|

시장보고서

상품코드

1911826

산후 서비스 시장 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2026-2031년)Postpartum Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

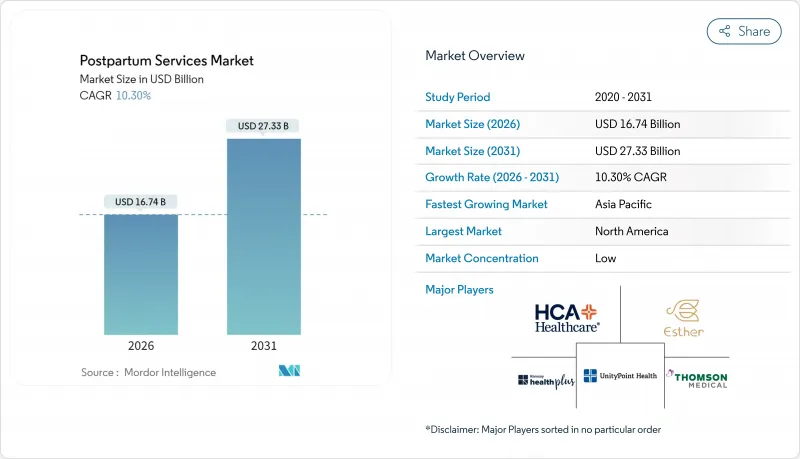

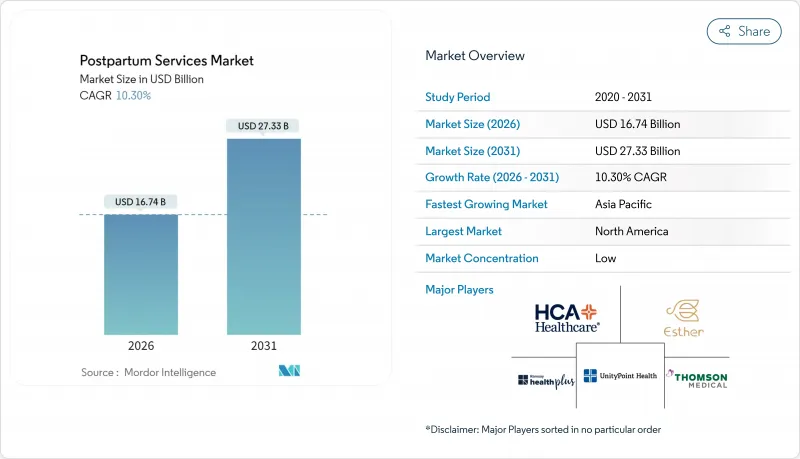

산후 서비스 시장 규모는 2026년에 167억 4,000만 달러로 추정되고, 2025년 151억 8,000만 달러에서 성장을 계속하고 있습니다.

2031년까지 273억 3,000만 달러에 이를 것으로 예측되며, 2026-2031년 CAGR 10.3%로 확대가 전망됩니다.

'제4의 3개월간'의 인지도 향상, 메디케이드 적용 범위 확대, 원격 의료의 급속한 보급에 의해 지불자, 제공업체 및 기술 기업이 장기 지원 경로를 조정하는 가운데 산후 서비스 시장은 확대하고 있습니다. 새로운 연방 참가 조건은 병원에 대해 기존의 6주간 검진을 넘은 케어의 연장을 요구하고 임산부 사망 대책 정책은 재택 방문, 수유 지원 및 멘탈 헬스 프로그램에 새로운 자금을 유도하고 있습니다. 디지털 플랫폼은 인공지능을 통한 트리아지, 원격 모니터링, 온디맨드 지도를 통합하여 지리적 격차 및 의료 종사자의 부담을 줄여줍니다. 산과 테크 스타트업에서 산후 케어 센터 체인에 이르는 통합의 움직임은 가상 접점과 대면 서비스를 결합한 상업 모델의 성숙을 촉진하고 있습니다. 이러한 요인들이 결합되어 산후 서비스 시장 전체에서 환자의 기대가 높아지고 경쟁이 격화되고 서비스의 표준화가 진행되고 있습니다.

세계의 산후 서비스 시장 동향 및 인사이트

임산부 사망률 감소에 대한 세계적 관심 증가

연방 정부 및 다자간 자금의 배분은 성과 기반 임산부 사망률 지표와 연동되어 병원은 출산 후 12개월간의 고혈압 질환, 심근증, 혈전 색전증 위험을 포착하는 근거에 근거한 산후 감시로 이행하고 있습니다. 백악관 블루프린트는 2024년 사망 회피 지표와 보상을 직접 연동시키는 혁신적인 감시 및 모바일 연수 솔루션에 대해 15개 주에 1,900만 달러를 교부했습니다. 유럽도 비슷한 자세를 보이고 있으며, WHO 유럽의 ALERT 프로젝트에서는 표준화된 감사 도구를 통해 16 병원에서 주산기 사망률을 25% 삭감했습니다. 이러한 노력은 엄격한 에스컬레이션 절차, 간호사 주도의 후속 조치, 지역 협력을 중시하고 공인 후 산출 서비스 벤더의 고객 기반을 확대하고 있습니다. 의료 시스템의 최고 정보 책임자(CIO)는 동시에 모체 조기 경고 분석을 전자 기록에 통합하여 예측 알고리즘, 원격 모니터링 키트, 전문의 소개 네트워크에 대한 지속적인 수요를 창출하고 있습니다. 따라서 강력한 정책 신호는 계약주기를 가속화하고 산후 서비스 시장에서 장기 투자의 위험을 줄입니다.

정부 자금으로 산후 케어 프로그램 확대

매사추세츠 주가 2024년에 제정한 보편적 가정 방문 의무화법은 산후 1년간에 걸쳐 두라 지원, 수유 지도, 행동 건강 서비스를 상환하는 메디케이드 및 공중 보건 보조금의 확대 경향을 상징하고 있습니다. 현재 30개 이상의 미국 주가 두라 케어 상환을 실시하고 있으며, TRICARE에서는 연속 분만 1회당 최대 957달러를 지불하는 진료 코드를 설정하고 있습니다. 헬시 스타트 기금은 격차가 큰 지역에 1억 500만 달러를 투입해, 교통수단, 영양 및 멘탈 헬스 지원을 보증하는 것으로, 지역의 산후 케어 제공업체에게 새로운 수익원을 개척하고 있습니다. 캐나다, 일본, 한국, 싱가포르에서도 같은 제도가 도입되어 산욕 케어 시설, 방문 간호사, 하이브리드형 원격 의료 프로그램에 국가 및 지자체의 자금이 투입되고 있습니다. 관리 비용 및 메디케이드의 저단가가 여전히 이익률을 압박하고 있는 반면, 공적 자금의 안정적인 유입에 의해 수요 곡선이 예측 가능하게 되어, 산후 서비스 시장의 장기적인 성장 상한이 인상되고 있습니다.

산후 관리 프로토콜의 표준화 부족

각국마다 다른 가이드라인(6주 국가도 있고 12개월 국가도 있음)은 상환의 논리를 분단하여 국경을 넘은 사업 확대를 복잡하게 합니다. 인증 기준의 불통일이 이 문제를 더욱 심각하게 하고 있습니다. 포스트팔톰 지원 인터내셔널(PSI)의 공인 정신건강 전문가는 2020년 시점에서 1,000명 미만이며, 필요한 규모와는 거리가 먼 상황입니다. 간호사 조산사의 배치 범위를 제한하는 법률이 존재하며, 출산 센터의 메디케이드 보상은 뉴저지주에서 1,300달러, 매사추세츠주에서 6,012달러로 지역차가 크고 환자 유동을 왜곡하고 있습니다. 통일된 임상 패키지가 없기 때문에 투자자들은 여러 주에서의 사업 확대에 대한 자금 제공을 망설이고 산후 서비스 시장의 성장 속도를 억제하고 있습니다.

부문 분석

수유 상담 서비스는 모유 육아의 성공이 모자 건강의 보편적인 지표인 것을 계속하기 때문에 2025년 산후 서비스 시장에서 28.10%의 선두 점유율을 획득했습니다. 높은 이용률은 병원의 '아기 친화적인 병원' 인증의 의무화 및 퇴원 후에도 지원을 계속하는 고용주의 수유 배려 의무법에 뿌리를 두고 있습니다. 보험사가 완전 모유 육아율에 연동한 가치 기반의 지불 방식을 채용함에 따라, 수유 분야의 산후 서비스 시장 규모는 점증적인 성장이 예상됩니다. 원격 의료에 의한 산후 케어는 규모가 작은 반면, 의료 종사자 부족 및 비디오 진찰을 선호하는 소비자의 경향을 배경으로, 12.48%의 연평균 복합 성장률(CAGR)로 가장 급속하게 확대하고 있습니다. 공급자는 안전한 메시징, 비동기 사진 검토, AI 트리아지를 통합하여 예약 백로그를 줄이기 위해 노력하고 있습니다.

물리치료 및 골반저서비스는 산후 요실금과 미래의 골반 장기 탈의 관련성을 조사가 밝히면서 의사의 소개가 증가하고 있습니다. 보완적인 식사 및 영양 카운셀링은 산욕식 스타일의 식사 택배를 상업화하고 있으며, 치요사의 50만 달러 규모의 수익 페이스는 북미에서의 침투를 뒷받침하고 있습니다. 정신 건강 및 산후 우울증 프로그램은 CMS(미국 의료 보험 서비스 센터)가 2025년에 도입을 의무화하는 보편적 스크리닝의 품질 지표를 받아 더욱 확대되고 있습니다. 이러한 서브라인은 종합적으로 산후 서비스 시장에서 텔레헬스를 틈새가 아닌 핵심으로 확립하는 다각적인 진입 경로를 형성하고 있습니다.

지역별 분석

2025년 산후 서비스 시장 규모의 39.75%를 북미가 견인했습니다. 연방 정부의 임산부 건강 지출 5억 5,800만 달러(중 4억 4,000만 달러가 방문 간호 네트워크에 투입)가 원동력이 되었습니다. 많은 주에서 메디케이드의 적용 기간이 산후 12개월까지 연장됨으로써, 지불자측의 수익이 안정되어, 지속적인 수유 지원, 멘탈 헬스 및 만성 질환 스크리닝 수요가 높아지고 있습니다. PARADIGM 이동 진료소 등의 지향 시책은 지방 출산의 산부에 있어서 중대한 이환율 9% 증가에 대처해, 원격 의료의 상환 균등화법 제정을 촉진하고 있습니다. 그러나 메디케어와 메디케이드 간의 상환 격차는 불평등을 계속하고 있으며, 정책의 뒷받침이 있음에도 불구하고 대응 가능한 수요의 완전한 포착을 제한하고 있습니다.

아시아태평양은 가장 성장하는 시장이며 2031년까지 연평균 복합 성장률(CAGR) 11.25%로 확대될 것으로 전망됩니다. 이것은 법적 서비스 의무화 및 산후 케어 센터 체인의 급성장에 의해 지원됩니다. 일본의 2019년법은 단기 체류형 주택과 방문 케어 패키지를 조성하여 산후 케어 이용을 보급했습니다. 한국에서는 5억 달러 규모의 산후 케어 센터 시장이 산부의 80% 이상을 커버해, 프랜차이즈 모델을 북미 및 중동에 전개중입니다. 싱가포르의 Re'Joy Suites는 AI 침술, 고압 산소 요법,월 12만 4,000달러에 이르는 포괄 요금 체계를 통해 고급 산후 케어의 새로운 기준을 확립하고 있습니다. 이러한 동향은 산후 서비스 시장에서 원격 의료에 의한 월경 상담 및 고이익률의 웰니스 부가 서비스의 수익성이 높은 분야를 개척하고 있습니다.

유럽에서는 충실한 산휴제도 및 WHO 주도 품질 개선 틀에 힘입어 꾸준한 확대가 계속되고 있습니다. EU는 최소 14주간의 유급 휴가를 의무화하고 있으며, 스칸디나비아 국가에서는 장기간의 급여를 연장하고 상환 대상 서비스의 기간을 확대하고 있습니다. WHO 유럽의 ALERT 감사는 사망률을 25% 줄이고 표준화된 산후 프로토콜의 채용을 촉진하고 소프트웨어, 모니터링 장비, 전문가 교육의 조달 기회를 확대하고 있습니다. 하지만 단편화한 각국의 보험 제도에 따라 벤더는 다른 요금 체계에 대응할 수밖에 없어 시장 진입 비용이 부풀어 규모의 경제 효과가 억제되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트에 의한 3개월간의 지원

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 임산부 사망률 삭감에 대한 세계의 관심 증가

- 정부 자금에 의한 산후 케어 프로그램 확대

- 재택 회복 솔루션에 대한 수요 증가

- 산과 의료에서 디지털 헬스 에코시스템의 보급

- 산후 케어 경로에 정신 건강 서비스 통합

- 홀리스틱 및 웰니스 산후 케어 시설 대두

- 시장 성장 억제요인

- 산후 케어 프로토콜의 표준화가 한정적인 것

- 의료 시스템 간의 상환 격차

- 인정 산후 전문가의 부족

- 서비스 도입에 있어서의 사회 문화적 장벽

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모 및 성장 예측

- 서비스별

- 수유 상담 서비스

- 물리치료 및 골반저치료

- 의료 처치 및 합병증 관리

- 식사 및 영양 상담

- 정신 건강 및 산후 우울증(PPD) 서비스

- 방문 서비스 및 두라

- 원격 의료에 의한 산후 케어

- 용도별

- 제왕 절개 후 회복

- 질 분만 후 회복

- 산후 우울증 및 불안증 관리

- 모유 육아 서포트

- 산후 체중 관리

- 시설 유형별

- 공립 병원 및 지역 의료 센터

- 사립산과병원 및 클리닉

- 재택 서비스

- 온라인 플랫폼 및 앱

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- HCA Healthcare

- Ramsay Health Care

- Ascension

- Thomson Medical Group Limited

- Cloudnine Group of Hospitals

- Esther Postpartum Care

- UnityPoint Health

- Fortis La Femme

- The Cochin Birthvillage Pvt. Ltd.

- ROYCE Postpartum & Postnatal Center

- Health 360

- Nejlika Confinement Care Centre

- Kimporo

- Cocoon Postpartum Care

- Felicity Postpartum Care

- Mount Sinai Health System

- Johns Hopkins Medicine

- Motherhood Hospitals

- Mednax

- Yue Yue Postnatal Care Center

- Parkview Health

- Newlife Confinement Center

제7장 시장 기회 및 장래 전망

AJY 26.01.30postpartum services market size in 2026 is estimated at USD 16.74 billion, growing from 2025 value of USD 15.18 billion with 2031 projections showing USD 27.33 billion, growing at 10.3% CAGR over 2026-2031.

Spiraling recognition of the "fourth trimester," broadened Medicaid coverage, and rapid telehealth normalization are enlarging the postpartum services market as payers, providers, and technology firms coordinate long-term support pathways. New federal Conditions of Participation press hospitals to extend care beyond the classic six-week visit, while maternal-mortality policies channel fresh capital into home-visiting, lactation, and mental-health programs. Digital platforms overlay artificial-intelligence triage, remote monitoring, and on-demand coaching, reducing geographic inequities and clinician workload. Consolidation momentum-from maternity-tech start-ups to confinement-center chains-is maturing commercial models that couple virtual touchpoints with in-person services. Collectively, these forces elevate patient expectations, intensify competition, and drive service standardization across the postpartum services market.

Global Postpartum Services Market Trends and Insights

Growing Global Focus on Maternal Mortality Reduction

Federal and multilateral funding funnels are now tied to outcome-based maternal-mortality metrics, steering hospitals toward evidence-based postpartum surveillance that captures hypertensive disorders, cardiomyopathy, and thromboembolic risk during the first 12 months after birth. The White House Blueprint awarded USD 19 million to 15 states in 2024 for innovative surveillance and mobile training solutions that directly link reimbursement to mortality-avoidance indicators. Europe mirrors this stance as WHO Europe's ALERT project cut perinatal mortality 25% across 16 hospitals through standardized audit tools. These initiatives emphasize rigid escalation protocols, nurse-led follow-ups, and community outreach, enlarging the customer base for certified postpartum service vendors. Health-system CIOs concurrently embed maternal early-warning analytics into electronic records, creating recurring demand for predictive algorithms, telemonitoring kits, and specialist referral networks. Strong policy signaling therefore accelerates contracting cycles and de-risks long-term investments in the postpartum services market.

Expansion of Government-Funded Postnatal Care Programs

Massachusetts' 2024 statute mandating universal home visits typifies a groundswell of Medicaid and public-health grants that reimburse doula, lactation, and behavioral-health services across a full year postpartum. Thirty-plus U.S. states now reimburse doula care, arranging codes that pay up to USD 957 per continuous-labor episode under TRICARE. Healthy Start funds inject USD 105 million into high-disparity communities, underwriting transportation, nutrition, and mental-health supports that unlock new revenue lines for regional postpartum providers. Similar schemes in Canada, Japan, South Korea, and Singapore bring national or municipal dollars to confinement centers, home-visiting nurses, and hybrid telehealth programs. Although administrative overhead and low Medicaid rates still pinch margins, the steady flow of public financing establishes predictable demand curves and lifts the long-run growth ceiling for the postpartum services market.

Limited Standardization of Postpartum Care Protocols

Varying national guidelines-six weeks in some countries versus 12 months in others-fracture reimbursement logic and complicate cross-border expansion. Certification inconsistencies amplify the issue; Postpartum Support International had fewer than 1,000 credentialed mental-health professionals by 2020, nowhere near required capacity. Scope-of-practice laws constrain nurse-midwife deployments, while birth-center Medicaid rates swing from USD 1,300 in New Jersey to USD 6,012 in Massachusetts, distorting patient flows. Without harmonized clinical bundles, investors hesitate to fund multi-state scale-ups, tempering velocity in the postpartum services market.

Other drivers and restraints analyzed in the detailed report include:

- Rising Demand for Home-Based Recovery Solutions

- Proliferation of Digital-Health Ecosystems in Maternal Care

- Reimbursement Gaps Across Healthcare Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Lactation consultancy secured a leading 28.10% postpartum services market share in 2025 as breastfeeding success remains a universal benchmark for maternal-infant health. High uptake is rooted in mandatory hospital baby-friendly certifications and employer lactation-accommodation laws that extend support beyond discharge. The postpartum services market size for lactation is poised for incremental growth as insurers adopt value-based payment tied to exclusive breastfeeding rates. Telehealth postpartum care, while smaller, is scaling fastest at a 12.48% CAGR on the back of clinician shortages and consumer preference for video visits. Providers integrate secure messaging, asynchronous photo review, and AI triage to slash appointment backlogs.

Physical-therapy and pelvic-floor services are gaining physician referrals as research highlights links between postpartum incontinence and future pelvic-organ prolapse. Complementary diet-and-nutrition counseling is commercializing confinement-style meal delivery; Chiyo's USD 0.5 million revenue run-rate evidences traction in North America. Mental-health and postpartum-depression programs rise further following CMS's 2025 quality measure mandating universal screening. Collectively these sublines create multichannel entry points that cement telehealth as a backbone rather than a niche within the postpartum services market.

The Postpartum Services Market Report is Segmented by Service (Lactation Consultancy, and More), Application (Cesarean-Section Recovery, and More), Facility Type (Public Hospitals & Community Centers, Private Maternity Hospitals & Clinics, and More), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America led with 39.75% of the postpartum services market size in 2025, powered by USD 558 million in federal maternal-health spending that funneled USD 440 million into home-visiting networks. Medicaid extensions to 12-month postpartum eligibility across many states stabilize payer revenue and heighten demand for ongoing lactation, mental-health, and chronic-disease screenings. Rural initiatives such as PARADIGM mobile clinics tackle the 9% higher severe-morbidity rate among rural birthing people, catalyzing telehealth reimbursement parity laws. Yet reimbursement gaps between Medicare and Medicaid sustain inequities, limiting full capture of addressable demand despite policy tailwinds.

Asia-Pacific is the fastest-growing arena, advancing at 11.25% CAGR through 2031, underpinned by legislated service mandates and booming confinement-center chains. Japan's 2019 law funds short-stay residential and home-visit packages, normalizing postpartum care utilization. South Korea's half-billion-dollar postpartum-center segment now serves more than 80% of mothers, exporting franchise models to North America and the Middle East. Singapore's Re'Joy Suites sets the luxury bar with AI acupuncture, hyperbaric oxygen therapy, and all-inclusive pricing that reaches USD 124,000 monthly. These developments carve lucrative lanes for telehealth cross-border consults and high-margin wellness add-ons within the postpartum services market.

Europe delivers steady expansion supported by robust maternity-leave protections and WHO-coordinated quality-improvement frameworks. The EU mandates at least 14 weeks paid leave, with Scandinavian nations extending benefits far longer, prolonging the window for reimbursed services. WHO Europe's ALERT audit cut mortality by 25%, driving adoption of standardized postpartum protocols that open procurement doors for software, monitoring devices, and specialist training. Fragmented national insurance structures, however, force vendors to navigate divergent tariff schedules, inflating go-to-market costs and tempering scale economies.

- HCA Healthcare

- Ramsay Health Care

- Ascension

- Thomson Medical Group Limited

- Cloudnine Group of Hospitals

- Esther Postpartum Care

- UnityPoint Health

- Fortis La Femme

- The Cochin Birthvillage Pvt. Ltd.

- ROYCE Postpartum & Postnatal Center

- Health 360

- Nejlika Confinement Care Centre

- Kimporo

- Cocoon Postpartum Care

- Felicity Postpartum Care

- Mount Sinai Health System

- Johns Hopkins Medicine

- Motherhood Hospitals

- Mednax

- Yue Yue Postnatal Care Center

- Parkview Health

- Newlife Confinement Center

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Global Focus on Maternal Mortality Reduction

- 4.2.2 Expansion of Government-Funded Postnatal Care Programs

- 4.2.3 Rising Demand for Home-Based Recovery Solutions

- 4.2.4 Proliferation of Digital Health Ecosystems in Maternal Care

- 4.2.5 Integration of Mental Health Services into Postpartum Care Pathways

- 4.2.6 Emergence of Holistic Wellness Confinement Centers

- 4.3 Market Restraints

- 4.3.1 Limited Standardization of Postpartum Care Protocols

- 4.3.2 Reimbursement Gaps across Healthcare Systems

- 4.3.3 Shortage of Certified Postpartum Specialists

- 4.3.4 Socio-Cultural Barriers to Service Adoption

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitutes

- 4.4.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Service

- 5.1.1 Lactation Consultancy

- 5.1.2 Physical & Pelvic-Floor Therapy

- 5.1.3 Medical Treatment & Complication Mgmt.

- 5.1.4 Diet & Nutrition Counseling

- 5.1.5 Mental-Health & PPD Services

- 5.1.6 Home Visits & Doulas

- 5.1.7 Telehealth Postpartum Care

- 5.2 By Application

- 5.2.1 Cesarean-Section Recovery

- 5.2.2 Vaginal Birth Recovery

- 5.2.3 Postpartum Depression & Anxiety Mgmt.

- 5.2.4 Breast-feeding Support

- 5.2.5 Post-partum Weight Mgmt.

- 5.3 By Facility Type

- 5.3.1 Public Hospitals & Community Centers

- 5.3.2 Private Maternity Hospitals & Clinics

- 5.3.3 Home-based Services

- 5.3.4 Online Platforms & Apps

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East & Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East & Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.3.1 HCA Healthcare

- 6.3.2 Ramsay Health Care

- 6.3.3 Ascension

- 6.3.4 Thomson Medical Group Limited

- 6.3.5 Cloudnine Group of Hospitals

- 6.3.6 Esther Postpartum Care

- 6.3.7 UnityPoint Health

- 6.3.8 Fortis La Femme

- 6.3.9 The Cochin Birthvillage Pvt. Ltd.

- 6.3.10 ROYCE Postpartum & Postnatal Center

- 6.3.11 Health 360

- 6.3.12 Nejlika Confinement Care Centre

- 6.3.13 Kimporo

- 6.3.14 Cocoon Postpartum Care

- 6.3.15 Felicity Postpartum Care

- 6.3.16 Mount Sinai Health System

- 6.3.17 Johns Hopkins Medicine

- 6.3.18 Motherhood Hospitals

- 6.3.19 Mednax

- 6.3.20 Yue Yue Postnatal Care Center

- 6.3.21 Parkview Health

- 6.3.22 Newlife Confinement Center

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment