|

시장보고서

상품코드

1913393

자동차용 나이트 비전 시스템 시장 : 기회, 성장 요인, 산업 동향 분석 및 예측(2026-2035년)Automotive Night Vision System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

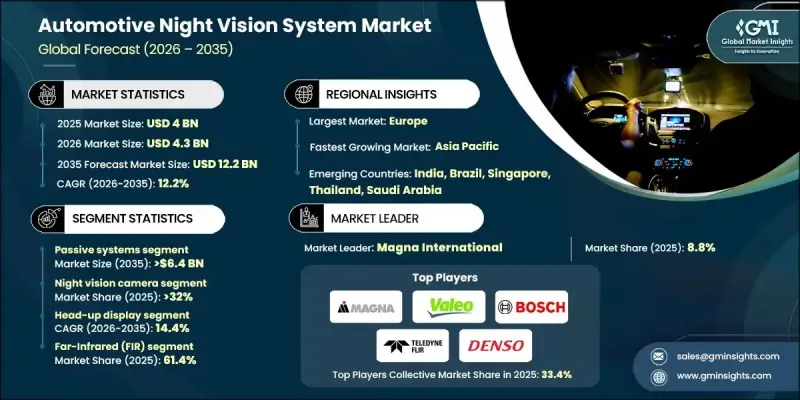

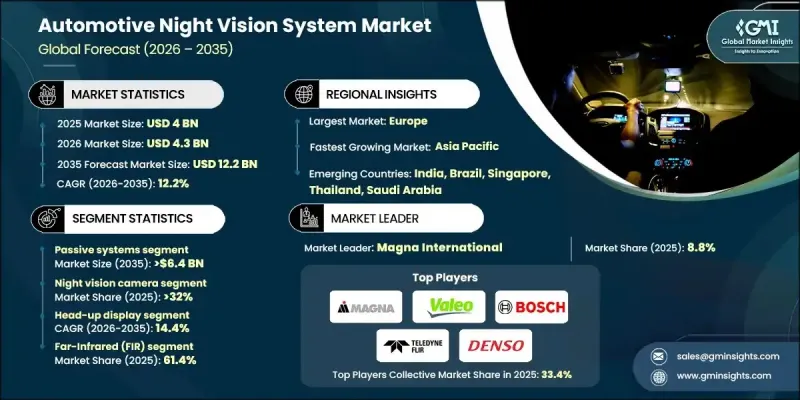

세계의 자동차용 나이트 비전 시스템 시장은 2025년 40억 달러로 평가되었으며, 2035년까지 연평균 복합 성장률(CAGR) 12.2%로 성장하여 122억 달러에 이를 것으로 예측됩니다.

시장 확대의 배경으로 사고 예방에 대한 관심 증가와 현대 차량의 지능형 안전 기술의 통합이 진행되고 있습니다. 전기자동차 및 자율주행차 플랫폼의 진보는 도입을 더욱 가속화하고 있으며, 나이트 비전 시스템은 광범위한 안전 아키텍처를 보완하는 역할을 하고 있습니다. 저조도 운전 환경에서의 시인성 과제에 대한 인식 증가가 고급차와 중가격대 차량 모두에서 수요를 강화하고 있습니다. 첨단 안전 기술에 대한 규제적 장려책은 제조업체가 종합적인 운전 지원 시스템에 나이트 비전 기능을 통합하는 형태로 간접적으로 보급을 뒷받침하고 있습니다. 적외선 센싱 기술, 열화상 정밀도 향상, 실시간 데이터 처리의 진전이 지속적으로 진행되어 신뢰성과 실용성이 향상되고 있기 때문에 이러한 시스템은 순정 장비로서의 통합에 있어서 점점 매력적이 되고 있습니다. 이러한 요인들이 결합되어 나이트 비전 시스템은 차세대 자동차 안전 전략에서 중요한 구성 요소로서의 지위를 확립하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 시작 규모 | 40억 달러 |

| 시장 규모 예측 | 122억 달러 |

| CAGR | 12.2% |

패시브 나이트 비전 시스템 부문은 2025년에 46%의 점유율을 차지했으며, 2035년까지 64억 달러에 도달할 것으로 예측됩니다. 이 부문은 외부 광원에 의존하지 않고 열 패턴을 검출할 수 있는 능력, 시인성이 낮은 환경에서도 안정된 성능을 발휘하는 점, 안전성을 중시한 차량 용도를 지원하는 점에서 계속 주도적인 지위를 유지하고 있습니다.

나이트 비전 카메라 부문은 2025년에 32%의 점유율을 차지했으며 추정 시장 규모는 13억 달러였습니다. 영상의 선명도, 검출 정밀도, 시스템 내구성의 지속적인 개선에 의해 폭넓은 운전 조건하에서 성능 신뢰성이 향상해, 자동차 제조업체에 의한 채용 확대를 지지하고 있습니다.

미국의 자동차용 나이트 비전 시스템 시장은 2025년 7억 6,100만 달러에 이르렀으며, 2026년부터 2035년까지 강력한 성장이 예상됩니다. 미국 시장의 기세는 첨단 안전 기능에 대한 소비자의 선호와 고부가가치 차종 카테고리에서의 지능화 차량 기술의 보급 확대에 의해 지원되고 있습니다.

자주 묻는 질문

목차

제1장 분석 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 업계의 생태계 분석

- 공급자의 상황

- 이익률 분석

- 비용 구조

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 요인

- 도로 안전과 사고 감축에 대한 관심 증가

- ADAS(첨단 운전자 보조 시스템)에 대한 규제지원 강화

- 적외선 센서 및 처리 기술의 진보

- 자동차의 프리미엄 안전 기능에 대한 수요 증가

- 디지털 조종석 및 헤드업 디스플레이 확대

- 업계의 잠재적 위험과 과제

- 나이트 비전 시스템 부품의 고비용

- 시스템 통합 및 조정의 복잡성

- 시장 기회

- 중급 승용차에 보급

- 자동운전 및 준자동운전 시스템과 통합

- 전기차 및 소프트웨어 정의 차량의 성장

- 신흥 자동차 시장 수요 증가

- 성장 요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 미국 - FMVSS(연방 자동차 안전 기준)

- 캐나다 - CMVSS

- 유럽

- 영국 - UNECE 자동차 규제

- 독일 - ISO 26262 기능안전

- 프랑스 - UNECE R152

- 이탈리아 - ISO 14001 환경 경영 시스템

- 스페인 - ISO 9001 품질 경영 시스템

- 아시아태평양

- 중국 - GB 자동차 규격

- 일본 - ISO 26262 기능안전

- 인도 - AIS 자동차 규격

- 라틴아메리카

- 브라질 - CONTRAN 자동차 규제

- 멕시코 - NOM 자동차 규격

- 아르헨티나 - ISO 14001 환경 경영 시스템

- 중동 및 아프리카

- 아랍에미리트(UAE) - UNECE(유엔 유럽 경제위원회) 차량 규제

- 남아프리카 - ISO 26262 기능안전

- 사우디아라비아 - SASO 자동차 규격

- 북미

- Porter's Five Forces 분석

- PESTEL 분석

- 기술과 혁신 동향

- 현재의 기술 동향

- 신흥기술

- 비용 내역 분석

- 개발 비용 구조

- R&D 비용 분석

- 마케팅 및 판매 비용

- 특허 분석

- 지속가능성과 환경면

- 지속가능한 실천

- 폐기물 감축 전략

- 생산에서의 에너지 효율

- 환경에 배려한 대처

- 미래 시장 전망과 기회

- OEM 및 Tier 1 공급업체의 조달 및 채용 기준

- 나이트 비전 채택에서 OEM의 의사 결정 요인

- 비용 대 안전 가치 평가

- 지역별 OEM 채용의 차이

- Tier 1 공급자 선정 기준

- ADAS 스택 통합 및 시스템 아키텍처의 역할

- 성능, 정밀도, 오감지의 트레이드 오프

- 책임, 안전성 검증 및 규제 리스크

제4장 경쟁 구도

- 소개

- 기업별 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 주요 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

- 주요 동향

- 기업 인수합병(M&A)

- 사업 제휴 및 협력

- 신제품 발매

- 사업 확대 계획과 자금 조달

제5장 시장의 추정 및 예측 : 제품별(2022-2035년)

- 액티브 시스템

- 패시브 시스템

- 교정 및 정렬 시스템

- 기타

제6장 시장의 추정 및 예측 : 컴포넌트별(2022-2035년)

- 나이트 비전 카메라

- 적외선 센서

- 영상 처리 및 제어 유닛

- 디스플레이 모듈

- 조명 유닛

- 소프트웨어 알고리즘

제7장 시장의 추정 및 예측 : 디스플레이별(2022-2035년)

- 헤드업 디스플레이(HUD)

- 계기 클러스터

- 네비게이션 디스플레이

- 복합 디스플레이 시스템

제8장 시장의 추정 및 예측 : 기술별(2022-2035년)

- 원적외선(FIR)

- 근적외선(NIR)

제9장 시장의 추정 및 예측 : 차량별(2022-2035년)

- 승용차

- 세단

- SUV

- 해치백

- 상용차

- 소형 상용차(LCV)

- 중형 상용차(MCV)

- 대형 상용차(HCV)

제10장 시장의 추정 및 예측 : 용도별(2022-2035년)

- 보행자 감지

- 동물 감지

- 장애물 및 물체 감지

- 충돌 경보 및 회피 시스템

- 운전자 지원 및 시인성 향상

제11장 시장의 추정 및 예측 : 판매 채널별(2022-2035년)

- OEM

- 애프터마켓

제12장 시장의 추정 및 예측 : 지역별(2022-2035년)

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 북유럽 국가

- 포르투갈

- 크로아티아

- 베네룩스 국가

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 싱가포르

- 태국

- 인도네시아

- 베트남

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 콜롬비아

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

제13장 기업 프로파일

- 국제적 기업

- Bosch

- Continental

- Magna International

- Valeo

- DENSO

- ZF Friedrichshafen

- Teledyne FLIR

- Autoliv

- Veoneer

- Panasonic

- 지역 기업

- Hella

- Gentex

- Harman International

- Visteon

- Hitachi Astemo

- Mobileye

- Ficosa International

- Hyundai Mobis

- Mitsubishi Electric

- Aptiv

- 신흥/디스럽터 기업

- Omnivision Technologies

- Infineon Technologies

- Omron

- Texas Instruments

- Luminar Technologies

- Hikvision Automotive

- Raytron Technology

The Global Automotive Night Vision System Market was valued at USD 4 billion in 2025 and is estimated to grow at a CAGR of 12.2% to reach USD 12.2 billion by 2035.

Market expansion is driven by increasing focus on accident prevention, along with the growing integration of intelligent safety technologies in modern vehicles. Advancements in electric and autonomous vehicle platforms are further accelerating adoption, as night vision systems complement broader safety architectures. Heightened awareness of visibility challenges during low-light driving conditions has strengthened demand across both premium and mid-priced vehicles. Regulatory encouragement for advanced safety technologies is indirectly reinforcing adoption as manufacturers package night vision capabilities within comprehensive driver assistance offerings. Ongoing progress in infrared sensing, thermal imaging accuracy, and real-time data processing is enhancing reliability and usability, making these systems increasingly attractive for original equipment integration. Together, these factors are establishing night vision systems as a critical component in next-generation automotive safety strategies.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $4 Billion |

| Forecast Value | $12.2 Billion |

| CAGR | 12.2% |

The passive night vision systems segment held 46% share in 2025 and is projected to reach USD 6.4 billion in value by 2035. This segment continues to lead due to its ability to detect heat patterns without relying on external light sources, delivering consistent performance in challenging visibility environments and supporting safety-oriented vehicle applications.

The night vision camera segment represented 32% share in 2025, with an estimated valuation of USD 1.3 billion. Continuous improvements in image clarity, sensing precision, and system durability are enhancing performance reliability across a wide range of driving conditions, supporting broader adoption by vehicle manufacturers.

US Automotive Night Vision System Market reached USD 761 million in 2025 and is expected to show strong growth between 2026 and 2035. Market momentum in the United States is supported by consumer preference for advanced safety features and increasing deployment of intelligent vehicle technologies across higher-value vehicle categories.

Key companies operating in the Global Automotive Night Vision System Market include Bosch, Continental, Valeo, Autoliv, Magna International, DENSO, Harman, Gentex, Teledyne Flir, Omnivision, and Delphi Technologies. Companies active in the automotive night vision system market are reinforcing their market position through continuous innovation, strategic collaborations, and deeper integration with vehicle safety platforms. Leading players are investing in enhanced sensor performance, advanced image processing software, and compact system designs to improve reliability and cost efficiency. Close collaboration with automakers enables early-stage integration into new vehicle architectures. Firms are also expanding production capabilities and focusing on scalable solutions to support broader adoption beyond luxury segments.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast

- 1.8 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Component

- 2.2.4 Display

- 2.2.5 Technology

- 2.2.6 Vehicle

- 2.2.7 Application

- 2.2.8 Sales channel

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook & strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1.1 Growth drivers

- 3.2.1.2 Growing focus on road safety and accident reduction

- 3.2.1.3 Increasing regulatory support for advanced driver assistance systems

- 3.2.1.4 Advancements in infrared sensor and processing technologies

- 3.2.1.5 Rising demand for premium safety features in vehicles

- 3.2.1.6 Expansion of digital cockpits and head-up displays

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of night vision system components

- 3.2.2.2 Complexity of system integration and calibration

- 3.2.3 Market opportunities

- 3.2.3.1 Penetration into mid-range passenger vehicles

- 3.2.3.2 Integration with autonomous and semi-autonomous driving systems

- 3.2.3.3 Growth of electric and software-defined vehicles

- 3.2.3.4 Emerging demand in developing automotive markets

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 U.S. - FMVSS

- 3.4.1.2 Canada - CMVSS

- 3.4.2 Europe

- 3.4.2.1 UK - UNECE Vehicle Regulations

- 3.4.2.2 Germany - ISO 26262 Functional Safety

- 3.4.2.3 France - UNECE R152

- 3.4.2.4 Italy - ISO 14001 Environmental Management Systems

- 3.4.2.5 Spain - ISO 9001 Quality Management Systems

- 3.4.3 Asia Pacific

- 3.4.3.1 China - GB Automotive Standards

- 3.4.3.2 Japan - ISO 26262 Functional Safety

- 3.4.3.3 India - AIS Automotive Standards

- 3.4.4 Latin America

- 3.4.4.1 Brazil - CONTRAN Automotive Regulations

- 3.4.4.2 Mexico - NOM Automotive Standards

- 3.4.4.3 Argentina - ISO 14001 Environmental Management Systems

- 3.4.5 Middle East & Africa

- 3.4.5.1 UAE - UNECE Vehicle Regulations

- 3.4.5.2 South Africa - ISO 26262 Functional Safety

- 3.4.5.3 Saudi Arabia - SASO Automotive Standards

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Cost breakdown analysis

- 3.8.1 Development cost structure

- 3.8.2 R&D cost analysis

- 3.8.3 Marketing & sales costs

- 3.9 Patent analysis

- 3.10 Sustainability and environmental aspects

- 3.10.1 Sustainable practices

- 3.10.2 Waste reduction strategies

- 3.10.3 Energy efficiency in production

- 3.10.4 Eco-friendly Initiatives

- 3.11 Future market outlook & opportunities

- 3.12 OEM & Tier-1 Procurement and Adoption Criteria

- 3.12.1 OEM decision drivers for night vision adoption

- 3.12.2 Cost vs safety value assessment

- 3.12.3 Regional OEM adoption differences

- 3.12.4 Tier-1 supplier selection criteria

- 3.13 ADAS stack integration & system architecture role

- 3.14 Performance, accuracy & false-detection trade-offs

- 3.15 Liability, safety validation & regulatory risk

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast By Product, 2022 - 2035 ($Bn, Units)

- 5.1 Key trends

- 5.2 Active system

- 5.3 Passive system

- 5.4 Calibration and alignment system

- 5.5 Others

Chapter 6 Market Estimates & Forecast, By Component, 2022 - 2035 ($Bn, Units)

- 6.1 Key trends

- 6.2 Night vision camera

- 6.3 Infrared sensors

- 6.4 Image processing and controlling unit

- 6.5 Display module

- 6.6 Illumination unit

- 6.7 Software and algorithms

Chapter 7 Market Estimates & Forecast, By Display, 2022 - 2035 ($Bn, Units)

- 7.1 Key trends

- 7.2 Head-up display

- 7.3 Instrument cluster

- 7.4 Navigation display

- 7.5 Combined Display System

Chapter 8 Market Estimates & Forecast, By Technology, 2022 - 2035 ($Bn, Units)

- 8.1 Key trends

- 8.2 Far-Infrared (FIR)

- 8.3 Near-Infrared (NIR)

Chapter 9 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Bn, Units)

- 9.1 Key trends

- 9.2 Passenger vehicle

- 9.2.1 Sedan

- 9.2.2 SUV

- 9.2.3 Hatchback

- 9.3 Commercial Vehicle

- 9.3.1 LCV

- 9.3.2 MCV

- 9.3.3 HCV

Chapter 10 Market Estimates & Forecast, By Application, 2022 - 2035 ($Bn, Units)

- 10.1 Key trends

- 10.2 Pedestrian detection

- 10.3 Animal detection

- 10.4 Obstacle and object detection

- 10.5 Collision warning and avoidance

- 10.6 Driver assistance and enhanced visibility

Chapter 11 Market Estimates & Forecast, By Sales Channel, 2022 - 2035 ($Bn, Units)

- 11.1 Key trends

- 11.2 OEM

- 11.3 Aftermarket

Chapter 12 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn, Units)

- 12.1 Key trends

- 12.2 North America

- 12.2.1 US

- 12.2.2 Canada

- 12.3 Europe

- 12.3.1 Germany

- 12.3.2 UK

- 12.3.3 France

- 12.3.4 Italy

- 12.3.5 Spain

- 12.3.6 Russia

- 12.3.7 Nordics

- 12.3.8 Portugal

- 12.3.9 Croatia

- 12.3.10 Benelux

- 12.4 Asia Pacific

- 12.4.1 China

- 12.4.2 India

- 12.4.3 Japan

- 12.4.4 Australia

- 12.4.5 South Korea

- 12.4.6 Singapore

- 12.4.7 Thailand

- 12.4.8 Indonesia

- 12.4.9 Vietnam

- 12.5 Latin America

- 12.5.1 Brazil

- 12.5.2 Mexico

- 12.5.3 Argentina

- 12.5.4 Colombia

- 12.6 MEA

- 12.6.1 South Africa

- 12.6.2 Saudi Arabia

- 12.6.3 UAE

- 12.6.4 Turkey

Chapter 13 Company Profiles

- 13.1 Global Players

- 13.1.1 Bosch

- 13.1.2 Continental

- 13.1.3 Magna International

- 13.1.4 Valeo

- 13.1.5 DENSO

- 13.1.6 ZF Friedrichshafen

- 13.1.7 Teledyne FLIR

- 13.1.8 Autoliv

- 13.1.9 Veoneer

- 13.1.10 Panasonic

- 13.2 Regional Players

- 13.2.1 Hella

- 13.2.2 Gentex

- 13.2.3 Harman International

- 13.2.4 Visteon

- 13.2.5 Hitachi Astemo

- 13.2.6 Mobileye

- 13.2.7 Ficosa International

- 13.2.8 Hyundai Mobis

- 13.2.9 Mitsubishi Electric

- 13.2.10 Aptiv

- 13.3 Emerging / Disruptor Players

- 13.3.1 Omnivision Technologies

- 13.3.2 Infineon Technologies

- 13.3.3 Omron

- 13.3.4 Texas Instruments

- 13.3.5 Luminar Technologies

- 13.3.6 Hikvision Automotive

- 13.3.7 Raytron Technology