|

시장보고서

상품코드

1876817

형상 기억 폴리머 시장 기회, 성장요인, 업계 동향 분석 및 예측(2025-2034년)Shape Memory Polymers Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

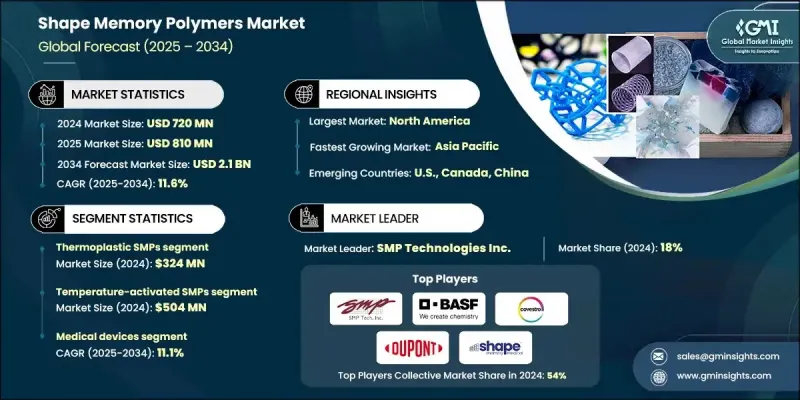

세계의 형상 기억 폴리머 시장은 2024년에 7억 2,000만 달러로 평가되었고, 2034년까지 연평균 복합 성장률(CAGR) 11.6%로 성장하여 21억 달러에 이를 것으로 예측됩니다.

산업 분야에서 스마트하고 반응성이 높은 소재의 활용이 점점 더 중요해지면서 시장은 계속 확대되고 있습니다. 형상기억고분자(SMP)가 외부 자극을 받으면 원래의 모양으로 되돌아가는 고유한 특성은 고성능 및 적응성이 높은 소재를 필요로 하는 첨단 분야에서 채택되고 있습니다. 지능형 소재 설계에 대한 관심이 높아지면서 제조, 의료, 자동차, 항공우주 산업에서 SMP의 활용이 촉진되고 있습니다. 이 폴리머는 지속가능성, 에너지 효율성, 자가 치유 능력의 혁신을 지원하여 제조업체가 더 가볍고 내구성이 뛰어난 구조물을 설계할 수 있게 해줍니다. 생체 의료 분야에서 SMP는 첨단 의료기기, 자가 확장형 스텐트, 최소 침습 임플란트에 점점 더 많이 채택되어 성능 향상과 환자 회복을 촉진하고 있습니다. 항공우주 및 방위 분야에서도 경량성, 내피로성, 프로그래밍 가능한 기계적 거동 등의 특성이 운영 효율성과 장기적인 신뢰성에 기여하기 때문에 SMP 기반 소재에 대한 투자가 활발히 이루어지고 있습니다. 지속적인 연구개발과 소재 기술 혁신을 통해 SMP는 차세대 소재 기술의 기반으로서 꾸준히 입지를 다져가고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2024년 |

| 예측 기간 | 2025-2034년 |

| 시작 금액 | 7억 2,000만 달러 |

| 예측 금액 | 21억 달러 |

| CAGR | 11.6% |

열가소성 형상 기억 폴리머(SMP) 부문은 2024년 3억 2,400만 달러 시장 규모를 형성했습니다. 이 소재들은 재활용성, 가공의 용이성, 지속 가능한 제품 개발의 가능성으로 인해 인기가 높아지고 있습니다. 열가소성 SMP는 일반적으로 강도가 낮고 내열성에도 한계가 있지만, 배합기술의 혁신과 하이브리드형, 다반응형 등 신소재의 도입으로 성능이 향상되고 있습니다. 또한, 지속가능성이 설계 및 제조에 있어 중요한 요소로 떠오르면서 생분해성 SMP와 복합 SMP에 대한 관심도 높아지고 있습니다. 고분자 화학 및 가공 기술이 지속적으로 발전함에 따라, 우수한 기능성을 갖춘 재프로그래밍 가능한 SMP에 대한 수요는 산업 전반에 걸쳐 확대될 것으로 예측됩니다.

온도 활성화형 형상기억 폴리머 부문은 2024년 5억 4,000만 달러 시장 규모를 기록했습니다. 이 카테고리는 간편한 활성화 프로세스와 표준 생산 기술과의 호환성으로 인해 선도적인 위치를 차지하고 있습니다. 이 소재들은 열 트리거에 효율적으로 반응하여 자동차, 항공우주, 바이오메디컬 분야에서 널리 활용되고 있습니다. 열 활성화로 형상 회복, 유연성, 자기 회복 거동에 대한 우수한 제어가 가능하여 다양한 엔지니어링 및 구조적 용도에 적합합니다.

북미 형상기억고분자 시장은 2024년 2억 8,800만 달러 규모로 40%의 점유율을 유지했습니다. 미국은 강력한 산업 기반, 기술 혁신, 확립된 연구개발 체제를 바탕으로 이 지역에서 가장 큰 점유율을 차지하고 있습니다. 항공우주, 의료기기, 자동차 등 주요 분야에서 광범위하게 사용되면서 시장 성장을 지속적으로 견인하고 있습니다. 또한, 이 지역에는 산업용 및 의료용 적응성 폴리머의 상용화에 주력하는 첨단 소재 제조업체와 폴리머 개발 기업이 다수 존재합니다. 주요 폴리머 제조업체의 입지와 R&D에 대한 지속적인 투자는 세계 형상기억고분자 시장에서 이 지역의 선도적인 위치를 더욱 강화시키고 있습니다.

세계 형상기억 폴리머 시장에서 활동하는 주요 기업으로는 Coating Place Inc. Inc.,DOW Corning,Balchem Corporation,Capsugel(Lonza Group) 등이 있습니다. 세계 형상 기억 폴리머 시장의 주요 기업들은 시장 기반을 강화하기 위해 여러 전략을 채택하고 있습니다. 여기에는 유연성, 재프로그래밍 능력, 생분해성 등 폴리머 특성을 개선하기 위한 R&D 투자가 포함됩니다. 소재 혁신과 응용 확대를 가속화하기 위해 학계 및 산업 파트너와의 전략적 제휴도 추진하고 있습니다. 많은 기업들이 다자극 반응형 SMP 개발 및 의료, 항공우주 등 고성장 분야로의 통합을 통한 제품 다각화에 주력하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급업체 상황

- 이익률

- 각 단계 부가가치

- 밸류체인에 영향을 미치는 요인

- 파괴적 변화

- 업계에 대한 영향요인

- 성장 촉진요인

- 업계의 잠재적 리스크&과제

- 시장 기회

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 가격 동향

- 지역별

- 재료 유형

- 자극 유형

- 용도

- 향후 시장 동향

- 기술과 혁신 동향

- 현재 기술 동향

- 신기술

- 특허 상황

- 무역 통계(HS코드)(주 : 무역 통계는 주요 국가에 한해 제공됩니다)

- 주요 수입국

- 주요 수출국

- 지속가능성과 환경면

- 지속가능한 대처

- 폐기물 감축 전략

- 생산 에너지 효율

- 친환경 이니셔티브

- 탄소발자국에 관한 고려사항

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 인수합병(M&A)

- 제휴 및 협업

- 신제품 발매

- 사업 확대 계획

제5장 시장 추산·예측 : 재료 유형별, 2021-2034

- 주요 동향

- 열가소성 SMP

- 폴리우레탄계 수지

- 폴리에스테르계 수지

- 폴리카프로락톤계 수지

- 열경화성 SMP

- 에폭시 수지계 시스템

- 시아네이트에스테르계

- 폴리이미드계 수지

- 생분해성 SMP

- Poly(ε-caprolactone) 기반

- PLGA 기반 시스템

- PHA 기반 시스템

- 복합 SMP

- 탄소섬유 강화

- 유리섬유 강화

- 나노입자 강화

제6장 시장 추산·예측 : 자극 유형별, 2021-2034

- 주요 동향

- 온도 작동형 형상기억합금

- 유리 전이 트리거 시스템

- 융점 트리거 시스템

- 체온 작동 시스템

- 광활성화 형상기억합금

- 자외선 트리거 시스템

- 가시광선 시스템

- 근적외 활성화 시스템

- 전기 작동형 SMP

- 줄 가열 시스템(Joule heating systems)

- 전도성 필러 통합

- 저항 가열 용도

- 자기 작동형 형상기억합금

- 산화철 나노입자 시스템

- 강자성 필러 통합

- 원격 작동 용도

제7장 시장 추산·예측 : 용도별, 2021-2034

- 주요 동향

- 의료기기

- 혈관색전 장비

- 스텐트 및 카테터

- 정형외과용 임플란트

- 외과용 기구

- 약물 전달 시스템

- 항공우주 및 방위

- 배치 가능한 구조물

- 변형 가능한 항공기 부품

- 우주 용도

- 자기치유 복합재료

- 액추에이터 시스템

- 자동차

- 자기치유 부품

- 적응형 공력 시스템

- 내장 용도

- 안전 시스템

- 경량화 용도

- 건설 및 인프라

- 파이프라인 개보수 시스템

- 적응형 건축 외피

- 내진성 용도

- 스마트 인프라 시스템

- 자기치유 콘크리트

- 산업 및 제조

- 액추에이터 시스템

- 스마트 컴포넌트

- 프로세스 기기

- 자동화 용도

- 섬유 용도

제8장 시장 추산·예측 : 지역별, 2021-2034

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 기타 라틴아메리카

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카공화국

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

제9장 기업 개요

- Shape Memory Medical Inc.

- Covestro AG

- BASF SE

- SMP Technologies Inc.

- Dupont De Nemours, Inc.

- Natureworks LLC

- Lubrizol Corporation

- Evonik Industries AG

- Spintech, LLC

- Huntsman International LLC

The Global Shape Memory Polymers Market was valued at USD 720 million in 2024 and is estimated to grow at a CAGR of 11.6% to reach USD 2.1 billion by 2034.

The market is expanding as industries increasingly focus on the use of smart and responsive materials. The unique ability of shape memory polymers (SMPs) to return to their original form when exposed to external stimuli has led to their adoption in advanced sectors requiring high-performance and adaptive materials. Growing emphasis on intelligent material design is promoting their use across manufacturing, healthcare, automotive, and aerospace industries. These polymers support innovations in sustainability, energy efficiency, and self-healing capabilities, allowing manufacturers to design lighter and more durable structures. In the biomedical field, SMPs are increasingly being used for advanced medical devices, self-expanding stents, and minimally invasive implants, offering enhanced performance and patient recovery. The aerospace and defense sectors are also investing heavily in SMP-based materials due to their low weight, fatigue resistance, and programmable mechanical behavior, all of which contribute to operational efficiency and long-term reliability. With ongoing R&D initiatives and material breakthroughs, SMPs are steadily becoming a cornerstone of next-generation material technology.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $720 Million |

| Forecast Value | $2.1 Billion |

| CAGR | 11.6% |

Thermoplastic shape memory polymers segment generated USD 324 million in 2024. These materials are gaining popularity due to their recyclability, ease of processing, and potential in sustainable product development. Although thermoplastic SMPs generally have lower strength and limited temperature tolerance, innovations in formulation and the introduction of hybrid and multi-responsive variants are improving their performance. The market is also witnessing growing interest in biodegradable and composite SMPs, as sustainability becomes a key factor in design and manufacturing. With continuous advancements in polymer chemistry and processing, the demand for reprogrammable SMPs with superior functionality is expected to expand across industrial applications.

The temperature-activated shape memory polymers segment generated USD 504 million in 2024. This category dominates due to its simple activation process and compatibility with standard production techniques. These materials respond efficiently to thermal triggers and are widely used in automotive, aerospace, and biomedical applications. Their thermal activation enables superior control over shape recovery, flexibility, and self-healing behavior, making them suitable for multiple engineering and structural applications.

North America Shape Memory Polymers Market accounted for USD 288 million in 2024 and held 40% share. The United States holds the largest share in the region, supported by a strong industrial foundation, technological innovation, and a well-established R&D framework. Extensive usage in key sectors such as aerospace, medical devices, and automotive continues to drive market growth. Additionally, the region is home to several advanced material producers and polymer developers focusing on the commercialization of adaptive polymers for industrial and medical use. The presence of major polymer manufacturers and ongoing investments in research are further enhancing the region's leadership position in the Global Shape Memory Polymers Market.

Major companies active in the Global Shape Memory Polymers Market include Coating Place Inc., Evonik Industries AG, 3M Company, DSM N.V., Syngenta AG, Aveka Inc., BASF SE, Ashland Global Holdings Inc., DOW Corning, Balchem Corporation, and Capsugel (Lonza Group). Leading companies in the Global Shape Memory Polymers Market are adopting multiple strategies to strengthen their market foothold. These include investments in R&D to enhance polymer properties such as flexibility, reprogramming capability, and biodegradability. Strategic collaborations with academic institutions and industrial partners are being pursued to accelerate material innovation and application expansion. Many firms are focusing on product diversification by developing multi-stimuli-responsive SMPs and integrating them into high-growth sectors like healthcare and aerospace.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Material Type

- 2.2.3 Stimulus Type

- 2.2.4 Application

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for smart materials

- 3.2.1.2 Advancements in biomedical applications

- 3.2.1.3 Growing aerospace and defense sector

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Limited recovery force compared to shape memory alloys

- 3.2.2.2 High production costs for specialty formulations

- 3.2.2.3 Temperature sensitivity & environmental stability challenges

- 3.2.3 Market opportunities

- 3.2.3.1 Climate-adaptive building envelope systems

- 3.2.3.2 Sustainable & bio-based formulation development

- 3.2.3.3 IoT integration & smart infrastructure applications

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and Innovation Landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 Material Type

- 3.7.3 Stimulus Type

- 3.7.4 Application

- 3.8 Future market trends

- 3.9 Technology and Innovation Landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Material Type, 2021 - 2034 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Thermoplastic SMPs

- 5.2.1 Polyurethane-based systems

- 5.2.2 Polyester-based systems

- 5.2.3 Polycaprolactone systems

- 5.3 Thermoset SMPs

- 5.3.1 Epoxy-based systems

- 5.3.2 Cyanate ester systems

- 5.3.3 Polyimide systems

- 5.4 Biodegradable SMPs

- 5.4.1 Poly(ε-caprolactone) based

- 5.4.2 PLGA-based systems

- 5.4.3 PHA-based systems

- 5.5 Composite SMPs

- 5.5.1 Carbon fiber reinforced

- 5.5.2 Glass fiber reinforced

- 5.5.3 Nanoparticle enhanced

Chapter 6 Market Estimates and Forecast, By Stimulus Type, 2021 - 2034 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Temperature-activated SMPs

- 6.2.1 Glass transition triggered systems

- 6.2.2 Melting temperature triggered systems

- 6.2.3 Body temperature activated systems

- 6.3 Light-activated SMPs

- 6.3.1 UV-triggered systems

- 6.3.2 Visible light systems

- 6.3.3 Nir-activated systems

- 6.4 Electrically activated SMPs

- 6.4.1 Joule heating systems

- 6.4.2 Conductive filler integration

- 6.4.3 Resistive heating applications

- 6.5 Magnetically activated SMPs

- 6.5.1 Iron oxide nanoparticle systems

- 6.5.2 Ferromagnetic filler integration

- 6.5.3 Remote activation applications

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Medical devices

- 7.2.1 Vascular embolization devices

- 7.2.2 Stents & catheters

- 7.2.3 Orthopedic implants

- 7.2.4 Surgical instruments

- 7.2.5 Drug delivery systems

- 7.3 Aerospace & defense

- 7.3.1 Deployable structures

- 7.3.2 Morphing aircraft components

- 7.3.3 Space applications

- 7.3.4 Self-healing composites

- 7.3.5 Actuator systems

- 7.4 Automotive

- 7.4.1 Self-repairable components

- 7.4.2 Adaptive aerodynamics

- 7.4.3 Interior applications

- 7.4.4 Safety systems

- 7.4.5 Lightweighting applications

- 7.5 Construction & infrastructure

- 7.5.1 Pipeline renovation systems

- 7.5.2 Adaptive building envelopes

- 7.5.3 Seismic resilience applications

- 7.5.4 Smart infrastructure systems

- 7.5.5 Self-healing concrete

- 7.6 Industrial & manufacturing

- 7.6.1 Actuator systems

- 7.6.2 Smart components

- 7.6.3 Process equipment

- 7.6.4 Automation applications

- 7.6.5 Textile applications

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 (USD million) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Shape Memory Medical Inc.

- 9.2 Covestro AG

- 9.3 BASF SE

- 9.4 SMP Technologies Inc.

- 9.5 Dupont De Nemours, Inc.

- 9.6 Natureworks LLC

- 9.7 Lubrizol Corporation

- 9.8 Evonik Industries AG

- 9.9 Spintech, LLC

- 9.10 Huntsman International LLC