|

시장보고서

상품코드

1892909

석유 및 가스용 전동 수중 펌프 시장 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2026-2035년)Oil and Gas Electric Submersible Pump Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

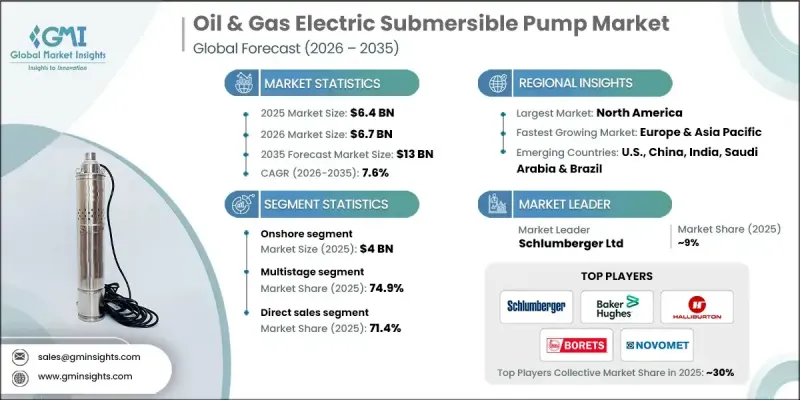

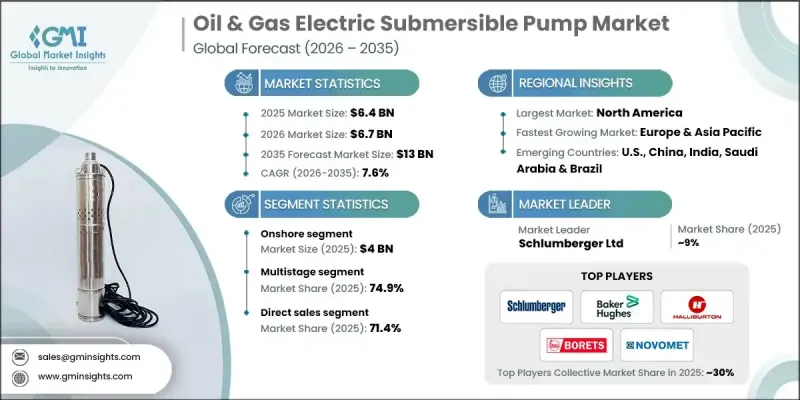

세계의 석유 및 가스용 전동 수중 펌프 시장은 2025년에 64억 달러로 평가되었고 2035년까지 연평균 복합 성장률(CAGR) 7.6%를 나타내 130억 달러에 달할 것으로 예측되고 있습니다.

신흥 경제국의 인구 증가와 급속한 산업화는 특히 확립된 시장에서 전례 없는 에너지 수요를 견인하고 있습니다. 이 에너지 수요의 급증으로 석유 및 가스 업계는 보다 선진적이고 효율적인 채굴 기술의 채용을 강요받고 있어 전동 수중 펌프가 그 중요한 역할을 담당하고 있습니다. ESP는 노후화된 유전에서의 생산성 향상과 대규모 조업에서 채굴 효율 최적화를 위해 널리 도입되고 있습니다. 이러한 이점이 있음에도 불구하고 초기 비용 상승과 같은 문제로 인해 특히 원유 가격이 부진한 시기에는 소규모 사업자에게 ESP를 도입하기가 어렵습니다. 그러나 펌프 설계 혁신, 내구성이 뛰어난 소재 및 실시간 모니터링 시스템의 통합으로 ESP는 점점 더 효율적이고 신뢰성이 높고 비용 효율적이며 에너지 수요가 증가하는 가운데 세계 생산 확대를 지원하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 연도 | 2026-2035년 |

| 시작 가치 | 64억 달러 |

| 예측 금액 | 130억 달러 |

| CAGR | 7.6% |

육상 부문은 2025년에 40억 달러를 차지했으며 2026년부터 2035년까지 연평균 복합 성장률(CAGR) 7.7%를 나타낼 것으로 예측됩니다. 이 성장은 성숙한 육상 유전에서 생산량을 유지할 필요성에 의해 견인되고 있으며, 인공 양수 솔루션은 생산 지속에 매우 중요합니다. 육상 사업은 해양 프로젝트보다 비용 효율적인 경향이 있으며 생산성을 최적화하면서 운영 경비를 관리하려는 사업자에게 매력적입니다. 탄화수소 수요 증가와 노후화된 저류층을 위한 증산기술의 발전으로 효율적인 유체처리와 생산율 향상을 위한 ESP(전기구동펌프)의 도입이 더욱 촉진되고 있습니다.

다단식 부문은 2025년에 74.9%의 점유율을 차지했고 2026년부터 2035년에 걸쳐 CAGR 7.3%를 나타낼 것으로 예상됩니다. 다수의 임펠러를 갖춘 다단식 ESP는 깊은 저장층에서 지표로 대량의 석유, 물, 가스를 이송하는 데 필요한 양력을 제공합니다. 이 펌프는 비 재래식, 해양 유전을 포함한 고용량, 복잡한 갱정에 이상적입니다. 탐사가 더 깊고 어려운 저류층으로 진행됨에 따라 다단식 시스템에 대한 수요는 꾸준히 증가하고 있습니다.

미국의 석유 및 가스용 전동 수중 펌프 시장은 2025년에 14억 1,000만 달러의 규모를 창출했으며, 2035년까지 연평균 복합 성장률(CAGR) 8.1%를 나타낼 것으로 추정됩니다. 신뢰성 향상, 효율성 향상, 디지털 모니터링 시스템과의 통합 등 ESP의 기술적 진보가 도입을 촉진하고 있어 운영자는 성능을 최적화하고 다운타임을 최소화할 수 있습니다. 해외 프로젝트에 투자하는 것 외에도 감쇠 우물에서 생산량을 극대화하는 비용 효율적인 기술의 필요성도 중요한 성장 촉진요인이 되었습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급업체 현황

- 이익률

- 각 단계별 부가가치

- 밸류체인에 영향을 주는 요인

- 업계에 미치는 영향요인

- 성장 촉진요인

- 세계 에너지 수요 증가

- 전기식 부상장치(ESP) 기술의 진전

- 심해 및 초심해 탐사

- 탄소 배출 감축에 대한 관심 증가

- 업계의 잠재적 위험 및 과제

- 초기 비용의 높이

- 복잡한 설치 및 유지보수

- 성장 촉진요인

- 성장 가능성 분석

- 향후 시장 동향

- 기술 및 혁신 현황

- 현재 기술 동향

- 신흥 기술

- 가격 동향

- 지역별

- 펌프 유형별

- 규제 상황

- 규격 및 컴플라이언스 요건

- 지역별 규제 프레임워크

- 인증기준

- 무역 통계

- 주요 수입국

- 주요 수출국

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 인수합병

- 파트너십 및 협력

- 신제품 출시

- 확대 계획

제5장 시장 추계·예측 : 펌프 유형별(2022-2035년)

- 원심식

- 축류식

- 용적식

- 프로그레시브 캐비티

제6장 시장 추계·예측 : 모터 유형별(2022-2035년)

- 유도 전동기

- 영구 자석 전동기(PMM)

- 고온 전동기

제7장 시장 추계·예측 : 출력별(2022-2035년)

- 500마력 이하

- 500-1,000마력

- 1,000-2,000마력

- 2,000마력 초과

제8장 시장 추계·예측 : 배포 방법별(2022-2035년)

- 기존 리그 기반 배치

- 대체 및 리그리스 배치

제9장 시장 추계·예측 : 유정 깊이별(2022-2035년)

- 얕은 유정(1,000m 이하)

- 중간 깊이(1,000-2,500미터)

- 심해(2,500-4,000미터)

- 초심해(4,000미터 초과)

제10장 시장 추계·예측 : 제어 시스템별(2022-2035년)

- 고정 주파수

- 가변 속도

- 디지털 최적화(지능형/IoT 대응 시스템)

제11장 시장 추계·예측 : 배포 모드별(2022-2035년)

- 육상

- 해상

제12장 시장 추계·예측 : 사업별(2022-2035년)

- 단단계

- 다단계

제13장 시장 추계·예측 : 용도별(2022-2035년)

- 원유 생산

- 가스 생산

- 물 주입

- 인공 리프트(EOR)

- 열회수

제14장 시장 추계·예측 : 유통 채널별(2022-2035년)

- 직접 판매

- 간접 판매

제15장 시장 추계·예측 : 지역별(2022-2035년)

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 인도네시아

- 말레이시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 남아프리카

제16장 기업 프로파일

- Atlas Copco AB

- Baker Hughes

- Borets International Ltd

- Crompton Greaves Consumer Electricals Limited

- EBARA CORPORATION

- Flowserve Corporation

- Gorman-Rupp Pumps

- Grundfos Holding A/S

- Halliburton

- Novomet

- Schlumberger Ltd

- Sulzer Ltd

- Tsurumi Manufacturing Co. Ltd.

- Weatherford

- WILO SE

The Global Oil & Gas Electric Submersible Pump Market was valued at USD 6.4 billion in 2025 and is estimated to grow at a CAGR of 7.6% to reach USD 13 billion by 2035.

The rising population and rapid industrialization in emerging economies are driving an unprecedented demand for energy, especially in well-established markets. This surge in energy requirements is pushing the oil and gas sector to adopt more advanced and efficient extraction technologies, with electric submersible pumps playing a key role. ESPs are widely deployed to enhance production in aging fields and optimize extraction efficiency for large-scale operations. Despite the benefits, challenges such as high upfront costs make ESP adoption difficult for smaller operators, particularly during periods of low oil prices. However, innovations in pump design, more durable materials, and the integration of real-time monitoring systems are making ESPs increasingly efficient, reliable, and cost-effective, supporting global production growth as energy demand continues to rise.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $6.4 Billion |

| Forecast Value | $13 Billion |

| CAGR | 7.6% |

The onshore segment accounted for USD 4 billion in 2025 and is expected to grow at a CAGR of 7.7% from 2026 to 2035. Growth is driven by the need to maintain output from mature onshore oilfields, where artificial lift solutions are critical for sustaining production. Onshore operations also tend to be more cost-effective than offshore projects, making them attractive to operators seeking to optimize productivity while controlling operational expenses. Rising hydrocarbon demand and enhanced recovery techniques for aging reservoirs are further boosting ESP adoption for efficient fluid handling and higher production rates.

The multistage segment held a 74.9% share in 2025 and is anticipated to grow at a CAGR of 7.3% from 2026 to 2035. Multistage ESPs, with multiple impellers, provide the necessary lift to transfer significant volumes of oil, water, and gas from deep reservoirs to the surface. These pumps are ideal for high-capacity, complex wells, including unconventional and offshore fields. As exploration moves toward deeper and more challenging reservoirs, the demand for multistage systems continues to rise steadily.

US Oil & Gas Electric Submersible Pump Market is generating USD 1.41 billion in 2025 and is expected to grow at a CAGR of 8.1% through 2035. Adoption is being driven by technological improvements in ESPs, such as enhanced reliability, greater efficiency, and integration with digital monitoring systems, which allow operators to optimize performance and minimize downtime. Investments in offshore projects, coupled with the need for cost-effective methods to maximize output from declining wells, are also significant growth factors.

Key players operating in the Global Oil & Gas Electric Submersible Pump Market include Schlumberger Ltd, Halliburton, Baker Hughes, Atlas Copco AB, Flowserve Corporation, Grundfos Holding A/S, Crompton Greaves Consumer Electricals Limited, EBARA CORPORATION, Gorman-Rupp Pumps, Novomet, Sulzer Ltd, Weatherford, WILO SE, Tsurumi Manufacturing Co. Ltd., and Borets International Ltd. Companies in the Oil & Gas Electric Submersible Pump Market are focusing on innovation, R&D, and digital integration to strengthen their market position. They are developing advanced pump designs with enhanced durability, energy efficiency, and real-time monitoring capabilities to optimize production and minimize downtime. Strategic partnerships with technology providers and digital solution companies allow operators to implement predictive maintenance and automation solutions. Firms are also expanding their geographic presence in emerging oil-producing regions and providing tailored services for onshore and offshore applications.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Pump type

- 2.2.3 Motor types

- 2.2.4 Power rating

- 2.2.5 Deployment method

- 2.2.6 Well depth

- 2.2.7 Control system

- 2.2.8 Deployment type

- 2.2.9 Operation

- 2.2.10 Application

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing global energy demand

- 3.2.1.2 Advancements in ESP technology

- 3.2.1.3 Deepwater and ultra-deepwater exploration

- 3.2.1.4 Rising focus on carbon emission reduction

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High initial costs

- 3.2.2.2 Complex installation and maintenance

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By pump type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Trade statistics

- 3.8.1 Major importing countries

- 3.8.2 Major exporting countries

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Pump Type, 2022 - 2035, (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Centrifugal

- 5.3 Axial flow

- 5.4 Positive displacement

- 5.5 Progressive cavity

Chapter 6 Market Estimates & Forecast, By Motor Types, 2022 - 2035, (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Induction motors

- 6.3 Permanent magnet motors (PMMs)

- 6.4 High-temperature motors

Chapter 7 Market Estimates & Forecast, By Power Rating, 2022 - 2035, (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Up to 500 HP

- 7.3 500-1000 HP

- 7.4 1000-2000 HP

- 7.5 Above 2000 HP

Chapter 8 Market Estimates & Forecast, By Deployment Method, 2022 - 2035, (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Conventional rig-based deployment

- 8.3 Alternative & rigless deployment

Chapter 9 Market Estimates & Forecast, By Well Depth, 2022 - 2035, (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Shallow wells (≤ 1,000 m)

- 9.3 Intermediate (1,000-2,500 m)

- 9.4 Deep (2,500-4,000 m)

- 9.5 Ultra-deep (> 4,000 m)

Chapter 10 Market Estimates & Forecast, By Control system, 2022 - 2035, (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 Fixed frequency

- 10.3 Variable speed

- 10.4 Digital optimization (Intelligent/IoT-enabled systems)

Chapter 11 Market Estimates & Forecast, By Deployment Type, 2022 - 2035, (USD Billion) (Thousand Units)

- 11.1 Key trends

- 11.2 Onshore

- 11.3 Offshore

Chapter 12 Market Estimates & Forecast, By Operation, 2022 - 2035, (USD Billion) (Thousand Units)

- 12.1 Key trends

- 12.2 Single stage

- 12.3 Multistage

Chapter 13 Market Estimates & Forecast, By Application, 2022 - 2035, (USD Billion) (Thousand Units)

- 13.1 Key trends

- 13.2 Oil production

- 13.3 Gas production

- 13.4 Water injection

- 13.5 Artificial lift (EOR)

- 13.6 Thermal recovery

Chapter 14 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Billion) (Thousand Units)

- 14.1 Key trends

- 14.2 Direct sales

- 14.3 Indirect sales

Chapter 15 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Billion) (Thousand Units)

- 15.1 Key trends

- 15.2 North America

- 15.2.1 U.S.

- 15.2.2 Canada

- 15.3 Europe

- 15.3.1 Germany

- 15.3.2 UK

- 15.3.3 France

- 15.3.4 Italy

- 15.3.5 Spain

- 15.4 Asia Pacific

- 15.4.1 China

- 15.4.2 India

- 15.4.3 Japan

- 15.4.4 South Korea

- 15.4.5 Australia

- 15.4.6 Indonesia

- 15.4.7 Malaysia

- 15.5 Latin America

- 15.5.1 Brazil

- 15.5.2 Mexico

- 15.5.3 Argentina

- 15.6 MEA

- 15.6.1 Saudi Arabia

- 15.6.2 UAE

- 15.6.3 South Africa

Chapter 16 Company Profiles

- 16.1 Atlas Copco AB

- 16.2 Baker Hughes

- 16.3 Borets International Ltd

- 16.4 Crompton Greaves Consumer Electricals Limited

- 16.5 EBARA CORPORATION

- 16.6 Flowserve Corporation

- 16.7 Gorman-Rupp Pumps

- 16.8 Grundfos Holding A/S

- 16.9 Halliburton

- 16.10 Novomet

- 16.11 Schlumberger Ltd

- 16.12 Sulzer Ltd

- 16.13 Tsurumi Manufacturing Co. Ltd.

- 16.14 Weatherford

- 16.15 WILO SE