|

시장보고서

상품코드

1892769

글리포세이트 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Glyphosate Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

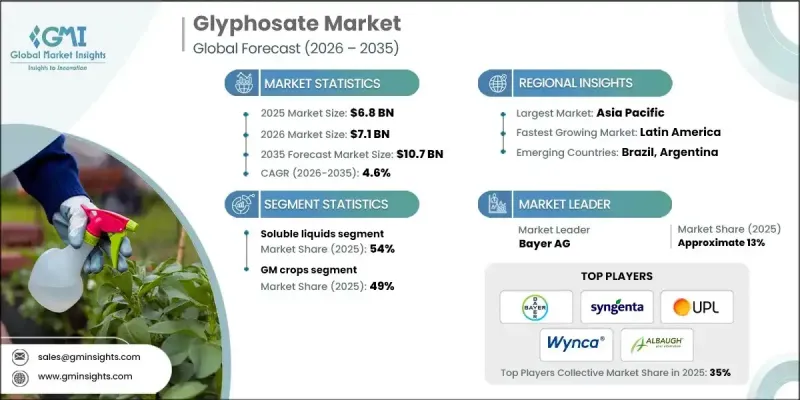

세계의 글리포세이트 시장은 2025년에 68억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 4.6%로 성장하여 107억 달러에 이를 것으로 예측됩니다.

글리포세이트는 관리 책임과 규제 요건이 강화되고 있음에도 불구하고, 재배 전 제초, 유전자 변형 작물 재배 시 작물 생육 중 사용, 수확 후 수확 후 잡초 관리에서 여전히 기본적인 역할을 하고 있습니다. 이 시장은 보전경작과 무경운 재배의 보급, 다작에 의한 집약화, 가격에 민감한 지역에서의 헥타르당 비용 우위에 의해 뒷받침되고 있습니다. 한편, 유럽 일부 지역의 내성 문제와 규제 강화로 인해 사용자들은 정밀한 살포와 다양한 탱크 믹스로 전환해야 하는 상황에 직면해 있습니다. 중국의 기술 공급업체들은 생산 능력을 간소화하고 환경 준수를 개선하여 순도 기준을 높이고, 안정적이고 장기적인 공급에 의존하는 세계 제제 제조업체를 위해 가격을 안정화시키고 있습니다. 폐수 처리 및 배출가스 관리 강화로 과거와 같은 급격한 수요 변동 주기를 최소화하여 미주 및 유럽 제제 제조업체는 안정적인 계획을 수립할 수 있게 되었습니다. 생산자들은 펄스 폭 변조, 구획 제어, 무인 항공기를 이용한 스팟 살포, 디지털 플랫폼을 도입하여 효과와 규정 준수를 유지하면서 살포량을 최적화하고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 연도 | 2026-2035년 |

| 개시 연도 시장 규모 | 68억 달러 |

| 예측 금액 | 107억 달러 |

| CAGR | 4.6% |

수용성 액체 부문은 2025년 54%의 점유율을 차지할 것으로 예상되며, 2035년까지 연평균 4.7%의 성장률을 보일 것으로 전망됩니다. 이러한 제제는 취급 용이성, 광범위한 탱크 혼합 호환성, 흡수성, 내우성 및 효과 향상(수로 및 해안선 관리를 위한 수생생물 승인 옵션 포함)으로 인해 선호되고 있습니다.

유전자 변형 작물 부문은 2025년에 49%의 점유율을 차지할 것으로 예상되며, 2035년까지 연평균 복합 성장률(CAGR) 5%를 보일 것으로 예측됩니다. 글리포세이트는 콩, 옥수수, 면화 재배에서 여전히 필수적이며, 저항성 생물형에 대응하고, 다년생 작물 및 과수원에서 파종 전 제초 처리 및 방향성 스트립 살포의 기초를 형성하고 있습니다. 수생 생물 및 산업 응용 분야에서는 긴 간격의 라벨과 수생 생물 안전 제제가 활용되고 있습니다.

북미 글리포세이트 시장은 2025년 23.9%의 점유율을 차지할 것으로 예상되며, 이는 성숙하고 고도로 전문화된 시장임을 반영합니다. 미국에서는 EPA 승인 라벨에 따라 운영되고 있으며, 멸종위기종 대책으로 살포 시기 엄격화, 완충지대 설정, 종합적인 기록 요건을 강화하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급업체 상황

- 이익률

- 각 단계별 부가가치

- 밸류체인에 영향을 미치는 요인

- 파괴적 변화

- 업계에 대한 영향요인

- 성장 촉진요인

- 업계의 잠재적 리스크&과제

- 시장 기회

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 가격 동향

- 지역별

- 제품 구성별

- 향후 시장 동향

- 기술과 혁신 동향

- 현재 기술 동향

- 신기술

- 특허 상황

- 무역 통계(HS코드)(주 : 무역 통계는 주요 국가에 한해 제공됩니다)

- 주요 수입국

- 주요 수출국

- 지속가능성과 환경면

- 지속가능한 대처

- 폐기물 감축 전략

- 생산 에너지 효율

- 친환경 이니셔티브

- 탄소발자국 고려

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 인수합병(M&A)

- 제휴 및 협업

- 신제품 발매

- 사업 확대 계획

제5장 시장 추산 및 예측 : 제품 형태별, 2022-2035

- 주요 동향

- 테크니컬 농축물(TC-분말)

- 테크니컬 농축물(TK-용액)

- 수용성 액체 농축물(SL)

- 수용성 과립(SG)

- 즉용형 액체

- 수생생물용 및 특수 제제

- 기타

제6장 시장 추산 및 예측 : 용도별, 2022-2035

- 주요 동향

- 유전자 재조합 작물

- 유전자 재조합 옥수수

- 유전자 재조합 면

- 유전자 재조합 카놀라

- 유전자 재조합 대두

- 유전자 재조합 사탕무

- 유전자 재조합 알팔파

- 비유전자 재조합 경작 작물

- 곡류

- 유량 작물

- 과일 및 채소

- 채소

- 과일

- 산업용 작물

- 사탕수수

- 기타 산업용 작물

- 비농업 용도

- 임업 관리

- 잔디 및 관상 식물

- 수역

- Rights-of-Way (ROW)

- 상업 및 산업용지

- 기타

제7장 시장 추산 및 예측 : 최종 용도별, 2022-2035

- 주요 동향

- 대규모 상업 농가

- 중소규모 농가

- 정부 및 공공기관

- 상업용 조경 업자

- 산업용 식생 관리 회사

- 주택 소비자

- 기타

제8장 시장 추산 및 예측 : 지역별, 2022-2035

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 기타 라틴아메리카

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카공화국

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

제9장 기업 개요

- ADAMA Agricultural Solutions Ltd.

- Albaugh, LLC

- Anhui Huaxing Chemical Industry Co., Ltd.

- Arysta LifeScience

- Bayer AG

- Excel Crop Care Limited

- FMC Corporation

- Gharda Chemicals Limited

- Helm AG

- Heranba Industries Limited

- Hubei Xingfa Chemicals Group

- Jiangsu Good Harvest-Weien Agrochemical Co., Ltd.

- Jiangsu Yangnong Chemical Co., Ltd.

- Nufarm Limited

- Nutrien Ag Solutions

- Rainbow Agro

- Sinon Corporation(Taiwan)

- Syngenta Group(ChemChina)

- UPL Limited

- Zhejiang Xinan Chemical Industrial Group Co., Ltd.

- Others

The Global Glyphosate Market was valued at USD 6.8 billion in 2025 and is estimated to grow at a CAGR of 4.6% to reach USD 10.7 billion by 2035.

Glyphosate remains a cornerstone for pre-plant burndown, in-crop use on traited systems, and post-harvest stubble management, even as stewardship and regulatory expectations increase. The market is supported by the adoption of conservation and no-till practices, intensified multi-cropping, and cost-per-hectare advantages in price-sensitive regions. At the same time, resistance issues and tighter regulations in some parts of Europe are pushing users toward precision applications and diversified tank mixes. Chinese technical suppliers have rationalized capacities and improved environmental compliance, boosting purity standards and stabilizing prices for global formulators reliant on consistent long-term supply. Upgraded wastewater and emissions controls have minimized historical boom-bust cycles, allowing formulators in the Americas and Europe to plan reliably. Growers are embracing pulse-width modulation, section control, UAV spot-spraying, and digital platforms to optimize application rates while maintaining efficacy and regulatory compliance.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $6.8 Billion |

| Forecast Value | $10.7 Billion |

| CAGR | 4.6% |

The soluble liquids segment held a 54% share in 2025 and is expected to grow at a CAGR of 4.7% through 2035. These formulations are favored for their ease of handling, broad tank-mix compatibility, and improved uptake, rainfastness, and efficacy, including aquatic-approved options for canal and shoreline management.

The GM crops segment accounted for a 49% share in 2025 and is projected to grow at a CAGR of 5% through 2035. Glyphosate remains essential in soybean, corn, and cotton systems, addressing resistant biotypes and forming the backbone of pre-plant burndown and directed strip applications in permanent crops and orchards. Aquatic and industrial use relies on long-interval labels and aquatic-safe formulations.

North America Glyphosate Market held a 23.9% share in 2025, reflecting a mature and highly professionalized glyphosate market. The U.S. operates under EPA-approved labels, with endangered-species mitigation measures reinforcing timing, buffer zones, and comprehensive documentation requirements.

Key players in the Glyphosate Market include ADAMA Agricultural Solutions Ltd., Albaugh, LLC, Anhui Huaxing Chemical Industry Co., Ltd., Arysta LifeScience, Bayer AG, Excel Crop Care Limited, FMC Corporation, Gharda Chemicals Limited, Helm AG, Heranba Industries Limited, Hubei Xingfa Chemicals Group, Jiangsu Good Harvest-Weien Agrochemical Co., Ltd., Jiangsu Yangnong Chemical Co., Ltd., Nufarm Limited, Nutrien Ag Solutions, Rainbow Agro, Sinon Corporation (Taiwan), Syngenta Group (ChemChina), UPL Limited, and Zhejiang Xinan Chemical Industrial Group Co., Ltd. Companies in the Global Glyphosate Market are implementing several strategies to strengthen their foothold. They are investing in R&D to improve formulation performance, including enhanced surfactant systems and precision-compatible products. Strategic alliances with distributors, cooperatives, and agritech platforms expand market penetration and support the adoption of digital application tools. Regional expansion, particularly in emerging markets with rising farm incomes, helps capture new growth opportunities. Companies are also optimizing supply chains, improving environmental compliance, and offering training and technical support to growers to ensure correct usage.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product formulation

- 2.2.3 Application

- 2.2.4 End use

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By Product formulations

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) ( Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Product Formulation, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Technical Concentrate (TC - Powder)

- 5.3 Technical Concentrate (TK - Solution)

- 5.4 Soluble Liquid Concentrate (SL)

- 5.5 Water Soluble Granules (SG)

- 5.6 Ready-to-Use Liquids

- 5.7 Aquatic & Specialty Formulations

- 5.8 Others

Chapter 6 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 GM Crops

- 6.2.1 GM Corn

- 6.2.2 GM Cotton

- 6.2.3 GM Canola

- 6.2.4 GM Soybean

- 6.2.5 GM Sugar Beet

- 6.2.6 GM Alfalfa

- 6.3 Non-GM Arable Crops

- 6.3.1 Cereal Grains

- 6.3.2 Oilseed Crops

- 6.4 Fruits & Vegetables

- 6.4.1 Vegetables

- 6.4.2 Fruits

- 6.5 Industrial Crops

- 6.5.1 Sugarcane

- 6.5.2 Other Industrial Crops

- 6.6 Non-Agricultural Uses

- 6.6.1 Forestry Management

- 6.6.2 Turf & Ornamentals

- 6.6.3 Aquatic Areas

- 6.6.4 Rights-of-Way (ROW)

- 6.6.5 Commercial & Industrial Sites

- 6.7 Others

Chapter 7 Market Estimates and Forecast, By End Use, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Large-Scale Commercial Farmers

- 7.3 Small & Medium Farmers

- 7.4 Government & Public Agencies

- 7.5 Commercial Landscapers

- 7.6 Industrial Vegetation Management Companies

- 7.7 Residential Consumers

- 7.8 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 ADAMA Agricultural Solutions Ltd.

- 9.2 Albaugh, LLC

- 9.3 Anhui Huaxing Chemical Industry Co., Ltd.

- 9.4 Arysta LifeScience

- 9.5 Bayer AG

- 9.6 Excel Crop Care Limited

- 9.7 FMC Corporation

- 9.8 Gharda Chemicals Limited

- 9.9 Helm AG

- 9.10 Heranba Industries Limited

- 9.11 Hubei Xingfa Chemicals Group

- 9.12 Jiangsu Good Harvest-Weien Agrochemical Co., Ltd.

- 9.13 Jiangsu Yangnong Chemical Co., Ltd.

- 9.14 Nufarm Limited

- 9.15 Nutrien Ag Solutions

- 9.16 Rainbow Agro

- 9.17 Sinon Corporation (Taiwan)

- 9.18 Syngenta Group (ChemChina)

- 9.19 UPL Limited

- 9.20 Zhejiang Xinan Chemical Industrial Group Co., Ltd.

- 9.21 Others