|

시장보고서

상품코드

1876636

자동차용 홀로그래픽 디스플레이 반도체 시장 : 시장 기회, 성장 촉진요인, 업계 동향 분석, 예측(2025-2034년)Automotive Holographic Display Semiconductors Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

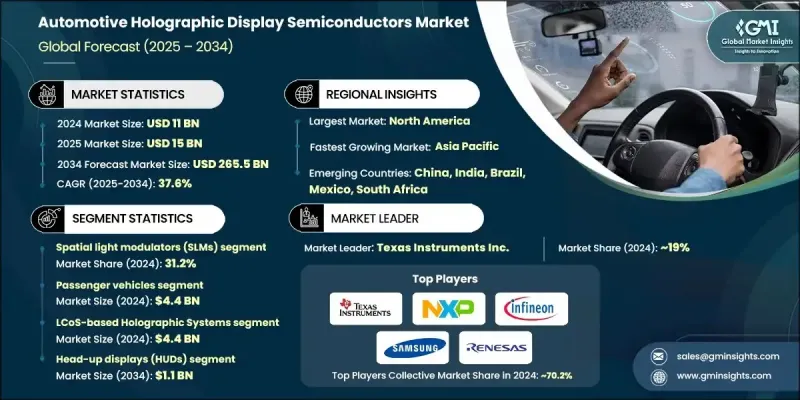

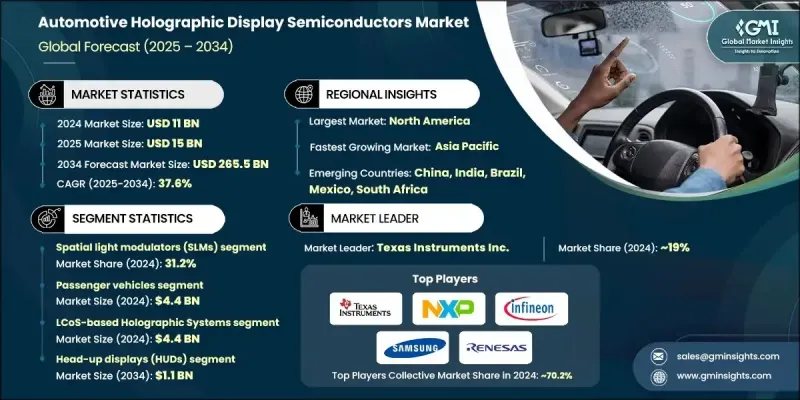

세계의 자동차용 홀로그래픽 디스플레이 반도체 시장은 2024년에 110억 달러로 평가되었고, 2034년까지 연평균 복합 성장률(CAGR) 37.6%로 성장할 전망이며, 2,655억 달러에 이를 것으로 예측됩니다.

자동차의 증강현실(AR) 및 디지털 시각화 기술의 급속한 보급으로 차세대 홀로그래픽 디스플레이 시스템을 구동하는 첨단 반도체에 대한 수요가 가속화되고 있습니다. 자동차 제조업체는 운전 안전성 향상 및 몰입형 인포테인먼트 체험을 실현하기 위해 초고화질 실시간 이미지를 제공할 수 있는 고성능 칩 통합에 주력하고 있습니다. 자동차 산업이 커넥티드카 및 자율주행차로 이동하는 동안 홀로그래픽 디스플레이는 중요한 데이터를 운전자의 시선에 직접 투영하여 상황인식 능력과 종합적인 안전성을 향상시키기 위해 활용되고 있습니다. 이러한 혁신적인 디스플레이 시스템은 복잡한 시각 정보를 즉시 처리하고 동적 조건 하에서도 성능을 유지하는 고성능 반도체에 의존합니다. 스마트모빌리티, 지속가능성, 전기자동차 기술을 추진하는 각국 정부도 반도체의 혁신과 보급을 견인하고 있습니다. 프리미엄 자동차 및 전기자동차의 생산 확대와 미래의 차내 환경을 요구하는 소비자 수요가 증가함에 따라 시장 성장이 계속 강화되고 있습니다. 기술 공급자, 반도체 기업 및 자동차 제조업체 간의 지속적인 협력은 디지털 조종실 경험을 재정의하는 고급 홀로그래픽 디스플레이 시스템의 상용화를 가속화하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 기간 | 2025-2034년 |

| 시작 금액 | 110억 달러 |

| 예측 금액 | 2,655억 달러 |

| CAGR | 37.6% |

디지털 마이크로미러 디바이스(DMD) 부문은 2024년 28억 달러 규모로 평가되었고, 2034년까지 연평균 복합 성장률(CAGR) 39.5%로 성장할 것으로 예측됩니다. DMD 기반 반도체는 탁월한 이미지 정확도, 밝기 및 대비를 제공하며 고성능 홀로그래픽 디스플레이와 헤드업 디스플레이에 필수적인 존재입니다. 이 시스템은 수천 개의 미세 거울을 사용하여 빛을 매우 정확하게 제어하여 선명하고 고해상도 투영을 실현합니다. 다양한 조명 환경에서도 명확성 및 응답성을 유지하는 능력은 운전자의 시인성과 실시간 인식 능력을 향상시킵니다. ADAS(선진운전지원시스템), 내비게이션 시각화, 안전경보를 지원하는 DMD의 전기자동차 및 자율주행차에 대한 통합은 급속히 확대되고 있어, 제조업체가 차세대 자동차 디스플레이 시스템에의 높아지는 기대에 부응하는 도움이 되고 있습니다.

승용차 부문은 2024년 44억 달러 시장 규모를 창출했습니다. 이러한 이점은 첨단 인포테인먼트, 증강현실 인터페이스 및 운전 지원 기술에 대한 소비자 관심 증가로 인한 것입니다. 전기차 및 고급차의 생산 증가에 따라 효율적인 전력 관리와 고품질의 시각 출력을 제공하는 홀로그래픽 디스플레이 반도체에 대한 수요가 더욱 높아지고 있습니다. 제조업체는 성능과 저렴한 가격의 균형을 이루기 위해 승용차용으로 특별히 설계된 비용 효율적이고 에너지 최적화된 반도체 솔루션 개발에 주력하고 있습니다. 자동차 내부의 몰입형 인터랙티브 디지털 디스플레이에 대한 수요는 계속 증가하고 있으며, 자동차 업계 전체의 사용자 경험 기준을 재구성하고 있습니다.

북미의 자동차용 홀로그래픽 디스플레이 반도체 시장은 2024년 28.2%의 점유율을 차지했습니다. 이 지역 시장은 급속한 기술 혁신, 전기자동차의 보급 확대, 증강현실 헤드업 디스플레이의 조기 통합 등의 이점을 누리고 있습니다. 연구개발에 대한 엄청난 투자, 커넥티드 모빌리티를 촉진하는 정부 시책, 주요 반도체 제조업체의 존재가 시장의 꾸준한 확대를 지원하고 있습니다. 이 지역의 자동차 업계는 홀로그래픽 디스플레이 시스템을 경쟁 차별화 요인으로 활용하여 커넥티드 자동차의 안전성, 운전자 인지도 및 엔터테인먼트 기능 향상에 주력하고 있습니다.

세계의 자동차용 홀로그래픽 디스플레이 반도체 시장을 형성하는 주요 기업은 Synaptics Incorporated, Samsung Electronics Co., Ltd., Texas Instruments Inc., Himax Technologies, Inc., NXP Semiconductors NV, Renesas Electronics Corporation, ROHM Semiconductor, Infineon Technologies AG, Magnachip Semiconductor Corporation, Novatek Microelectronics Corp.、ON Semiconductor Corporation、Raydium Semiconductor Corporation、LX Semicon Co., Ltd.、FocalTech Systems Co., Ltd.、ams OSRAM AG、Valens Semiconductor Ltd.、Appotronics Co., Ltd.、Ceres Holographics Ltd.、Envisics Ltd. 등이 있습니다. 자동차용 홀로그래픽 디스플레이 반도체 시장의 주요 기업들은 이미지 정밀도, 에너지 효율, 통합 능력 향상에 중점을 둔 혁신 주도 전략을 추진하고 있습니다. 많은 기업들이 증강현실(AR) 및 실시간 3D 시각화에 최적화된 반도체 아키텍처 개발을 위해 연구 개발(R&D)에 많은 투자를 하고 있습니다. 자동차 제조업체나 기술 개발 기업과의 제휴에 의해 차세대 차량에 있어서 제품 테스트 및 도입이 가속하고 있습니다. 또한 헤드업 디스플레 및 홀로그래픽 표시 시스템에 사용되는 고속, 저소비전력 칩 수요 증가에 대응하기 위해 각사는 제조 능력의 확충에도 임하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

- 업계 생태계 분석

- 업계에 미치는 영향요인

- 성장 촉진요인

- 드라이버의 안전성 및 내비게이션 시각화 향상을 위한 증강현실(AR) 헤드업 디스플레이(HUD)의 채용 확대

- 고급 디지털 시스템을 탑재한 프리미엄 자동차 및 전기자동차에 대한 수요 증가

- 디스플레이 성능 및 에너지 효율을 향상시키고 있는 반도체 설계에 있어서 지속적인 기술 진보

- 몰입형으로 미래적인 차내 체험에 대한 소비자 선호의 고조

- 업계의 잠재적 리스크 및 과제

- 홀로그래픽 디스플레이 반도체와 관련된 높은 생산 비용 및 통합 비용

- 컴팩트 차량 대시보드의 열 관리 및 소형화에 관한 과제

- 시장 기회

- 차세대 AR 및 3D 디스플레이 시스템용 에너지 절약 반도체 재료 개발

- 예측 항행 및 안전 경보를 위한 AI 구동형 홀로그래픽 가시화의 통합

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 미국

- 캐나다

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 북미

- 기술 동향

- 현재의 동향

- 신흥 기술

- 파이프라인 분석

- 장래 시장 동향

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서문

- 기업의 시장 점유율 분석

- 세계

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병 및 인수

- 제휴 및 협력 관계

- 신제품 발매

- 확대 계획

제5장 시장 추계 및 예측 : 반도체 디바이스 유형별(2021-2034년)

- 주요 동향

- 공간 광 변조기(SLMs)

- 디지털 마이크로 미러 디바이스(DMD)

- 반도체 프로세싱

- 드라이버 집적 회로

- 전원 관리 IC

제6장 시장 추계 및 예측 : 차량 유형별(2021-2034년)

- 주요 동향

- 승용차

- 상용차

- 자율주행차

제7장 시장 추계 및 예측 : 홀로그래픽 기술 유형별(2021-2034년)

- 주요 동향

- LCoS 기반 홀로그래픽 시스템

- DLP 기반 홀로그래픽 시스템

- 메타서피스 기반 시스템

- 도파로 통합 시스템

제8장 시장 추계 및 예측 : 용도별(2021-2034년)

- 주요 동향

- 헤드업 디스플레이(HUD)

- 계기 클러스터 디스플레이

- 인포테인먼트 시스템

제9장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 네덜란드

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제10장 기업 프로파일

- Texas Instruments Inc.

- NXP Semiconductors NV

- Renesas Electronics Corporation

- Samsung Electronics Co., Ltd.

- Himax Technologies, Inc.

- ROHM Semiconductor

- Infineon Technologies AG

- Synaptics Incorporated

- Magnachip Semiconductor Corporation

- Novatek Microelectronics Corp.

- ON Semiconductor Corporation

- Raydium Semiconductor Corporation

- LX Semicon Co., Ltd.

- FocalTech Systems Co., Ltd.

- ams OSRAM AG

- Valens Semiconductor Ltd.

- Ceres Holographics Ltd.

- Appotronics Co., Ltd.

- Envisics Ltd.

The Global Automotive Holographic Display Semiconductors Market was valued at USD 11 billion in 2024 and is estimated to grow at a CAGR of 37.6% to reach USD 265.5 billion by 2034.

The rapid adoption of augmented reality and digital visualization technologies in vehicles is accelerating demand for advanced semiconductors that power next-generation holographic display systems. Automakers are increasingly focusing on integrating high-performance chips capable of delivering ultra-clear, real-time images for enhanced driver safety and immersive infotainment experiences. As the automotive industry transitions toward connected and autonomous vehicles, holographic displays are being used to project critical data directly within the driver's line of sight, improving situational awareness and overall safety. These innovative display systems rely on powerful semiconductors that process complex visual information instantly and maintain performance under dynamic conditions. Governments promoting smart mobility, sustainability, and electric vehicle technologies are also driving semiconductor innovation and adoption. The expansion of premium and electric vehicle production, combined with growing consumer demand for futuristic in-car environments, continues to strengthen market growth. Ongoing collaboration between technology providers, semiconductor companies, and automotive manufacturers is accelerating the commercialization of advanced holographic display systems that redefine the digital cockpit experience.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $11 Billion |

| Forecast Value | $265.5 Billion |

| CAGR | 37.6% |

The digital micromirror devices (DMDs) segment accounted for USD 2.8 billion in 2024 and is anticipated to grow at a CAGR of 39.5% through 2034. DMD-based semiconductors deliver exceptional image precision, brightness, and contrast, making them integral to high-performance holographic and head-up displays. These systems employ thousands of microscopic mirrors to manipulate light with extreme accuracy, resulting in vivid and high-resolution projections. Their ability to maintain clarity and responsiveness in diverse lighting environments enhances driver visibility and real-time awareness. The integration of DMDs into electric and autonomous vehicles is expanding rapidly as they support advanced driver assistance, navigation visualization, and safety alerts, helping manufacturers meet growing expectations for next-level automotive display systems.

The passenger vehicle segment generated USD 4.4 billion in 2024. This dominance is attributed to rising consumer interest in advanced infotainment, augmented reality interfaces, and driver assistance technologies. The increasing production of electric and luxury cars is further elevating the need for holographic display semiconductors that provide efficient power management and premium visual output. Manufacturers are emphasizing the development of cost-effective, energy-optimized semiconductor solutions specifically designed for passenger vehicles to balance performance and affordability. The demand for immersive, interactive digital displays inside vehicles continues to rise, reshaping user experience standards across the automotive industry.

North America Automotive Holographic Display Semiconductors Market held a share of 28.2% in 2024. The regional market benefits from rapid technological innovation, strong electric vehicle adoption, and early integration of augmented reality head-up displays. High investment in R&D, government initiatives promoting connected mobility, and the presence of prominent semiconductor producers are supporting steady market expansion. The region's automotive sector is leveraging holographic display systems as a competitive differentiator, focusing on enhancing safety, driver awareness, and entertainment capabilities within connected vehicles.

Key players shaping the Global Automotive Holographic Display Semiconductors Market include Synaptics Incorporated, Samsung Electronics Co., Ltd., Texas Instruments Inc., Himax Technologies, Inc., NXP Semiconductors N.V., Renesas Electronics Corporation, ROHM Semiconductor, Infineon Technologies AG, Magnachip Semiconductor Corporation, Novatek Microelectronics Corp., ON Semiconductor Corporation, Raydium Semiconductor Corporation, LX Semicon Co., Ltd., FocalTech Systems Co., Ltd., ams OSRAM AG, Valens Semiconductor Ltd., Appotronics Co., Ltd., Ceres Holographics Ltd., and Envisics Ltd. Leading companies in the Automotive Holographic Display Semiconductors Market are pursuing innovation-driven strategies focused on enhancing image precision, energy efficiency, and integration capabilities. Many are investing heavily in R&D to develop semiconductor architectures optimized for augmented reality and real-time 3D visualization. Collaborations with automakers and technology developers are accelerating product testing and deployment in next-generation vehicles. Companies are also expanding manufacturing capacity to meet growing demand for high-speed, low-power chips used in head-up and holographic display systems.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional Trends

- 2.2.2 Semiconductor Device Type Trends

- 2.2.3 Vehicle Type Trends

- 2.2.4 Holographic Technology Type Trends

- 2.2.5 Application Trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing Adoption of Reality (AR) Head-Up Displays (HUDs) for Improved Driver Safety and Navigation Visualization.

- 3.2.1.2 Rising Demand for Premium and Electric Vehicles Equipped with Advanced Digital Systems.

- 3.2.1.3 Continuous Technological Advancements in Semiconductor Design Enhancing Display Performance and Energy Efficiency.

- 3.2.1.4 Increasing Consumer Preference for Immersive and Futuristic In-Car Experiences.

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High Production and Integration Costs Associated with Holographic Display Semiconductors.

- 3.2.2.2 Thermal Management and Miniaturization Issues in Compact Vehicle Dashboards.

- 3.2.3 Market opportunities

- 3.2.3.1 Development of Energy-efficient Semiconductor Materials for Next-Generation AR and 3D Display Systems.

- 3.2.3.2 Integration of AI-driven Holographic Visualization for Predictive Navigation and Safety Alerts.

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 U.S.

- 3.4.1.2 Canada

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.4.1 North America

- 3.5 Technology landscape

- 3.5.1 Current trends

- 3.5.2 Emerging technologies

- 3.6 Pipeline analysis

- 3.7 Future market trends

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 Global

- 4.2.2 North America

- 4.2.3 Europe

- 4.2.4 Asia Pacific

- 4.2.5 Latin America

- 4.2.6 Middle East and Africa

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Semiconductor Device Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Spatial Light Modulators (SLMs)

- 5.3 Digital Micromirror Devices (DMDs)

- 5.4 Processing Semiconductors

- 5.5 Driver Integrated Circuits

- 5.6 Power Management ICs

Chapter 6 Market Estimates and Forecast, By Vehicle Type, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Passenger Vehicles

- 6.3 Commercial Vehicles

- 6.4 Autonomous Vehicles

Chapter 7 Market Estimates and Forecast, By Holographic Technology Type, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 LCoS-based Holographic Systems

- 7.3 DLP-based Holographic Systems

- 7.4 Metasurface-based Systems

- 7.5 Waveguide-integrated Systems

Chapter 8 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Head-Up Displays (HUDs)

- 8.3 Instrument Cluster Displays

- 8.4 Infotainment Systems

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Texas Instruments Inc.

- 10.2 NXP Semiconductors N.V.

- 10.3 Renesas Electronics Corporation

- 10.4 Samsung Electronics Co., Ltd.

- 10.5 Himax Technologies, Inc.

- 10.6 ROHM Semiconductor

- 10.7 Infineon Technologies AG

- 10.8 Synaptics Incorporated

- 10.9 Magnachip Semiconductor Corporation

- 10.10 Novatek Microelectronics Corp.

- 10.11 ON Semiconductor Corporation

- 10.12 Raydium Semiconductor Corporation

- 10.13 LX Semicon Co., Ltd.

- 10.14 FocalTech Systems Co., Ltd.

- 10.15 ams OSRAM AG

- 10.16 Valens Semiconductor Ltd.

- 10.17 Ceres Holographics Ltd.

- 10.18 Appotronics Co., Ltd.

- 10.19 Envisics Ltd.