|

시장보고서

상품코드

1876646

산후 출혈 관리 기기 시장 : 시장 기회, 성장 촉진요인, 업계 동향 분석, 예측(2025-2034년)Postpartum Hemorrhage Management Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

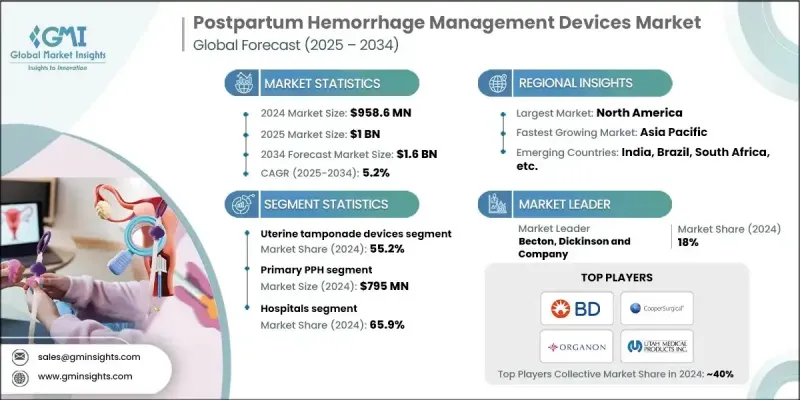

세계의 산후 출혈 관리 기기 시장은 2024년에 9억 5,860만 달러로 평가되었고, 2034년까지 연평균 복합 성장률(CAGR) 5.2%로 성장할 전망이며, 16억 달러에 이를 것으로 예측됩니다.

산후 출혈의 세계적인 발생률이 증가하고 모체 건강에 대한 의식이 높아짐에 따라 업계는 계속 발전하고 있습니다. 또한 의료기기 혁신의 급속한 진전, 긴급 산과 의료 이용 확대, 출산 합병증 예방에 초점을 맞춘 계발 활동의 강화도 수요에 영향을 미치고 있습니다. 이러한 노력은 모체 케어 기술에 대한 액세스 확대, 의료 시스템과의 제휴 강화, 전체적인 도입 촉진을 통해 제조업체에게 보다 지원적인 환경 만들기에 공헌하고 있습니다. 향후 수년간 AI 구동형 분석 툴, 디지털 접속성, 휴대형 기기 및 기타 기술적 개선의 통합이 진행됨에 따라 개발이 가속될 것으로 예측됩니다. 산후 출혈 관리 기기는 분만 후 과도한 출혈을 제어하고 산과 긴급 상황에서 임산부 사망률을 줄이는 데 기여하도록 설계되었습니다. 임상 팀은 효율성, 저침습성, 입증된 효과로부터 자궁 풍선 시스템에 대한 의존도를 높이고 있습니다. 뛰어난 안전성 실적과 신뢰성이 높은 성능으로 세계 의료시설에서의 채용이 계속 확대되고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 기간 | 2025-2034년 |

| 시작 금액 | 9억 5,860만 달러 |

| 예측 금액 | 16억 달러 |

| CAGR | 5.2% |

자궁 탐포나데 부문은 자궁 무력증 및 빈혈과 같은 질병의 높은 발생률과 임산부의 결과 개선을 목적으로 한 정부 시책에 힘입어 2024년에 55.2%의 점유율을 차지했습니다. 이러한 기기는 심각한 출혈을 관리하기 위해 자궁에 압력을 가하고 환자의 상태를 신속하게 안정화하면서 외과적 치료의 필요성을 줄일 수 있습니다.

2차 성산후 출혈 부문은 2024년 1억 6,360만 달러 규모로 평가되었습니다. 출산 후 24시간 이상 경과한 후 12주 이내에 발생하는 출혈로 정의되는 이 형태의 출혈은 일반적으로 감염, 잔존 조직 또는 치유 지연과 관련이 있습니다. 진단용 화상 검사나 자궁 수축 촉진제를 이용한 치료, 혹은 외과적 처치가 필요한 경우가 많습니다. 1차 산후 출혈만큼 빈도는 높지 않지만, 2차 성산후 출혈은 보다 복잡한 결과로 이어지기 쉽고, 장기적인 모체 건강 계획 및 예방 의료 전략의 중요성을 부각시키고 있습니다.

미국의 산후 출혈 관리 기기 시장 규모는 2024년 3억 3,080만 달러에 달했습니다. 이 나라의 산후 출혈의 높은 발생률은 제품 수요를 지속적으로 밀어 올리고 있습니다. 미국은 강력한 규제 감독, 널리 발달된 병원 시스템, 임산부 건강에 대한 우선순위에 대한 광범위한 인식을 통해 PPH 기기의 도입을 이끌고 추진하는 국가 중 하나입니다. 임산부 케어에 대한 공적 노력과 민간 투자는 이러한 장비에 대한 접근을 확대하고 새로운 혁신을 촉진하고 있습니다.

주요 산후 출혈 관리 기기 시장 시장 진출기업으로는 Becton, Dickinson and Company, PREGNA INTERNATIONAL, CooperSurgical, SINAPI, CELOX MEDICAL, ORGANON, STERIMED, ZOEX NIASG, 3rd Stone Design, UTAH MEDICAL PRODUCTS, INC., MedGyn 등이 있습니다. 산후 출혈 관리 기기 시장에서 경쟁하는 기업은 세계 지위를 강화하기 위해 몇 가지 전략적 행동에 주력하고 있습니다. 많은 기업들이 신뢰성, 휴대성 및 환자 안전을 향상시키기 위한 고급 제품 엔지니어링에 투자하고 있습니다. 각 조직은 신속한 도입과 개입 위험을 줄이는 새로운 장치 설계를 도입하기 위해 연구개발 프로그램을 확대하고 있습니다. 병원과 임산부 케어 네트워크와의 관계를 강화하는 것은 선진국 및 신흥국에서의 유통 확대와 함께 우선 순위가 계속되고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

- 업계 생태계 분석

- 업계에 미치는 영향요인

- 성장 촉진요인

- 세계적으로 증가하는 산후 출혈의 유병률

- 임산부 사망률에 관한 계발 활동 증가

- PPH 관리 장치의 기술적 진보

- 업계의 잠재적 리스크 및 과제

- 자원이 한정된 환경에 있어서 기기에 대한 액세스 제한

- 신규 의료기기 승인에 있어서 규제 상의 지연

- 기회

- 예측적 임산부 건강 분석을 위한 AI 통합

- 임산부 보건 프로그램에 대한 자금 증액

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 기술 및 혁신 동향

- 현재의 기술 동향

- 신흥 기술

- 투자 환경

- 가격 분석(2024년)

- 상환 시나리오

- 지속가능성 및 환경에 대한 배려

- 임상적 증거 및 결과 분석

- Porter's Five Forces 분석

- PESTEL 분석

- 갭 분석

- 장래 시장 동향

제4장 경쟁 구도

- 서문

- 기업 매트릭스 분석

- 기업의 시장 점유율 분석

- 세계

- 북미

- 유럽

- 아시아태평양

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병 및 인수

- 제휴 및 협업

- 신제품 발매

- 확대 계획

제5장 시장 추계 및 예측 : 제품 유형별(2021-2034년)

- 주요 동향

- 자궁 탐포나데 기기

- 풍선 탐포나데

- 진공 유도식 기기

- 비공기식 쇼크 방지 의(NASG)

- 프리필드 주사 시스템

제6장 시장 추계 및 예측 : 환자 유형별(2021-2034년)

- 주요 동향

- 원발성 PPH

- 2차성 PPH

제7장 시장 추계 및 예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 병원

- 산과 및 분만 센터

- 외래수술센터(ASC)

- 기타 최종 용도

제8장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제9장 기업 프로파일

- 3rd Stone Design

- Becton, Dickinson and Company

- CELOX MEDICAL

- CooperSurgical

- MedGyn

- ORGANON

- PREGNA INTERNATIONAL

- SINAPI

- STERIMED

- UTAH MEDICAL PRODUCTS, INC.

- ZOEX NIASG

The Global Postpartum Hemorrhage Management Devices Market was valued at USD 958.6 million in 2024 and is estimated to grow at a CAGR of 5.2% to reach USD 1.6 billion by 2034.

The industry continues to advance as the worldwide occurrence of postpartum hemorrhage climbs and awareness of maternal health strengthens. Demand is also influenced by rapid progress in device innovation, growing use of emergency obstetric care, and heightened educational campaigns focused on preventing childbirth complications. These efforts are helping create a more supportive environment for manufacturers by expanding access to maternal care technologies, building stronger collaborations with healthcare systems, and improving overall adoption. Increasing integration of AI-driven analytical tools, digital connectivity, portable equipment, and other technological enhancements is expected to accelerate development over the coming years. Postpartum hemorrhage management devices are designed to control excessive bleeding after childbirth and contribute to reducing maternal mortality during obstetric emergencies. Clinical teams increasingly rely on uterine balloon systems due to their efficiency, minimally invasive nature, and proven effectiveness. Strong safety results and dependable performance continue to broaden their acceptance in healthcare facilities worldwide.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $958.6 Million |

| Forecast Value | $1.6 Billion |

| CAGR | 5.2% |

The uterine tamponade segment held a 55.2% share in 2024, supported by high rates of conditions such as uterine atony and anemia, as well as governmental measures aimed at improving maternal outcomes. These devices deliver internal uterine pressure to manage severe bleeding and can often reduce the need for surgical procedures while stabilizing patients rapidly.

The secondary postpartum hemorrhage segment was valued at USD 163.6 million in 2024. Defined as bleeding occurring more than 24 hours and up to 12 weeks after childbirth, this form of hemorrhage is generally associated with infection, retained tissue, or delayed healing. Diagnostic imaging and treatment using uterotonic medications or surgical options are often required. Although less common than primary postpartum hemorrhage, the secondary category is linked to more complex outcomes and highlights the importance of long-term maternal health planning and preventive-care strategies.

United States Postpartum Hemorrhage Management Devices Market generated USD 330.8 million in 2024. The country's high prevalence of postpartum hemorrhage continues to elevate product demand. The U.S. remains one of the leading adopters of PPH devices due to strong regulatory oversight, a widely developed hospital system, and extensive awareness of maternal health priorities. Public initiatives and private investment in maternal care are broadening access to these devices and stimulating further innovation.

Key Postpartum Hemorrhage Management Devices Market participants include Becton, Dickinson and Company, PREGNA INTERNATIONAL, CooperSurgical, SINAPI, CELOX MEDICAL, ORGANON, STERIMED, ZOEX NIASG, 3rd Stone Design, UTAH MEDICAL PRODUCTS, INC., and MedGyn. Companies competing in the postpartum hemorrhage management devices market are focusing on several strategic actions to enhance their global standing. Many firms are channeling investment toward advanced product engineering to improve reliability, portability, and patient safety. Organizations are expanding R&D programs to introduce new device designs that offer quicker deployment and reduced intervention risks. Strengthening relationships with hospitals and maternal care networks remains a priority, along with broadening distribution in both developed and emerging regions.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product type trends

- 2.2.3 Patient type trends

- 2.2.4 End Use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of postpartum hemorrhage globally

- 3.2.1.2 Increasing maternal mortality awareness campaigns

- 3.2.1.3 Technological advancements in PPH management devices

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Limited access to devices in low-resource settings

- 3.2.2.2 Regulatory delays for new device approvals

- 3.2.3 Opportunities

- 3.2.3.1 Integration of AI for predictive maternal health analytics

- 3.2.3.2 Increased funding for maternal health programs

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Investment landscape

- 3.7 Pricing analysis, 2024

- 3.8 Reimbursement scenario

- 3.9 Sustainability & environmental considerations

- 3.10 Clinical evidence & outcomes analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

- 3.13 Gap analysis

- 3.14 Future market trends

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Uterine tamponade devices

- 5.2.1 Balloon tamponade

- 5.2.2 Vacuum-induced devices

- 5.3 Non-pneumatic anti-shock garments (NASG)

- 5.4 Prefilled injection system

Chapter 6 Market Estimates and Forecast, By Patient Type, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Primary PPH

- 6.3 Secondary PPH

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Maternity & birthing centers

- 7.4 Ambulatory surgical centers

- 7.5 Other End Use

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 3rd Stone Design

- 9.2 Becton, Dickinson and Company

- 9.3 CELOX MEDICAL

- 9.4 CooperSurgical

- 9.5 MedGyn

- 9.6 ORGANON

- 9.7 PREGNA INTERNATIONAL

- 9.8 SINAPI

- 9.9 STERIMED

- 9.10 UTAH MEDICAL PRODUCTS, INC.

- 9.11 ZOEX NIASG