|

시장보고서

상품코드

1913389

배양육 시장 : 기회, 성장 요인, 산업 동향 분석 및 예측(2026-2035년)Cultured Meat Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

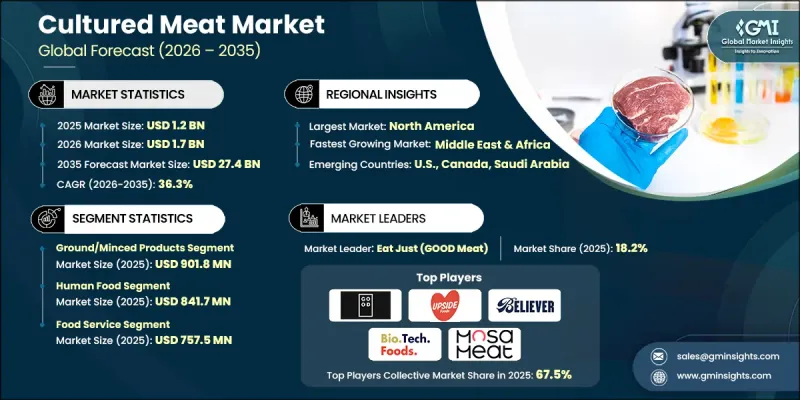

세계의 배양육 시장은 2025년 12억 달러로 평가되었으며, 2035년까지 연평균 복합 성장률(CAGR) 36.3%로 성장해 274억 달러에 이를 것으로 예측되고 있습니다.

배양육 바이오리액터는 배양육 산업의 핵심을 이루고 도축을 필요로 하지 않는 실험실 배양육 생산을 위한 확장 가능한 솔루션을 제공합니다. 이 생물반응기는 동물 세포 배양을 위한 정밀한 환경을 창조하고 통제된 성장, 영양 공급 및 스트레스 관리를 가능하게 합니다. 교반기형, 관류형, 에어리프트형, 중공사형 바이오리액터 등 다양한 시스템이 확장성과 세포 유지에 독특한 이점을 제공합니다. 바이오리액터 설계, 배양 배지 최적화, 스케일업 기술의 최근 혁신으로 비용 효율성을 높여 대량 생산을 더욱 실현할 수 있게 되었습니다. 기술의 진보는 시간이 지남에 따라 생산 비용을 낮추고 저렴한 가격과 가용성을 높일 것으로 예측됩니다. 배양육의 식감, 풍미, 품질의 향상도 소비자의 채용을 촉진해, 시장 확대를 뒷받침할 것입니다. 윤리적, 환경적, 지속가능성에 대한 우려 증가와 고기 대체품에 대한 수요 증가는 이 시장을 추진하는 주요 요인입니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 시작 규모 | 12억 달러 |

| 시장 규모 예측 | 274억 달러 |

| CAGR | 36.3% |

지속가능성은 배양육 생물 반응기 시장의 주요 촉진 요인입니다. 실험실에서 배양된 고기는 전통적인 고기 생산을 대체하는 환경 친화적이고 윤리적인 선택을 제공하며 변화하는 소비자의 선호도를 따릅니다. 그러나 높은 초기 자본과 운영 비용이 과제가 되고 있으며, 특히 스타트업 기업이나 신흥 기업에 있어서는 강한 시장 잠재력이 있음에도 불구하고, 상업화의 대처를 늦추고 있습니다.

2025년에는 다짐육 제품이 9억 180만 달러로 큰 점유율을 차지했습니다. 이러한 배양육 제품은 성형육 제품에 비해 제조 공정이 간단하고 생산 규모를 보다 신속하게 확대할 수 있기 때문에 시장을 선도하고 있습니다. 조직 형성이 용이하기 때문에 제조업체는 식감이나 감각적 품질을 손상시키지 않고, 보다 소형 바이오리액터로 조업하는 것이 가능합니다. 게다가 햄버거, 미트볼, 만두, 너겟 등 인기있는 용도에 대한 범용성이 높기 때문에 소비자의 수용이 진행되고 있습니다. 이러한 호환성을 통해 생산자는 예측 가능한 수요 패턴을 유지하면서 초기 가격의 높이를 흡수할 수 있는 대량 소비 부문을 타겟팅할 수 있습니다.

2025년 인간 식품 부문은 8억 4,170만 달러 시장 규모를 창출했습니다. 인간의 소비에 초점을 맞추는 것은 배양육 산업의 큰 원동력이 되고 있으며, 각 회사는 주류 식습관과 상업 푸드서비스 수요에 따라 제품을 우선하고 있습니다. 시식회, 초기 규제 승인, 제한적인 소매 전개는 주로 인간을 위한 소비를 목적으로 하며, 기업은 맛, 식감, 안전성을 보다 광범위한 규모로 검증할 수 있습니다. 이 접근법은 지속가능성과 윤리적 단백질 동향과도 일치하며 배양육가 기존의 동물 제품을 대체하는 현실적인 선택으로 확립되는 데 도움이 됩니다.

북미의 배양육 시장은 2025년에 38%의 점유율을 차지했고 미국이 주도적 입장에 있습니다. 이것은 세포 농업 스타트업의 강력한 생태계, 광범위한 벤처 캐피탈 지원, FDA 및 USDA에 의한 초기 단계의 규제 대응이 배경에 있습니다. 이 지역의 성장은 대규모 생산 시설에 대한 많은 투자, 주요 제조업체의 상업 플랜트의 지속적인 개발, 외식 산업 채널에서의 파일럿 프로젝트의 지속으로 지원되며, 이들은 소비자의 수용도와 광범위한 보급에 대한 준비 태세를 확인하는 데 도움이 됩니다.

자주 묻는 질문

목차

제1장 분석 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 업계의 생태계 분석

- 공급자의 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 요인

- 동물 유래 제품의 대체품 수요 증가

- 온라인 식품 배달 채널의 급속한 진화

- 기술의 성숙화와 비용 절감

- 업계의 잠재적 위험과 과제

- 엄격한 규제 환경과 승인 스케줄

- 고액의 설비 투자와 초기 비용

- 시장 기회

- 동물 유래 성분을 포함하지 않는 배지의 상업화

- 하이브리드 제품 개발

- 성장 요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 가격 동향

- 지역별

- 제품

- 미래 시장 동향

- 기술과 혁신 동향

- 현재의 기술 동향

- 신흥기술

- 특허 상황

- 무역 통계(HS코드)(참고 : 무역 통계는 주요 국가에서만 제공됨)

- 주요 수입국

- 주요 수출국

- 지속가능성과 환경면

- 지속가능한 대처

- 폐기물 감축 전략

- 생산에서의 에너지 효율

- 환경에 배려한 대처

- 탄소발자국에 관한 고려 사항

제4장 경쟁 구도

- 소개

- 기업별 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 동향

- 기업 인수합병(M&A)

- 사업 제휴 및 협력

- 신제품 발매

- 확대 계획

제5장 시장의 추정 및 예측 : 제품 유형별(2022-2035년)

- 다짐육 제품

- 햄버거

- 미트볼

- 소시지

- 다짐육

- 성형제품

- 너겟

- 스트립 및 텐더

- 덩어리

- 기타

제6장 시장의 추정 및 예측 : 용도별(2022-2035년)

- 인간용 식품

- 반려동물 식품

- 개

- 고양이

- 이색 반려동물

- 연구개발(R&D)

- 학술 연구

- 제품 개발

- 규제 시험

- 기타

제7장 시장의 추정 및 예측 : 유통 채널별(2022-2035년)

- DTC(소비자용 직접 판매)

- 소매점포

- 슈퍼마켓 및 하이퍼마켓

- 전문점

- 편의점

- 외식산업

- 레스토랑

- 케이터링 서비스

- 시설용 푸드서비스

- B2B

제8장 시장의 추정 및 예측 : 지역별(2022-2035년)

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 기타 라틴아메리카

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

제9장 기업 프로파일

- Mosa Meat

- Upside Foods

- Aleph Farms

- Finless Foods

- Meatable

- Believer Meats(formerly Future Meat Technologies)

- HigherSteaks

- Avant Meats

- BlueNalu

- Eat Just(GOOD Meat)

- BioFood Systems

- Balletic Foods

- Biotech Foods

The Global Cultured Meat Market was valued at USD 1.2 billion in 2025 and is estimated to grow at a CAGR of 36.3% to reach USD 27.4 billion by 2035.

Cultured meat bioreactors are at the heart of the cultivated meat industry, providing scalable solutions for producing lab-grown meat without the need for animal slaughter. These bioreactors create precise environments for animal cell cultivation, enabling controlled growth, nutrient supply, and stress management. Different systems, including stirred-tank, perfusion, airlift, and hollow-fiber bioreactors, offer unique advantages for scalability and cell maintenance. Recent innovations in bioreactor design, culture media optimization, and scale-up techniques have improved cost efficiency, making mass production more feasible. Technological progress is expected to reduce production costs over time, increasing affordability and accessibility. Improved texture, flavor, and quality of cultivated meat will also drive consumer adoption, fueling market expansion. Growing ethical, environmental, and sustainability concerns, coupled with rising demand for meat alternatives, are key factors propelling this market.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.2 Billion |

| Forecast Value | $27.4 Billion |

| CAGR | 36.3% |

Sustainability is a central driver for the cultured meat bioreactors market. Lab-grown meat provides an environmentally friendly and ethical alternative to traditional meat production, aligning with changing consumer preferences. However, high initial capital and operational costs pose challenges, particularly for startups and emerging companies, slowing commercialization efforts despite strong market potential.

Ground and minced products accounted for a substantial share, valued at USD 901.8 million in 2025. These forms of cultured meat are leading the market due to their simpler production process and faster scalability compared with structured cuts. Their ease of tissue formation allows manufacturers to operate smaller bioreactors without compromising texture or sensory quality. Additionally, their versatility for popular applications such as burgers, meatballs, dumplings, and nuggets boosts consumer adoption. This compatibility enables producers to target high-volume segments that can absorb higher initial pricing while supporting predictable demand patterns.

The human food segment generated USD 841.7 million in 2025. The focus on human consumption drives much of the cultured-meat industry, as companies prioritize products aligned with mainstream diets and commercial foodservice demand. Pilot tastings, early regulatory approvals, and limited retail launches primarily target human consumption, allowing firms to validate taste, texture, and safety on a broader scale. This approach also aligns with sustainability and ethical protein trends, helping cultivated meat establish itself as a viable alternative to conventional animal products.

North America Cultured Meat Market captured 38% share in 2025, with the U.S. leading due to a strong ecosystem of cell-agriculture startups, extensive venture capital support, and initial regulatory engagement from the FDA and USDA. The region's growth is supported by substantial investments in large-scale production facilities, ongoing commercial plant developments by major manufacturers, and continued pilot projects in foodservice channels, which help confirm consumer acceptance and readiness for wider adoption.

Key players in the Global Cultured Meat Market include ABEC, Alfa Laval, Bioengineering AG, Eppendorf AG, Esco Lifesciences Group, GEA, Infors HT, INNOVA Bio-meditech, KBiotech GmbH, Merck KGaA, OLLITAL Technology, Pall Corporation, Sartorius AG, Solaris Biotech, and Vogtlin Instruments GmbH. Companies in the Global Cultured Meat Market are strengthening their foothold through strategic R&D investments to enhance bioreactor efficiency, scalability, and automation. Collaborations with research institutions and startups help accelerate technology development and optimize culture conditions. Expanding manufacturing capacities, developing cost-effective culture media, and offering turnkey solutions for pilot and commercial-scale production enhance market presence. Firms are also diversifying product portfolios to address specific applications in cellular agriculture and cultivated meat production. Regulatory engagement, participation in industry consortia, and sustainability initiatives further reinforce credibility and position companies as leaders in this emerging market.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product Type

- 2.2.3 Application

- 2.2.4 Distribution Channel

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing demand for animal-based product alternatives

- 3.2.1.2 Rapid evolution of online food delivery channels

- 3.2.1.3 Technology maturation & cost reduction

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Stringent regulatory environment & approval timelines

- 3.2.2.2 High capital expenditure & setup costs

- 3.2.3 Market opportunities

- 3.2.3.1 Animal-free media commercialization

- 3.2.3.2 hybrid product development

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 Product

- 3.8 Future market trends

- 3.9 Technology and Innovation Landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022 - 2035 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Ground/minced products

- 5.2.1 Burgers

- 5.2.2 Meatballs

- 5.2.3 Sausages

- 5.2.4 Ground meat

- 5.3 Structured products

- 5.3.1 Nuggets

- 5.3.2 Strips/tenders

- 5.3.3 Whole cuts

- 5.4 Others

Chapter 6 Market Estimates and Forecast, By Application, 2022 - 2035 (USD million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Human food

- 6.3 Pet food

- 6.3.1 Dog food

- 6.3.2 Cat food

- 6.3.3 Exotic pet food

- 6.4 Research & development

- 6.4.1 Academic research

- 6.4.2 Product development

- 6.4.3 Regulatory testing

- 6.5 Others

Chapter 7 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 (USD million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Direct-to-Consumer (DTC)

- 7.3 Retail Stores

- 7.3.1 Supermarkets & hypermarkets

- 7.3.2 Specialty stores

- 7.3.3 Convenience stores

- 7.4 Food Service

- 7.4.1 Restaurants

- 7.4.2 Catering Services

- 7.4.3 Institutional Food Service

- 7.5 B2B

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 (USD million) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Mosa Meat

- 9.2 Upside Foods

- 9.3 Aleph Farms

- 9.4 Finless Foods

- 9.5 Meatable

- 9.6 Believer Meats (formerly Future Meat Technologies)

- 9.7 HigherSteaks

- 9.8 Avant Meats

- 9.9 BlueNalu

- 9.10 Eat Just (GOOD Meat)

- 9.11 BioFood Systems

- 9.12 Balletic Foods

- 9.13 Biotech Foods