|

시장보고서

상품코드

1910607

의약품 물류 시장 : 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Pharmaceutical Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

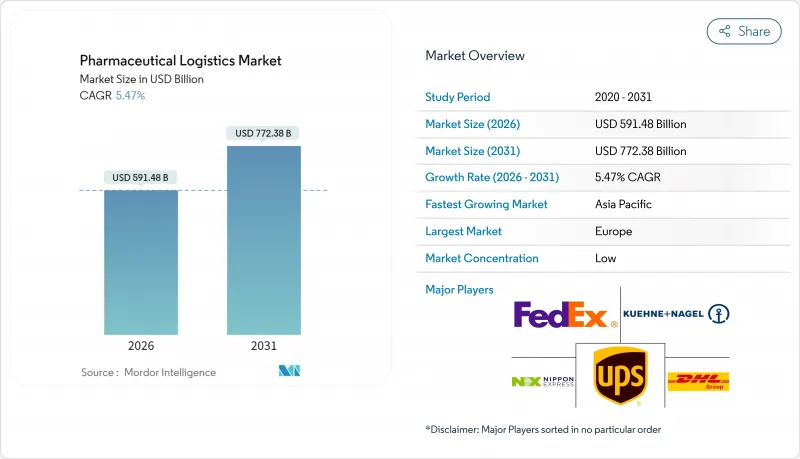

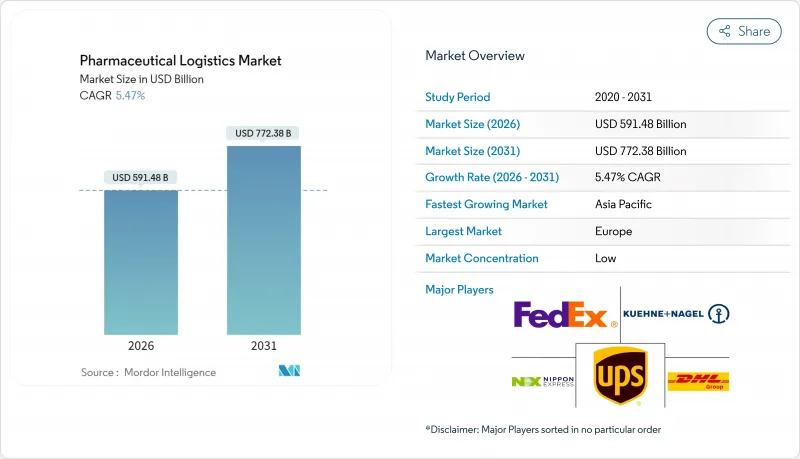

세계의 의약품 물류 시장은 2025년 5,608억 1,000만 달러로 평가되었으며, 2026년 5,914억 8,000만 달러에서 2031년까지 7,723억 8,000만 달러에 이를 것으로 예측됩니다. 예측 기간 중(2026-2031년) CAGR은 5.47%로 예상됩니다.

견고한 성장은 생물학적 제형의 보급, 엄격한 직렬화 의무 및 정밀한 유통 능력을 필요로 하는 환자 직접 배송 모델로의 전환에 기인합니다. 세계 통합사업자들의 강력한 설비투자, 지속적인 전자 약국의 도입, 온도관리 인프라의 확대는 경쟁을 격화시키고 있는 한편, 엔드 투 엔드에서 컴플라이언스를 준수하는 공급망 솔루션에 대한 잠재적인 수요를 확대하고 있습니다. 기술 도입, 특히 IoT 센서, 블록체인에 의한 추적성, AI 구동 네트워크 최적화는 이해관계자가 온도 편차와 위조 위험을 방지하기 위해 가속화되고 있습니다. 동시에 배출량 저감을 위한 지속가능성에 대한 노력은 운송수단을 복합수송과 해상수송으로 전환시켜 전문 서비스 제공업체에게 새로운 틈새 시장을 개척하고 있습니다. 콜드체인의 에너지 비용과 여러 관할 구역에 걸친 컴플라이언스와 관련된 가격 압력은 여전히 역풍이지만, 저탄소 포장, 지역별 재고 관리, 대체 연료에 대한 투자를 촉진하고 결국 의약품 물류 시장의 확대로 이어지고 있습니다.

세계의 의약품 물류 시장 동향과 통찰

온라인 약국 확대

현재 소비자의 거의 절반이 의약품의 온라인 주문을 선호하고 있으며, 운송업자에게는 온도 관리가 중요한 제품을 위해 2-8℃의 환경을 보장하는 문앞 배송 네트워크의 구축이 요구되고 있습니다. 아시아태평양 공급자는 디지털 결제와 원격 의료 플랫폼을 활용하여 상온 및 냉장 소포 서비스의 확대를 도모하고 있습니다. 반면 미국의 통합 사업자는 IoT 지원 포장 솔루션을 통해 라스트 마일 가시성을 높이고 있습니다. 규제 당국은 이에 대응해, 직렬화와 추적 관리를 단품 레벨까지 확대하빈다. 컴플라이언스 장애물은 높아지는 반면 실시간 온도 및 위치 데이터를 제공하는 사업자의 차별화도 진행되고 있습니다. 전자 약국의 취급량이 증가하는 가운데, 마이크로풀필먼트 허브를 향한 네트워크 재설계에 의해 리드 타임이 단축되어, 복약 준수율이 향상되고 의약품 물류 시장 전체에서 수요 증가를 추진하고 있습니다.

OTC 의약품 수요 증가와 만성 질환 부담

OTC 의약품은 처방약에 비해 취급 규칙이 덜 엄격하기 때문에 통합형 유통업체의 보관 비용 절감으로 이어지는 혼합 수송 루트가 가능해집니다. 그러나 당뇨병과 심혈관 질환의 유병률 상승으로 지속적인 보충 사이클이 요구되고 시간 엄수 재고의 처리 능력 요건이 강화되고 있습니다. 물류 파트너는 로봇에 의한 피킹 및 패킹이나 스마트 블리스터 포장 등의 자동화 기술을 활용해 OTC 의약품과 만성 질환 치료제을 통합 플로우로 조합함으로써 체류 시간을 삭감하고 있습니다. 하이브리드 모델은 의약품 물류 시장에서 자산 활용률을 높이고 수익성을 유지하는 동시에 약국과 클리닉에 대한 서비스 품질을 향상시킵니다.

온도 관리 배송의 높은 비용

콜드체인 장애는 의약품 제조업체에 연간 350억 달러의 손실을 초래합니다. 이것은 폐기 처리, 재포장, 벌칙 첨부 배송 등을 반영한 금액입니다. 상변화물질를 이용한 패시브 포장은 보호 시간을 96시간까지 연장 가능하지만, 소포당의 비용을 크게 증가시키는 경우가 많아, 자금이 한정되는 신흥 시장용 프로그램에 부담을 가하고 있습니다. 중복 감시 장비와 자격을 갖춘 직원의 필요성은 간접비를 증가시키고 의약품 물류 시장에서 중소 운송업체의 이익률을 제한합니다. 저탄소 냉매와 재사용 가능한 토트백의 혁신은 운송 비용 절감을 목표로 하지만 초기 투자액이 장벽이 되고 광범위한 도입은 여전히 제약을 받고 있습니다.

부문 분석

운송 부문은 2025년 수익의 51.40%를 차지했으며 물리적 이동이 의약품 물류 시장의 핵심임을 보여줍니다. 도로화물 운송은 지역 간 유통, 특히 유럽과 북미를 연결하는 흐름을 담당하고, 항공화물 운송은 익일 배송 보증에 의한 장거리 바이오 의약품 보충을 지원합니다. 해운 루트는 배출량 감축을 위해 GDP에 준거한 냉장 컨테이너를 활용하는 화주가 지속 가능한 선택을 추구하는 중 중요성을 늘리고 있습니다.

부가가치 서비스는 CAGR 4.42%로 확대되고 있으며, 라벨 부착, 2차 포장, 주문 키트화, 직렬화 컨설팅 등이 포함되어 제조업체의 비중핵 업무 부담을 경감합니다. 수요가 가장 빠르게 성장하고 있는 것은 아시아태평양이며, 계약 제조 업체는 다국어 규제 인쇄를 처리할 수 있는 단일 소스 파트너를 찾고 있습니다. 데이터 무결성에 대한 규제가 강화됨에 따라 인증된 재라벨 부착 및 변조 방지 포장은 옵션 추가 서비스에서 조달 전제조건으로 변화하여 의약품 물류 시장 전반에 걸친 이익률 향상을 촉진하고 있습니다.

지역별 분석

유럽은 2025년에도 31.70%의 수익 점유율을 유지했습니다. 이것은 조화로운 GDP 시행, 조밀한 도로망, 독일, 스위스, 아일랜드의 대규모 제조 클러스터에 의해 지원되었습니다. 국경을 넘은 철도 및 항공 회랑에 대한 투자는 리드 타임을 손상시키지 않고 배출량을 삭감하는 모달 시프트를 지원하고 있습니다. 유럽의 의약품 물류 시장 규모는 Cold Chain Technologies의 네덜란드 신허브 등 지속적인 용량 증강의 혜택을 받고 있으며, 이로써 지역의 PCM 생산이 강화되어 운송 리스크가 저감됩니다.

북미는 DSCSA(의약품안전공급법)에 근거한 시리얼화 시스템의 성숙도와 팬데믹 대책에 지속적인 공적 자금 투입에 의해 계속해서 주요 시장으로서의 지위를 유지하고 있습니다. DHL은 20억 유로(20억 8,000만 달러) 계획의 50%를 미국/캐나다 시설에 배분하고 서비스 수준을 유지하면서 배출량을 억제하는 태양광 발전 창고와 LNG 트럭을 도입했습니다. FedEx의 4억 4,000만 달러 규모 의료 유통 센터 확장과 함께 이 지역은 데이터 가시성과 지속가능성에 대한 모범 사례를 재정의하고 있습니다.

아시아태평양은 중국과 인도의 생산 증가, 보험 적용 범위 확대, 전자 약국의 보급에 힘입어 2026년부터 2031년까지 5.02%의 연평균 복합 성장률(CAGR)로 가장 빠른 성장이 전망되고 있습니다. 인도는 2025년 GDP 준수 창고 시설에 세금 환급을 하는 등 각국 정부는 콜드체인 업그레이드를 장려하고 있습니다. 지역 운송업체는 중국과 유럽을 연결하는 회랑을 따라 철도, 트럭, 해상 및 항공의 복합 운송 솔루션을 도입하여 비용 절감과 운송 중 배출 가스를 줄이기 위해 노력하고 있습니다. 중동 및 아프리카는 인프라 정비가 늦었지만 걸프 협력 회의(GCC)의 현지화 프로그램이 창고 투자를 자극하고 미래의 의약품 물류 시장 확대를 확보하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 온라인 약국 확대

- OTC 의약품 수요 증가와 만성 질환의 부담 증가

- 생물 제제 및 백신용 콜드체인 수요의 가속

- 3PL/4PL 전문업체에 아웃소싱 급증

- 필수 엔드 투 엔드 IoT/블록체인 추적 시스템

- 넷 제로 물류 투자에 의한 인프라 갱신의 추진

- 시장 성장 억제요인

- 온도 관리 배송의 고비용

- 복잡하고 다양화하는 세계의 컴플라이언스 기준

- 고급 상변화 포장재 부족

- 신흥 시장에서 라스트 마일 생물 제제 배송의 병목

- 가치/공급망 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

- COVID-19 및 지정학적 이벤트의 영향

제5장 시장 규모와 성장 예측

- 서비스 유형별

- 교통기관

- 도로화물 운송

- 항공화물

- 해상 운송

- 철도화물 운송

- 창고 보관 및 저장

- 부가가치 서비스 및 기타

- 교통기관

- 운용 모드별

- 콜드체인 물류

- 비콜드체인 물류

- 제품 유형별

- 처방약

- 일반용 의약품

- 바이오의약품 및 바이오시밀러

- 백신 및 혈액 제제

- 임상시험 자료

- 세포 및 유전자 치료

- 의료기기 및 진단기기

- 수의학

- 기타

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 페루

- 칠레

- 아르헨티나

- 기타 남미

- 아시아태평양

- 인도

- 중국

- 일본

- 호주

- 한국

- 동남아시아(싱가포르, 말레이시아, 태국, 인도네시아, 베트남, 필리핀)

- 기타 아시아태평양

- 유럽

- 영국

- 독일

- 프랑스

- 스페인

- 이탈리아

- 베네룩스(벨기에, 네덜란드, 룩셈부르크)

- 북유럽 국가(덴마크, 핀란드, 아이슬란드, 노르웨이, 스웨덴)

- 기타 유럽

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 사우디아라비아

- 남아프리카

- 나이지리아

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Deutsche Post DHL

- Kuehne Nagel

- UPS

- FedEx

- Nippon Express

- World Courier

- SF Express

- CEVA Logistics

- DSV

- Kerry Logistics

- CH Robinson

- Lineage Logistics

- United States Cold Storage

- Americold Logistics

- Nichirei Logistics Group

- Kloosterboer

- NewCold Advanced Cold Logistics

- VersaCold Logistics Services

- Rhenus Logistics

- Cencora

제7장 시장 기회와 미래 전망

SHW 26.01.26The Pharmaceutical Logistics Market was valued at USD 560.81 billion in 2025 and estimated to grow from USD 591.48 billion in 2026 to reach USD 772.38 billion by 2031, at a CAGR of 5.47% during the forecast period (2026-2031).

Robust growth stems from biologics proliferation, rigorous serialization mandates, and the pivot toward direct-to-patient delivery models that require precision distribution capacities. Strong capital spending by global integrators, sustained e-pharmacy adoption, and expanding temperature-controlled infrastructure continue to intensify competition while enlarging addressable demand for end-to-end, compliant supply-chain solutions. Technology deployment-particularly IoT sensors, blockchain traceability, and AI-driven network optimization-has accelerated as stakeholders guard against temperature excursions and counterfeit risk. At the same time, sustainability commitments are redirecting capacity toward intermodal and ocean transportation to curb emissions, opening new service niches for specialty providers. Price pressures linked to cold-chain energy costs and multi-jurisdictional compliance remain headwinds, yet they also spur investment in low-carbon packaging, regionalized inventories, and alternative fuels that ultimately expand the pharmaceutical logistics market.

Global Pharmaceutical Logistics Market Trends and Insights

Expansion of Online Pharmacies

Nearly half of consumers now prefer ordering medicines online, compelling carriers to engineer door-step delivery networks that secure 2 °C-8 °C conditions for sensitive products. Providers in Asia-Pacific leverage digital payments and telehealth platforms to scale ambient and refrigerated parcel services, while U.S. integrators enhance last-mile visibility through IoT-enabled pack-out solutions. Regulators have responded by extending serialization and track-and-trace to the single-unit level, raising compliance hurdles but also differentiating operators that offer real-time temperature and location data. As e-pharmacy volumes climb, network redesign toward micro-fulfillment hubs tightens lead-times, improving medication adherence and fueling incremental demand across the pharmaceutical logistics market.

Rising OTC-Medicine Demand & Chronic-Disease Burden

OTC formulations carry less-stringent handling rules than prescription drugs, enabling blended transport lanes that cut storage costs for integrated distributors. However, the rising prevalence of diabetes and cardiovascular disease forces continual replenishment cycles that intensify throughput requirements for time-critical inventory. Logistics partners exploit automation, such as robotic pick-and-pack and smart blister packaging, to combine OTC and chronic-care medications within unified flows that reduce dwell time. Hybrid models improve asset utilization and sustain profitability within the pharmaceutical logistics market while enhancing service quality for pharmacies and clinics.

High Cost of Temperature-Controlled Distribution

Cold-chain failures cost drug makers an estimated USD 35 billion each year, reflecting write-offs, repackaging, and penalty shipments. Passive packaging with phase-change materials can extend protection to 96 hours but often doubles per-parcel expenses, placing strain on emerging-market programs where funding is scarce. The need for redundant monitoring equipment and qualified staff compounds overhead, limiting profit margins for smaller carriers within the pharmaceutical logistics market. Innovation in low-carbon refrigerants and reusable totes aims to reduce cost per shipment, yet wide deployment remains constrained by initial capital outlay.

Other drivers and restraints analyzed in the detailed report include:

- Acceleration of Biologics & Vaccine Cold-Chain Needs

- Outsourcing Surge to 3PL/4PL Specialists

- Complex & Divergent Global Compliance Standards

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Transportation generated 51.40% of 2025 revenue, illustrating that physical movement remains the backbone of the pharmaceutical logistics market. Road freight captures regional flows, particularly across Europe and North America, while air freight underpins long-haul biologics replenishment with next-day service guarantees. Ocean lanes gain relevance as shippers pursue sustainable options, leveraging GDP-compliant reefer containers to curb emissions.

Value-added services, growing at a 4.42% CAGR, include labeling, secondary packaging, order kitting, and serialization consulting that relieve manufacturers of non-core tasks. Demand rises fastest in Asia-Pacific, where contract manufacturers seek single-source partners to handle regulatory printing in multiple languages. As data integrity rules tighten, certified relabeling and tamper-evident pack-outs transform from optional extras into procurement prerequisites, driving incremental margin across the pharmaceutical logistics market.

The Pharmaceutical Logistics Market Report is Segmented by Service Type (Transportation, Warehousing & Storage, and Value-Added Services & Others), Mode of Operation (Cold-Chain Logistics and Non-Cold-Chain Logistics), Product Type (Prescription Drugs, OTC Drugs, Biologics & Biosimilars, and More), Geography (North America, South America, Europe, Asia-Pacific, and, More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Europe maintained a 31.70% revenue share in 2025, underpinned by harmonized GDP enforcement, dense road networks, and large-scale manufacturing clusters in Germany, Switzerland, and Ireland. Investment in cross-border rail-air corridors supports modal shifts that lower emissions without compromising lead times. The pharmaceutical logistics market size in Europe benefits from continual capacity additions such as Cold Chain Technologies' new Netherlands hub, which augments regional PCM production and reduces transit risk.

North America remains a powerhouse thanks to DSCSA-driven serialization maturity and sustained public-sector funding for pandemic preparedness. DHL allocated 50% of its EUR 2 billion (USD 2.08 billion) plan to U.S. and Canadian facilities, integrating solar-powered warehouses and LNG trucks that curb emissions while preserving service standards. Combined with FedEx's USD 440 million expansion of healthcare distribution centers, the region continues to redefine best practices around data visibility and sustainability.

Asia-Pacific is expected to post the fastest growth at 5.02% CAGR from 2026 to 2031, buoyed by increased production out of China and India, widening insurance coverage, and e-pharmacy proliferation. Governments incentivize cold-chain upgrades, as evidenced by India's 2025 tax rebates on GDP-compliant warehousing equipment. Regional carriers deploy rail-truck sea-air solutions along the China-Europe corridor, trimming cost and cutting transit emissions. Middle East & Africa trail in infrastructure, yet Gulf Cooperation Council localization programs spur warehouse investment, securing future pharmaceutical logistics market expansion.

- Deutsche Post DHL

- Kuehne + Nagel

- UPS

- FedEx

- Nippon Express

- World Courier

- SF Express

- CEVA Logistics

- DSV

- Kerry Logistics

- C.H. Robinson

- Lineage Logistics

- United States Cold Storage

- Americold Logistics

- Nichirei Logistics Group

- Kloosterboer

- NewCold Advanced Cold Logistics

- VersaCold Logistics Services

- Rhenus Logistics

- Cencora

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expansion of online pharmacies

- 4.2.2 Rising OTC-medicine demand & chronic-disease burden

- 4.2.3 Acceleration of biologics & vaccine cold-chain needs

- 4.2.4 Outsourcing surge to 3PL/4PL specialists

- 4.2.5 Mandatory end-to-end IoT / blockchain track-and-trace

- 4.2.6 Net-zero logistics investments driving infrastructure renewal

- 4.3 Market Restraints

- 4.3.1 High cost of temperature-controlled distribution

- 4.3.2 Complex & divergent global compliance standards

- 4.3.3 Shortage of advanced phase-change packaging materials

- 4.3.4 Last-mile biologic delivery bottlenecks in emerging markets

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Impact of COVID-19 & Geo-Political Events

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Service Type

- 5.1.1 Transportation

- 5.1.1.1 Road Freight

- 5.1.1.2 Air Freight

- 5.1.1.3 Sea Freight

- 5.1.1.4 Rail Freight

- 5.1.2 Warehousing & Storage

- 5.1.3 Value-added Services and Others

- 5.1.1 Transportation

- 5.2 By Mode of Operation

- 5.2.1 Cold-Chain Logistics

- 5.2.2 Non-Cold-Chain Logistics

- 5.3 By Product Type

- 5.3.1 Prescription Drugs

- 5.3.2 OTC Drugs

- 5.3.3 Biologics & Biosimilars

- 5.3.4 Vaccines & Blood Products

- 5.3.5 Clinical Trail Materials

- 5.3.6 Cell & Gene Therapies

- 5.3.7 Medical Devices & Diagnostics

- 5.3.8 Veterinary Medicine

- 5.3.9 Others

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Peru

- 5.4.2.3 Chile

- 5.4.2.4 Argentina

- 5.4.2.5 Rest of South America

- 5.4.3 Asia-Pacific

- 5.4.3.1 India

- 5.4.3.2 China

- 5.4.3.3 Japan

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines)

- 5.4.3.7 Rest of Asia-Pacific

- 5.4.4 Europe

- 5.4.4.1 United Kingdom

- 5.4.4.2 Germany

- 5.4.4.3 France

- 5.4.4.4 Spain

- 5.4.4.5 Italy

- 5.4.4.6 BENELUX (Belgium, Netherlands, and Luxembourg)

- 5.4.4.7 NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- 5.4.4.8 Rest of Europe

- 5.4.5 Middle East and Africa

- 5.4.5.1 United Arab of Emirates

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 South Africa

- 5.4.5.4 Nigeria

- 5.4.5.5 Rest of Middle East And Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials, Strategic Info, Market Rank/Share, Products & Services, Recent Developments)

- 6.4.1 Deutsche Post DHL

- 6.4.2 Kuehne + Nagel

- 6.4.3 UPS

- 6.4.4 FedEx

- 6.4.5 Nippon Express

- 6.4.6 World Courier

- 6.4.7 SF Express

- 6.4.8 CEVA Logistics

- 6.4.9 DSV

- 6.4.10 Kerry Logistics

- 6.4.11 C.H. Robinson

- 6.4.12 Lineage Logistics

- 6.4.13 United States Cold Storage

- 6.4.14 Americold Logistics

- 6.4.15 Nichirei Logistics Group

- 6.4.16 Kloosterboer

- 6.4.17 NewCold Advanced Cold Logistics

- 6.4.18 VersaCold Logistics Services

- 6.4.19 Rhenus Logistics

- 6.4.20 Cencora

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment