|

시장보고서

상품코드

1913297

고무 가공용 화학제품 시장 예측 : 기회, 성장 요인, 업계 동향 분석(2026-2035년)Rubber Processing Chemicals Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

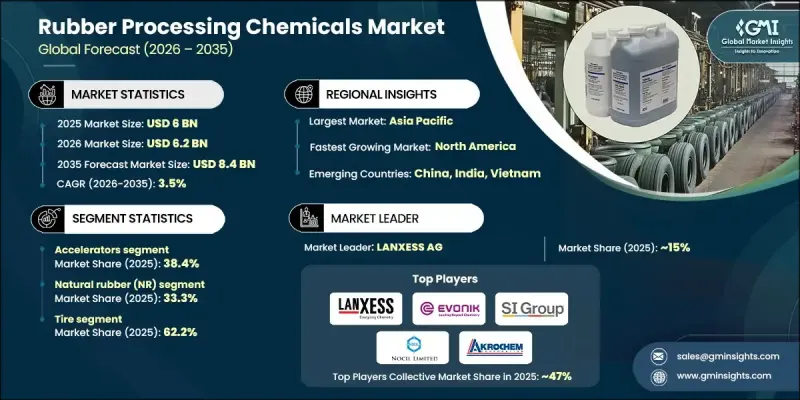

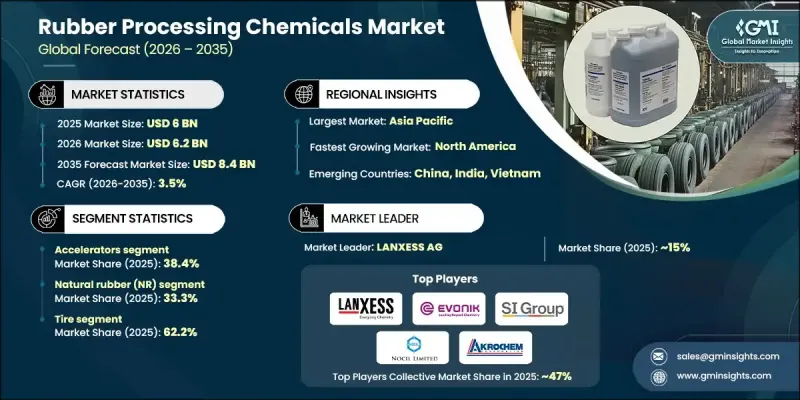

세계의 고무 가공용 화학제품 시장은 2025년에 60억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 3.5%로 성장하여 84억 달러에 이를 것으로 예측됩니다.

고무 가공용 화학제품은 천연 고무 및 합성 고무의 내구성, 가공 효율, 기능 성능을 향상시켜 고무 제조에 있어서 기본적인 역할을 합니다. 이러한 제제는 가황 효율, 내열성, 접착 특성, 난연성 및 재료 전체의 안정성을 개선하여 고무 생산의 중요한 단계를 지원합니다. 시장의 성장은 운송, 산업 생산, 인프라 개발 및 지속가능성을 중시하는 생산 기법의 지속적인 변화에 의해 형성됩니다. 제조업체 각 회사는 진화하는 규제 프레임 워크와 기업의 지속가능성 목표에 부합하기 때문에 환경 친화적 인 화학 솔루션을 점점 더 우선시하고 있습니다. 그 결과 시장은 성능을 유지하면서 환경 부하를 줄이는 선진적이고 깨끗한 화학 기술로 꾸준히 전환하고 있습니다. 다양한 산업용도에서 고품질 고무 제품에 대한 수요 증가와 고무 배합 기술의 진보가 함께 장기적인 수요를 지속적으로 강화하고 있습니다. 현대적인 제조 시스템의 확대와 세계 시장의 성능 일관성에 대한 기대 증가가 고무 가공용 화학제품의 꾸준한 진화를 더욱 강화하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 연도 | 2026-2035년 |

| 시작 금액 | 60억 달러 |

| 예측 금액 | 84억 달러 |

| CAGR | 3.5% |

가속제 부문은 2025년에 38.4%의 점유율을 차지했고 2035년까지 연평균 복합 성장률(CAGR) 3.7%로 성장할 것으로 예측됩니다. 이 이점은 가황 거동을 제어하고 생고무를 내구성있는 탄성 재료로 변환하는 데 필수적인 기능으로 인해 발생합니다. 가속제는 최적의 강도, 유연성 및 내열성을 실현하는 역할 때문에 모든 고무 가공 공정에서 여전히 필수적입니다.

천연 고무 부문은 2025년에 33.3%의 점유율을 차지했고 2035년까지 연평균 복합 성장률(CAGR)은 3.8%를 보일 것으로 예측됩니다. 그 주도적 지위는 엄격한 성능 요건을 뒷받침하는 고유의 기계적 이점에서 비롯됩니다. 천연 고무의 독특한 분자 구조는 시장 변동에도 불구하고 그 중요성을 계속 유지하고 있으며 성능에 중점을 둔 고무 응용 분야에서 일관된 수요를 보장합니다.

미국 고무 가공용 화학제품 시장은 2025년 10억 달러 규모에 달했습니다. 이 나라의 성장은 성숙한 제조거점과 자동차 및 산업용 고무 생산의 강한 수요에 의해 뒷받침됩니다. 확립된 공급 생태계와 첨단 고무 배합에 대한 지속적인 투자는 북미 전역에서 안정적인 시장 동향에 기여하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급업체 현황

- 수익률

- 단계별 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 업계의 잠재적 위험 및 과제

- 시장 기회

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 기술과 혁신 동향

- 현재의 기술 동향

- 신규 기술

- 가격 동향

- 지역별

- 제품 유형별

- 장래 시장 동향

- 특허 동향

- 무역 통계(HS코드)(참고: 무역 통계는 주요 국가에 대해서만 제공됨.)

- 주요 수입국

- 주요 수출국

- 지속가능성과 환경면

- 지속가능한 대처

- 폐기물 감축 전략

- 생산에 있어서의 에너지 효율

- 친환경 이니셔티브

- 탄소발자국 고려

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병 및 인수

- 제휴 및 협업

- 신제품 발매

- 확대 계획

제5장 시장 추정 및 예측 : 제품 유형별, 2022-2035

- 촉진제

- Thiazoles

- Sulfenamides

- Thiurams

- Guanidines

- Dithiocarbamates

- Thiophosphates

- Thioureas

- Aldehyde amines

- 열화 방지제

- 산화 방지제

- 오존 방지제

- 왁스류

- 실란 결합제

- 에톡시실란

- 메톡시실란

- Mercaptosilanes

- 신규 결합 시스템

- 실란 대체품

- 가공 조제 및 가소제

- 가소제

- 펩타이저

- 분산제

- 가공 촉진제

- 몰드 방출제

- 윤활제

- 바이오 베이스 가공 보조제

- 난연제

- 할로겐계 난연제

- 인계 난연제

- 무기 충전제

- 기타

제6장 시장 추정 및 예측 : 고무 유형별, 2022-2035

- 천연 고무(NR)

- SBR(용액 및 에멀젼)

- 니트릴 고무(NBR)

- EPDM

- 부틸 고무 및 할로부틸 고무

- 특수 고무

제7장 시장 추정 및 예측 : 용도별, 2022-2035

- 타이어

- 자동차(비타이어 용도)

- 산업제품

- 건설

- 전선 및 케이블

- 의료 및 헬스케어

- 소비재

- 항공우주

제8장 시장추정 및 예측 : 지역별, 2022-2035

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 기타 라틴아메리카

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

제9장 기업 프로파일

- LANXESS AG

- Evonik Industries

- SI Group

- Nocil Limited

- Akrochem Corporation

- Sennics Co., Ltd.

- RT Vanderbilt

- KUMHO PETROCHEMICAL

- Duslo as

- Struktol Company

- Robinson Brothers

- Sinopec Corp.

- China Sunsine

- Eastman Chemical

- Arkema SA

The Global Rubber Processing Chemicals Market was valued at USD 6 billion in 2025 and is estimated to grow at a CAGR of 3.5% to reach USD 8.4 billion by 2035.

Rubber processing chemicals play a foundational role in rubber manufacturing by enhancing durability, processing efficiency, and functional performance of both natural and synthetic rubber. These formulations support critical stages of rubber production by improving curing efficiency, resistance to degradation, adhesion properties, flame resistance, and overall material stability. Market growth is shaped by ongoing changes in transportation, industrial manufacturing, infrastructure development, and sustainability-driven production practices. Manufacturers are increasingly prioritizing environmentally responsible chemical solutions to align with evolving regulatory frameworks and corporate sustainability goals. As a result, the market is steadily transitioning toward advanced and cleaner chemistries that maintain performance while reducing environmental impact. The growing need for high-quality rubber products across diverse industrial applications, combined with advancements in rubber formulation technologies, continues to reinforce long-term demand. Expansion of modern manufacturing systems and rising expectations for performance consistency across global markets further support the steady evolution of rubber processing chemicals.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $6 Billion |

| Forecast Value | $8.4 Billion |

| CAGR | 3.5% |

The accelerators segment held a 38.4% share in 2025 and is expected to grow at a CAGR of 3.7% through 2035. This dominance is attributed to their indispensable function in controlling curing behavior and enabling the transformation of raw rubber into durable, elastic materials. Accelerators remain essential across all rubber processing activities due to their role in achieving optimal strength, flexibility, and thermal resistance.

The natural rubber segment accounted for 33.3% share in 2025 and is forecast to grow at a CAGR of 3.8% by 2035. Its leadership stems from inherent mechanical advantages that support demanding performance requirements. The unique molecular structure of natural rubber continues to sustain its relevance despite market fluctuations, ensuring consistent demand across performance-focused rubber applications.

U.S. Rubber Processing Chemicals Market generated USD 1 billion in 2025. Growth in the country is supported by a mature manufacturing base and strong demand from automotive and industrial rubber production. A well-established supply ecosystem and continued investment in advanced rubber formulations contribute to stable market momentum across North America.

Key companies active in the Rubber Processing Chemicals Market include Evonik Industries, LANXESS AG, Eastman Chemical, Arkema S.A., SI Group, China Sunsine, Nocil Limited, KUMHO PETROCHEMICAL, Robinson Brothers, R.T. Vanderbilt, Akrochem Corporation, Duslo a.s., Sennics Co., Ltd., Sinopec Corp., and Struktol Company. Companies operating in the Global Rubber Processing Chemicals Market are reinforcing their market position through innovation-led product development and sustainability-focused strategies. Many players are investing in research to create high-performance formulations that comply with stricter environmental standards while maintaining efficiency and durability. Capacity expansion in emerging manufacturing regions and strengthening distribution networks remain key priorities. Strategic collaborations with rubber producers help companies deliver customized solutions and improve long-term customer engagement.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Product Type

- 2.2.2 Rubber Type

- 2.2.3 Application

- 2.2.4 Regional

- 2.3 TAM Analysis, 2025-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product type

- 3.9 Future market trends

- 3.10 Patent landscape

- 3.11 Trade statistics (HS code)( Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Accelerators

- 5.2.1 Thiazoles

- 5.2.2 Sulfenamides

- 5.2.3 Thiurams

- 5.2.4 Guanidines

- 5.2.5 Dithiocarbamates

- 5.2.6 Thiophosphates

- 5.2.7 Thioureas

- 5.2.8 Aldehyde amines

- 5.3 Antidegradants

- 5.3.1 Antioxidants

- 5.3.2 Antiozonants

- 5.3.3 Waxes

- 5.3.4 Silane coupling agents

- 5.4 Ethoxy silanes

- 5.4.1 Methoxy silanes

- 5.4.2 Mercaptosilanes

- 5.4.3 Novel coupling systems

- 5.4.4 Silane alternatives

- 5.5 Processing aids & plasticizers

- 5.5.1 Plasticizers

- 5.5.2 Peptizers

- 5.5.3 Dispersing agents

- 5.5.4 Processing promoters

- 5.5.5 Mold release agents

- 5.5.6 Lubricants

- 5.5.7 Bio-based processing aids

- 5.6 Flame retardants

- 5.6.1 Halogenated flame retardants

- 5.6.2 Phosphorus-based flame retardants

- 5.6.3 Mineral fillers

- 5.7 Others

Chapter 6 Market Estimates and Forecast, By Rubber Type, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Natural rubber (NR)

- 6.3 SBR (solution & emulsion)

- 6.4 Nitrile rubber (NBR)

- 6.5 EPDM

- 6.6 Butyl & halobutyl rubber

- 6.7 Specialty rubbers

Chapter 7 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Tire

- 7.3 Automotive (non-tire)

- 7.4 Industrial goods

- 7.5 Construction

- 7.6 Wire & cable

- 7.7 Medical & healthcare

- 7.8 Consumer goods

- 7.9 Aerospace

Chapter 8 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 LANXESS AG

- 9.2 Evonik Industries

- 9.3 SI Group

- 9.4 Nocil Limited

- 9.5 Akrochem Corporation

- 9.6 Sennics Co., Ltd.

- 9.7 R.T. Vanderbilt

- 9.8 KUMHO PETROCHEMICAL

- 9.9 Duslo a.s.

- 9.10 Struktol Company

- 9.11 Robinson Brothers

- 9.12 Sinopec Corp.

- 9.13 China Sunsine

- 9.14 Eastman Chemical

- 9.15 Arkema S.A.