|

시장보고서

상품코드

1885891

발효 유래 단백질 시장 : 기회, 성장 요인, 업계 동향 분석 및 예측(2025-2034년)Fermentation-Derived Proteins Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

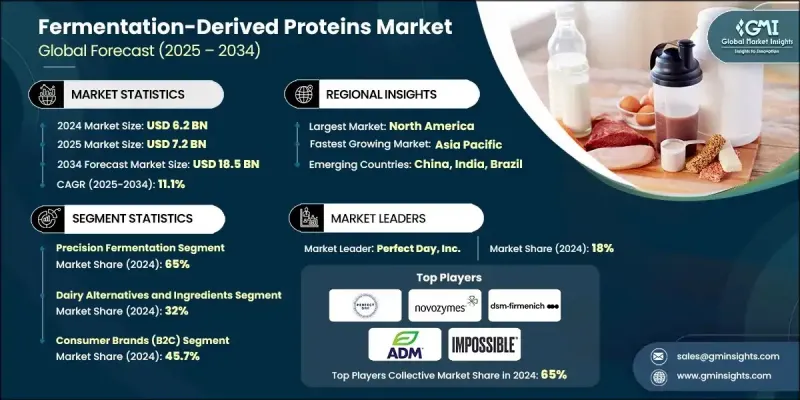

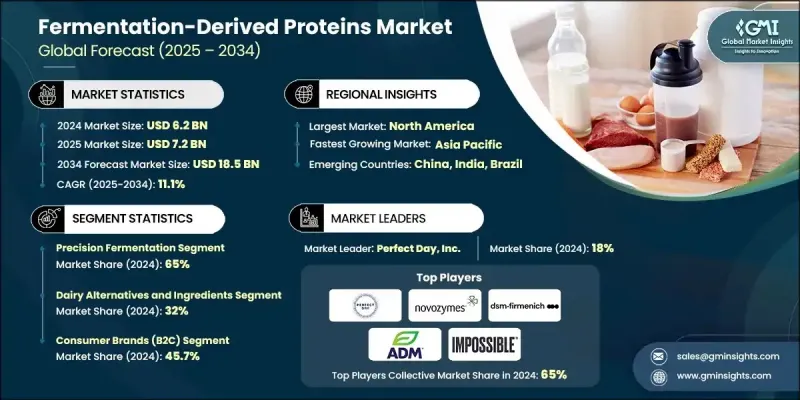

세계의 발효 유래 단백질 시장은 2024년에 62억 달러로 평가되었고, 2034년까지 연평균 복합 성장률(CAGR)은 11.1%를 나타낼 것으로 예측되며 185억 달러로 성장할 전망입니다.

기후 변화 압박이 심화되고 식품 부문이 기존 축산업에서 벗어나기 위해 가속화됨에 따라, 광범위한 단백질 환경은 점점 더 발효 기반 시스템으로 전환되고 있습니다. 발효 기술의 상업적 채택은 유제품, 육류, 계란 단백질의 특성을 재현하는 대체품 생산을 기업들이 확대함에 따라 급속히 확대되었습니다. 투자 유입은 쿼른(Quorn), 임파서블 푸즈(Impossible Foods), 퍼펙트 데이(Perfect Day)와 같은 선도적 혁신 기업의 시장 입지를 강화한 반면, ADM 및 DSM-피르메니히(DSM-Firmenich)를 포함한 주요 글로벌 식품 그룹들은 산업적 통합을 개선하기 위해 협력을 심화했습니다. 온실가스 감축 및 토지 이용 효율성 등 지속가능성 문제가 이러한 전환을 뒷받침하고 있으며, 2021년 이후 발표된 연구들은 발효 유래 단백질이 전통적 가축 시스템 대비 환경적 이점을 일관되게 입증하고 있습니다. 항생제 사용 및 인수공통감염 위험에 대한 공론화는 기후 및 식량 안보 정책 기획의 전략적 컴포넌트로서 발효 기술에 대한 관심을 더욱 촉진하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 가치 | 62억 달러 |

| 예측 가치 | 185억 달러 |

| CAGR | 11.1% |

정밀 발효 부문은 2024년 65%의 점유율을 기록했으며, 2034년까지 연평균 10.9%의 성장률을 보일 것으로 예상됩니다. 기업들은 정밀 발효, 바이오매스 발효, 전통적 발효 플랫폼을 활용해 필수적인 거품 형성, 겔화, 용융 특성을 제공하는 고기능성 단백질을 개발합니다. 이러한 원료는 개선된 식감, 감각적 성능, 영양가를 갖춘 클린 라벨 재구성을 추구하는 소비재 기업들에 채택되고 있습니다.

유제품 대체품 및 원료 응용 부문은 2024년 32%의 점유율을 기록했으며, 2034년까지 연평균 8.6%의 성장률을 보일 것으로 예상됩니다. 발효 유래 원료는 음료, 제빵 제품, 육류 대체품, 유제품 대체품 등 다양한 부문에서 동물성 단백질의 성능을 따라잡거나 능가할 수 있습니다. 브랜드들은 특히 소스, 냉동 디저트, 즉석 음료 제형과 같은 품목에서 입안감 향상, 유화력 강화, 성분 목록 간소화, 규제 기준 충족을 위해 이러한 단백질을 제품에 통합합니다.

북미의 발효 유래 단백질 시장은 2024년 23억 달러를 기록했으며, 2034년까지 69억 달러에 달할 것으로 전망됩니다. 이 지역은 강력한 연구개발 인프라, 조기 상용화 경로, 활발한 벤처 캐피털 활동, 수용적인 유통망을 바탕으로 대체 유제품, 계란, 육류 제품 전반에 걸친 채택을 가속화하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 각 단계의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 지속 가능하고 동물 유래가 아닌 단백질 솔루션에 대한 수요 증가

- 정밀 발효 및 균주 공학의 발전

- 세계적인 식품 및 음료 기업과의 전략적 제휴

- 업계의 잠재적 위험 및 과제

- 높은 생산량과 설비 투자의 필요성

- 규제 불확실성과 승인 공정 지연

- 시장 기회

- 증가하는 기업의 기후 및 ESG 약속

- 신흥 시장 및 응용 부문의 미개척 가능성

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 가격 동향

- 지역별

- 원료별

- 장래 시장 동향

- 기술과 혁신 동향

- 현재의 기술 동향

- 신흥기술

- 특허 동향

- 무역 통계(HS코드)(참고 : 무역 통계는 주요 국가에서만 제공됨)

- 주요 수입국

- 주요 수출국

- 지속가능성과 환경면

- 지속가능한 대처

- 폐기물 감축 전략

- 생산의 에너지 효율

- 환경에 배려한 대처

- 탄소발자국 고려

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병 및 인수

- 제휴 및 협업

- 신제품 발매

- 사업 확대 계획

제5장 시장 추계 및 예측 : 발효 공정별(2021-2034년)

- 주요 동향

- 정밀 발효

- 우유 단백질

- 계란 단백질

- 기능성 및 특수 단백질

- 풍미 및 향기 단백질/화합물

- 바이오매스 발효

- 균류 단백질

- 효모 또는 박테리아 기반 바이오매스

- 가스 또는 비기존 원료로부터 단세포 단백질

- 기존/혼합 발효

- 발효 식물성 단백질 매트릭스

- 동물 또는 식물 유래 원료를 이용 하이브리드 발효

제6장 시장 추계 및 예측 : 용도별(2021-2034년)

- 주요 동향

- 유제품 대체품 및 원료

- 계란 대체품 및 기능성 계란 원료

- 고기 및 어패류 대체품

- 베이커리, 과자류, 디저트

- 음료 및 영양제품

- 외식산업용 및 공업용 원료

제7장 시장 추계 및 예측 : 유통 채널별(2021-2034년)

- 주요 동향

- 소비자용 브랜드(B2C)

- 원료 및 제형 공급업체(B2B)

- 위탁 개발 제조기관(CDMO)

- 사료 및 반려동물 식품 제조 업체

제8장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 기타 라틴아메리카

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

제9장 기업 프로파일

- Perfect Day, Inc.

- The EVERY Company

- Impossible Foods Inc.

- Nature’s Fynd

- The Better Meat Co.

- Solar Foods Oy

- TurtleTree Labs

- Formo

- Onego Bio

- Standing Ovation

- Quorn Foods

- Givaudan(including Naturals &Ingredients)

- Novozymes A/S

- ADM(Archer Daniels Midland)

- DSM-Firmenich

- Kerry Group

- Cargill

- Corbion

- DuPont(IFF)

- Calysta

The Global Fermentation-Derived Proteins Market was valued at USD 6.2 billion in 2024 and is estimated to grow at a CAGR of 11.1% to reach USD 18.5 billion by 2034.

The broader protein landscape is increasingly shifting toward fermentation-based systems as climate pressures intensify and the food sector accelerates its move away from conventional animal agriculture. Commercial adoption of fermentation technologies has expanded rapidly as companies scale production of alternatives that replicate the characteristics of dairy, meat, and egg proteins. Investment inflows have strengthened the market presence of leading innovators such as Quorn, Impossible Foods, and Perfect Day, while major global food groups-including ADM and DSM-Firmenich have deepened collaboration to improve industrial integration. Sustainability concerns, including greenhouse gas reduction and land-use efficiency, have supported the transition, as research published after 2021 consistently demonstrates the environmental advantages of fermentation-derived proteins compared to traditional livestock systems. Public conversations about antibiotic use and zoonotic risks have driven further interest in fermentation technologies as a strategic component in climate and food-security policy planning.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $6.2 Billion |

| Forecast Value | $18.5 Billion |

| CAGR | 11.1% |

The precision fermentation segment held a 65% share in 2024 and is estimated to grow at a CAGR of 10.9% through 2034. Companies rely on precision, biomass, and traditional fermentation platforms to develop highly functional proteins that provide essential foaming, gelling, and melting characteristics. These ingredients are adopted by consumer product firms seeking clean-label reformulations with improved texture, sensory performance, and nutritional value.

The dairy alternatives and ingredient applications segment accounted for a 32% share in 2024 and is expected to grow at an 8.6% CAGR toward 2034. Fermentation-derived ingredients can match or exceed the performance of animal-based proteins across categories such as beverages, baked goods, meat substitutes, and dairy alternatives. Brands integrate these proteins into products to enhance mouthfeel, strengthen emulsification, simplify ingredient lists, and meet regulatory standards, especially in items like sauces, frozen desserts, and ready-to-drink formulations.

North America Fermentation-Derived Proteins Market generated USD 2.3 billion in 2024 and is forecast to reach USD 6.9 billion by 2034. The region benefits from strong R&D infrastructure, early commercialization pathways, robust venture capital activity, and receptive distribution networks that accelerate adoption across alternative dairy, egg, and meat products.

Key companies active in the Global Fermentation-Derived Proteins Market include The Better Meat Co., ADM (Archer Daniels Midland), Givaudan, DuPont (IFF), Solar Foods Oy, Perfect Day, Inc., TurtleTree Labs, Quorn Foods, Kerry Group, Standing Ovation, Novozymes A/S, DSM-Firmenich, Cargill, Calysta, Onego Bio, Impossible Foods Inc., Nature's Fynd, Formo, EVERY Company, and Corbion. Companies in the Fermentation-Derived Proteins Market are strengthening their competitive position through aggressive capacity expansion, product diversification, and long-term partnerships with major food and beverage manufacturers. Many are developing proprietary fermentation strains to improve yield, reduce cost, and create differentiated functional proteins. Strategic collaborations with ingredient suppliers and CPG brands help accelerate formulation adoption while reinforcing supply chain stability.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Fermentation Process

- 2.2.3 Application

- 2.2.4 Distribution Channel

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing demand for sustainable, animal-free protein solutions

- 3.2.1.2 Advances in precision fermentation and strain engineering

- 3.2.1.3 Strategic partnerships with global food and beverage players

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High production and capital expenditure requirements

- 3.2.2.2 Regulatory uncertainty and slow approval pathways

- 3.2.3 Market opportunities

- 3.2.3.1 Rising corporate climate and ESG commitments

- 3.2.3.2 Untapped potential in emerging markets and applications

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By Source

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) ( Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Fermentation Process, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Precision fermentation

- 5.2.1 Dairy proteins

- 5.2.2 Egg proteins

- 5.2.3 Functional and specialty proteins

- 5.2.4 Flavor and aroma proteins/compounds

- 5.3 Biomass fermentation

- 5.3.1 Mycoprotein

- 5.3.2 Yeast- or bacterial-based biomass

- 5.3.3 Single-cell protein from gases or unconventional feedstocks

- 5.3.4 Traditional / mixed fermentation

- 5.3.5 Fermented plant-based protein matrices

- 5.3.6 Hybrid fermentation with animal or plant inputs

Chapter 6 Market Estimates and Forecast, By Application, 2021-2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Dairy alternatives and ingredients

- 6.3 Egg alternatives and functional egg ingredients

- 6.4 Meat and seafood alternatives

- 6.5 Bakery, confectionery, and desserts

- 6.6 Beverages and nutrition products

- 6.7 Food service and industrial ingredients

Chapter 7 Market Estimates and Forecast, By Distribution Channel, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Consumer brands (B2C)

- 7.3 Ingredient and formulation suppliers (B2B)

- 7.4 Contract development and manufacturing organizations (CDMOs)

- 7.5 Feed and pet food manufacturers

Chapter 8 Market Estimates and Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Perfect Day, Inc.

- 9.2 The EVERY Company

- 9.3 Impossible Foods Inc.

- 9.4 Nature’s Fynd

- 9.5 The Better Meat Co.

- 9.6 Solar Foods Oy

- 9.7 TurtleTree Labs

- 9.8 Formo

- 9.9 Onego Bio

- 9.10 Standing Ovation

- 9.11 Quorn Foods

- 9.12 Givaudan (including Naturals & Ingredients)

- 9.13 Novozymes A/S

- 9.14 ADM (Archer Daniels Midland)

- 9.15 DSM-Firmenich

- 9.16 Kerry Group

- 9.17 Cargill

- 9.18 Corbion

- 9.19 DuPont (IFF)

- 9.20 Calysta