|

시장보고서

상품코드

1892648

스마트 물류 플랫폼 시장 기회, 성장요인, 업계 동향 분석 및 예측(2025-2034년)Smart Logistics Platforms Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

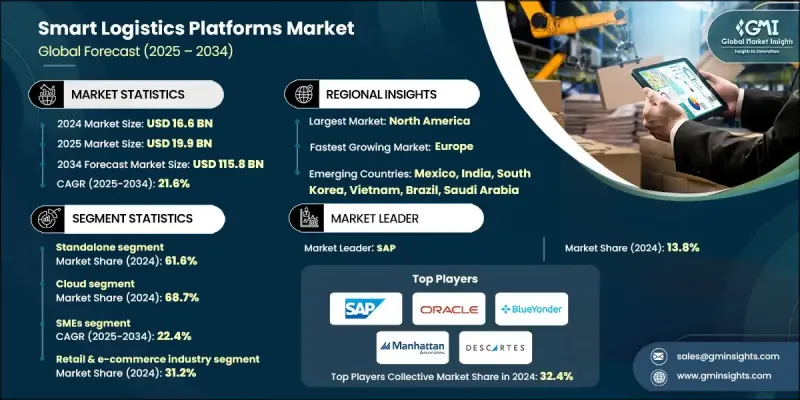

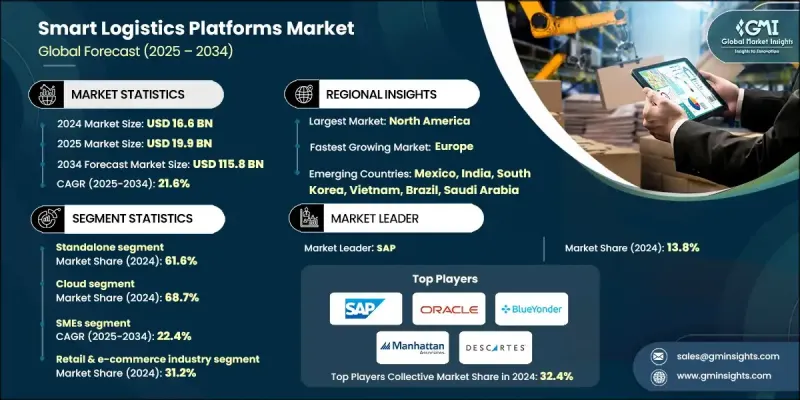

세계의 스마트 물류 플랫폼 시장은 2024년에 166억 달러로 평가되었고, 2034년까지 연평균 복합 성장률(CAGR) 21.6%로 성장하여 1,158억 달러에 이를 것으로 예측됩니다.

세계 무역이 확대됨에 따라 차량 관리, 실시간 추적, 경로 최적화, 재고 관리, 창고 관리와 같은 첨단 물류 솔루션에 대한 수요가 증가하고 있습니다. 기업들은 복잡한 공급망 전반에서 업무 효율성과 가시성을 높이기 위해 이러한 플랫폼 도입을 가속화하고 있습니다. 기업은 단일 플랫폼에서 여러 기능을 제공하는 통합형 솔루션과 업무 요구사항에 따라 특정 업무에 특화된 독립형 솔루션 중 하나를 선택할 수 있습니다. 인공지능(AI)과 머신러닝은 경로 최적화, 예측 분석 정확도 향상, 보안 강화, 사이버 위협 방지를 통해 시장 성장을 더욱 가속화하고 있습니다. 북미와 유럽은 세계 수출에 대한 막대한 투자로 인해 계속해서 선두를 유지할 것으로 예상되지만, 아시아태평양은 수출 지향적 경제의 확대에 힘입어 가장 빠르게 성장하는 시장으로 부상하고 있습니다. 중국, 미국, 독일이 세계 무역을 주도하고 있으며, 국제 공급망을 효과적으로 관리할 수 있는 혁신적인 물류 솔루션에 대한 강력한 수요를 창출하고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2024년 |

| 예측 기간 | 2025-2034년 |

| 개시 연도 시장 규모 | 166억 달러 |

| 예측 금액 | 1,158억 달러 |

| CAGR | 21.6% |

독립형 부문은 2024년 61.6%의 점유율을 차지했습니다. 빠른 도입과 낮은 초기 비용, 그리고 경로 최적화, 차량 모니터링, 창고 가시성 등 특정 물류 기능을 전체 시스템 통합 없이도 처리할 수 있다는 점이 인기의 이유입니다. 이 솔루션은 사용자 정의가 가능하고 도입이 용이하며, 빠르고 집중적인 결과를 필요로 하는 기업에 적합합니다.

클라우드 도입 부문은 2024년 68.7%의 점유율을 차지했습니다. 클라우드 플랫폼은 실시간 추적, 확장성 있는 운영, AI 기반 분석 기능으로 인해 널리 선호되고 있습니다. 파트너 간의 원활한 협업을 가능하게 하고, 공급망 가시성을 높여 물류 사업자가 대규모 On-Premise 인프라를 구축하지 않고도 변동하는 수요에 효과적으로 대응할 수 있도록 지원합니다.

미국의 스마트 물류 플랫폼 시장은 2024년 69억 달러에 달했습니다. 국내총생산(GDP)의 8-10% 이상을 차지하는 높은 물류비용은 경로 최적화, 자원 낭비 감소, 업무 효율성 향상을 실현하는 AI 탑재 플랫폼 도입을 촉진하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

- 시장 범위와 정의

- 조사 설계

- 조사 접근

- 데이터 수집 방법

- 데이터 마이닝 소스

- 세계

- 지역별/국가별

- 기본 추정치와 계산

- 기준연도 계산

- 시장 추정 주요 동향

- 1차 조사와 검증

- 1차 정보

- 예측

- 조사의 전제조건과 제한 사항

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급업체 상황

- 이익률

- 비용 구조

- 각 단계별 부가가치

- 밸류체인에 영향을 미치는 요인

- 파괴적 변화

- 업계에 대한 영향요인

- 성장 촉진요인

- 업계의 잠재적 리스크&과제

- 시장 기회

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 기술과 혁신 동향

- 현재 기술 동향

- 신기술

- 기술 로드맵과 진화

- 테크놀러지 도입 수명주기 분석

- 가격 동향

- 지역별

- 제품별

- 특허 분석

- 사이버 보안과 데이터 거버넌스 현황

- 고객 과제점과 워크플로우 최적화 분석

- 도입 사례와 성공 지표

- 베스트 케이스 시나리오

- 디지털 전환 경제성과 총 소유비용(TCO) 분석

- 클라우드 마이그레이션 비용 효율 분석

- SaaS와 영구 라이선스 TCO 비교

- 도입 비용과 전문 서비스

- 변경 관리와 연수 투자

- 사이버 보안 아키텍처와 데이터 프라이버시 프레임워크

- 클라우드 보안과 멀티 테넌트 분리

- 데이터 암호화

- ID 및 액세스 관리(IAM)

- GDPR(EU 개인정보보호규정), CCPA 및 국경간 데이터 규제

- 공급망 사이버 위협과 공격 벡터

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- LATAM

- 중동 및 아프리카

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

- 주요 발전

- 인수합병(M&A)

- 제휴 및 협업

- 신제품 발매

- 사업 확대 계획과 자금조달

- 벤더 선정 기준

- 공급망 및 파트너 생태계 분석

제5장 시장 추산 및 예측 : 솔루션별, 2021-2034

- 주요 동향

- 스탠드얼론

- 통합형

제6장 시장 추산 및 예측 : 도입 모델별, 2021-2034

- 주요 동향

- On-Premise

- 클라우드

- 프라이빗 클라우드

- 퍼블릭 클라우드

- 하이브리드 클라우드

- 하이브리드

제7장 시장 추산 및 예측 : 기업 규모별, 2021-2034

- 주요 동향

- 중소기업

- 대기업

제8장 시장 추산 및 예측 : 최종 용도별, 2021-2034

- 주요 동향

- 소매업 및 전자상거래

- 제조업

- 제3자 물류

- 식품 및 음료

- 의약품

- 기타

제9장 시장 추산 및 예측 : 지역별, 2021-2034

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 북유럽 국가

- 베네룩스

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- ANZ

- 싱가포르

- 말레이시아

- 인도네시아

- 베트남

- 태국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 콜롬비아

- 중동 및 아프리카

- 남아프리카공화국

- 사우디아라비아

- 아랍에미리트(UAE)

제10장 기업 개요

- Global companies

- Manhattan Associates

- SAP

- Oracle

- Blue Yonder

- Uber Freight

- Kinaxis

- E2 open

- Infor

- Descartes Systems

- HighJump

- Magaya Supply Chain

- LogiNext Mile

- Alpega

- Honeywell

- Regional companies

- Project44

- FourKites

- C.H. Robinson Worldwide

- XPO Logistics

- J.B. Hunt Transport Services

- Transporeon

- Trimble Transportation

- Samsara

- Emerging companies

- Flexport

- Convoy

- Waymo Via

- Starship Technologies

- Waabi

- Nuro

- Loadsmart

The Global Smart Logistics Platforms Market was valued at USD 16.6 billion in 2024 and is estimated to grow at a CAGR of 21.6% to reach USD 115.8 billion by 2034.

The expansion of global trade is fueling the need for advanced logistics solutions, including fleet management, live tracking, route optimization, inventory control, and warehouse management. Companies are increasingly adopting these platforms to streamline operations, enhance efficiency, and improve visibility across complex supply chains. Businesses can choose between integrated solutions, which offer multiple functionalities within a single platform, and standalone solutions, which focus on specific tasks tailored to operational requirements. Artificial intelligence and machine learning are further accelerating market growth by optimizing routes, improving predictive analytics, strengthening security, and preventing cyber threats. North America and Europe are expected to remain leaders due to substantial investments in global exports, while the Asia-Pacific region is emerging as the fastest-growing market, driven by the expansion of export-oriented economies. China, followed by the U.S. and Germany, dominates global trade, creating strong demand for innovative logistics solutions to manage international supply chains effectively.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $16.6 Billion |

| Forecast Value | $115.8 Billion |

| CAGR | 21.6% |

The standalone segment held a 61.6% share in 2024. Its popularity is attributed to faster deployment, lower initial costs, and the ability to handle specific logistics functions such as route optimization, fleet monitoring, and warehouse visibility without full system integration. These solutions are customizable, easy to implement, and ideal for businesses requiring quick, focused results.

The cloud deployment segment held a 68.7% share in 2024. Cloud platforms are widely preferred for their real-time tracking, scalable operations, and AI-driven analytics. They enable seamless collaboration among partners, enhance supply chain visibility, and allow logistics providers to respond effectively to fluctuating demand without heavy on-premises infrastructure.

U.S. Smart Logistics Platforms Market reached USD 6.9 billion in 2024. High logistics costs, which account for more than 8-10% of the national GDP, have driven the adoption of AI-powered platforms that optimize routes, reduce resource waste, and improve operational efficiency.

Key players in the Smart Logistics Platforms Market include Blue Yonder, SAP, Oracle, Manhattan Associates, Descartes Systems, LogiNext Mile, Honeywell, Magaya Supply Chain, Alpega, and Infor. Companies in the Global Smart Logistics Platforms Market are focusing on AI and ML integration to enhance predictive analytics, optimize fleet management, and strengthen cybersecurity. Cloud-based platform development is prioritized to improve scalability, real-time collaboration, and global supply chain visibility. Strategic partnerships with logistics providers, manufacturers, and technology firms help expand market reach and foster innovation. Firms are investing in R&D to introduce customizable and modular solutions that meet diverse client needs. Market players are also emphasizing digital transformation, offering IoT-enabled platforms to track shipments, monitor inventory, and reduce operational inefficiencies.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Solution

- 2.2.3 Deployment model

- 2.2.4 Enterprise size

- 2.2.5 End use

- 2.3 TAM analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 E-Commerce growth & omnichannel Fulfilment demands

- 3.2.1.2 Supply chain visibility & resilience imperatives

- 3.2.1.3 Labor shortages & automation adoption

- 3.2.1.4 Cloud adoption & digital transformation mandates

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial implementation costs & TCO concerns

- 3.2.2.2 Data security & privacy compliance burden

- 3.2.3 Market opportunities

- 3.2.3.1 Autonomous logistics & hybrid human-robot networks

- 3.2.3.2 Generative AI for operational assistance

- 3.2.3.3 Last-mile delivery innovation

- 3.2.3.4 Landlocked & least developed country (LDC) logistics digitization

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.7.3 Technology roadmaps & evolution

- 3.7.4 Technology adoption lifecycle analysis

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Patent analysis

- 3.10 Cybersecurity & data governance landscape

- 3.11 Customer pain points & workflow optimization analysis

- 3.11.1 Visibility gap & real-time tracking challenges

- 3.11.2 Manual processes & data entry inefficiencies

- 3.11.3 Carrier capacity constraints & freight procurement

- 3.11.4 Last-Mile delivery cost & customer experience

- 3.11.5 Inventory accuracy & warehouse labor productivity

- 3.12 Case studies & implementation success metrics

- 3.13 Best case scenarios

- 3.14 Digital transformation economics & TCO analysis

- 3.14.1 Cloud migration cost-benefit analysis

- 3.14.2 SaaS vs perpetual license TCO comparison

- 3.14.3 Implementation costs & professional services

- 3.14.4 Change management & training investments

- 3.15 Cybersecurity architecture & data privacy framework

- 3.15.1 Cloud security & multi-tenant isolation

- 3.15.2 Data Encryption

- 3.15.3 Identity & access management (IAM)

- 3.15.4 GDPR, CCPA & cross-border data regulations

- 3.15.5 Supply chain cyber threats & attack vectors

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

- 4.7 Vendor selection criteria

- 4.8 Supply chain & partner ecosystem analysis

Chapter 5 Market Estimates & Forecast, By Solution, 2021 - 2034 ($Mn)

- 5.1 Key trends

- 5.2 Standalone

- 5.3 Integrated

Chapter 6 Market Estimates & Forecast, By Deployment Model, 2021 - 2034 ($Mn)

- 6.1 Key trends

- 6.2 On-premises

- 6.3 Cloud

- 6.3.1 Private Cloud

- 6.3.2 Public Cloud

- 6.3.3 Hybrid Cloud

- 6.4 Hybrid

Chapter 7 Market Estimates & Forecast, By Enterprise Size, 2021 - 2034 ($Mn)

- 7.1 Key trends

- 7.2 SME

- 7.3 Large Enterprises

Chapter 8 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Mn)

- 8.1 Key trends

- 8.2 Retail & E-commerce

- 8.3 Manufacturing

- 8.4 Third party logistics

- 8.5 Food & Beverage

- 8.6 Pharmaceuticals

- 8.7 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.3.8 Benelux

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Singapore

- 9.4.7 Malaysia

- 9.4.8 Indonesia

- 9.4.9 Vietnam

- 9.4.10 Thailand

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Colombia

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global companies

- 10.1.1 Manhattan Associates

- 10.1.2 SAP

- 10.1.3 Oracle

- 10.1.4 Blue Yonder

- 10.1.5 Uber Freight

- 10.1.6 Kinaxis

- 10.1.7. E2 open

- 10.1.8 Infor

- 10.1.9 Descartes Systems

- 10.1.10 HighJump

- 10.1.11 Magaya Supply Chain

- 10.1.12 LogiNext Mile

- 10.1.13 Alpega

- 10.1.14 Honeywell

- 10.2 Regional companies

- 10.2.1 Project44

- 10.2.2 FourKites

- 10.2.3 C.H. Robinson Worldwide

- 10.2.4 XPO Logistics

- 10.2.5 J.B. Hunt Transport Services

- 10.2.6 Transporeon

- 10.2.7 Trimble Transportation

- 10.2.8 Samsara

- 10.3 Emerging companies

- 10.3.1 Flexport

- 10.3.2 Convoy

- 10.3.3 Waymo Via

- 10.3.4 Starship Technologies

- 10.3.5 Waabi

- 10.3.6 Nuro

- 10.3.7 Loadsmart