|

시장보고서

상품코드

1876580

이식형 심장 모니터(ICM) 시장 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2025-2034년)Implantable Cardiac Monitor Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

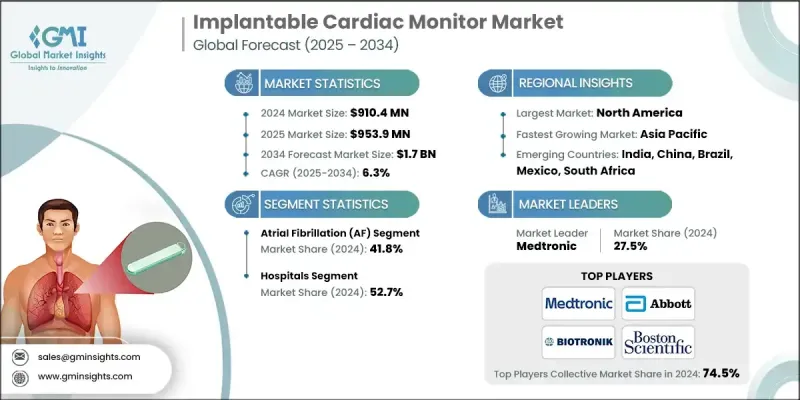

세계의 이식형 심장 모니터(ICM) 시장은 2024년에 9억 1,040만 달러로 평가되었으며, 2034년까지 연평균 복합 성장률(CAGR) 6.3%를 나타내 17억 달러에 이를 것으로 예측됩니다.

심혈관 질환의 유병률 상승, 고령화 인구 증가, 지속적인 원격 심전 모니터링의 필요성 증가가 시장 확대를 이끌고 있습니다. 원격 모니터링 솔루션의 기술적 진보는 환자 결과를 개선하고 적시에 개입할 수 있게 함으로써 성장에 기여하고 있습니다. 이식형 심장 모니터는 병원, 전문 심장 센터, 외래 수술 센터(ASC) 및 의료 기술 기업에 부정맥의 조기 감지 및 임상 워크 플로우의 효율성을 제공하는 고급 솔루션을 제공합니다. 장기 임베디드 루프 레코더, 무선 전송 시스템 및 원격 모니터링 기술을 통해 지속적인 리듬 추적, 조기 진단 및 개별화된 환자 관리가 가능합니다. 세계적인 노화와 함께 만성 심혈관 질환이 더욱 흔해지면서 장기 모니터링 수요가 더욱 증가하고 있습니다. 의료 제공업체와 환자 모두에서 부정맥의 조기 발견과 지속적인 모니터링에 대한 인식 증가가 시장 도입을 촉진하고 있습니다. 소형화된 장치와 무선 연결성도 환자의 컴플라이언스와 임상 효율을 향상시킵니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 기간 | 2025-2034년 |

| 시작 가치 | 9억 1,040만 달러 |

| 예측 금액 | 17억 달러 |

| CAGR | 6.3% |

심방세동부문은 2024년에 41.8%의 점유율을 차지했습니다. 이 주도적 지위는 심방세동의 유병률 상승, 뇌졸중 위험 증가, 조기 진단에 대한 수요에 의해 추진되고 있으며, 이로써 지속적인 이식형 모니터링이 필수적입니다. 심방 세동은 특히 노인과 기초 질환을 가진 심혈관 질환 환자에서 가장 흔한 부정맥으로 남아 있습니다. 장기 모니터링을 통한 조기 발견은 뇌졸중과 심부전을 포함한 심각한 합병증을 예방하는 데 도움이 됩니다.

병원 부문은 52.7%의 점유율을 차지했으며 2025년부터 2034년까지 9억 370만 달러에 달할 것으로 예측됩니다. 병원 부문이 우세한 배경에는 고급 인프라, 전문 순환기과 부문 및 이식 수술을 수행할 수 있는 숙련된 인력이 포함됩니다. 입원 환자에서 부정맥 및 심방 세동의 발생률 증가는 지속적인 모니터링에 대한 수요를 촉진하고 있습니다. 전자 건강 기록 및 원격 모니터링 플랫폼과의 통합은 병원의 효율성과 환자 데이터 관리를 더욱 향상시킵니다.

북미의 이식형 심장 모니터(ICM) 시장은 2024년 35.5%의 점유율을 차지했습니다. 이 지역은 고령층에서 심혈관 질환의 유병률이 높고, 확립된 의료 인프라, 이식형 치료에 대응할 수 있는 병원 및 전문 심장 센터의 광범위한 네트워크의 혜택을 받고 있습니다. 소형화된 루프 레코더, 무선 모니터링 시스템, AI 구동 예측 분석 등의 기술 혁신을 통해 환자의 치료 성과 향상과 업무 효율 개선을 도모하여 이 기술의 채용을 더욱 촉진하고 있습니다.

이식형 심장 모니터(ICM) 시장의 주요 기업으로는 Medtronic, Vectorious Medical Technologies, Abbott, BIOTRONIK, Boston Scientific, AngelMed / Avertix 등이 있습니다. 이식형 심장 모니터(ICM) 시장의 기업은 무선 및 원격 모니터링 기능을 갖춘 소형 에너지 효율적인 장치를 개발하기 위해 R&D에 투자함으로써 존재감을 강화하고 있습니다. 많은 기업들이 ICM 시스템을 임상 워크플로우에 통합하기 위해 병원, 심장병 센터, 기술 공급자와 전략적 제휴를 맺고 있습니다. 또한 신흥 시장에 진입하기 위해 사업 전개 지역과 유통 네트워크의 확대도 진행하고 있습니다. 예측 분석, AI 구동 진단, 실시간 환자 모니터링을 위한 소프트웨어 플랫폼 강화도 또 다른 중요한 전략입니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 업계에 미치는 영향요인

- 성장 촉진요인

- 심부정맥 및 심방세동의 유병률 증가

- 원격 모니터링 및 연결 기술의 발전

- 고령화 인구 증가와 관련된 심장 위험

- 유리한 상환 정책과 조기 진단 프로그램

- 업계의 잠재적 위험 및 과제

- 디바이스 및 이식 수술의 고비용

- 환자 및 일반 개업의에서의 인지도의 낮음

- 시장 기회

- 인공지능 및 예측 분석과의 통합

- 스마트하고 소형화되어 긴 수명의 디바이스 개발

- 성장 촉진요인

- 성장 가능성 분석

- 가격 분석(2024년)

- 판매된 이식형 심장 모니터의 대수(대, 2021-2034년)

- 세계

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- LAMEA

- 기술적 진보

- 현재의 기술 동향

- 장기 심장 모니터링용 소형 이식형 루프 레코더

- 실시간 심리듬 데이터 전송을 가능하게 하는 원격 모니터링 플랫폼

- 환자의 편안함과 치료 효율을 향상시키는 환자에게 사용하기 쉬운 저침습 장치

- 신흥기술

- 조기 진단을 위한 AI 탑재 부정맥 검출 및 예측 분석

- 스마트폰 및 클라우드 플랫폼을 통합한 무선 접속형 이식형 심장 모니터

- 적응형 경보 시스템과 자동화된 의료 종사자 통지 기능을 갖춘 스마트 디바이스

- 현재의 기술 동향

- 갭 분석

- Porter's Five Forces 분석

- PESTEL 분석

- 향후 시장 동향

- AI, 디지털 헬스 및 접속형 심장 디바이스의 융합

- 재택 및 외래 심장 모니터링 솔루션 확대

- 의료 인프라가 개선되고 있는 신흥 시장에서의 성장

제4장 경쟁 구도

- 서론

- 기업 매트릭스 분석

- 기업의 시장 점유율 분석

- 세계

- 북미

- 유럽

- 아시아태평양

- LAMEA

- 경쟁 포지셔닝 매트릭스

- 주요 시장 기업의 경쟁 분석

- 주요 발전

- 인수 및 합병

- 파트너십 및 협력

- 신규 서비스 유형 출시

- 확장 계획

제5장 시장 추계·예측 : 적응증별(2021-2034년)

- 주요 동향

- 심방세동(AF)

- 부정맥

- 서맥

- 빈맥

- 기타 적응증

제6장 시장 추계·예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 병원

- 전문 심장 센터

- 외래 수술 센터(ASC)

- 기타 최종 용도

제7장 시장 추계·예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제8장 기업 프로파일

- Abbott

- AngelMed/Avertix

- BIOTRONIK

- Boston Scientific

- Medtronic

- Vectorious Medical Technologies

The Global Implantable Cardiac Monitor Market was valued at USD 910.4 million in 2024 and is estimated to grow at a CAGR of 6.3% to reach USD 1.7 billion by 2034.

The rising prevalence of cardiovascular diseases, an aging population, and the increasing need for continuous remote cardiac monitoring are driving market expansion. Technological advancements in remote monitoring solutions are also contributing to growth by enhancing patient outcomes and enabling timely intervention. Implantable cardiac monitors provide hospitals, specialized cardiac centers, ambulatory surgical facilities, and health technology companies with advanced solutions to detect arrhythmias early and streamline clinical workflows. Long-term implantable loop recorders, wireless transmission systems, and remote monitoring technologies allow continuous rhythm tracking, early diagnosis, and personalized patient management. With the global population aging, chronic cardiovascular conditions are becoming more common, further increasing demand for long-term monitoring. Greater awareness among healthcare providers and patients regarding early arrhythmia detection and continuous monitoring is boosting market adoption. Miniaturized devices and wireless connectivity have also improved patient compliance and clinical efficiency.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $910.4 Million |

| Forecast Value | $1.7 Billion |

| CAGR | 6.3% |

The atrial fibrillation segment held a 41.8% share in 2024. This leadership is driven by the rising prevalence of AF, heightened stroke risk, and demand for early diagnosis, which makes continuous implantable monitoring essential. Atrial fibrillation remains the most common cardiac arrhythmia, particularly among older adults and patients with underlying cardiovascular disorders. Early detection through long-term monitoring helps prevent serious complications, including stroke and heart failure.

The hospitals segment held a 52.7% share and is expected to reach USD 903.7 million during 2025-2034. Hospitals dominate because of their advanced infrastructure, specialized cardiology departments, and skilled personnel capable of performing implantable procedures. The increasing incidence of arrhythmias and atrial fibrillation among inpatients fuels demand for continuous monitoring. Integration with electronic health records and remote monitoring platforms further enhances hospital efficiency and patient data management.

North America Implantable Cardiac Monitor Market held a 35.5% share in 2024. The region benefits from a high prevalence of cardiovascular conditions among its elderly population, a well-established healthcare infrastructure, and an extensive network of hospitals and specialty cardiac centers equipped for implantable procedures. Adoption is further supported by technological innovations such as miniaturized loop recorders, wireless monitoring systems, and AI-driven predictive analytics, which enhance patient outcomes and improve operational efficiency.

Key players in the Implantable Cardiac Monitor Market include Medtronic, Vectorious Medical Technologies, Abbott, BIOTRONIK, Boston Scientific, and AngelMed / Avertix. Companies in the Implantable Cardiac Monitor Market are strengthening their presence by investing in R&D to develop miniaturized, energy-efficient devices with wireless and remote monitoring capabilities. Many are forming strategic collaborations with hospitals, cardiology centers, and technology providers to integrate their ICM systems into clinical workflows. Companies are also expanding their geographical footprint and distribution networks to access emerging markets. Enhancing software platforms for predictive analytics, AI-driven diagnostics, and real-time patient monitoring is another key strategy.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Indication trends

- 2.2.3 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of cardiac arrhythmias and atrial fibrillation

- 3.2.1.2 Advancements in remote monitoring and connectivity technologies

- 3.2.1.3 Growing geriatric population and associated cardiac risk

- 3.2.1.4 Favorable reimbursement policies and early diagnosis programs

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of devices and implantation procedures

- 3.2.2.2 Limited awareness among patients and general practitioners

- 3.2.3 Market opportunities

- 3.2.3.1 Integration with artificial intelligence and predictive analytics

- 3.2.3.2 Development of smart, miniaturized, and long-life devices

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Pricing analysis, 2024

- 3.5 Number of implantable cardiac monitors sold (Units), 2021 - 2034

- 3.5.1 Global

- 3.5.2 North America

- 3.5.3 Europe

- 3.5.4 Asia Pacific

- 3.5.5 Latin America

- 3.5.6 MEA

- 3.6 Regulatory landscape

- 3.6.1 North America

- 3.6.2 Europe

- 3.6.3 Asia Pacific

- 3.6.4 LAMEA

- 3.7 Technological advancements

- 3.7.1 Current technological trends

- 3.7.1.1 Miniaturized implantable loop recorders for long-term cardiac monitoring

- 3.7.1.2 Remote monitoring platforms enabling real-time heart rhythm data transmission

- 3.7.1.3 Patient-friendly, minimally invasive devices improving comfort and procedural efficiency

- 3.7.2 Emerging technologies

- 3.7.2.1 AI-powered arrhythmia detection and predictive analytics for early diagnosis

- 3.7.2.2 Wireless connected implantable cardiac monitors integrating smartphone and cloud platforms

- 3.7.2.3 Smart devices with adaptive alert systems and automated clinician notifications

- 3.7.1 Current technological trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

- 3.11 Future market trends

- 3.11.1 Convergence of AI, digital health, and connected cardiac devices

- 3.11.2 Expansion of home-based and outpatient cardiac monitoring solutions

- 3.11.3 Growth in emerging markets with improving healthcare infrastructure

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.3.5 LAMEA

- 4.4 Competitive positioning matrix

- 4.5 Competitive analysis of major market players

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New service type launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Indication, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Atrial fibrillation (AF)

- 5.3 Arrhythmia

- 5.4 Bradycardia

- 5.5 Tachycardia

- 5.6 Other indications

Chapter 6 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Hospitals

- 6.3 Specialized cardiac centers

- 6.4 Ambulatory surgical centers

- 6.5 Other end use

Chapter 7 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Netherlands

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Japan

- 7.4.3 India

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.6 Middle East and Africa

- 7.6.1 South Africa

- 7.6.2 Saudi Arabia

- 7.6.3 UAE

Chapter 8 Company Profiles

- 8.1 Abbott

- 8.2 AngelMed / Avertix

- 8.3 BIOTRONIK

- 8.4 Boston Scientific

- 8.5 Medtronic

- 8.6 Vectorious Medical Technologies