|

시장보고서

상품코드

2062120

고무 가황 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Rubber Vulcanization - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

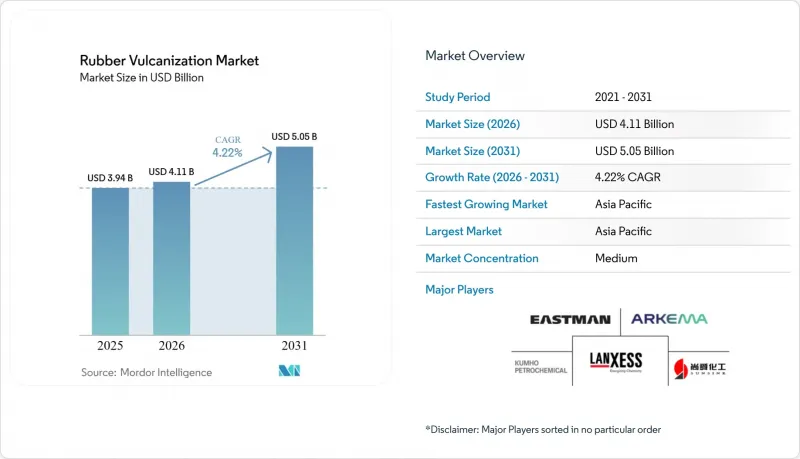

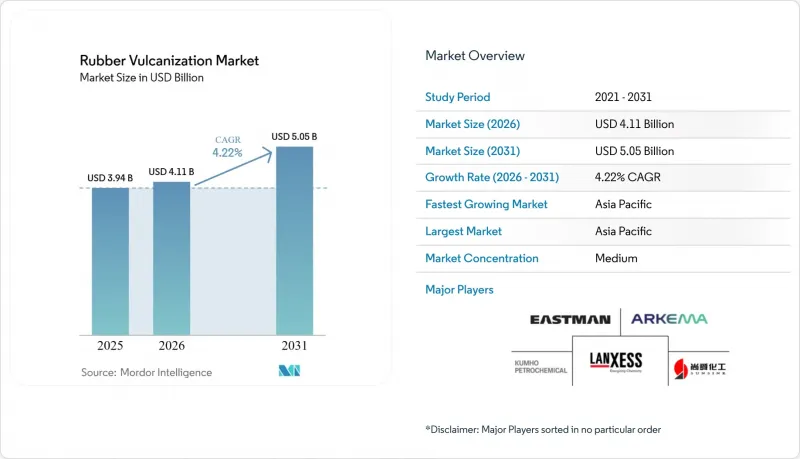

Mordor Intelligence에 의하면, 고무 가황 시장 규모는 2025년에 39억 4,000만 달러로 평가되었습니다. 2026년 41억 1,000만 달러에서 2031년까지 50억 5,000만 달러로 확대되어 2026-2031년에 걸쳐 CAGR은 4.22%를 나타낼 것으로 예측되고 있습니다.

본 보고서는 제품 유형(가속제, 가황제, 활성화제, 기타), 용도(자동차 및 운송, 산업용, 소비재, 신발, 기타), 지역(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 고무 가황 시장 동향 및 인사이트

고성능·저구름저항 고무 컴파운드로의 전환

타이어의 에너지 효율에 관한 전 세계적인 규제를 배경으로, 각 컴파운더 기업들은 카본블랙에서 침전 실리카로의 전환을 추진하고 있습니다. 이러한 전환에 따라, 더 낮은 온도에서 가황을 시작할 수 있는 티우람계 및 설펜아미드계 가황 촉진제의 사용이 필요하게 됩니다. 콘티넨탈은 2025년에 ‘EcoContact 7’ 타이어를 출시하여, 젖은 노면에서의 접지력을 저하시키지 않으면서도 구름 저항을 줄이는 데 성공했습니다. 이는 천연 고무에 초고속 CBS 가황 촉진제를 배합함으로써 달성되었습니다. 앞으로 시행될 유럽연합(EU)의 규정에 따라, 제품의 탄소 발자국을 나타내는 QR 코드 표기가 의무화됩니다. 이에 따라 탄소 발자국이 적은 가황 촉진제는 OEM의 조달 과정에서 중요한 기준이 됩니다. 이에 대응하여 BASF는 2026년, 제품의 탄소 발자국을 줄인 부탄디올 및 PolyTHF 제품 라인을 출시하여, 배합 설계자들이 배출량을 대폭 감축했다는 점을 강조할 수 있도록 했습니다. 또한, Kraton의 SYLVATRAXX와 같은 바이오 첨가제가 이러한 배합을 강화하여 반발 특성을 유지하면서 접지력을 향상시키고 있습니다.

아시아·태평양 지역의 제조업 및 인프라 투자 확대

2025년, 중국은 세계 생산량에서 큰 비중을 차지하며 다수의 승용차용 타이어를 생산했습니다. 한편, 2026년에는 인도 역시 전년 대비 생산량이 크게 증가했습니다. 양국 모두 주요 국내 브랜드들의 막대한 투자를 바탕으로 신규 생산 능력 확충을 추진하고 있습니다. 업스트림 부문에서는 금호석유화학과 도소가 맞춤형 가황 포장이 필요한 특수 엘라스토머 제품의 생산 라인을 확대되고 있습니다. 이와 동시에, 랑세스는 해당 지역의 적시 생산(JIT) 수요에 대응하기 위해 칭다오에 위치한 프로모터 공장의 생산량을 대폭 늘렸습니다. 이러한 전략적인 현지화는 아시아태평양의 수출 주도형 타이어 산업 확장과 발맞추어, 고무 가황용 화학제품 시장의 성장을 부각시키고 있습니다.

원자재 가격의 변동성 - 부타디엔, 유황, 산화아연

2025년, 중국의 부타디엔 가격이 상승했습니다. 2026년 초에는 북미의 계약 가격도 대폭 상승하여, 비통합형 촉진제 제조업체들에게 큰 가격 차이가 발생했고, 헤지하기 어려운 상황이 되었습니다. 동 기간 동안 이란 광산의 생산량 감소로 인해 유황 가격이 급등하여 심각한 공급 부족이 발생했습니다. 또한, 원가 상승으로 인해 제련소가 생산량을 줄였기 때문에 2026년 초에는 산화아연 가격도 상승했습니다. 이러한 가격 동향으로 인해 이익률이 압박을 받으면서, NOCIL의 2026 회계연도 3분기 이자·세금·감가상각비·상각비 차감 전 이익(EBITDA)이 감소했습니다. 대형 다국적 기업들은 여러 지역에 걸친 조달 네트워크를 활용하여 이러한 과제를 극복했지만, 중소기업들은 고정 계약에 얽매인 채로 있어 운전자금에 압박을 받고 있습니다.

부문별 분석

2025년 매출액에서 가속제가 차지하는 비중은 41.11%에 달했으며, 모든 주요 고무 배합에서 핵심적인 역할을 하고 있음이 확인되었습니다. 설페나미드 계열 제품은 가소화 온도에서 충분한 스코치 안전성을 확보하고, 압착 온도에서 단시간 내에 완전한 가황을 달성하기 때문에 타이어 및 산업용 제품 분야에서 대표적인 제품으로서의 입지를 확고히 하고 있습니다. 치우람 계열 가속제는 비싸지만, 유황 첨가량을 최소한으로 줄일 수 있습니다. 이 특성은 저회전저항 트레드 컴파운드에 있어 매우 중요하며, 콘티넨탈은 이를 ‘EcoContact 7’에 적용했습니다. 산화아연과 같은 활성제는 숙성 과정이 느리지만, 마이크로파 개질 기술을 통해 열적 핫스팟에 대한 내성을 갖춘 마그네슘계 변형체 수요가 증가하고 있습니다. 고무 가황용 화학제품 시장에서 가황제 시장 규모는 촉진제 시장 규모를 상회할 것으로 예측됩니다. 이러한 변화는 유황 공급제 및 과산화물 계열이 유황 공급 및 고온 환경에서의 내구성과 관련된 과제를 효과적으로 해결함에 따라, 2026년부터 2031년까지 연평균 성장률(CAGR) 4.63%로 시장 규모가 확대되고 있기 때문입니다. China Sunsine과 NOCIL은 통합형 황 공급제 포장에 주력하고 있으며, 원스톱 포장을 선호하는 고객을 확보하는 것을 목표로 하고 있습니다.

가황제에는 원소 유황, 황 공여제, 과산화물, 특수 불용성 유황이 포함됩니다. 고가형 불용성 유황은 레이디얼 벨트의 표면 블룸 현상을 효과적으로 방지합니다. 한편, 과산화물 가황 방식은 에틸렌-프로파일렌-디엔-모노머(EPDM) 호스, 특히 기존 파워트레인보다 고온에서 작동하는 전기차의 냉각 회로에서 점차 보급되고 있습니다. 현재 중국공급업체들은 가황 촉진제와 유황 공급제를 결합한 마스터배치를 제공함으로써 물류 효율화를 도모하고 있습니다. 이는 시장 점유율을 유지하기 위해 유럽과 미국의 중견 기업들이 따라야 할 서비스입니다. 또한, 마이크로파 가황의 보급으로 인해 가교 반응을 대폭 단축할 수 있는 초고속 가교제 수요가 증가하고 있습니다. 이러한 동향은 고무 가황 화학제품 시장에서 상품화보다 혁신이 더 중요시되고 있음을 보여줍니다.

지역별 분석

아시아태평양은 2025년 매출의 50.22%를 차지했으며, 2026년부터 2031년까지 연평균 성장률(CAGR) 5.13%를 나타낼 것으로 예측됩니다. 중국은 승용차용 타이어 생산량이 압도적으로 많으며, 인도가 그 뒤를 잇고 있습니다. 새로운 레이디얼 타이어 공장에 대한 막대한 투자가 계속해서 이루어지고 있습니다. LANXESS는 칭다오 공장의 생산 능력을 대폭 확대했습니다. 한편, 차이나 선샤인은 대규모 가황 라인을 활용하여 경쟁력 있는 단가로 통합 포장을 제공합니다. 일본에서는 토소가 클로로프렌 고무의 제품 라인을 확대하고 있는데, 이는 수입에 의존하는 가황제에 대한 수요를 보여주는 것으로, 아시아 선진 시장의 지속적인 수요를 뒷받침하고 있습니다.

북미와 유럽은 세계 수요의 상당 부분을 차지하고 있습니다. 성장은 견조한 추세를 보이고 있지만, 자동차 보유 대수의 포화 상태와 특히 특정 화학 물질에 대한 규제 강화와 같은 과제로 인해 그 기세가 주춤하고 있습니다. LANXESS는 사우스캐롤라이나주에서 특수 등급 제품의 생산을 시작하여, 미국 타이어 제조업체에 현지 조달처를 제공하는 동시에 운송 시간을 단축하고 있습니다. BASF는 배기가스 표시 기준을 준수하기 위해 친환경 전구체를 채택하고, 중국에 위치한 통합 생산 거점을 100% 재생에너지로 전환함으로써 유럽 고객들에게 규정 준수 측면에서 우위를 제공합니다.

남미, 중동 및 아프리카의 합산 점유율은 전체 시장에서 비교적 낮은 임베디드니다. 브라질은 트럭 및 버스용 레이디얼 타이어 생산량을 늘리고 있으며, 멕시코도 상당한 수준의 타이어 생산을 유지하고 있지만, 두 나라 모두 아시아에서 가황 촉진제를 수입하는 데 크게 의존하고 있습니다. 이란산 유황 공급이 감소함에 따라, 이 지역에서는 원료 공급이 부족해지고 있습니다. 이에 대응하여 브라질의 여러 공장에서 황 사용량을 대폭 줄이는 대체 시스템에 대한 실험을 진행하고 있습니다. 사우디아라비아는 지역 수요에 부응하기 위해 타이어 생산 능력을 확대하고 있으며, 이러한 생산 라인이 가동되면 특수 가황제에 새로운 기회가 생길 것으로 보입니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.22According to Mordor Intelligence, the rubber vulcanization market size was valued at USD 3.94 billion in 2025 and is expected to grow from USD 4.11 billion in 2026 to USD 5.05 billion by 2031, growing at a CAGR of 4.22% from 2026 to 2031.

This report is Segmented by Product Type (Accelerators, Vulcanizing Agents, Activators, and Others), Application (Automotive and Transportation, Industrial, Consumer Goods, Footwear, and Others), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Rubber Vulcanization Market Trends and Insights

Shift Toward High-Performance, Low-Rolling-Resistance Rubber Compounds

Driven by global mandates on tire energy efficiency, compounders are shifting from carbon black to precipitated silica. This transition necessitates the use of thiuram and sulfenamide accelerators, which can initiate curing at lower temperatures. Continental introduced its EcoContact 7 tire in 2025, achieving a reduction in rolling resistance without compromising wet grip. This was accomplished by blending natural rubber with ultra-fast CBS accelerators. A forthcoming European Union regulation mandates a QR code indicating a product's carbon footprint. This makes low-product-carbon-footprint accelerators a key criterion for original equipment manufacturer procurement. In response, BASF launched a 2026 line of butanediol and PolyTHF with reduced product carbon footprint, enabling formulators to tout significant emission reductions. Additionally, bio-based additives like Kraton's SYLVATRAXX are enhancing these formulations, boosting traction while preserving rebound properties.

Expansion of Asia-Pacific Manufacturing and Infrastructure Spend

In 2025, China accounted for a significant share of global production, manufacturing a substantial number of passenger-car tires. Meanwhile, in 2026, India also recorded notable growth in production compared to the previous year. Both nations are strengthening their greenfield capacities, supported by considerable investments from leading domestic brands. On the upstream front, Kumho Petrochemical and Tosoh are expanding their specialty elastomer lines, which require customized curing packages. Concurrently, LANXESS has significantly increased the output of its Qingdao promoter plant to meet the region's just-in-time demand. This strategic localization highlights the growth of the rubber vulcanization chemicals market, aligning with the expansion of Asia-Pacific's export-driven tire industry.

Raw-Material Price Volatility - Butadiene, Sulfur, Zinc Oxide

In 2025, Chinese butadiene prices experienced an increase. By early 2026, North American contracts also saw a significant rise, creating a challenging price gap for non-integrated accelerator producers, making hedging difficult. During the same period, sulfur prices witnessed a substantial surge due to reduced output from Iranian mines, which resulted in a notable supply deficit. Zinc oxide prices also increased in early 2026 as smelters reduced production because of higher costs. These price dynamics have led to tighter profit margins, with NOCIL's earnings before interest, taxes, depreciation, and amortization declining in the third quarter of the fiscal year 2026. Larger multinational companies have managed to navigate these challenges by leveraging multi-regional sourcing networks, while smaller firms remain constrained by fixed contracts, putting pressure on their working capital.

Other drivers and restraints analyzed in the detailed report include:

- Industrial Demand for Conveyor, Hose and Belt Upgrades

- Microwave and Continuous-Line Vulcanization Retrofits Slash Cure Time

- 6PPD-Quinone Eco-Toxicity Scrutiny and Potential Bans

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Accelerators contributed 41.11% of 2025 sales, confirming their central role in every major rubber recipe. Sulfenamide grades ensure sufficient scorch safety at mixing temperatures and achieve full curing in a short time at press temperatures, solidifying their status as a staple for tires and industrial products. While more expensive, Thiuram accelerators allow for minimal sulfur loadings. This capability is crucial for low-rolling-resistance tread compounds, a feature Continental integrated into its EcoContact 7. While activators like zinc oxide have a slow maturation process, there is a rising demand for magnesium-based variants, which resist thermal hotspots, thanks to microwave retrofits. The market for vulcanizing agents in rubber vulcanization chemicals is projected to surpass that of accelerators. This shift comes as sulfur donors and peroxide systems effectively tackle challenges related to sulfur supply and durability at high temperatures, expanding at a 4.63% CAGR between 2026 and 2031. China Sunsine and NOCIL are doubling down on integrated sulfur-donor packages, aiming to lock in customers that prefer a single-source bundle.

Vulcanizing agents include elemental sulfur, sulfur donors, peroxides, and specialty insoluble sulfur. Insoluble sulfur, which commands a premium, effectively eliminates surface bloom on radial belts. Meanwhile, peroxide curing is gaining traction in ethylene propylene diene monomer hoses, especially for electric-vehicle coolant circuits that operate at higher temperatures than traditional powertrains. Chinese suppliers are now providing combined accelerator-sulfur donor masterbatches, streamlining logistics. This is a service that mid-sized western firms need to match to maintain their market share. Additionally, microwave curing is driving up demand for ultra-fast donors, capable of completing cross-linking in a significantly reduced time. This trend underscores the rubber vulcanization chemicals market's preference for innovation over commoditization.

Geography Analysis

Asia-Pacific accounted for 50.22% of 2025 revenue and is expected to advance at a 5.13% CAGR through 2026 to 2031. China leads with a significant output of passenger-car tires, followed closely by India. Substantial investments continue to flow into new radial plants. LANXESS has notably increased capacity at its Qingdao facility. Meanwhile, China Sunsine is utilizing its large-scale accelerator line to deliver integrated packages at competitive landed costs. In Japan, Tosoh is expanding its offerings with chloroprene rubber, dependent on imported vulcanization chemicals, signaling a sustained demand in developed Asian markets.

North America and Europe account for a considerable portion of the global demand. Growth remains steady but is tempered by a mature vehicle parc and regulatory challenges, notably the impending limits on certain chemical compounds. LANXESS has commenced production of specialized grades in South Carolina, providing United States tire manufacturers with a local source and reducing freight times. BASF, in a bid to meet emission-labeling standards, has adopted environmentally friendly precursors and transitioned its Verbund site in China to fully renewable energy, offering a compliance edge to European clients.

South America, the Middle-East and Africa collectively account for a smaller share of the market. Brazil has increased its truck-bus-radial output, while Mexico has maintained a notable level of tire production, with both nations heavily reliant on accelerator imports from Asia. Due to reduced sulfur availability from Iran, feedstock supplies have tightened in this region. In response, several Brazilian plants are experimenting with alternative systems that significantly reduce sulfur input. Saudi Arabia is expanding its tire production capacity to cater to regional demand, presenting new opportunities for specialty curing agents once these lines become operational.

- Arkema

- BASF

- Bolflex

- China Sunsine Chemical Holdings Ltd.

- Duslo a.s.

- Eastman Chemical Company

- Finorchem

- KUMHO PETROCHEMICAL

- LANXESS

- NOCIL Ltd

- OSAKA SODA

- OUCHI SHINKO CHEMICAL INDUSTRIAL CO., LTD

- Sumitomo Chemical Co., Ltd.

- Thomas Swan

- Tianjin Kemai Chemical

- Vanderbilt Holding Company, Inc.

- Zhejiang Baina Rubber & Plastic Equipment Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Shift toward high-performance, low-rolling-resistance rubber compounds

- 4.2.2 Expansion of Asia-Pacific manufacturing and infrastructure spend

- 4.2.3 Industrial demand for conveyor, hose and belt upgrades

- 4.2.4 Microwave and continuous-line vulcanization retrofits slash cure time

- 4.2.5 AI-driven real-time cure-profile optimization boosting plant yield

- 4.3 Market Restraints

- 4.3.1 Raw-material price volatility-butadiene, sulfur, zinc oxide

- 4.3.2 6PPD-quinone eco-toxicity scrutiny and potential bans

- 4.3.3 Sulfur-supply shocks from mining curtailments in 2026-27

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Accelerators

- 5.1.2 Vulcanizing Agents

- 5.1.3 Activators

- 5.1.4 Others

- 5.2 By Application

- 5.2.1 Automotive and Transportation

- 5.2.2 Industrial

- 5.2.3 Consumer Goods

- 5.2.4 Footwear

- 5.2.5 Others

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN

- 5.3.1.6 Australia and New Zealand

- 5.3.1.7 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 France

- 5.3.3.3 United Kingdom

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Russia

- 5.3.3.7 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 Arkema

- 6.4.2 BASF

- 6.4.3 Bolflex

- 6.4.4 China Sunsine Chemical Holdings Ltd.

- 6.4.5 Duslo a.s.

- 6.4.6 Eastman Chemical Company

- 6.4.7 Finorchem

- 6.4.8 KUMHO PETROCHEMICAL

- 6.4.9 LANXESS

- 6.4.10 NOCIL Ltd

- 6.4.11 OSAKA SODA

- 6.4.12 OUCHI SHINKO CHEMICAL INDUSTRIAL CO., LTD

- 6.4.13 Sumitomo Chemical Co., Ltd.

- 6.4.14 Thomas Swan

- 6.4.15 Tianjin Kemai Chemical

- 6.4.16 Vanderbilt Holding Company, Inc.

- 6.4.17 Zhejiang Baina Rubber & Plastic Equipment Co., Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment