고 있습니다. 이로 인해 운영 비용이 가스에서 재생에너지로 전환됩니다. 이러한 움직임은 화학적 조건과 전기화학적 조건 모두에서 효과적으로 작동하는 상호 호환성 이질성 촉매 수요를 촉진합니다.

석유화학·정제부문은 2024년에 13억 달러로 평가되어 31.3%의 점유율을 차지했고 2025년부터 2034년에 걸쳐 CAGR은 8.9%를 보일 것으로 예측됩니다. 정제분야에서는 여전히 불균일계 촉매의 대부분이 소비되고 있으며, 현재는 대체 원료의 처리나 제품 수율의 최적화에 의해 엄격한 황 규제에 대한 대응이 진행되고 있습니다. 첨단 촉매 조성으로 정유소는 전통적인 운영에서 부가가치 창출 프로세스로 전환하고 있습니다.

북미의 그린케미스트리용 불균일 촉매 시장은 2024년 12억 달러 규모를 기록했으며, 2034년까지 26억 달러에 이를 것으로 전망됩니다. 인플레이션 억제법에 근거한 우대 조치를 포함한 지원 정책은 재생가능 연료 및 CO2 화학 프로젝트에 대한 투자를 촉진하고 있습니다. 이 프로그램은 Albemarle, Johnson Matthey 등의 업계 리더와 신흥 혁신가가 생산하는 은(Ag), 구리 아연(CuZn), 니켈 철(NiFe) 등의 내구성 있는 촉매에 대한 안정적인 수요를 창출하고 있습니다. 촉매, 디지털 트윈 기술 및 금속 환매 프로그램을 결합한 다년 서비스 계약은 공급망 확보 및 가격 안정화를 위해 점점 채택되고 있습니다.

세계의 그린 케미컬용 불균일 촉매 시장에서 주요 기업으로는 Evonik Industries AG, Johnson Matthey plc, Clariant AG, BASF SE, Albermarle Corporation 등이 있습니다. 그린케미스트리를 위한 불균일계 촉매 시장의 기업은 자사의 지위를 강화하고 존재감을 확대하기 위해 몇 가지 전략을 채용하고 있습니다. 화학 공정과 전기 화학 공정 모두에서 효율성, 선택성 및 상호 호환성이 높은 촉매를 개발하기 위해 첨단 연구 개발에 투자하고 있습니다. 산업 최종 사용자 및 연구 기관과의 전략적 제휴는 제품 채택과 검증을 가속화하는 데 도움이 됩니다. 또한 시뮬레이션, AI, 클라우드 기반 분석을 통해 디지털 기능을 강화하고 촉매 성능과 라이프사이클 관리 최적화를 도모하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

- 시장 범위와 정의

- 조사 설계

- 조사 접근

- 데이터 수집 방법

- 데이터 마이닝의 출처

- 세계

- 지역별/국가별

- 기본 추정치와 계산

- 기준연도 계산

- 시장 추정에서의 주요 동향

- 1차 조사·검증

- 1차 정보

- 예측 모델

- 조사의 전제조건과 제한 사항

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 업계의 잠재적 리스크 및 과제

- 시장 기회

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 가격 동향

- 지역별

- 장래 시장 동향

- 기술과 혁신 동향

- 현재의 기술 동향

- 신규기술

- 특허 상황

- 무역 통계(주 : 무역 통계는 주요 국가에서만 제공됨)

- 주요 수입국

- 주요 수출국

- 지속가능성과 환경적 측면

- 지속가능한 실천

- 폐기물 감축 전략

- 생산에 있어서의 에너지 효율

- 친환경 이니셔티브

- 탄소발자국 고려

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병 및 인수

- 제휴 및 협력관계

- 신제품 발매

- 사업 확대 계획

제5장 시장 추정 및 예측 : 유형별, 2025년-2034년

- 주요 동향

- 금속계 촉매

- 귀금속 촉매(Pt, Pd, Rh, Au)

- 베이스 메탈 촉매(Ni, Cu, Co, Fe)

- 이금속 및 합금 시스템

- 금속 산화물 촉매

- 단일 금속 산화물

- 혼합 금속 산화물·페로브스카이트

- 제올라이트계 촉매

- 합성 제올라이트

- 계층 구조·수식 제올라이트

- 금속 유기 구조체(MOFs)

- Zr-MOFs 및 UiO series

- Cu-MOFs 및 HKUST-1 유도체

- 탄소 기반 촉매

- 활성탄 및 바이오차

- 탄소나노튜브 및 그래핀

제6장 시장 추정 및 예측 : 프로세스별, 2025년-2034년

- 주요 동향

- 산화 공정

- 수소화·환원

- 산염기 촉매 반응

- 탄소-탄소 결합 형성 반응

- 광촉매·전기 촉매 공정

제7장 시장 추정 및 예측 : 최종 용도별, 2025년-2034년

- 주요 동향

- 석유화학·정제

- 수소 처리 응용

- 유동 접촉 분해

- 개질 및 이성질화

- 정밀화학 및 의약품

- API 합성

- 특수화학제품의 제조

- 키랄 및 엔안티오선택적 합성

- 환경 응용

- 대기오염 방지

- 수처리 기술

- 이산화탄소 전환 및 활용

- 고분자 및 플라스틱 생산

- 폴리올레핀 촉매

- 지속가능한 폴리머 합성

- 기타

제8장 시장 추정 및 예측 : 지역별, 2025년-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 기타 라틴아메리카

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

제9장 기업 프로파일

- BASF SE

- Clariant AG

- Evonik Industries AG

- Johnson Matthey plc

- Albemarle Corporation

- WR Grace &Co.

- Haldor Topsoe A/S

- Honeywell UOP

- Axens SA

- Umicore

- Zeolyst International

- JGC Catalysts and Chemicals Ltd.

- CRI Catalyst Company

- SOLVAY SA

- Sud-Chemie India Pvt Ltd

The Global Heterogeneous Catalysts for Green Chemistry Market was valued at USD 4.1 billion in 2024 and is estimated to grow at a CAGR of 8% to reach USD 8.7 billion by 2034.

The growth is being driven by technological breakthroughs, regulatory pressures, and the rising focus on sustainable chemical processes. Advancements in computational modeling, high-throughput screening, and digital twin simulations are significantly shortening research cycles and enabling faster identification of high-performance catalysts. Meanwhile, regulations targeting sulfur and CO2 emissions in major regions like the European Union and China are encouraging refineries and chemical plants to invest in next-generation catalysts, even during periods of economic uncertainty. The industry is increasingly data-driven, combining in-situ spectroscopy with cloud analytics to accelerate concept-to-commercialization timelines. These trends are attracting new entrants with digital-first approaches, while established players are continuously upgrading processes to comply with evolving environmental standards.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.1 Billion |

| Forecast Value | $8.7 Billion |

| CAGR | 8% |

The oxidation processes segment was valued at USD 1.1 billion in 2024 and is expected to grow at a CAGR of 7% from 2025 to 2034. Low-temperature electrified platforms are enabling decarbonization, with oxidation and hydrogenation reactions increasingly sharing water-electrolysis infrastructure, shifting operating costs from gas to renewable power. This is driving demand for cross-compatible heterogeneous catalysts that perform effectively under both chemical and electrochemical conditions.

The petrochemicals and refining segment was valued at USD 1.3 billion in 2024, accounting for a 31.3% share, and is projected to grow at a CAGR of 8.9% during 2025-2034. Refining continues to consume the majority of heterogeneous catalyst volumes, with operations now processing alternative feedstocks and optimizing product yields to meet stringent sulfur regulations. Advanced catalyst formulations are helping refineries transform traditional operations into value-generating processes.

North America Heterogeneous Catalysts for Green Chemistry Market generated USD 1.2 billion in 2024 and is expected to reach USD 2.6 billion by 2034. Supportive policies, including incentives under the Inflation Reduction Act, are driving investments in renewable-fuel and CO2-to-chemical projects. These programs create a steady demand for durable catalysts like Ag, CuZn, and NiFe produced by industry leaders such as Albemarle, Johnson Matthey, and emerging innovators. Multi-year service contracts bundling catalysts, digital twin technologies, and metal buy-back programs are increasingly adopted to secure supply chains and stabilize pricing.

Key players operating in the Global Heterogeneous Catalysts for Green Chemistry Market include Evonik Industries AG, Johnson Matthey plc, Clariant AG, BASF SE, and Albemarle Corporation. Companies in the Heterogeneous Catalysts for Green Chemistry Market are employing several strategies to strengthen their position and expand their presence. They are investing in advanced research and development to create catalysts with higher efficiency, selectivity, and cross-compatibility for both chemical and electrochemical processes. Strategic collaborations with industrial end-users and research institutions help accelerate product adoption and validation. Firms are also enhancing digital capabilities through simulation, AI, and cloud-based analytics to optimize catalyst performance and lifecycle management.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Process

- 2.2.4 End use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and Environmental Aspects

- 3.12.1 Sustainable Practices

- 3.12.2 Waste Reduction Strategies

- 3.12.3 Energy Efficiency in Production

- 3.12.4 Eco-friendly Initiatives

- 3.13 Carbon Footprint Considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Type, 2025 - 2034 (USD Billion, Kilo Tons)

- 5.1 Key trends

- 5.2 Metal-based catalysts

- 5.2.1 Noble metal catalysts (Pt, Pd, Rh, Au)

- 5.2.2 Base metal catalysts (Ni, Cu, Co, Fe)

- 5.2.3 Bimetallic and alloy systems

- 5.3 Metal oxide catalysts

- 5.3.1 Single metal oxides

- 5.3.2 Mixed metal oxides and perovskites

- 5.4 Zeolite-based catalysts

- 5.4.1 Synthetic zeolites

- 5.4.2 Hierarchical and modified zeolites

- 5.5 Metal-organic frameworks (MOFs)

- 5.5.1 Zr-MOFs and UiO series

- 5.5.2 Cu-MOFs and HKUST-1 derivatives

- 5.6 Carbon-based catalysts

- 5.6.1 Activated carbon and biochar

- 5.6.2 Carbon nanotubes and graphene

Chapter 6 Market Estimates and Forecast, By Process, 2025 - 2034 (USD Billion, Kilo Tons)

- 6.1 Key trends

- 6.2 Oxidation processes

- 6.3 Hydrogenation and reduction

- 6.4 Acid-base catalyzed reactions

- 6.5 C-C bond formation reactions

- 6.6 Photocatalytic and electrocatalytic processes

Chapter 7 Market Estimates and Forecast, By End Use, 2025 - 2034 (USD Billion, Kilo Tons)

- 7.1 Key trends

- 7.2 Petrochemicals & refining

- 7.2.1 Hydroprocessing applications

- 7.2.2 Fluid catalytic cracking

- 7.2.3 Reforming and isomerization

- 7.3 Fine chemicals & pharmaceuticals

- 7.3.1 API synthesis

- 7.3.2 Specialty chemical production

- 7.3.3 Chiral and enantioselective synthesis

- 7.4 Environmental applications

- 7.4.1 Air pollution control

- 7.4.2 Water treatment technologies

- 7.4.3 CO2 conversion and utilization

- 7.5 Polymer & plastics production

- 7.5.1 Polyolefin catalysis

- 7.5.2 Sustainable polymer synthesis

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By Region, 2025 - 2034 (USD Billion, Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East & Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East & Africa

Chapter 9 Company Profiles

- 9.1 BASF SE

- 9.2 Clariant AG

- 9.3 Evonik Industries AG

- 9.4 Johnson Matthey plc

- 9.5 Albemarle Corporation

- 9.6 W. R. Grace & Co.

- 9.7 Haldor Topsøe A/S

- 9.8 Honeywell UOP

- 9.9 Axens S.A.

- 9.10 Umicore

- 9.11 Zeolyst International

- 9.12 JGC Catalysts and Chemicals Ltd.

- 9.13 CRI Catalyst Company

- 9.14 SOLVAY S.A.

- 9.15 Sud-Chemie India Pvt Ltd