|

시장보고서

상품코드

1913302

구조용 접착제 시장 예측 : 기회, 성장 요인, 업계 동향 분석(2026-2035년)Structural Adhesive Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

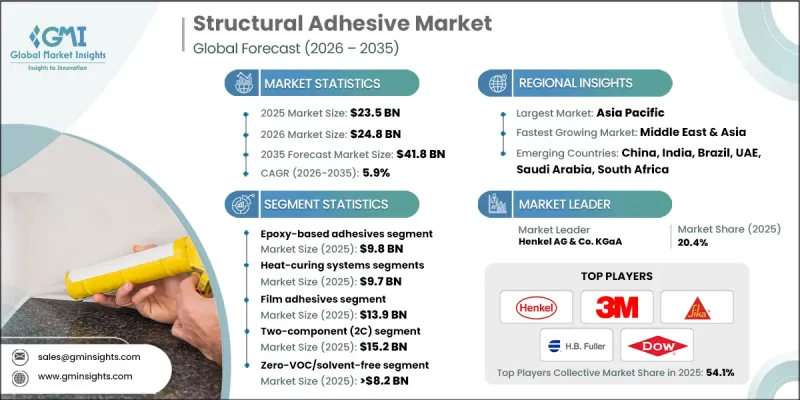

세계의 구조용 접착제 시장은 2025년에 235억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 5.9%로 성장하여 418억 달러에 이를 것으로 예측되고 있습니다.

구조용 접착제는 자동차, 항공우주, 전자기기, 선박, 풍력에너지, 건설 등 다양한 산업에서의 채택이 증가하고 있기 때문에 현저한 성장을 이루고 있습니다. 이러한 접착제는 균일한 응력 분산 및 경량 어셈블리가 요구되는 용도에서 용접 및 기계적 체결 부품을 점차적으로 대체합니다. 전기차 생산 급증과 항공기에 복합재료의 통합이 이 전환을 가속화하고 있습니다. 게다가 규제 프레임워크가 시장을 수계, 저 VOC, 제로 VOC 배합 등 환경 친화적인 화학제품으로 인도하고 있으며, 지속가능성과 컴플라이언스 기준에 따른 움직임이 되고 있습니다. 시장 성장은 대규모 자동차 생산에 의해 견인되고 있으며, 바디 인 화이트, 유리 장착 및 배터리 조립에서 구조용 접착제에 대한 수요가 증가하고 있습니다. 동시에, 엄격한 환경 규제는 솔벤트 프리 및 저 배출 대체품을 추구하는 경향을 강화하고 있습니다. 이러한 요인으로 인해 제조업체는 컴플라이언스를 충족시키면서 높은 성능과 효율성을 실현하는 배합의 개발과 혁신을 강요하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 연도 | 2026-2035년 |

| 시작 금액 | 235억 달러 |

| 예측 금액 | 418억 달러 |

| CAGR | 5.9% |

에폭시계 접착제 부문은 2025년에 98억 달러 시장 규모를 창출했습니다. 에폭시 구조용 접착제는 우수한 인장 강도와 전단 강도, 내약품성 및 내열성이 높게 평가되고 있습니다. 이러한 특성은 전기자동차 배터리 팩, 항공우주 복합재, 바디 인 화이트 조립 등 중요한 용도에 이상적입니다. 강화 에폭시계 접착제는 보강 및 접합 용도로 널리 채택되고 있어, 고탄성률 시스템은 풍력 발전 용도에 있어서 긴 스팬에서의 반복 하중에 견디는데 공헌하고 있습니다. 아크릴계 구조용 접착제 부문도 다양한 산업 분야에서 채택이 확대되고 있습니다.

열경화형 시스템 부문은 2025년에 97억 달러 시장 규모를 기록해 오븐 소성을 필요로 하는 항공우주용 복합재나 자동차 바디 인 화이트 용도 등 가혹한 가동 환경 하에서 수요가 높아지고 있습니다. 이 시스템은 가교 밀도가 낮고 내구성이 우수하기 때문에 수명이 긴 용도에 적합합니다. 그러나 이액성 상온 경화형 에폭시 수지 및 폴리우레탄(PU)은 유연성, 현장 및 라인 조립의 용이성, 노동 집약적인 설치 작업의 불필요함으로부터 주목을 받고 있습니다. 이러한 시스템은 성능과 편의성의 균형을 제공하며 산업 및 건설 프로젝트에서 점점 더 많이 사용되고 있습니다.

미국 구조용 접착제 시장은 항공우주 분야의 견고함과 자동차 산업에서 전기자동차의 보급 확대로 2025년 50억 달러 규모에 달했습니다. 미국에서 생산 능력이 주도적인 역할을 하는 반면 캐나다는 항공우주 및 건설 용도를 통해 공헌하고 있습니다. 멕시코의 자동차 생산 확대도 지역 시장의 성장을 지원합니다. 변화하는 규제 상황은 저 VOC 및 제로 VOC 화학물질을 촉진하고 구조용 유리 접착 및 특수 접착제 응용 분야에서 기술 혁신을 이끌고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급업체 현황

- 수익률

- 단계별 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 자동차 및 항공우주 분야에서의 경량화

- 증가하는 건설 및 인프라 프로젝트

- 기술적 진보

- 업계의 잠재적 위험 및 과제

- 긴 경화 시간

- 체결 부품(Fasteners) 대비 높은 비용

- 시장 기회

- 전기자동차(EV)의 확대

- 3D 프린팅 및 적층 제조

- 수리 및 보수 용도

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 기술과 혁신 동향

- 현재의 기술 동향

- 신규 기술

- 가격 동향

- 지역별

- 기술 플랫폼별

- 장래 시장 동향

- 특허 상황

- 무역 통계(HS코드)(참고: 무역 통계는 주요 국가에 대해서만 제공됨.)

- 주요 수입국

- 주요 수출국

- 지속가능성과 환경면

- 지속가능한 대처

- 폐기물 감축 전략

- 생산에 있어서의 에너지 효율

- 친환경 이니셔티브

- 탄소발자국 고려

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병 및 인수

- 제휴 및 협업

- 신제품 발매

- 확대 계획

제5장 시장 추정 및 예측 : 기술 플랫폼별, 2022-2035

- 에폭시 접착제

- 폴리우레탄(PU) 접착제

- 아크릴 접착제

- 사이아노아크릴레이트 접착제

- 실리콘 접착제

- 기타 기술

제6장 시장 추정 및 예측 : 경화 메커니즘별, 2022-2035

- 열경화 시스템

- 고온 경화(150°C 초과)

- 중온 경화(120-150°C)

- 저온 경화(70-120°C)

- 상온 경화 시스템

- 습기 경화 시스템

- UV 및 방사선 경화 시스템

- 듀얼 경화 시스템

제7장 시장 추정 및 예측 : 형태별, 2022-2035

- 필름 접착제

- 페이스트형 접착제

- 액상 및 저점도 접착제

제8장 시장 추정 및 예측 : 구성 시스템별, 2022-2035

- 1액(1C) 시스템

- 2액(2C) 시스템

제9장 시장 추정 및 예측 : VOC 함유량별, 2022-2035

- 저 VOC 함유 접착제(50 g/L 미만)

- 무 VOC/용제 프리 접착제

- 수성 접착제

- 바이오 베이스 / 재생 가능 원료 함유율

제10장 시장 추정 및 예측 : 용도별, 2022-2035

- 금속 간 접착

- 복합 재료 접착

- 이종 소재 접착

- 플라스틱 접착

- 목재 및 가공 목재 접착

- 콘크리트 및 조적 접착

- 유리 접착

- 기타

제11장 시장추정 및 예측 : 최종용도산업별, 2022-2035

- 자동차

- 항공 및 우주산업

- 풍력에너지

- 해양 및 조선

- 건설 및 인프라

- 전자 및 전기

- 상하수도

- 기타

제12장 시장추정 및 예측 : 지역별, 2022-2035

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 기타 라틴아메리카

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

제13장 기업 프로파일

- 3M Company

- Arkema SA

- Ashland Global Holdings Inc.

- Bostik(Arkema)

- Cemedine Co., Ltd.

- Dow Inc.

- Dymax Corporation

- Henkel AG & Co. KGaA

- HB Fuller Company

- Huntsman Corporation

- Kangda New Materials

- Kisling AG

- Master Bond Inc.

- Panacol-Elosol GmbH

- Parson Adhesives

- PPG Industries

- Sika AG

- ThreeBond Holdings Co., Ltd.

- Toagosei Co., Ltd.

- Weiss Chemie Technik GmbH & Co. KG

The Global Structural Adhesive Market was valued at USD 23.5 billion in 2025 and is estimated to grow at a CAGR of 5.9% to reach USD 41.8 billion by 2035.

Structural adhesives are experiencing significant growth as multiple industries, including automotive, aerospace, electronics, marine, wind energy, and construction, increasingly adopt them. These adhesives are gradually replacing welding and mechanical fasteners in applications that require evenly distributed stresses and lightweight assemblies. The surge in electric vehicle production and the integration of composite materials in aircraft have accelerated this transition. Additionally, regulatory frameworks are steering the market toward environmentally friendly chemistries, such as water-based, low-VOC, and zero-VOC formulations, aligning with sustainability and compliance standards. Market growth is driven by large-scale vehicle production, creating high demand for structural adhesives in body-in-white, glazing, and battery assembly, alongside stringent environmental regulations encouraging solvent-free and low-emission alternatives. These factors compel manufacturers to innovate and develop formulations that meet compliance while delivering high performance and efficiency.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $23.5 Billion |

| Forecast Value | $41.8 Billion |

| CAGR | 5.9% |

The epoxy-based adhesives segment generated USD 9.8 billion in 2025. Epoxy structural adhesives are highly valued for their exceptional tensile and shear strength, as well as chemical and thermal resistance. These properties make them ideal for critical applications, including electric vehicle battery packs, aerospace composites, and body-in-white assemblies. Toughened epoxy adhesives are widely used for reinforcement and bonding applications, while high-modulus systems in wind energy applications help withstand cyclic loads across long spans. The acrylic structural adhesives segment is also witnessing growing adoption across various industries.

The heat-curing systems segment was valued at USD 9.7 billion in 2025 and is seeing rising demand in challenging operating environments, such as aerospace composites and automotive body-in-white applications that require oven baking. These systems offer lower cross-link density and high durability, making them suitable for long-lasting applications. However, two-component, room-temperature curing epoxies and polyurethanes (PUs) are gaining traction due to their flexibility, ease of field and line assembly, and elimination of labor-intensive installations. These systems are increasingly used in industrial and construction projects, providing a balance between performance and convenience.

U.S. Structural Adhesive Market reached USD 5 billion in 2025, owing to a strong aerospace sector and growing adoption of electric vehicles in the automotive industry. Manufacturing capabilities in the U.S. play a leading role, while Canada contributes through aerospace and construction applications. Mexico's growing automotive production also supports regional market expansion. The evolving regulatory landscape promotes low and zero-VOC chemistries, driving innovation in structural glazing and specialty adhesive applications.

Key players in the Global Structural Adhesive Market include 3M, Arkema S.A., Ashland Global Holdings Inc., Dow Inc., Bostik (Arkema), Dymax Corporation, Henkel AG & Co. KGaA, H.B. Fuller Company, Huntsman Corporation, Kangda New Materials, Kisling AG, Master Bond Inc., Panacol-Elosol GmbH, Parson Adhesives, PPG Industries, Sika AG, ThreeBond Holdings Co., Ltd., Toagosei Co., Ltd., and Weiss Chemie + Technik GmbH & Co. KG. Companies in the Global Structural Adhesive Market are implementing several strategies to strengthen their market presence and enhance competitiveness. Investments in research and development focus on creating high-performance, environmentally friendly formulations, including low- and zero-VOC adhesives. Strategic partnerships with automotive, aerospace, and electronics manufacturers facilitate product integration into large-scale production. Firms are expanding regional manufacturing capacities to serve emerging markets and enhance supply chain resilience. Emphasis on sustainability, regulatory compliance, and innovative product design helps companies differentiate their offerings.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Technology platform

- 2.2.2 Curing mechanism

- 2.2.3 Form

- 2.2.4 Component system

- 2.2.5 VOC content

- 2.2.6 Application

- 2.2.7 End use industry

- 2.2.8 Regional

- 2.3 TAM Analysis, 2025-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Lightweighting in automotive & aerospace

- 3.2.1.2 Rising construction & infrastructure projects

- 3.2.1.3 Technological advancements

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Long curing times

- 3.2.2.2 High cost compared to fasteners

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion in electric vehicles (EVS)

- 3.2.3.2 3D printing & additive manufacturing

- 3.2.3.3 Repair & maintenance applications

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By technology platform

- 3.9 Future market trends

- 3.10 Patent landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Technology Platform, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Epoxy-based adhesives

- 5.3 Polyurethane (PU) adhesives

- 5.4 Acrylic adhesives

- 5.5 Cyanoacrylate adhesives

- 5.6 Silicone adhesives

- 5.7 Other technologies

Chapter 6 Market Estimates and Forecast, By Curing Mechanism, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Heat-curing systems

- 6.2.1 High-temperature cure (>150°C)

- 6.2.2 Medium-temperature cure (120-150°C)

- 6.2.3 Low-temperature cure (70-120°C)

- 6.3 Room-temperature curing systems

- 6.4 Moisture-curing systems

- 6.5 UV & radiation-curing systems

- 6.6 Dual-cure systems

Chapter 7 Market Estimates and Forecast, By Form, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Film adhesives

- 7.3 Paste adhesives

- 7.4 Liquid & low-viscosity adhesives

Chapter 8 Market Estimates and Forecast, By Component System, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Single-component (1C) systems

- 8.3 Two-component (2C) systems

Chapter 9 Market Estimates and Forecast, By VOC Content, 2022-2035 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 Low-VOC adhesives (<50 g/L)

- 9.3 Zero-VOC/solvent-free adhesives

- 9.4 Water-based adhesives

- 9.5 Bio-based/renewable content

Chapter 10 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion) (Kilo Tons)

- 10.1 Key trends

- 10.2 Metal-to-metal bonding

- 10.3 Composite bonding

- 10.4 Mixed-material bonding

- 10.5 Plastic bonding

- 10.6 Wood & engineered wood bonding

- 10.7 Concrete & masonry bonding

- 10.8 Glass bonding

- 10.9 Others

Chapter 11 Market Estimates and Forecast, By End Use Industry, 2022-2035 (USD Billion) (Kilo Tons)

- 11.1 Key trends

- 11.2 Automotive

- 11.3 Aviation & aerospace

- 11.4 Wind energy

- 11.5 Marine & shipbuilding

- 11.6 Construction & infrastructure

- 11.7 Electronics & electrical

- 11.8 Water & wastewater

- 11.9 Others

Chapter 12 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 12.1 Key trends

- 12.2 North America

- 12.2.1 U.S.

- 12.2.2 Canada

- 12.2.3 Mexico

- 12.3 Europe

- 12.3.1 Germany

- 12.3.2 UK

- 12.3.3 France

- 12.3.4 Spain

- 12.3.5 Italy

- 12.3.6 Rest of Europe

- 12.4 Asia Pacific

- 12.4.1 China

- 12.4.2 India

- 12.4.3 Japan

- 12.4.4 Australia

- 12.4.5 South Korea

- 12.4.6 Rest of Asia Pacific

- 12.5 Latin America

- 12.5.1 Brazil

- 12.5.2 Mexico

- 12.5.3 Argentina

- 12.5.4 Rest of Latin America

- 12.6 Middle East and Africa

- 12.6.1 Saudi Arabia

- 12.6.2 South Africa

- 12.6.3 UAE

- 12.6.4 Rest of Middle East and Africa

Chapter 13 Company Profiles

- 13.1 3M Company

- 13.2 Arkema S.A.

- 13.3 Ashland Global Holdings Inc.

- 13.4 Bostik (Arkema)

- 13.5 Cemedine Co., Ltd.

- 13.6 Dow Inc.

- 13.7 Dymax Corporation

- 13.8 Henkel AG & Co. KGaA

- 13.9 H.B. Fuller Company

- 13.10 Huntsman Corporation

- 13.11 Kangda New Materials

- 13.12 Kisling AG

- 13.13 Master Bond Inc.

- 13.14 Panacol-Elosol GmbH

- 13.15 Parson Adhesives

- 13.16 PPG Industries

- 13.17 Sika AG

- 13.18 ThreeBond Holdings Co., Ltd.

- 13.19 Toagosei Co., Ltd.

- 13.20 Weiss Chemie + Technik GmbH & Co. KG