|

시장보고서

상품코드

1892708

항공기 열교환기 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Aircraft Heat Exchanger Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

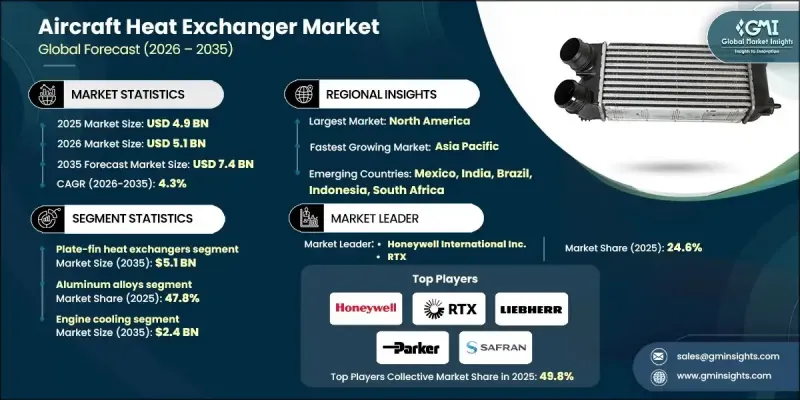

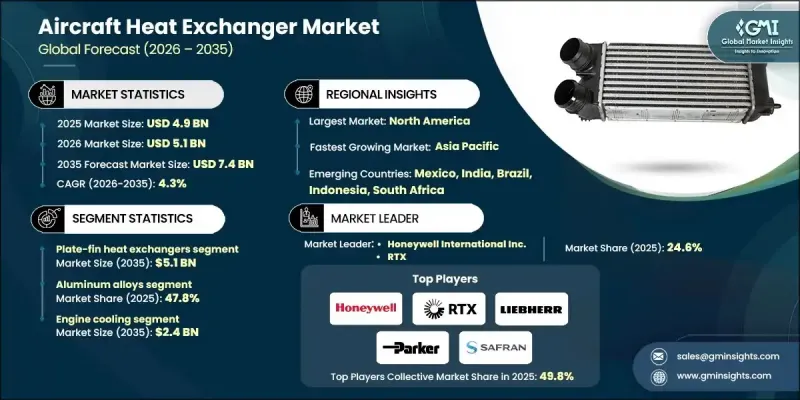

세계의 항공기 열교환기 시장은 2025년에 49억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 4.3%로 성장하여 74억 달러에 이를 것으로 예측됩니다.

시장 성장은 항공 여객 수송량 증가, 연료 효율성에 대한 관심 증가, 첨단 항공 모빌리티의 부상, 무인항공기(UAV) 및 군용 항공기 적용 확대에 의해 주도되고 있습니다. 승객 수요 증가는 항공사가 항공기의 성능, 효율성 및 지속가능성을 향상시켜야 한다는 압력을 가하고 있으며, 이는 열교환기 채택을 촉진하고 있습니다. 전기 및 수소 전기 추진 시스템은 첨단 파워트레인에서 발생하는 다량의 열을 관리할 수 있는 경량, 고성능 열 솔루션의 필요성을 증가시키고 있습니다. 열교환기는 모든 항공기 시스템, 특히 차세대 전기 및 하이브리드 전기 플랫폼에서 최적의 운영 성능을 유지하는 데 중요한 역할을 하며 저공해 항공 및 지속 가능한 비행 이니셔티브에 대한 기대에 부응하고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 연도 | 2026-2035년 |

| 개시 연도 시장 규모 | 49억 달러 |

| 예측 금액 | 74억 달러 |

| CAGR | 4.3% |

판형 열교환기 부문은 2035년까지 51억 달러에 달할 것으로 예측됩니다. 컴팩트한 형태, 높은 열효율, 그리고 첨단 경량 항공기 설계에 대한 적합성으로 인해 채택이 가속화되고 있습니다. 성장세는 주로 제한된 공간 내에서 효율적인 열 방출이 필요한 현대식 엔진, 무인 항공기(UAV), 전기 항공기와의 통합에 의해 주도되고 있습니다.

알루미늄 합금 부문은 2025년 47.8%의 점유율을 차지했습니다. 알루미늄 합금 열교환기는 우수한 강도 대 중량비, 제조 용이성, 비용 효율성으로 인해 선호되고 있습니다. 항공사들은 경량화 및 연료 효율성 향상을 위해 협동체, 와이드바디 항공기, 무인항공기 플랫폼에서 이러한 소재에 대한 의존도를 높이고 있습니다. 제조업체들은 차세대 항공기 설계를 지원하기 위해 고강도 및 열전도율이 우수한 알루미늄 재종에 집중할 것으로 예측됩니다.

미국 항공기 열교환기 시장은 2025년 16억 달러 규모에 달할 것으로 예측됩니다. 이 지역의 성장은 기체 현대화, 상업 및 지역 항공 교통량 증가, 하이브리드 전기 및 무인 항공기 플랫폼의 채택 증가에 의해 주도되고 있습니다. 각 업체들은 차세대 항공기를 위한 모듈식 열교환기 개발에 집중하는 한편, 무인항공기 및 지역 항공 확대를 지원하는 기술에 대한 투자를 진행하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

- 시장 범위와 정의

- 조사 설계

- 조사 접근

- 데이터 수집 방법

- 데이터 마이닝 소스

- 세계

- 지역별/국가별

- 기본 추정치와 계산

- 기준연도 계산

- 시장 추정 주요 동향

- 1차 조사와 검증

- 1차 정보

- 예측 모델

- 조사의 전제조건과 제한 사항

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급업체 상황

- 이익률 분석

- 비용 구조

- 각 단계별 부가가치

- 밸류체인에 영향을 미치는 요인

- 파괴적 변화

- 업계에 대한 영향요인

- 성장 촉진요인

- 업계의 잠재적 리스크&과제

- 시장 기회

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 기술과 혁신 동향

- 현재 기술 동향

- 신기술

- 신흥 비즈니스 모델

- 컴플라이언스 요건

- 공급망 회복탄력성

- 지정학적 분석

- 노동력 분석

- 디지털 전환

- 합병, 인수 및 전략적 제휴 동향

- 리스크 평가와 관리

- 주요 계약 획득 사례(2022-2025년)

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 주요 기업의 경쟁 벤치마킹

- 재무 실적 비교

- 매출

- 이익률

- 연구개발

- 제품 포트폴리오 비교

- 제품 라인 폭

- 기술

- 혁신

- 지역별 전개 비교

- 세계 전개 분석

- 서비스 네트워크 커버율

- 지역별 시장 침투율

- 경쟁 포지셔닝 매트릭스

- 리더 기업

- 챌린저

- 팔로워

- 니치 기업

- 전략적 전망 매트릭스

- 재무 실적 비교

- 주요 발전, 2021-2024

- 인수합병(M&A)

- 제휴 및 공동 사업

- 기술적 진보

- 확대와 투자 전략

- 디지털 전환 대처

- 신흥/스타트업 경쟁 동향

제5장 시장 추산 및 예측 : 열교환기 유형별, 2022-2035

- 주요 동향

- 플레이트 핀 열교환기

- 튜브 핀 열교환기

제6장 시장 추산 및 예측 : 재질별, 2022-2035

- 주요 동향

- 알루미늄 합금

- 스테인리스 스틸

- 티타늄

- 구리

- 기타

제7장 시장 추산 및 예측 : 냉각 매체별, 2022-2035

- 주요 동향

- Air-to-air

- Air-to-liquid

- Liquid-to-liquid

- Liquid-to-air

제8장 시장 추산 및 예측 : 용도별, 2022-2035

- 주요 동향

- 엔진 냉각

- 객실 냉난방(ECS)

- 아비오닉스 냉각

- 유압 냉각

- 연료 가열 및 냉각

- 기타

제9장 시장 추산 및 예측 : 항공기 유형별, 2022-2035

- 주요 동향

- 민간 항공기

- 협폭동체 항공기

- 광폭동체 항공기

- 리저널 제트기

- 군용기

- 전투기

- 수송기

- 비즈니스 항공

- 일반 항공

- 헬리콥터 및 회전익기

제10장 시장 추산 및 예측 : 최종 용도별, 2022-2035

- 주요 동향

- OEM(LINE-FIT)

- 애프터마켓(MRO)

제11장 시장 추산 및 예측 : 지역별, 2021-2034

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 네덜란드

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카공화국

- 사우디아라비아

- 아랍에미리트(UAE)

제12장 기업 개요

- 세계의 주요 기업

- Honeywell International Inc.

- RTX

- Liebherr Group

- Parker Hannifin Corp

- 지역별 주요 기업

- 북미

- 3D Systems, Inc

- AMETEK Inc.

- Boyd Corporation

- 유럽

- Safran S.A

- Meggitt PLC

- Triumph Group

- 아시아태평양

- JAMCO Corporation

- HS-Nauka

- TAT Technologies Ltd

- 북미

- 니치 기업/디스럽터

- Conflux Technology

- Essex Industries, Inc.

- ETP Thermal Dynamics

- THERMOVAC AEROSPACE

- Wall Colmonoy

The Global Aircraft Heat Exchanger Market was valued at USD 4.9 billion in 2025 and is estimated to grow at a CAGR of 4.3% to reach USD 7.4 billion by 2035.

Market growth is propelled by rising air passenger traffic, increasing focus on fuel efficiency, the emergence of advanced air mobility, and the growing applications of UAVs and military aircraft. Rising passenger demand is creating pressure on airlines to improve aircraft performance, efficiency, and sustainability, which in turn fuels the adoption of heat exchangers. Electric and hydrogen-electric propulsion systems are driving the need for lightweight, high-performance thermal solutions that can manage substantial heat from advanced powertrains. Heat exchangers play a critical role in maintaining optimal operational performance across all aircraft systems, particularly in new-generation electric and hybrid-electric platforms, meeting the expectations of low-emission aviation and sustainable flight initiatives.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $4.9 Billion |

| Forecast Value | $7.4 Billion |

| CAGR | 4.3% |

The plate-fin heat exchangers segment is expected to reach USD 5.1 billion by 2035. Their compact form, high thermal efficiency, and suitability for advanced and lightweight aircraft designs have accelerated adoption. Growth is largely driven by integration with modern engines, UAVs, and electric aircraft, which require efficient heat dissipation within confined spaces.

The aluminum alloys segment held 47.8% share in 2025. Heat exchangers made from aluminum alloys are favored for their superior strength-to-weight ratio, manufacturability, and cost-effectiveness. Airlines increasingly rely on these materials across narrow-body, wide-body, and UAV platforms to reduce weight and enhance fuel efficiency. Manufacturers are expected to focus on high-strength, thermally conductive aluminum grades to support next-generation aircraft designs.

U.S. Aircraft Heat Exchanger Market generated USD 1.6 billion in 2025. Growth in this region is driven by fleet modernization, expanding commercial and regional air traffic, and rising adoption of hybrid-electric and UAV platforms. Companies are concentrating on modular, thermally optimized heat exchangers for next-generation aircraft while investing in technology to support UAVs and regional aviation expansion.

Key players operating in the Global Aircraft Heat Exchanger Market include 3D Systems, Inc., AMETEK Inc., Boyd Corporation, Conflux Technology, Essex Industries, Inc., ETP Thermal Dynamics, Honeywell International Inc., HS-Nauka, JAMCO Corporation, Liebherr Group, and Meggitt PLC. Companies in the Global Aircraft Heat Exchanger Market strengthen their position by focusing on research and development to design high-efficiency, lightweight, and thermally optimized solutions for next-generation aircraft. They are investing in advanced manufacturing techniques such as 3D printing to produce complex geometries with enhanced heat transfer efficiency. Strategic collaborations with aviation OEMs and defense contractors expand market reach and support co-development of electric and hybrid propulsion systems. Firms also emphasize modular product designs for faster integration and cost-effective maintenance, while targeting regional markets with growing air traffic and UAV adoption to secure long-term contracts and boost market presence globally.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Heat exchanger type trends

- 2.2.2 Material type trends

- 2.2.3 Cooling medium trends

- 2.2.4 Application trends

- 2.2.5 Aircraft type trends

- 2.2.6 End use trends

- 2.2.7 Regional trends

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising air passenger traffic

- 3.2.1.2 Rising demand for fuel efficiency

- 3.2.1.3 Growth of advanced air mobility & electrified propulsion

- 3.2.1.4 Modular & integrated thermal management architectures

- 3.2.1.5 Rise of UAVs & military aircraft applications

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High manufacturing complexity and certification requirements

- 3.2.2.2 Weight and space constraints in aircraft design

- 3.2.3 Market opportunities

- 3.2.3.1 Adoption of additive manufacturing for complex heat exchanger geometries

- 3.2.3.2 Integration of smart and embedded sensors for real-time thermal monitoring

- 3.2.3.3 Expansion in UAV, MALE/HALE, and defense platforms requiring advanced cooling

- 3.2.3.4 Development of next-generation lightweight materials

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Emerging business models

- 3.9 Compliance requirements

- 3.10 Supply chain resilience

- 3.11 Geopolitical analysis

- 3.12 Workforce analysis

- 3.13 Digital transformation

- 3.14 Mergers, acquisitions, and strategic partnerships landscape

- 3.15 Risk assessment and management

- 3.16 Major contract awards (2022-2025)

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2021-2024

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Heat Exchanger Type, 2022 - 2035 (USD Million & Units)

- 5.1 Key trends

- 5.2 Plate-fin heat exchangers

- 5.3 Tube-fin heat exchangers

Chapter 6 Market Estimates and Forecast, By Material Type, 2022 - 2035 (USD Million & Units)

- 6.1 Key trends

- 6.2 Aluminum alloys

- 6.3 Stainless steel

- 6.4 Titanium

- 6.5 Copper

- 6.6 Others

Chapter 7 Market Estimates and Forecast, By Cooling Medium, 2022 - 2035 (USD Million & Units)

- 7.1 Key trends

- 7.2 Air-to-air

- 7.3 Air-to-liquid

- 7.4 Liquid-to-liquid

- 7.5 Liquid-to-air

Chapter 8 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million & Units)

- 8.1 Key trends

- 8.2 Engine cooling

- 8.3 Cabin heating & cooling (ECS)

- 8.4 Avionics cooling

- 8.5 Hydraulic cooling

- 8.6 Fuel heating & cooling

- 8.7 Others

Chapter 9 Market Estimates and Forecast, By Aircraft Type, 2022 - 2035 (USD Million & Units)

- 9.1 Key trends

- 9.2 Commercial aircraft

- 9.2.1 Narrow-body aircraft

- 9.2.2 Wide-body aircraft

- 9.2.3 Regional jets

- 9.3 Military aircraft

- 9.3.1 Fighter jets

- 9.3.2 Transport aircraft

- 9.4 Business aviation

- 9.5 General aviation

- 9.6 Helicopters & rotorcraft

Chapter 10 Market Estimates and Forecast, By End Use, 2022 - 2035 (USD Million & Units)

- 10.1 Key trends

- 10.2 OEM (Line-Fit)

- 10.3 Aftermarket (MRO)

Chapter 11 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Million & Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Netherlands

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Global Key Players

- 12.1.1 Honeywell International Inc.

- 12.1.2 RTX

- 12.1.3 Liebherr Group

- 12.1.4 Parker Hannifin Corp

- 12.2 Regional Key Players

- 12.2.1 North America

- 12.2.1.1 3D Systems, Inc

- 12.2.1.2 AMETEK Inc.

- 12.2.1.3 Boyd Corporation

- 12.2.2 Europe

- 12.2.2.1 Safran S.A

- 12.2.2.2 Meggitt PLC

- 12.2.2.3 Triumph Group

- 12.2.3 APAC

- 12.2.3.1 JAMCO Corporation

- 12.2.3.2 HS-Nauka

- 12.2.3.3 TAT Technologies Ltd

- 12.2.1 North America

- 12.3 Niche Players / Disruptors

- 12.3.1 Conflux Technology

- 12.3.2 Essex Industries, Inc.

- 12.3.3 ETP Thermal Dynamics

- 12.3.4 THERMOVAC AEROSPACE

- 12.3.5 Wall Colmonoy