|

시장보고서

상품코드

1892793

자동차용 마이크로모터 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Automotive Micro Motors Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

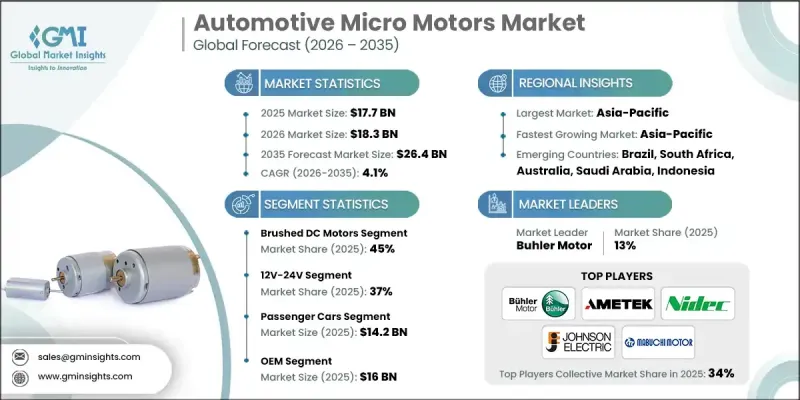

세계의 자동차용 마이크로모터 시장은 2025년에 177억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 4.1%로 성장하여 264억 달러에 이를 것으로 예측됩니다.

모터 기술의 발전, 생산 방법의 변화, 산업 요구 사항의 진화로 인해 마이크로모터의 설계 및 제조 방법이 재구성되고 있습니다. 브러시 DC 모터에서 브러쉬리스 DC(BLDC) 모터로의 전환은 BLDC 시스템의 효율성 향상, 수명 연장 및 유지보수 감소를 배경으로 한 주요 기술 전환점입니다. 반도체 비용의 하락과 대규모 생산의 확대에 따라 BLDC 모터는 자동차 용도에서 보다 비용 효율적인 선택이 되고 있습니다. 전 세계 모터 제조업체의 생산 능력 확대는 공급량을 더욱 늘리고 전체 생산 비용을 낮춰 자동차 산업 전반에 걸쳐 첨단 모터 기술의 보급을 촉진하고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 연도 | 2026-2035년 |

| 개시 연도 시장 규모 | 177억 달러 |

| 예측 금액 | 264억 달러 |

| CAGR | 4.1% |

일본전산, 존슨 일렉트릭, 뷰러 모터 등 여러 주요 BLDC 모터 제조업체들은 자동차 제조업체 수요 증가에 대응하기 위해 생산 능력을 확대하고 있습니다. 여기에는 자동차 용도용 마이크로모터 공급을 위한 추가 시설 설립도 포함되어 있으며, 이는 업계가 새로운 모터 기술로 전환하는 움직임을 촉진하고 있습니다.

브러쉬리스 DC 모터 부문은 2025년 45%의 점유율을 차지할 것으로 예상되며, 2026년부터 2035년까지 연평균 3.2%의 성장률을 보일 것으로 예측됩니다. 이 모터는 특히 비용에 민감한 차량 카테고리에서 윈도우 시스템, 미러 위치 조정, 시트 메커니즘 등 다양한 차량 구성 요소에 널리 사용되고 있습니다. 그러나 기계식 정류 방식에 따른 고유한 성능 제한이 존재합니다.

12V-24V 모터 카테고리는 2025년 37%의 점유율을 차지할 것으로 예상되며, 2035년까지 연평균 3.5%의 성장률을 보일 것으로 전망됩니다. 이 전압 범위는 자동차 마이크로모터 용도에서 가장 일반적인 전압 범위이며, 파워 윈도우, 시트 조절, 선루프, 기본 송풍기 시스템 등의 기능을 지원합니다. 이 모터의 표준 작동 전압은 여전히 12V와 24V입니다.

중국 자동차 마이크로모터 시장은 2025년 46억 달러 규모에 달할 것으로 예측됩니다. 이 지역은 세계 최대 자동차 생산기지라는 지위와 더불어 인구 증가, 자동차 소유율 상승, 자동차 전동화 가속화 지원 정책의 혜택을 누리고 있습니다. 이러한 요인들은 다양한 차량 시스템에서 마이크로모터에 대한 강력한 수요를 견인하고 있습니다.

세계 자동차 마이크로모터 시장에서 활동하는 기업으로는 아메텍, 마부치 모터, 존슨 일렉트릭, 맥슨 모터스, 일본전기(NIDEC), 뷰러 모터, 미츠바 등이 있습니다. 자동차용 마이크로모터 시장의 기업들은 전략적 제조 확대, 기술 강화, 다양한 제품 제공을 통해 경쟁력을 강화하고 있습니다. 많은 제조업체들은 전 세계 자동차 OEM 수요 증가에 대응하기 위해 생산 설비 규모를 확대하는 동시에 품질 향상과 비용 절감을 위한 자동화에 투자하고 있습니다. BLDC 모터 개발에 집중함으로써 고효율화, 장수명화를 지향하는 업계 트렌드에 부합할 수 있도록 하고 있습니다. 또한, 자동차 부품 공급업체와의 제휴를 통해 자사 모터를 보다 광범위한 차량 기능에 통합하기 위한 노력도 진행하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급업체 상황

- 부품 제조업체

- 자동차 제조업체 및 시스템 통합사업자

- 자동차 제조업체 님 및 차량 제조업체

- 애프터마켓 유통 채널

- 최종 사용 및 서비스 네트워크

- 비용 구조

- 이익률

- 각 단계별 부가가치

- 수직통합 동향

- 디스럽터

- 공급업체 상황

- 영향요인

- 성장 촉진요인

- 업계의 잠재적 리스크&과제

- 시장 기회

- 기술 동향과 혁신 에코시스템

- 현행 기술

- 브러쉬 DC 모터와 브러쉬리스 DC 모터 기술 비교

- 서보 및 스테핑 모터 기술의 진보

- 선형 액추에이터 통합 동향

- 자석 및 희토류 원소 없는 모터 개발

- 신기술

- 디지털 트윈 아키텍처와 구현

- 클라우드 처리와 엣지 처리 트레이드 오프

- 무선 업데이트(OTA)

- 펌웨어 업데이트 기능

- 현행 기술

- 성장 가능성 분석

- 규제 상황

- SAE 국제 규격

- UNECE WP.29 규제

- 규제 준수 비용 분석

- 규제 로드맵과 향후 요건

- 지역별 규제 비교

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 비용 내역 분석

- 가격 동향

- 가격 재정 기회

- 가격 하락 동향과 상품화

- 원재료 가격 동향 영향

- 평균 판매 가격(ASP) 동향

- 리스크 평가와 경감 전략

- 리스크 특정과 분류

- 컴플라이언스 및 규제 리스크

- 기술 및 혁신 리스크

- 리스크 경감 전략

- 특허 분석

- 지역별 특허 출원 건수

- 특허 취득율과 취득까지 기간

- 기술 특화형 특허 분석

- 특허 상황 매핑

- 제품 파이프라인과 연구개발 로드맵

- 제품 개발 파이프라인 분석

- 주요 기업별 기술 로드맵

- 연구개발 중점 영역과 투자 우선순위

- 공동 연구개발 구상

- 지속가능성과 환경 측면

- 카 내비게이션 시스템의 탄소발자국

- 순환형 경제 전략

- 지속가능내비게이션 기능

- 기업 지속가능성 이니셔티브

- 기후 변화가 내비게이션에 미치는 영향

- 시장 도입·침투율 분석

- 기술 보급 곡선 분석

- 지역별 보급률

- 차량 부문별 보급률

- 기능 채택 분석

- 보급 촉진 전략

- 고객 및 최종 사용에 관한 통찰

- 인증 및 인가 요건

- OEM 고객 세분화

- OEM 과제와 미해결 요구

- Tier 1 공급업체 고객 분석

- 시나리오 계획과 감도 분석

- 시나리오 계획 프레임워크

- 기반 케이스 시나리오

- 규제 영향 감응도

- 신규 참여 기업과 비즈니스 모델

- 규제 영향 감응도

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

- 주요 발전

- 인수합병(M&A)

- 제휴 및 협업

- 신제품 발매

- 사업 확대 계획과 자금조달

- 프리미엄 포지셔닝 전략

- 경쟁 분석과 독자적인 강점(USP)

제5장 시장 추산 및 예측 : 모터별, 2022-2035

- 주요 동향

- 브러쉬 직류 모터

- 브러쉬리스 DC 모터

- 스테핑 모터

제6장 시장 추산 및 예측 : 소비전력별, 2022-2035

- 주요 동향

- 3V-12V

- 12V-24V

- 25V-48V

- 48V 이상

제7장 시장 추산 및 예측 : 차량별, 2022-2035

- 주요 동향

- 승용차

- SUV

- 세단

- 해치백

- 상용차

- 상업용 경차(LCV)

- MCV

- 대형 상용차(HCV)

제8장 시장 추산 및 예측 : 용도별, 2022-2035

- 주요 동향

- 파워 윈도우

- 와이퍼

- 전동 파워 스티어링(EPS)

- 시트 조정

- 미러 조정

- 선루프 액추에이터

- HVAC 시스템

- 기타

제9장 시장 추산 및 예측 : 판매채널별, 2022-2035

- 주요 동향

- OEM

- 애프터마켓

제10장 시장 추산 및 예측 : 지역별, 2022-2035

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 벨기에

- 네덜란드

- 스웨덴

- 러시아

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 싱가포르

- 한국

- 베트남

- 인도네시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카공화국

- 사우디아라비아

- 아랍에미리트(UAE)

제11장 기업 개요

- 세계 기업

- Continental

- Denso

- Garmin

- HARMAN International

- Hyundai Mobis

- Mitsubishi Electric

- Panasonic

- Robert Bosch

- Region players

- Alpine Electronics

- Clarion

- Desay SV Automotive

- JVCKENWOOD

- LG Electronics

- Marelli

- Pioneer

- Valeo

- Visteon

- 신규 기업

- Aisin Corporation

- Dynavin

- Luxoft

- NNG Software

- Preh Car Connect

- Vinland

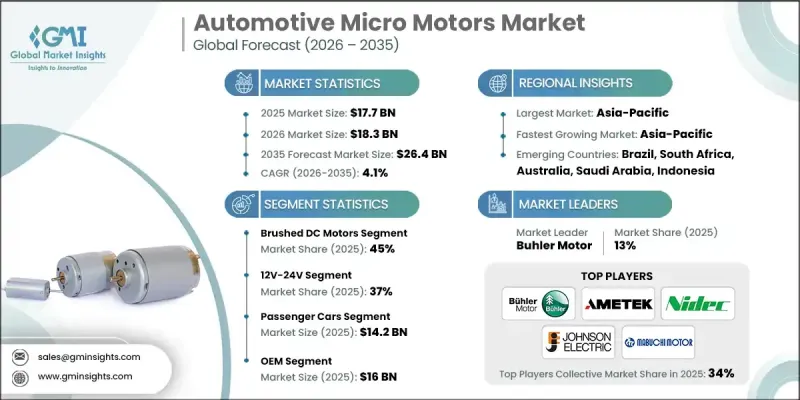

The Global Automotive Micro Motors Market was valued at USD 17.7 billion in 2025 and is estimated to grow at a CAGR of 4.1% to reach USD 26.4 billion by 2035.

Advancements in motor technology, changing production methods, and evolving industry requirements are reshaping the way micro motors are designed and manufactured. The shift from brushed DC motors to brushless DC (BLDC) motors represents a major technological transition, driven by the improved efficiency, longer lifespan, and reduced maintenance needs of BLDC systems. As semiconductor costs decline and large-scale production increases, BLDC motors are becoming more cost-effective for automotive applications. Expanding manufacturing capacity across global motor producers is further enhancing availability and lowering overall production expenses, supporting broader adoption of advanced motor technologies throughout the automotive sector.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $17.7 Billion |

| Forecast Value | $26.4 Billion |

| CAGR | 4.1% |

Multiple leading BLDC motor manufacturers, including NIDEC, Johnson Electric, and Buhler Motor, have increased their production capabilities to meet rising demand from automakers. This includes the establishment of additional facilities dedicated to supplying micro motors for automotive applications, reinforcing the industry's transition toward newer motor technologies.

The brushed DC motors segment accounted for a 45% share in 2025 and is forecasted to grow at a CAGR of 3.2% from 2026 to 2035. These motors remain widely used in various vehicle components, including window systems, mirror positioning, and seating mechanisms, especially within cost-sensitive vehicle categories. However, their mechanical commutation creates inherent performance limitations.

The 12V-24V motor category held a 37% share in 2025 and is projected to grow at a CAGR of 3.5% through 2035. This voltage range remains the most common for automotive micro motor applications, supporting functions such as power windows, seat adjustments, sunroofs, and basic blower systems. The standard operating voltages for these motors continue to be 12V and 24V.

China Automotive Micro Motors Market generated USD 4.6 billion in 2025. The region benefits from its position as the world's largest vehicle manufacturing hub, coupled with population growth, increasing vehicle ownership, and supportive policies designed to accelerate automotive electrification. These factors drive strong demand for micro motors across various vehicle systems.

Companies active in the Global Automotive Micro Motors Market include AMETEK, Mabuchi Motor, Johnson Electric, Maxon Motors, NIDEC, Buhler Motor, and Mitsuba. Companies in the Automotive Micro Motors Market are reinforcing their competitive position through strategic manufacturing expansion, technology enhancements, and diversified product offerings. Many manufacturers are scaling production facilities to meet rising demand from global automotive OEMs, while also investing in automation to improve quality and reduce cost. Emphasis on BLDC motor development allows companies to align with industry trends favoring higher efficiency and longer-lasting components. Firms are also leveraging partnerships with automotive suppliers to integrate their motors into a broader range of vehicle functions.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast

- 1.4 Primary research and validation

- 1.5 Some of the primary sources

- 1.6 Data mining sources

- 1.6.1 Secondary

- 1.6.1.1 Paid Sources

- 1.6.1.2 Public Sources

- 1.6.1.3 Sources, by region

- 1.6.1 Secondary

- 1.7 Inclusion & Exclusion

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Motor

- 2.2.3 Power Consumption

- 2.2.4 Vehicle

- 2.2.5 Application

- 2.2.6 Sales Channel

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Key decision points for industry executives

- 2.4.2 Critical success factors for market players

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Component manufacturers

- 3.1.1.2 Motor manufacturers & integrators

- 3.1.1.3 OEMs & vehicle manufacturers

- 3.1.1.4 Aftermarket distribution channels

- 3.1.1.5 End use & service networks

- 3.1.2 Cost structure

- 3.1.3 Profit margin

- 3.1.4 Value addition at each stage

- 3.1.5 Vertical integration trends

- 3.1.6 Disruptors

- 3.1.1 Supplier landscape

- 3.2 Impact on forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising vehicle electrification & powertrain shift

- 3.2.1.2 Proliferation of comfort & convenience features

- 3.2.1.3 Integration of advanced safety & ADAS

- 3.2.1.4 Stringent emission & fuel economy regulations

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Shift from Brushed DC to Brushless DC (BLDC) Motors

- 3.2.2.2 Modularization & system integration

- 3.2.3 Market opportunities

- 3.2.3.1 AI & predictive navigation

- 3.2.3.2 Smartphone & app projection systems

- 3.2.1 Growth drivers

- 3.3 Technology trends & innovation ecosystem

- 3.3.1 Current technologies

- 3.3.1.1 Brushed vs brushless DC motor technologies

- 3.3.1.2 Servo & Stepper motor advancements

- 3.3.1.3 Linear Actuator integration trends

- 3.3.1.4 Magnet-free & rare-earth-free motor development

- 3.3.2 Emerging technologies

- 3.3.2.1 Digital twin architecture & implementation

- 3.3.2.2 Cloud vs Edge processing trade-offs

- 3.3.2.3 Over-the-Air (OTA) updates

- 3.3.2.4 Firmware update capabilities

- 3.3.1 Current technologies

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.5.1 SAE international standards

- 3.5.2 UNECE WP.29 regulations

- 3.5.3 Regulatory compliance cost analysis

- 3.5.4 Regulatory roadmap & future requirements

- 3.5.5 Regional regulatory comparison

- 3.5.5.1 North America

- 3.5.5.2 Europe

- 3.5.5.3 Asia-Pacific

- 3.5.5.4 Latin America

- 3.5.5.5 Middle East & Africa

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

- 3.8 Cost breakdown analysis

- 3.9 Price trends

- 3.9.1 Price arbitrage opportunities

- 3.9.2 Price erosion trends & commoditization

- 3.9.3 Impact of raw material price trends

- 3.9.4 Average Selling Price (ASP) Trends

- 3.10 Risk assessment & mitigation strategies

- 3.10.1 Risk identification & classification

- 3.10.2 Compliance & regulatory risks

- 3.10.3 Technology & innovation risks

- 3.10.4 Risk mitigation strategies

- 3.11 Patent analysis

- 3.11.1 Patent filings by region

- 3.11.2 Patent grant rates & timelines

- 3.11.3 Technology-specific patent analysis

- 3.11.4 Patent landscape mapping

- 3.12 Product Pipeline & R&D Roadmap

- 3.12.1 Product development pipeline analysis

- 3.12.2 Technology roadmap by key players

- 3.12.3 R&D focus areas & investment priorities

- 3.12.4 Collaborative R&D initiatives

- 3.13 Sustainability and environmental aspects

- 3.13.1 Carbon footprint of navigation systems

- 3.13.2 Circular economic strategies

- 3.13.3 Sustainable navigation features

- 3.13.4 Corporate sustainability initiatives

- 3.13.5 Climate change impact on navigation

- 3.14 Market adoption & penetration analysis

- 3.14.1 Technology adoption curve analysis

- 3.14.2 Penetration rates by region

- 3.14.3 Penetration rates by vehicle segment

- 3.14.4 Feature adoption analysis

- 3.14.5 Adoption acceleration strategies

- 3.15 Customer & End use insights

- 3.15.1 Qualification & certification requirements

- 3.15.2 OEM customer segmentation

- 3.15.3 OEM pain points & unmet needs

- 3.15.4 Tier-1 supplier customer analysis

- 3.16 Scenario planning & sensitivity analysis

- 3.16.1 Scenario planning framework

- 3.16.2 Base case scenario

- 3.16.3 Regulatory impact sensitivity

- 3.16.4 New entrants & business models

- 3.16.5 Regulatory impact sensitivity

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia-Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

- 4.6 Premium positioning strategies

- 4.7 Competitive analysis and USPs

Chapter 5 Market Estimates & Forecast, By Motor, 2022 - 2035 ($Bn, Units)

- 5.1 Key trends

- 5.2 Brushed DC Motors

- 5.3 Brushless DC Motors

- 5.4 Stepper Motors

Chapter 6 Market Estimates & Forecast, By Power Consumption, 2022 - 2035 ($Bn, units)

- 6.1 Key trends

- 6.2 3V-12V

- 6.3 12V-24V

- 6.4 25V-48V

- 6.5 More than 48V

Chapter 7 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Bn, Units)

- 7.1 Key trends

- 7.2 Passenger Cars

- 7.2.1 SUV

- 7.2.2 Sedan

- 7.2.3 Hatchback

- 7.3 Commercial Vehicles

- 7.3.1 LCV

- 7.3.2 MCV

- 7.3.3 HCV

Chapter 8 Market Estimates & Forecast, By Application, 2022 - 2035 ($Bn, Units)

- 8.1 Key trends

- 8.2 Power Windows

- 8.3 Windshield Wipers

- 8.4 Electric Power Steering (EPS)

- 8.5 Seat Adjustments

- 8.6 Mirror Adjustments

- 8.7 Sunroof Actuators

- 8.8 HVAC Systems

- 8.9 Others

Chapter 9 Market Estimates & Forecast, By Sales Channel, 2022 - 2035 ($Bn, Units)

- 9.1 Key trends

- 9.2 OEM

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn, Units)

- 10.1 North America

- 10.1.1 US

- 10.1.2 Canada

- 10.2 Europe

- 10.2.1 UK

- 10.2.2 Germany

- 10.2.3 France

- 10.2.4 Italy

- 10.2.5 Spain

- 10.2.6 Belgium

- 10.2.7 Netherlands

- 10.2.8 Sweden

- 10.2.9 Russia

- 10.3 Asia Pacific

- 10.3.1 China

- 10.3.2 India

- 10.3.3 Japan

- 10.3.4 Australia

- 10.3.5 Singapore

- 10.3.6 South Korea

- 10.3.7 Vietnam

- 10.3.8 Indonesia

- 10.4 Latin America

- 10.4.1 Brazil

- 10.4.2 Mexico

- 10.4.3 Argentina

- 10.5 MEA

- 10.5.1 South Africa

- 10.5.2 Saudi Arabia

- 10.5.3 UAE

Chapter 11 Company Profiles

- 11.1 Global players

- 11.1.1 Continental

- 11.1.2 Denso

- 11.1.3 Garmin

- 11.1.4 HARMAN International

- 11.1.5 Hyundai Mobis

- 11.1.6 Mitsubishi Electric

- 11.1.7 Panasonic

- 11.1.8 Robert Bosch

- 11.2 Region players

- 11.2.1 Alpine Electronics

- 11.2.2 Clarion

- 11.2.3 Desay SV Automotive

- 11.2.4 JVCKENWOOD

- 11.2.5 LG Electronics

- 11.2.6 Marelli

- 11.2.7 Pioneer

- 11.2.8 Valeo

- 11.2.9 Visteon

- 11.3 Emerging players

- 11.3.1 Aisin Corporation

- 11.3.2 Dynavin

- 11.3.3 Luxoft

- 11.3.4 NNG Software

- 11.3.5 Preh Car Connect

- 11.3.6 Vinland