|

시장보고서

상품코드

1892765

벌크 자재관리 장비 시장 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2026-2035년)Bulk Material Handling Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

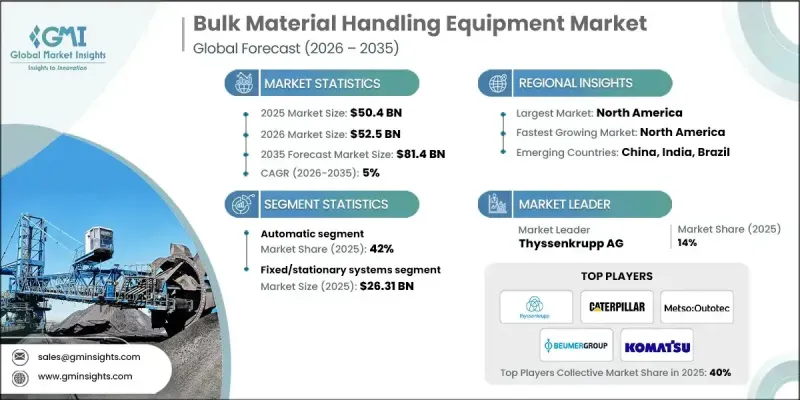

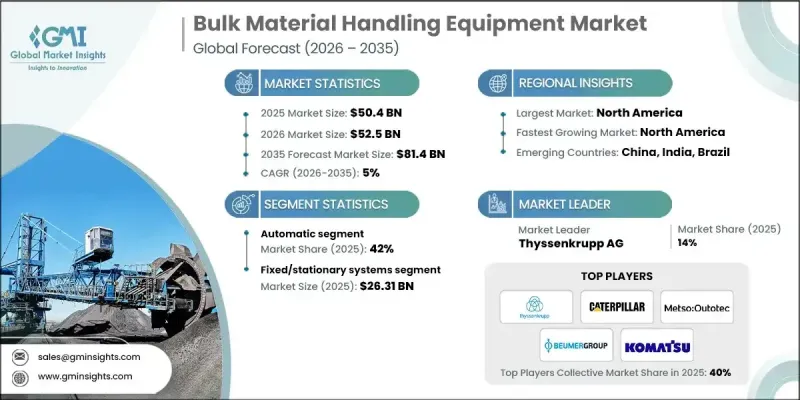

세계의 벌크 자재관리 장비 시장은 2025년에 504억 달러로 평가되었으며, 2035년까지 CAGR 5%로 성장하여 814억 달러에 달할 것으로 예측됩니다.

자동화된 벌크 핸들링으로의 전환은 기업이 기존의 수동 시스템을 넘어 현대 공급망의 과제를 해결하는 첨단 솔루션을 채택함에 따라 산업을 계속 변화시키고 있습니다. 자동화는 더 이상 단순한 인건비 절감 수단으로 간주되지 않고, 워크플로우 효율성 향상, 작업장 안전 강화, 업무 중단 최소화, 보다 견고하고 적응력 있는 물류 네트워크 구축에 필수적인 요소로 인식되고 있습니다. 현대의 자동화 시스템은 수요 변동에 대응하는 기업을 지원하고, 대량 처리 업무의 일관성 유지에 기여합니다. E-Commerce의 급속한 성장은 이러한 시스템에 의존하는 산업의 범위를 확대함으로써 벌크 자재 취급의 상황을 크게 변화시켰습니다. 과거에는 광업, 해운, 제조업 등 산업 부문을 중심으로 발전해 왔지만, 현재는 대규모 디지털 상거래와 가속화되는 배송 기대치를 지원하는 데 필요한 인프라의 핵심 요소로 자리 잡고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 연도 | 2026-2035 |

| 시작 가치 | 504억 달러 |

| 예측 금액 | 814억 달러 |

| CAGR | 5% |

자동화 부문은 2025년 42%의 점유율을 차지했습니다. 자동화된 벌크 핸들링 솔루션에 대한 수요는 이러한 시스템의 성능 향상과 운영 비용 절감으로 인해 지속적으로 견조한 수요를 보이고 있습니다. 간소화된 자재 라우팅 및 지능형 이동 기술을 포함한 자동화 도구는 상품의 정확한 흐름과 배송을 보장하는 데 도움이 됩니다.

고정식 및 고정형 시스템 부문은 2025년 52%의 점유율을 차지하며 263억 1,000만 달러의 시장 규모를 형성했습니다. 이러한 시스템이 주류가 된 이유는 중단 없는 대량 자재 처리를 다루는 업무에서 필수적인 존재이기 때문입니다. 스태커, 컨베이어 구조, 호퍼 등의 고정형 설비는 장소를 이동하지 않고 벌크 화물의 연속적인 이동을 가능하게 하여 장시간 자재 이송에 의존하는 산업에서 필수적인 설비로 자리 잡았습니다.

미국의 벌크 자재 취급 장비 시장은 2025년 4억 8,640만 달러로 평가되었습니다. 북미는 광범위한 자동화 도입과 산업 시설 현대화에 대한 지속적인 투자로 견조한 성장세를 이어가고 있습니다. 미국 시장은 다양한 산업 기반과 광업, 건설, 물류 부문의 수요 증가로 인해 세계에서 가장 빠르게 성장하고 있는 시장 중 하나로 자리매김하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급업체 상황

- 이익률

- 각 공정의 부가가치

- 밸류체인에 영향을 미치는 요인

- 업계에 대한 영향요인

- 성장 촉진요인

- 포장 및 인쇄의 정밀성에 대한 수요 상승

- 자동화와 기술 진보

- E-Commerce와 맞춤화 동향 확대

- 업계의 잠재적 리스크와 과제

- 높은 초기 투자 및 유지 관리 비용

- 기능 부족과 운영상 복잡성

- 기회

- 성장 촉진요인

- 성장 가능성 분석

- 향후 시장 동향

- 기술과 혁신 동향

- 현재 기술 동향

- 신기술

- 가격 동향

- 지역별

- 장비별

- 규제 상황

- 규격 및 컴플라이언스 요건

- 지역별 규제 프레임워크

- 인증 기준

- Porters 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 인수합병

- 제휴·협업

- 신제품 발매

- 확대 계획

제5장 시장 추정 및 예측 : 설비 유형별, 2022-2035

- 주요 동향

- 컨베이어 시스템

- 벨트 컨베이어 시스템

- 파이프 컨베이어 시스템

- 드래그 체인 컨베이어 시스템

- 스크류 컨베이어 시스템

- 스태커·리클레이머 시스템

- 원형 스태커·리클레이머

- 리니어 스태커·리클레이머

- 복합 스태커·리클레이머

- 선박 적재·하역 시스템

- 연속식 선적기

- 그랩식 선적기

- 공압식 선적기

- 버킷 휠 굴착기

- 갈탄 채굴 용도

- 철광석 용도

- 표토 제거 용도

- 피더 및 공급 장비

- 진동 피더

- 벨트 피더

- 에이프런 피더

- 분쇄기 및 분쇄 장비

- 조 크러셔

- 콘 크러셔

- 임팩트 크러셔

- 해머 밀

- 체분·분리 장비

- 진동 스크린

- 분급기·분리기

- 저장 시스템

- 호퍼 및 빈

- 사일로 및 저장 시설

- 보조·지원 설비

- 벨트 클리너 및 스크레이퍼

- 수취 시스템

- 이송 장비 및 슈트

- 집진 시스템

- 자기 분리기

제6장 시장 추정 및 예측 : 용량별, 2022-2035

- 주요 동향

- 소용량 시스템(1,000톤/시 미만)

- 중용량 시스템(1,000-5,000톤/시)

- 고용량 시스템(5,000-8,000톤/시)

- 초대용량 시스템(8,000톤/시 이상)

제7장 시장 추정 및 예측 : 설치 유형별, 2022-2035

- 주요 동향

- 고정식/고정형 시스템

- 이동식 시스템

- 휴대형/반 이동식 시스템

제8장 시장 추정 및 예측 : 자동화 유형별, 2022-2035

- 주요 동향

- 수동

- 반자동

- 자동화

제9장 시장 추정 및 예측 : 상품 유형별, 2022-2035

- 주요 동향

- 철광석

- 석탄

- 구리

- 비료·화학제품

- 복수 상품 시스템

- 기타 상품 유형

제10장 시장 추정 및 예측 : 최종 용도별, 2022-2035

- 주요 동향

- 광업 오퍼레이션

- 항만·터미널 운영

- 발전

- 시멘트 제조

- 철강·금속 가공

- 농업·식품 가공

- 건설·골재

- 물류·유통 센터

- 기타 최종 용도

제11장 시장 추정 및 예측 : 유통 채널별, 2022-2035

- 주요 동향

- 직접 판매

- 간접 판매

제12장 시장 추정 및 예측 : 지역별, 2022-2035

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카공화국

- 사우디아라비아

- 아랍에미리트

제13장 기업 개요

- KOCH Solutions GmbH

- Caterpillar Inc.

- Komatsu Ltd.

- Metso Outotec Corporation

- thyssenkrupp AG

- Sandvik AB

- BEUMER Group GmbH & Co. KG

- AUMUND Group

- TAKRAF GmbH

- CITIC Heavy Industries Co., Ltd.

- Tenova S.p.A.

- Siwertell AB

- Vigan Engineering S.A.

- Liebherr Group

- Continental AG

The Global Bulk Material Handling Equipment Market was valued at USD 50.4 billion in 2025 and is estimated to grow at a CAGR of 5% to reach USD 81.4 billion by 2035.

The transition toward automated bulk handling continues to reshape the industry as companies move beyond traditional manual systems and adopt advanced solutions designed for today's supply chain challenges. Automation is no longer viewed simply as a method to cut labor costs; it has become essential for improving workflow efficiency, enhancing workplace safety, minimizing operational disruptions, and building a more resilient and adaptable logistics network. Modern automated systems support businesses as they respond to fluctuating demand and help maintain consistency across high-volume operations. Rapid growth in e-commerce has also significantly influenced the landscape of bulk material handling by expanding the range of industries that rely on these systems. What was once centered around industrial sectors such as mining, shipping, and manufacturing is now a core component of the infrastructure needed to support large-scale digital commerce and accelerated delivery expectations.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $50.4 Billion |

| Forecast Value | $81.4 Billion |

| CAGR | 5% |

The automatic segment held a 42% share in 2025. Demand for automated bulk handling solutions remains strong because these systems enhance performance and reduce operating expenses. Automated tools, including streamlined material routing and intelligent movement technologies, help ensure accurate flow and delivery of goods.

The fixed and stationary systems segment held a 52% share and generated USD 26.31 billion in 2025. These systems dominate because they are indispensable in operations that handle uninterrupted, high-volume material processing. Stationary equipment, such as stackers, conveyor structures, and hoppers, enables continuous movement of bulk goods without relocation, making them essential for industries that depend on long-duration material transfer.

U.S. Bulk Material Handling Equipment Market was valued at USD 486.4 million in 2025. North America continues to show strong growth due to the widespread adoption of automation and sustained investment in modernizing industrial facilities. The U.S. market benefits from a diverse industrial base and rising demand from mining, construction, and logistics sectors, helping the region maintain one of the fastest-expanding market environments worldwide.

Key companies in the Global Bulk Material Handling Equipment Market include KOCH Solutions GmbH, Caterpillar Inc., Komatsu Ltd., Metso Outotec Corporation, thyssenkrupp AG, Sandvik AB, BEUMER Group GmbH & Co. KG, AUMUND Group, TAKRAF GmbH, CITIC Heavy Industries Co., Ltd., Tenova S.p.A., Siwertell AB, Vigan Engineering S.A., Liebherr Group, and Continental AG. Companies in the Bulk Material Handling Equipment Market are strengthening their competitive position by expanding automated product portfolios and integrating digital technologies such as smart monitoring, predictive maintenance, and advanced control systems. Many manufacturers are prioritizing energy-efficient equipment designs, reflecting the demand for lower operating costs and reduced environmental impact. Strategic partnerships with mining, construction, and logistics operators help companies deliver customized handling systems that fit high-volume applications. Firms are also investing in modular and scalable equipment platforms, enabling customers to upgrade as capacity needs grow.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Equipment Type

- 2.2.3 Capacity

- 2.2.4 Installation Type

- 2.2.5 Automation Type

- 2.2.6 Commodity

- 2.2.7 End Use

- 2.2.8 Distribution Channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing demand for precision in packaging and printing

- 3.2.1.2 Automation and technological advancements

- 3.2.1.3 Expansion of e-commerce and customization trends

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High initial investment and maintenance costs

- 3.2.2.2 Skill gap and operational complexity

- 3.2.3 Opportunities

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By equipment type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Equipment Type, 2022 - 2035 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Conveyor systems

- 5.2.1 Belt conveyor systems

- 5.2.2 Pipe conveyor systems

- 5.2.3 Drag chain conveyor systems

- 5.2.4 Screw conveyor systems

- 5.3 Stacker-reclaimer systems

- 5.3.1 Circular stacker-reclaimers

- 5.3.2 Linear stacker-reclaimers

- 5.3.3 Combined stacker-reclaimers

- 5.4 Shiploader & shipunloader systems

- 5.4.1 Continuous shiploaders

- 5.4.2 Grab-type shipunloaders

- 5.4.3 Pneumatic shipunloaders

- 5.5 Bucket wheel excavators

- 5.5.1 Lignite mining applications

- 5.5.2 Iron ore applications

- 5.5.3 Overburden removal applications

- 5.6 Feeders & feeding equipment

- 5.6.1 Vibratory feeders

- 5.6.2 Belt feeders

- 5.6.3 Apron feeders

- 5.7 Crushers & size reduction equipment

- 5.7.1 Jaw crushers

- 5.7.2 Cone crushers

- 5.7.3 Impact crushers

- 5.7.4 Hammer mills

- 5.8 Screening & separation equipment

- 5.8.1 Vibrating screens

- 5.8.2 Classifiers & separators

- 5.9 Storage systems

- 5.9.1 Hoppers & bins

- 5.9.2 Silos & storage facilities

- 5.10 Auxiliary & support equipment

- 5.10.1 Belt cleaners & scrapers

- 5.10.2 Take-up systems

- 5.10.3 Transfer equipment & chutes

- 5.10.4 Dust collection systems

- 5.10.5 Magnetic separators

Chapter 6 Market Estimates and Forecast, By Capacity, 2022 - 2035 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Small capacity systems (under 1,000 tph)

- 6.3 Medium capacity systems (1,000-5,000 tph)

- 6.4 High-capacity systems (5,000-8,000 tph)

- 6.5 Ultra-high-capacity systems (8,000+ tph)

Chapter 7 Market Estimates and Forecast, By Installation Type, 2022 - 2035 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Fixed/stationary systems

- 7.3 Mobile systems

- 7.4 Portable/semi-mobile systems

Chapter 8 Market Estimates and Forecast, By Automation Type, 2022 - 2035 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Manual

- 8.3 Semi-automatic

- 8.4 Automatic

Chapter 9 Market Estimates and Forecast, By Commodity Type, 2022 - 2035 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Iron ore

- 9.3 Coal

- 9.4 Copper

- 9.5 Fertilizers & chemicals

- 9.6 Multi-commodity systems

- 9.7 Other bulk commodities

Chapter 10 Market Estimates and Forecast, By End Use, 2022 - 2035 (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 Mining operations

- 10.3 Port & terminal operations

- 10.4 Power generation

- 10.5 Cement manufacturing

- 10.6 Steel & metals processing

- 10.7 Agriculture & food processing

- 10.8 Construction & aggregates

- 10.9 Logistics & distribution centers

- 10.10 Other end-use industries

Chapter 11 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 (USD Billion) (Thousand Units)

- 11.1 Key trends

- 11.2 Direct sales

- 11.3 Indirect sales

Chapter 12 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion) (Thousand Units)

- 12.1 Key trends

- 12.2 North America

- 12.2.1 U.S.

- 12.2.2 Canada

- 12.3 Europe

- 12.3.1 Germany

- 12.3.2 UK

- 12.3.3 France

- 12.3.4 Italy

- 12.3.5 Spain

- 12.4 Asia Pacific

- 12.4.1 China

- 12.4.2 Japan

- 12.4.3 India

- 12.4.4 Australia

- 12.4.5 South Korea

- 12.5 Latin America

- 12.5.1 Brazil

- 12.5.2 Mexico

- 12.5.3 Argentina

- 12.6 Middle East and Africa

- 12.6.1 South Africa

- 12.6.2 Saudi Arabia

- 12.6.3 UAE

Chapter 13 Company Profiles

- 13.1 KOCH Solutions GmbH

- 13.2 Caterpillar Inc.

- 13.3 Komatsu Ltd.

- 13.4 Metso Outotec Corporation

- 13.5 thyssenkrupp AG

- 13.6 Sandvik AB

- 13.7 BEUMER Group GmbH & Co. KG

- 13.8 AUMUND Group

- 13.9 TAKRAF GmbH

- 13.10 CITIC Heavy Industries Co., Ltd.

- 13.11 Tenova S.p.A.

- 13.12 Siwertell AB

- 13.13 Vigan Engineering S.A.

- 13.14 Liebherr Group

- 13.15 Continental AG