|

시장보고서

상품코드

1876566

압축천연가스(CNG) 자동차 시스템 시장 : 기회, 성장 촉진요인, 업계 동향 분석, 예측(2025-2034년)Compressed Natural Gas (CNG) Vehicle System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

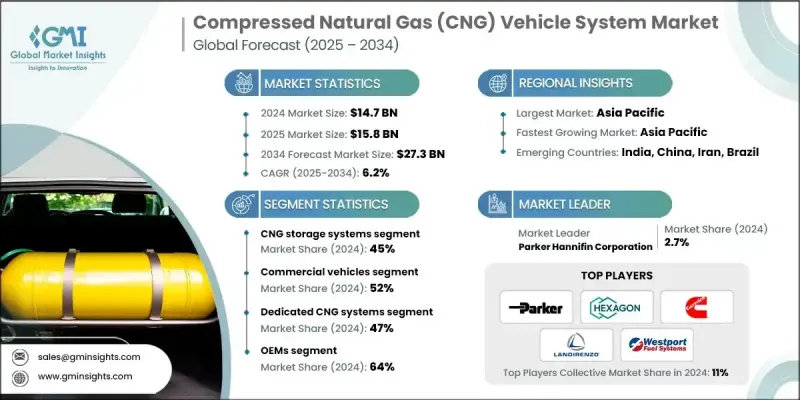

세계의 압축천연가스(CNG) 자동차 시스템 시장은 2024년 147억 달러로 평가되었으며, 2034년까지 연평균 복합 성장률(CAGR) 6.2%로 성장해 273억 달러에 이를 것으로 예측됩니다.

이 시장 확대는 주요 자동차 지역의 배출 가스 규제와 탄소 감축 규제의 강화에 의해 추진되고 있으며, OEM 제조업체나 플릿 사업자가 CNG 등의 깨끗한 대체 연료의 도입을 촉진하고 있습니다. 디젤 및 가솔린 차량에 비해 CNG 차량은 CO2, 질소산화물(NOx), 미립자(PM) 배출량이 상당히 낮아 승용차 및 상용차용 유로 6 및 버랏 스테이지 VI와 같은 환경 규제 준수를 지원합니다. CNG의 비용 우위성도 시장 성장을 뒷받침하고 있으며, 가솔린이나 디젤에 비해 1킬로미터당 비용이 약 30-40% 낮아, 플릿 사업자나 비용 의식이 높은 소비자에게 있어 큰 절약 효과를 가져옵니다. 세계적인 원유가격의 변동에 따라 특히 신흥지역에서는 연료수입 의존도를 줄이는 전략으로 CNG 도입을 촉진하는 정부의 이니셔티브이 진행되고 있습니다. CNG의 급유·유통 인프라에 대한 투자에 의해 접근성이 향상되고, 관민 제휴나 정부 자금에 의한 대처에 의해 고속도로나 도시 회랑을 따라의 스테이션 네트워크가 확대하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 147억 달러 |

| 예측 금액 | 273억 달러 |

| CAGR | 6.2% |

CNG 저장 시스템 부문은 2024년에 66억 6,000만 달러로 평가되었고, 2034년까지 122억 1,000만 달러에 이를 것으로 예측됩니다. 이 부문은 경량 복합재료의 기술 진보의 이점을 얻었으며, 복합 탱크의 제조 비용이 30%에서 50%까지 줄어들 가능성이 조사에 제시되어 있습니다.

전용 CNG 시스템 부문은 2024년에 47%의 점유율을 차지했고 2025년부터 2034년에 걸쳐 CAGR 7.8%로 성장할 것으로 예측됩니다. 이 차량은 연료 효율과 낮은 배출 가스 특성으로 인해 함대와 도시 교통 시스템에서 인기가 있습니다. 기존 CNG 인프라는 여전히 제한적이지만 제조업체는 신뢰성 향상을 위해 엔진 설계 및 저장 시스템 최적화에 주력하고 있으며 전용 시스템은 지속 가능한 교통 이니셔티브의 중심이되었습니다.

미국의 압축 천연가스(CNG) 자동차 시스템 시장은 2024년 91%의 점유율을 차지하여 1억640만 달러의 수익을 올렸습니다. 미국은 세계 시장에서 그 점유율은 작지만, 이 나라는 석유 자원이 풍부하기 때문에 대체 연료에 중점적으로 임하고 있는 지역에 비해 성장은 한정적이지만, 성숙한 시장이 계속되고 있습니다.

압축 천연가스(CNG) 자동차 시스템 시장에서 사업을 전개하고 있는 주요 기업으로는 Westport Fuel Systems, Parker Hannifin, Hexagon Composites, Clean Energy Fuels, Cummins, BRC Gas, Galileo Technologies, Luxfer, Landi Renzo, Worthington Industries 등이 있습니다. 압축 천연가스(CNG) 자동차 시스템 시장의 기업들은 자신의 지위를 강화하고 시장 점유율을 확대하기 위해 여러 전략을 채택하고 있습니다. 엔진 효율, 저장 용량, 연료 시스템의 내구성을 높이기 위한 연구 개발에 투자하고 있습니다. 자동차 OEM과의 전략적 제휴를 통해 CNG 시스템을 신차 모델에 원활하게 통합할 수 있습니다. 기업은 세계 유통 네트워크를 확대하고, 연료 공급 인프라 제공업체와 제휴 관계를 구축하고, 보다 깨끗한 운송에 관한 정부의 이니셔티브을 지원하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

- 시장 범위와 정의

- 조사 설계

- 조사 접근

- 데이터 수집 방법

- 데이터 마이닝의 출처

- 세계

- 지역별/국가별

- 기본 추정치와 계산

- 기준연도 계산

- 시장 추정에서의 주요 동향

- 1차 조사·검증

- 1차 정보

- 예측 모델

- 조사의 전제조건과 제한 사항

제2장 주요 요약

제3장 업계 인사이트

- 업계 생태계 분석

- 공급자의 상황

- 이익률

- 비용 구조

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 엄격한 배출규제

- 연료비 격차 확대

- 급유 인프라의 확충

- OEM 제조업체와의 통합·기술적 진보

- 업계의 잠재적 리스크 및 과제

- 신흥 지역의 한정된 급유 인프라

- 높은 초기 전환 및 저장 비용

- 시장 기회

- 정부 보조금·우대 조치

- 플릿 전동화·하이브리드 통합

- 도시 지역의 대중 교통 수요 증가

- 경량 복합재 실린더의 개발

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 기술과 혁신 동향

- 현재의 기술 동향

- 신규 기술

- 기술 준비도·성숙도 평가

- 가격 동향

- 지역별

- 제품별

- 생산 통계

- 생산 거점

- 소비 거점

- 수출과 수입

- 코스트 내역 분석

- 특허 분석

- 지속가능성과 환경면

- 지속가능한 실천

- 폐기물 감축 전략

- 생산에 있어서의 에너지 효율화

- 친환경 이니셔티브

- 탄소발자국 고려

- 비즈니스 모델 분석

- 설비 판매 모델과 리스 모델

- 서비스 및 유지보수 수익원

- IaaS(Infrastructure-as-a-service) 모델

- 연료 공급 계약의 구조

- 최종 용도 조사의 지견과 요건

- 리스크 평가 및 경감책

- 기술 리스크 분석

- 시장 리스크 요인

- 규제 리스크 평가

- 공급망 위험 평가

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

- 주요 발전

- 합병 및 인수

- 제휴 및 협력관계

- 신제품 발매

- 사업 확대 계획과 자금 조달

- 제품 및 서비스 벤치마킹

- R&D 투자 분석

- 벤더 선정 기준

제5장 시장 추정 및 예측 : 제품별, 2021년-2034년

- 주요 동향

- CNG 저장 시스템

- 유형 I(강철)

- 유형 II(강철+복합재)

- 유형 III(알루미늄+복합재)

- 유형 IV(완전 복합재)

- 연료 공급 시스템

- 압력 조절기

- 연료 분사기

- 전자제어유닛

- 연료 라인 및 피팅

- 전환 키트

- 완전한 리노베이션 시스템

- 이중 연료 전환 키트

- 전용 CNG 시스템

- 기타 구성요소

- 안전 시스템

- 계측기 및 표시기

- 설치용 액세서리

제6장 시장 추정 및 예측 : 시스템별, 2021년-2034년

- 주요 동향

- 전용 CNG 시스템

- 바이퓨엘(CNG/가솔린) 시스템

- 듀얼 연료(CNG/디젤) 시스템

제7장 시장 추정 및 예측 : 차량별, 2021년-2034년

- 주요 동향

- 승용차

- 세단

- SUV

- 해치백

- 상용차

- 소형 상용차(LCV)

- 대형 상용차(HCV)

- 중형 상용차(MCV)

- 오프 하이웨이 차량

제8장 시장 추정 및 예측 : 최종 용도별, 2021년-2034년

- 주요 동향

- OEM

- 애프터마켓

제9장 시장 추정 및 예측 : 지역별, 2021년-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 북유럽 국가

- 러시아

- 폴란드

- 루마니아

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- ANZ

- 베트남

- 인도네시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 이란

제10장 기업 프로파일

- Global companies

- BRC Gas

- Chart Industries

- Clean Energy Fuel

- Cummins

- Hexagon Composites

- Landi Renzo

- Luxfer

- Parker Hannifin

- Westport Fuel Systems

- Worthington Industries

- Regional companies

- Allison Transmission

- Angi Energy Systems

- Faber Industrie

- Quantum Fuel Systems Technologies

- Swagelok Company

- Trillium CNG

- WEH

- Emerging companies

- Ashok Leyland

- Beijing Tianhai Industry

- Censtar Science &Technology

- Galileo Technologies

- IMPCO Technologies

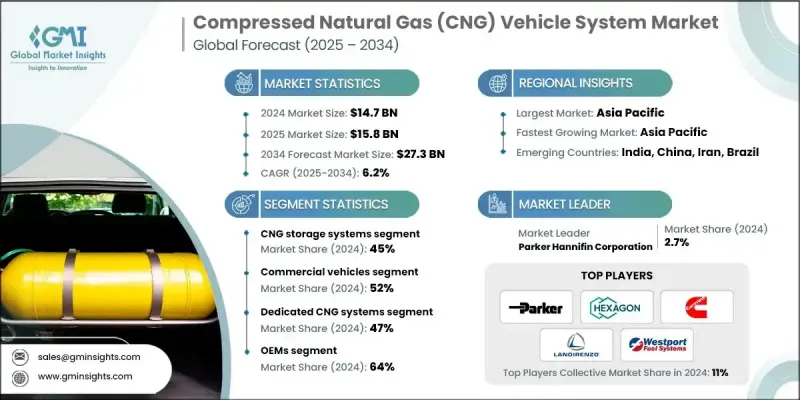

The Global Compressed Natural Gas (CNG) Vehicle System Market was valued at USD 14.7 billion in 2024 and is estimated to grow at a CAGR of 6.2% to reach USD 27.3 billion by 2034.

The market expansion is driven by stringent emission and carbon reduction regulations across major automotive regions, encouraging OEMs and fleet operators to adopt cleaner fuel alternatives such as CNG. Compared to diesel and gasoline vehicles, CNG-powered vehicles emit substantially lower levels of CO2, NOx, and particulate matter, helping manufacturers comply with environmental regulations like Euro 6 and Bharat Stage VI standards for both passenger and commercial vehicles. The cost advantage of CNG further supports market growth, as it costs approximately 30-40% less per kilometer than gasoline or diesel, offering significant savings for fleet operators and cost-conscious consumers. Global crude oil price volatility has prompted governments, particularly in emerging regions, to incentivize CNG adoption as a strategy to reduce fuel import dependence. Investment in CNG refueling and distribution infrastructure is improving accessibility, with public-private partnerships and government-funded initiatives expanding station networks along highways and urban corridors.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $14.7 Billion |

| Forecast Value | $27.3 Billion |

| CAGR | 6.2% |

The CNG storage systems segment generated USD 6.66 billion in 2024 and is expected to reach USD 12.21 billion by 2034. This segment benefits from advances in lightweight composite materials, with research showing potential cost reductions of 30-50% in manufacturing composite tanks.

The dedicated CNG systems segment held a 47% share in 2024 and is projected to grow at a CAGR of 7.8% from 2025 to 2034. These vehicles are popular among fleets and urban transit systems due to their fuel efficiency and low emissions. Although existing CNG infrastructure remains limited, manufacturers are focusing on optimizing engine designs and storage systems to improve reliability, making dedicated systems central to sustainable transportation initiatives.

US Compressed Natural Gas (CNG) Vehicle System Market accounted for a 91% share and generated USD 106.4 million in 2024. While the US represents a smaller portion of the global opportunity, it remains a mature market with limited growth compared to regions focusing heavily on alternative fuels, largely due to the country's abundant petroleum resources.

Key players operating in the Compressed Natural Gas (CNG) Vehicle System Market include Westport Fuel Systems, Parker Hannifin, Hexagon Composites, Clean Energy Fuels, Cummins, BRC Gas, Galileo Technologies, Luxfer, Landi Renzo, and Worthington Industries. Companies in the Compressed Natural Gas (CNG) Vehicle System Market are employing multiple strategies to strengthen their position and expand market share. They are investing in research and development to enhance engine efficiency, storage capacity, and fuel system durability. Strategic collaborations with automotive OEMs allow seamless integration of CNG systems into new vehicle models. Firms are expanding their global distribution networks, establishing partnerships with fueling infrastructure providers, and supporting government initiatives for cleaner transportation.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 System

- 2.2.4 Vehicle

- 2.2.5 End Use

- 2.3 TAM analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook

- 2.6 Strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Stringent emission regulations

- 3.2.1.2 Rising fuel cost differentials

- 3.2.1.3 Expanding refueling infrastructure

- 3.2.1.4 OEMs integration and technological advancements

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Limited refueling infrastructure in emerging regions

- 3.2.2.2 High initial conversion and storage costs

- 3.2.3 Market opportunities

- 3.2.3.1 Government subsidies and incentives

- 3.2.3.2 Fleet electrification-hybrid integration

- 3.2.3.3 Growing urban public transport demand

- 3.2.3.4 Lightweight composite cylinder development

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.7.3 Technology readiness & maturity assessment

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Production statistics

- 3.9.1 Production hubs

- 3.9.2 Consumption hubs

- 3.9.3 Export and import

- 3.10 Cost breakdown analysis

- 3.11 Patent analysis

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint considerations

- 3.14 Business model analysis

- 3.14.1 Equipment sales vs leasing models

- 3.14.2 Service and maintenance revenue streams

- 3.14.3 Infrastructure-as-a-service models

- 3.14.4 Fuel supply contract structures

- 3.15 End Use survey insights & requirements

- 3.16 Risk assessment & mitigation strategies

- 3.16.1 Technology risk analysis

- 3.16.2 Market risk factors

- 3.16.3 Regulatory risk assessment

- 3.16.4 Supply chain risk evaluation

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

- 4.7 Product and service benchmarking

- 4.8 R&D investment analysis

- 4.9 Vendor selection criteria

Chapter 5 Market Estimates & Forecast, By Product, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 CNG storage systems

- 5.2.1 Type I (Steel)

- 5.2.2 Type II (Steel+composite)

- 5.2.3 Type III (Aluminum+composite)

- 5.2.4 Type IV (Full composite)

- 5.3 Fuel delivery systems

- 5.3.1 Pressure regulators

- 5.3.2 Fuel injectors

- 5.3.3 Electronic control units

- 5.3.4 Fuel lines & fittings

- 5.4 Conversion kits

- 5.4.1 Complete retrofit systems

- 5.4.2 Bi-fuel conversion kits

- 5.4.3 Dedicated CNG systems

- 5.5 Other components

- 5.5.1 Safety systems

- 5.5.2 Gauges & indicators

- 5.5.3 Installation accessories

Chapter 6 Market Estimates & Forecast, By System, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Dedicated CNG systems

- 6.3 Bi-fuel (CNG/Gasoline) systems

- 6.4 Dual-fuel (CNG/Diesel) systems

Chapter 7 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Passenger cars

- 7.2.1 Sedan

- 7.2.2 SUV

- 7.2.3 Hatchback

- 7.3 Commercial vehicles

- 7.3.1 Light commercial vehicles (LCV)

- 7.3.2 Heavy commercial vehicles (HCV)

- 7.3.3 Medium commercial vehicles (MCV)

- 7.4 Off-highway vehicles

Chapter 8 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 OEMs (Original equipment manufacturer)

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Nordics

- 9.3.7 Russia

- 9.3.8 Poland

- 9.3.9 Romania

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Vietnam

- 9.4.7 Indonesia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

- 9.6.4 Iran

Chapter 10 Company Profiles

- 10.1 Global companies

- 10.1.1 BRC Gas

- 10.1.2 Chart Industries

- 10.1.3 Clean Energy Fuel

- 10.1.4 Cummins

- 10.1.5 Hexagon Composites

- 10.1.6 Landi Renzo

- 10.1.7 Luxfer

- 10.1.8 Parker Hannifin

- 10.1.9 Westport Fuel Systems

- 10.1.10 Worthington Industries

- 10.2 Regional companies

- 10.2.1 Allison Transmission

- 10.2.2 Angi Energy Systems

- 10.2.3 Faber Industrie

- 10.2.4 Quantum Fuel Systems Technologies

- 10.2.5 Swagelok Company

- 10.2.6 Trillium CNG

- 10.2.7 WEH

- 10.3 Emerging companies

- 10.3.1 Ashok Leyland

- 10.3.2 Beijing Tianhai Industry

- 10.3.3 Censtar Science & Technology

- 10.3.4 Galileo Technologies

- 10.3.5 IMPCO Technologies