|

시장보고서

상품코드

1876818

재생 탄소섬유 시장 기회, 성장요인, 업계 동향 분석 및 예측(2025-2034년)Recycled Carbon Fiber Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

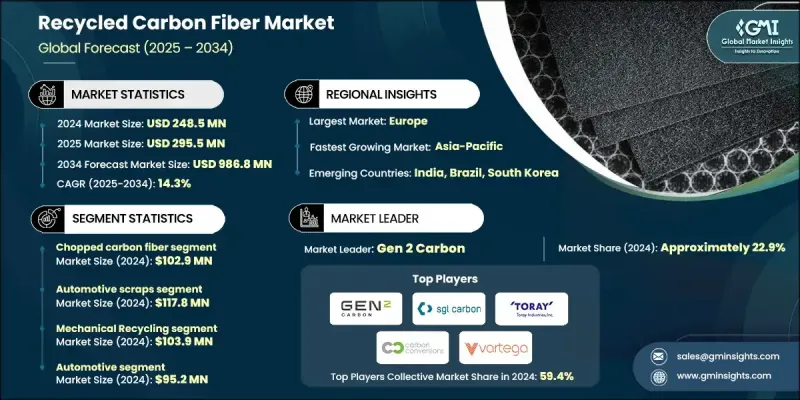

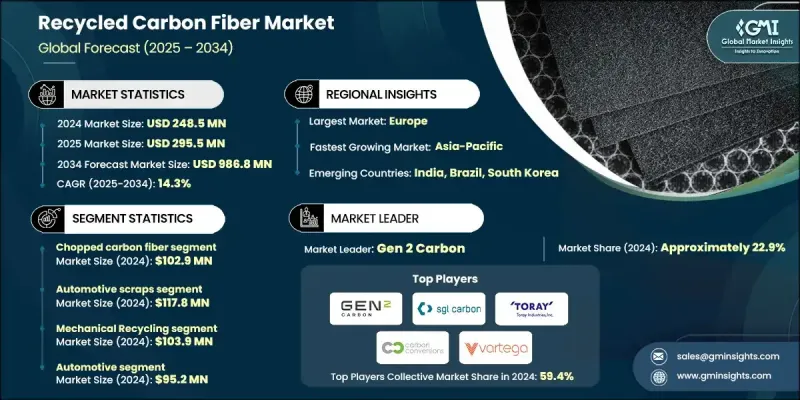

세계의 재생 탄소섬유 시장은 2024년에 2억 4,850만 달러로 평가되었고, 2034년까지 연평균 복합 성장률(CAGR) 14.3%로 성장하여 9억 8,680만 달러에 이를 것으로 예측됩니다.

시장 성장의 배경에는 1차 탄소섬유 생산의 환경 부하를 줄이기 위한 움직임이 가속화되고 있으며, 이에 따라 자동차 제조업체들은 전기자동차 부품 및 경량 자동차 내장재에 재생 탄소섬유(rCF)의 채용을 추진하고 있습니다. Vartega, ELG Carbon Fibre 등의 기업들은 수요 증가에 대응하기 위해 생산능력을 확충하고 있습니다. 특히 정부 주도의 교통 분야 연구 프로젝트는 차량 효율 향상과 배출가스 저감을 목적으로 rCF의 보급을 촉진하고 있습니다. 열분해 및 용해 분해 기술의 발전으로 더 긴 섬유 가닥의 생산이 가능하여 구조적 응용의 실용성이 향상되었습니다. 항공우주산업 및 자동차 산업에서는 내장재, 플라스틱 보강재, 차체 하부 부품에 재생 탄소섬유(rCF)의 사용이 확대되고 있습니다. 중국도 이러한 노력을 강화하고 있으며, 풍력 터빈 블레이드와 복합재 폐기물을 관리하는 재활용 거점을 개발하고 있습니다. 틈새 응용에서 대규모 상업 생산으로의 전환은 순환 경제 정책과 청정 복합재 가공 기술에 의해 뒷받침되고 있습니다. 저온 열분해 및 화학적 용해 분해와 같은 섬유 회수 기술의 혁신으로 섬유의 길이와 강도가 향상되고 있습니다. Vartega와 Carbon Conversions와 같은 기업들은 열가소성 수지 및 시트 성형 컴파운드에 적합한 거의 처녀 품질에 가까운 재생 탄소섬유(rCF)를 생산하여 마감과 성능이 중요한 고성능 가전제품 및 스포츠 용품에 적용할 수 있도록 하고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 2억 4,850만 달러 |

| 예측 금액 | 9억 8,680만 달러 |

| CAGR | 14.3% |

단섬유 탄소섬유 부문은 2024년에 1억 2,900만 달러로 평가되었고, 2034년까지 연평균 13.1% 성장할 것으로 예측됩니다. 단섬유 및 분쇄된 rCF는 열가소성 플라스틱 및 수지와의 통합이 용이하기 때문에 특히 자동차 및 전자제품 제조에 널리 사용되고 있습니다. 이러한 섬유를 이용한 사출 성형으로 경량 부품의 대량 생산이 가능하며, 섬유 크기의 일관성이 OEM 제조업체의 중요한 초점이 되고 있습니다.

자동차 스크랩 유래 재생 탄소섬유(rCF) 시장은 2024년 1억 1,780만 달러로 평가되었고, 2025년부터 2034년까지 17%의 연평균 복합 성장률(CAGR)을 보일 것으로 예측됩니다. 전기차 붐과 매립지 규제 강화로 가속화되는 자동차 및 산업폐기물 증가가 이 부문을 주도하고 있습니다. 파쇄된 탄소섬유강화플라스틱(CFRP) 폐기물은 사출성형용으로 다진 섬유나 밀드 파이버로 가공되는 사례가 증가하고 있습니다. 유럽에서는 풍력 터빈 블레이드의 재활용도 진전되고 있으며, 혼합된 원료로부터의 재료 회수를 위한 선진적인 방법의 시험 운영이 진행되고 있습니다.

미국의 재생 탄소섬유 시장은 2024년 5,850만 달러로 평가되었고, 2034년까지 연평균 14.4% 성장할 것으로 예측됩니다. 수요는 경량화 노력, 전기자동차의 보급 확대, 매립 폐기물에 대한 규제 압력에 의해 주도되고 있습니다. 카본 컨버전스, 발테가와 같은 기업들은 국내 자동차 제조업체와 협력하고, 에너지부는 자동차 재활용 기술 혁신을 지원하고 있습니다. 미국 소재의 산업용 재활용 거점은 OEM 업체들이 순환형 제조 방식을 확대하는 가운데, 생산 규모 확대의 기회를 제공합니다.

세계 재생 탄소섬유 시장의 주요 기업으로는 Vartega, Gen 2 Carbon, Toray Corporation, Carbon Conversions, SGL Carbon 등이 있습니다. 재생 탄소섬유 분야의 기업들은 섬유 회수율 향상, 구조적 무결성 유지, 재생 탄소섬유(rCF)의 품질 향상을 위해 연구개발에 많은 투자를 하고 있으며, 시장에서의 입지를 강화하기 위해 노력하고 있습니다. 자동차 및 항공우주 OEM과의 전략적 제휴를 통해 기업은 장기 공급 계약을 확보하고 생산 규모를 확대할 수 있습니다. 또한, 수요 증가에 대응하기 위해 세계 생산능력을 확대하고, 환경의식이 높은 고객을 확보하기 위해 순환경제를 실천하고 있습니다. 열분해, 용해분해, 저온 처리의 기술 혁신으로 거의 신품과 동등한 품질의 섬유를 확보하여 가전제품이나 스포츠 용품 등 고부가가치 용도로의 진출이 가능해졌습니다.

자주 묻는 질문

목차

제1장 조사 방법

- 시장 범위와 정의

- 조사 설계

- 조사 접근

- 데이터 수집 방법

- 데이터 마이닝 정보원

- 세계

- 지역별/국가별

- 기본 추정치와 계산

- 기준연도 계산

- 시장 추정 주요 동향

- 1차 조사 및 검증

- 1차 정보

- 예측 모델

- 조사의 전제조건과 제한 사항

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급업체 상황

- 이익률

- 각 단계 부가가치

- 밸류체인에 영향을 미치는 요인

- 파괴적 변화

- 업계에 대한 영향요인

- 성장 촉진요인

- 업계의 잠재적 리스크&과제

- 시장 기회

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 가격 동향

- 지역별

- 향후 시장 동향

- 기술과 혁신 동향

- 현재 기술 동향

- 신기술

- 특허 상황

- 무역 통계(주 : 무역 통계는 주요 국가에 한해 제공)

- 주요 수입국

- 주요 수출국

- 지속가능성과 환경적 측면

- 지속가능한 실천

- 폐기물 감축 전략

- 생산 에너지 효율

- 친환경 이니셔티브

- 탄소발자국에 관한 고려사항

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 인수합병(M&A)

- 제휴 및 협력 관계

- 신제품 발매

- 사업 확대 계획

제5장 시장 추산·예측 : 제품 유형별, 2025-2034

- Chopped carbon fiber

- Milled carbon fiber

- Carbon fiber mat

- 기타

제6장 시장 추산·예측 : 소스별, 2025-2034

- 주요 동향

- 자동차 스크랩

- 항공우주 스크랩

- 기타

제7장 시장 추산·예측 : 재활용 방법별, 2025-2034

- 주요 동향

- 기계적 재활용

- 화학적 재활용

- 열분해

- 용해 분해

- 기타

제8장 시장 추산·예측 : 최종 용도별, 2025-2034

- 주요 동향

- 항공우주 및 방위 분야

- 자동차

- 풍력에너지

- 스포츠 및 레저

- 건설

- 전자기기

- 기타

제9장 시장 추산·예측 : 지역별, 2025-2034

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 기타 라틴아메리카

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카공화국

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

제10장 기업 개요

- Gen 2 Carbon

- Carbon Conversions

- Vartega

- SGL Carbon

- Toray Industries

- Mitsubishi Chemical

- Procotex Corporation

- Shocker Composites

- Carbon Fiber Recycling

- CFK Valley Stade

- Zoltek(Toray Group)

- Karborek

- Alpha Recyclage

- Sigmatex

- Carbon Clean Tech

- Recycled Carbon Fiber Ltd

- Composite Recycling Ltd

- Adherent Technologies

- Carbon Fiber Remanufacturing

- Fiberline Composites

The Global Recycled Carbon Fiber Market was valued at USD 248.5 million in 2024 and is estimated to grow at a CAGR of 14.3% to reach USD 986.8 million by 2034.

Market growth is fueled by the increasing push to reduce the environmental impact of primary carbon fiber production, prompting Original Equipment Manufacturers to integrate rCF in electric vehicle components and lightweight automotive interiors. Companies such as Vartega and ELG Carbon Fibre have expanded their production capacities to meet growing demand. Government-backed research initiatives, particularly in the transportation sector, are promoting rCF for enhanced vehicle efficiency and lower emissions. Advances in pyrolysis and solvolysis are enabling longer fiber strands, making structural applications more feasible. Aerospace and automotive industries are scaling the use of rCF in interiors, plastic reinforcements, and underbody components. China has also intensified efforts, developing recycling hubs to manage wind turbine blades and composite waste. The transition from niche applications to scalable commercial production is supported by circular economy policies and cleaner composite processing technologies. Innovations in fiber recovery, including low-temperature pyrolysis and chemical solvolysis, are enhancing fiber length and strength. Companies such as Vartega and Carbon Conversions are producing rCF with near-virgin quality suitable for thermoplastics and sheet molding compounds, enabling applications in high-performance consumer electronics and sporting goods where finish and performance are critical.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $248.5 Million |

| Forecast Value | $986.8 Million |

| CAGR | 14.3% |

The chopped carbon fiber segment was valued at USD 102.9 million in 2024 and is expected to grow at a CAGR of 13.1% through 2034. Chopped and milled rCF is widely used due to its ease of integration with thermoplastics and resins, particularly in automotive and electronics manufacturing. Injection molding of these fibers has enabled mass production of lightweight components, with consistent fiber sizing being a key focus for OEMs.

The automotive scrap-based rCF was valued at USD 117.8 million in 2024, with a projected CAGR of 17% from 2025 to 2034. Rising volumes of automotive and industrial waste, accelerated by the electric vehicle boom and stricter landfill regulations, are driving this segment. Shredded CFRP waste is increasingly processed into chopped and milled fibers for injection molding applications. Wind turbine blade recycling is also gaining traction in Europe, with advanced methods being piloted to recover materials from mixed sources.

U.S. Recycled Carbon Fiber Market was valued at USD 58.5 million in 2024 and is expected to grow at a CAGR of 14.4% through 2034. Demand is driven by lightweighting initiatives, increased EV adoption, and regulatory pressure on landfill waste. Companies like Carbon Conversions and Vartega have partnered with domestic automakers, while the Department of Energy supports innovation in automotive-focused recycling. U.S.-based industrial recycling hubs offer opportunities to scale production as OEMs increasingly adopt circular manufacturing practices.

Key players in the Global Recycled Carbon Fiber Market include Vartega, Gen 2 Carbon, Toray Industries, Carbon Conversions, and SGL Carbon. To strengthen their foothold, companies in the recycled carbon fiber sector are investing heavily in research and development to improve fiber recovery, maintain structural integrity, and enhance the quality of rCF. Strategic partnerships with automotive and aerospace OEMs allow firms to secure long-term supply contracts and scale production. Firms are also expanding their global production capacity to meet rising demand and adopting circular economy practices to attract environmentally conscious clients. Technological innovation in pyrolysis, solvolysis, and low-temperature processing ensures near-virgin quality fibers, enabling entry into high-value applications like consumer electronics and sports equipment.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product Type

- 2.2.3 Source

- 2.2.4 Recycling Method

- 2.2.5 End use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and Environmental Aspects

- 3.12.1 Sustainable Practices

- 3.12.2 Waste Reduction Strategies

- 3.12.3 Energy Efficiency in Production

- 3.12.4 Eco-friendly Initiatives

- 3.13 Carbon Footprint Considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2025 - 2034 (USD Million, Kilo Tons)

- 5.1 Chopped carbon fiber

- 5.2 Milled carbon fiber

- 5.3 Carbon fiber mat

- 5.4 Others

Chapter 6 Market Estimates and Forecast, By Source, 2025 - 2034 (USD Million, Kilo Tons)

- 6.1 Key trends

- 6.2 Automotive scrap

- 6.3 Aerospace scrap

- 6.4 Other

Chapter 7 Market Estimates and Forecast, By Recycling Method, 2025 - 2034 (USD Million, Kilo Tons)

- 7.1 Key trends

- 7.2 Mechanical Recycling

- 7.3 Chemical Recycling

- 7.4 Pyrolysis

- 7.5 Solvolysis

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By End Use, 2025 - 2034 (USD Million, Kilo Tons)

- 8.1 Key trends

- 8.2 Aerospace and Defense

- 8.3 Automotive

- 8.4 Wind Energy

- 8.5 Sports and Leisure

- 8.6 Construction

- 8.7 Electronics

- 8.8 Others

Chapter 9 Market Estimates and Forecast, By Region, 2025 - 2034 (USD Million, Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East & Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East & Africa

Chapter 10 Company Profiles

- 10.1 Gen 2 Carbon

- 10.2 Carbon Conversions

- 10.3 Vartega

- 10.4 SGL Carbon

- 10.5 Toray Industries

- 10.6 Mitsubishi Chemical

- 10.7 Procotex Corporation

- 10.8 Shocker Composites

- 10.9 Carbon Fiber Recycling

- 10.10 CFK Valley Stade

- 10.11 Zoltek (Toray Group)

- 10.12 Karborek

- 10.13 Alpha Recyclage

- 10.14 Sigmatex

- 10.15 Carbon Clean Tech

- 10.16 Recycled Carbon Fiber Ltd

- 10.17 Composite Recycling Ltd

- 10.18 Adherent Technologies

- 10.19 Carbon Fiber Remanufacturing

- 10.20 Fiberline Composites