|

시장보고서

상품코드

1876575

차량 내 웰니스 모니터링 시스템 시장 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2025-2034년)In-Car Wellness Monitoring System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

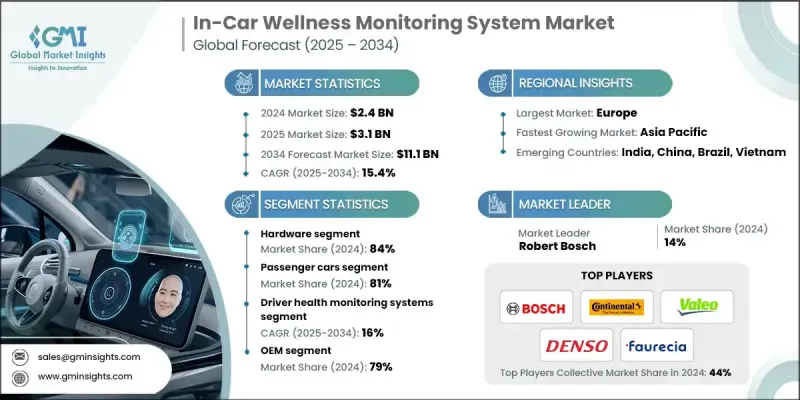

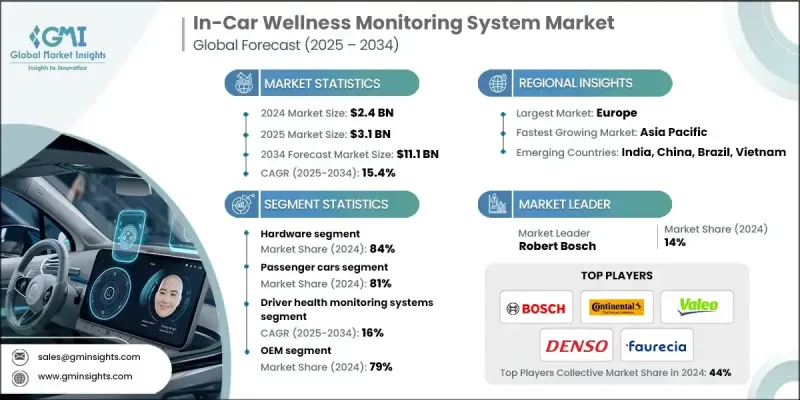

세계의 차량 내 웰니스 모니터링 시스템 시장은 2024년 24억 달러로 평가되었으며, 2034년까지 연평균 복합 성장률(CAGR) 15.4%를 나타내 111억 달러에 이를 것으로 예측됩니다.

차량에 센서, 카메라, AI 기술이 탑재되어 심박수, 피로도, 스트레스 수준 등 중요한 건강 지표를 추적하는 사례가 증가하고 있기 때문에 시장이 급속히 확대되고 있습니다. 차재 안전에 대한 소비자의 의식의 높아짐과, 선진적인 커넥티드 기능이나 고급차 장비의 보급이, 이 성장을 뒷받침하고 있습니다. AI 구동형 모니터링 솔루션은 첨단 컴퓨터 비전 알고리즘을 활용하여 95% 이상의 감지 정확도를 실현하여 안전 기능 이상의 가치를 제공합니다. 여러 센서를 통합함으로써 이러한 시스템은 생리적 신호, 환경 조건, 행동 패턴을 평가하고 탑승자의 건강, 편안함, 각성을 모니터링하는 종합적인 웰빙 생태계를 구축합니다. 적외선 카메라, 생체인식센서, 멀티센서 구성이 활용되어 바이탈 사인, 자세, 스트레스를 실시간으로 추적합니다. 이러한 기술은 스마트 조종석 구조에 통합되는 케이스가 증가하고 있으며, 사전 액티브 운전 지원, 적응형 에어컨 제어, 개인화된 편안함 설정을 실현하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 가치 | 24억 달러 |

| 예측 금액 | 111억 달러 |

| CAGR | 15.4% |

차량 탑재 시스템이 웨어러블 디바이스 및 모바일 헬스 플랫폼과 연동하여 지속적인 건강 모니터링과 클라우드 기반 분석을 가능하게 하여 생태계를 더욱 강화할 수 있습니다. 자율주행 차량의 보급과 함께, 특히 차량이 부분적인 제어를 담당하는 상황에서 웰빙 모니터링은 안전과 정서적 안정성을 유지하는데 중요한 역할을 합니다.

하드웨어 부문은 2024년에 84%의 점유율을 차지했으며 2025년부터 2034년에 걸쳐 CAGR 15.6%를 나타낼 것으로 예측됩니다. 고해상도 카메라, 적외선 센서, 캐빈 감시 광학 기기가 하드웨어 분야를 주도하는 반면, 레이더 기반 센서는 웨어러블 기기 없이 심박수, 호흡 패턴, 미세한 움직임을 비접촉으로 감시합니다. 보쉬를 비롯한 기업은 차내 건강 모니터링을 위한 AI 강화형 레이더 솔루션을 제공합니다.

운전자 건강 모니터링 시스템 부문은 2024년에 39.2%의 점유율을 차지하며 안전성, 규제 준수 및 OEM 채용에 중요한 역할을 부각했습니다. 이러한 시스템은 피로를 감지하고 주의력을 추적하며 심장마비와 뇌졸중과 같은 의료 응급 상황을 확인합니다. 고급 운전자 모니터링 솔루션은 생리적 감지를 통합하여 심박수, 스트레스, 생체 신호 측정을 통해 실시간 건강 평가를 가능하게 합니다.

독일 차량 내 웰니스 모니터링 시스템 시장은 2025년부터 2034년까지 연평균 복합 성장률(CAGR) 14.3%를 나타낼 것으로 예측됩니다. 이 나라의 주도적 입장은 강력한 자동차 제조 부문과 운전자 안전에 대한 노력에 기인합니다. 아우디나 BMW 등의 주요 자동차 업체들은 생체인증 센서, 운전자의 주의력 추적, 감정 인식 등 AI 구동 웰니스 모니터를 통합하여 탑승자의 건강 증진을 도모하고 있습니다. 이러한 기술은 전기화, 커넥티드, 반자동 운전 차량의 보급과 함께 개인화된 건강에 중점을 둔 운전 경험에 대한 수요에 부응합니다.

세계의 차량 내 웰니스 모니터링 시스템 시장에서 사업을 전개하고 있는 주요 기업으로는 Continental, Faurecia, Robert Bosch, Aptiv, Denso, Valeo, Seeing Machines, Smart Eye, Tata Elxsi, Gentex 등이 있습니다. 차량 내 웰니스 모니터링 시스템 시장의 기업은 그 존재와 시장의 지위를 강화하기 위해 몇 가지 전략을 개발하고 있습니다. 공급자는 감지의 정확성과 신뢰성을 높이기 위해 AI, 컴퓨터 비전 및 다중 센서 기술에 많은 투자를 하고 있습니다. 자동차 OEM과의 전략적 파트너십을 통해 웰빙 솔루션을 신차 모델에 원활하게 통합할 수 있습니다. 또한 기업은 클라우드 분석 및 모바일 헬스 플랫폼에 차량을 연결하는 소프트웨어 하드웨어 생태계에 주력하고 있으며 지속적인 건강 모니터링을 제공합니다.

자주 묻는 질문

목차

제1장 조사 방법

- 시장 범위와 정의

- 조사 설계

- 조사 접근

- 데이터 수집 방법

- 데이터 마이닝의 출처

- 세계

- 지역별/국가별

- 기본 추정치와 계산

- 기준연도 계산

- 시장 추정에서의 주요 동향

- 1차 조사 및 검증

- 1차 정보

- 예측 모델

- 조사의 전제조건과 제한 사항

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률 분석

- 비용 구조

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 파괴적 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 운전자의 안전과 건강에 대한 주목 증가

- AI, IoT 및 고급 센서의 통합

- 정부의 안전규제와 의무화

- 고급차 및 프리미엄차에 있어서 보급 확대

- 웨어러블 기기 및 모바일 디바이스와의 기술적 융합

- 업계의 잠재적 위험 및 과제

- 시스템 비용의 높이와 통합의 복잡성

- 데이터 프라이버시와 보안에 대한 우려

- 시장 기회

- 상용차 및 플릿 차량에의 전개

- 자율주행차 및 준자동운전차의 성장

- 웨어러블 디바이스 및 모바일 헬스 플랫폼과의 제휴

- AI 구동형 예측 건강 분석의 개발

- 성장 가능성 분석

- 규제 상황

- Porter's Five Forces 분석

- PESTEL 분석

- 기술과 혁신 동향

- 현재의 기술 동향

- 신흥기술

- 기술 성숙도와 도입 라이프사이클 분석

- 기술 성숙도(TRL) 평가

- 시장 부문별 보급 곡선

- 파괴적 혁신 보급 패턴

- 시장 침투율 예측

- 가격 분석과 비용 구조의 동향

- 과거 가격 동향 분석(2021-2024)

- 부품별 비용 내역

- 제조 비용 구조 분석

- R&D 투자가 가격 설정에 미치는 영향

- 수량 기준 가격 설정 전략

- 비용편익 및 투자이익률(ROI) 분석

- 총소유비용(TCO) 모델

- 투자이익률(ROI)의 산출

- 투자회수기간 분석

- 경제적 영향 평가

- 특허 분석

- 지속가능성과 환경적 측면

- 지속가능한 실천

- 폐기물 감축 전략

- 생산에 있어서 에너지 효율

- 환경에 배려한 대처

- 탄소발자국에 관한 고려 사항

- 무역 분석

- 관세·무역정책의 영향

- 공급망의 현지화 동향

- 지역별 제조 거점

- 사용자 체험과 인체공학

- 운전자의 수용도와 보급률

- 사용성 테스트 및 사용자 인터페이스 설계

- 프라이버시에 대한 인식과 소비자의 우려

- 경고 피로 관리

- 시스템 설계에 있어서 행동 심리학

- 사이버 보안 및 데이터 프라이버시의 틀

- 보험과 플릿 관리의 통합

- OEM과 애프터마켓 생태계 사이의 역학

- 건강 데이터의 상호 운용성 기준

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

- 주요 발전

- 인수 및 합병

- 파트너십 및 협력

- 신제품 발매

- 사업 확장 계획과 자금 조달

제5장 시장 추계·예측 : 구성 요소별(2021-2034년)

- 주요 동향

- 하드웨어

- 센서

- 카메라

- 스티어링 휠 및 시트 센서

- 제어 장치 및 프로세서

- 소프트웨어

- AI 기반 헬스케어 분석

- 운전자 모니터링 알고리즘

- 데이터 통합 및 경보 시스템

- 서비스

- 클라우드 연결성 및 데이터 관리

- 긴급 지원 및 원격의료 통합

제6장 시장 추계·예측 : 차량별(2021-2034년)

- 주요 동향

- 승용차

- 해치백

- 세단

- SUV

- 상용차

- 소형 상용차

- 중형 상용차

- 대형 상용차

- 전기자동차

제7장 시장 추계·예측 : 시스템별(2021-2034년)

- 주요 동향

- 운전자 건강 모니터링 시스템

- 승객 웰니스 모니터링 시스템

- 차 내 환경 및 편의 모니터링 시스템

- 통합 차량 웰니스 시스템

- 기타

제8장 시장 추계·예측 : 판매 채널별(2021-2034년)

- 주요 동향

- OEM

- 애프터마켓

제9장 시장 추계·예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 북유럽 국가

- 포르투갈

- 크로아티아

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 싱가포르

- 태국

- 인도네시아

- 베트남

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

제10장 기업 프로파일

- 세계의 기업

- Aptiv

- Continental

- Denso

- HARMAN International

- Magna International

- NXP Semiconductors

- Robert Bosch

- Valeo

- 지역 기업

- Antolin

- Faurecia

- Gentex

- LG Electronics

- Panasonic Automotive

- Seeing Machines

- Smart Eye

- Tata Elxsi

- Tobii

- Visteon

- 신흥 기술 혁신 기업

- Affectiva

- Allegro MicroSystems

- Binah.ai

- Cerence

- Cipia

- Guardian Optical Technologies

- Ultraleap

The Global In-Car Wellness Monitoring System Market was valued at USD 2.4 billion in 2024 and is estimated to grow at a CAGR of 15.4% to reach USD 11.1 billion by 2034.

The market is rapidly expanding as vehicles increasingly incorporate sensors, cameras, and AI technologies to track vital health metrics, including heart rate, fatigue, and stress levels. Consumer awareness around in-vehicle safety, combined with the adoption of advanced connected and luxury vehicle features, is fueling this growth. AI-driven monitoring solutions now offer more than safety functions, leveraging sophisticated computer vision algorithms to achieve detection accuracy exceeding 95%. By integrating multiple sensors, these systems assess physiological signals, environmental conditions, and behavioral patterns, creating comprehensive wellness ecosystems that monitor occupant health, comfort, and alertness. Infrared cameras, biometric sensors, and multi-sensor setups are used to track vital signs, posture, and stress in real time. These technologies are increasingly embedded in smart cockpit architectures, enabling proactive driver assistance, adaptive climate control, and personalized comfort settings.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.4 Billion |

| Forecast Value | $11.1 Billion |

| CAGR | 15.4% |

The ecosystem is further strengthened as in-car systems connect with wearable devices and mobile health platforms, enabling continuous health monitoring and cloud-based analytics. With the rise of automated vehicles, wellness monitoring plays a critical role in maintaining both safety and emotional stability, especially during situations where the vehicle assumes partial control.

The hardware segment held an 84% share in 2024 and is expected to grow at a CAGR of 15.6% from 2025 to 2034. High-resolution cameras, infrared sensors, and cabin monitoring optics dominate the hardware segment, while radar-based sensors allow contactless monitoring of heart rate, breathing patterns, and micro-movements without wearables. Bosch, among others, provides radar solutions enhanced by AI for in-cabin health monitoring.

The driver health monitoring systems segment held a 39.2% share in 2024, highlighting its crucial role in safety, regulatory compliance, and OEM adoption. These systems detect fatigue, track attention, and identify medical emergencies such as heart attacks or strokes. Advanced driver monitoring solutions integrate physiological sensing, enabling real-time health assessments through heart rate, stress, and vital sign measurements.

Germany In-Car Wellness Monitoring System Market is projected to grow at a CAGR of 14.3% from 2025 to 2034. The country's leadership stems from its strong automotive manufacturing sector and commitment to driver safety. Leading automakers like Audi and BMW are incorporating AI-driven wellness monitors, including biometric sensors, driver attention tracking, and emotion recognition, to enhance occupant well-being. These technologies align with the increasing adoption of electrified, connected, and semi-autonomous vehicles, catering to the demand for personalized, health-focused driving experiences.

Key companies operating in the Global In-Car Wellness Monitoring System Market include Continental, Faurecia, Robert Bosch, Aptiv, Denso, Valeo, Seeing Machines, Smart Eye, Tata Elxsi, and Gentex. Companies in the In-Car Wellness Monitoring System Market are deploying several strategies to strengthen their presence and market position. Providers are investing heavily in AI, computer vision, and multi-sensor technologies to enhance detection accuracy and reliability. Strategic partnerships with automotive OEMs enable seamless integration of wellness solutions into new vehicle models. Firms are also focusing on software-hardware ecosystems that connect vehicles with cloud analytics and mobile health platforms to offer continuous health monitoring.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Vehicle

- 2.2.4 System

- 2.2.5 Sales Channel

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1.1 Growth drivers

- 3.2.1.2 Rising focus on driver safety and health

- 3.2.1.3 Integration of AI, IoT, and advanced sensors

- 3.2.1.4 Government safety regulations and mandates

- 3.2.1.5 Increasing adoption in luxury and premium vehicles

- 3.2.1.6 Technological convergence with wearables and mobile devices

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High system cost and integration complexity

- 3.2.2.2 Data privacy and security concerns

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion into commercial and fleet vehicles

- 3.2.3.2 Growth in autonomous and semi-autonomous vehicles

- 3.2.3.3 Integration with wearable devices and mobile health platforms

- 3.2.3.4 Development of AI-driven predictive health analytics

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.7.3 Technology maturity & adoption lifecycle analysis

- 3.7.3.1 Technology readiness level (TRL) assessment

- 3.7.3.2 Adoption curve by market segment

- 3.7.3.3 Innovation diffusion patterns

- 3.7.3.4 Market penetration forecasting

- 3.8 Pricing analysis & cost structure dynamics

- 3.8.1 Historical price trend analysis (2021-2024)

- 3.8.2 Cost breakdown by component

- 3.8.3 Manufacturing cost structure analysis

- 3.8.4 R&d investment impact on pricing

- 3.8.5 Volume-based pricing strategies

- 3.9 Cost-benefit & ROI analysis

- 3.9.1 Total cost of ownership (TCO) models

- 3.9.2 Return on investment (ROI) calculations

- 3.9.3 Payback period analysis

- 3.9.4 Economic impact assessment

- 3.10 Patent analysis

- 3.11 Sustainability and environmental aspects

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly Initiatives

- 3.12 Carbon footprint considerations

- 3.13 Trade analysis

- 3.13.1 Tariff & trade policy impact

- 3.13.2 Supply chain localization trends

- 3.13.3 Regional manufacturing hubs

- 3.14 User experience and human factors

- 3.14.1 Driver acceptance and adoption rates

- 3.14.2 Usability testing and user interface design

- 3.14.3 Privacy perception and consumer concerns

- 3.14.4 Alert fatigue management

- 3.14.5 Behavioral psychology in system design

- 3.15 Cybersecurity and data privacy framework

- 3.16 Insurance and fleet management integration

- 3.17 OEM vs. aftermarket ecosystem dynamics

- 3.18 Health data interoperability standards

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 (USD Mn, Units)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 Sensors

- 5.2.2 Cameras

- 5.2.3 Steering wheel and seat sensors

- 5.2.4 Control units and processors

- 5.3 Software

- 5.3.1 AI-based health analytics

- 5.3.2 Driver monitoring algorithms

- 5.3.3 Data integration and alert systems

- 5.4 Services

- 5.4.1 Cloud connectivity and data management

- 5.4.2 Emergency assistance and telehealth integration

Chapter 6 Market Estimates & Forecast, By Vehicle, 2021 - 2034 (USD Mn, Units)

- 6.1 Key trends

- 6.2 Passenger cars

- 6.2.1 Hatchbacks

- 6.2.2 Sedans

- 6.2.3 SUVs

- 6.3 Commercial vehicles

- 6.3.1 Light commercial vehicles

- 6.3.2 Medium commercial vehicles

- 6.3.3 Heavy commercial vehicles

- 6.4 Electric vehicles

Chapter 7 Market Estimates & Forecast, By System, 2021 - 2034 (USD Mn, Units)

- 7.1 Key trends

- 7.2 Driver health monitoring systems

- 7.3 Passenger wellness monitoring systems

- 7.4 In-cabin environment and comfort monitoring systems

- 7.5 Integrated vehicle wellness systems

- 7.6 Others

Chapter 8 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 (USD Mn, Units)

- 8.1 Key trends

- 8.2 OEM

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Mn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.3.8 Portugal

- 9.3.9 Croatia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Singapore

- 9.4.7 Thailand

- 9.4.8 Indonesia

- 9.4.9 Vietnam

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

- 9.6.4 Turkey

Chapter 10 Company Profiles

- 10.1 Global Players

- 10.1.1 Aptiv

- 10.1.2 Continental

- 10.1.3 Denso

- 10.1.4 HARMAN International

- 10.1.5 Magna International

- 10.1.6 NXP Semiconductors

- 10.1.7 Robert Bosch

- 10.1.8 Valeo

- 10.2 Regional Players

- 10.2.1 Antolin

- 10.2.2 Faurecia

- 10.2.3 Gentex

- 10.2.4 LG Electronics

- 10.2.5 Panasonic Automotive

- 10.2.6 Seeing Machines

- 10.2.7 Smart Eye

- 10.2.8 Tata Elxsi

- 10.2.9 Tobii

- 10.2.10 Visteon

- 10.3 Emerging Technology Innovators

- 10.3.1 Affectiva

- 10.3.2 Allegro MicroSystems

- 10.3.3 Binah.ai

- 10.3.4 Cerence

- 10.3.5 Cipia

- 10.3.6 Guardian Optical Technologies

- 10.3.7 Ultraleap