|

시장보고서

상품코드

1913404

제3자물류(3PL) 시장 : 기회, 성장 요인, 산업 동향 분석 및 예측(2026-2035년)Third-Party Logistics (3PL) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

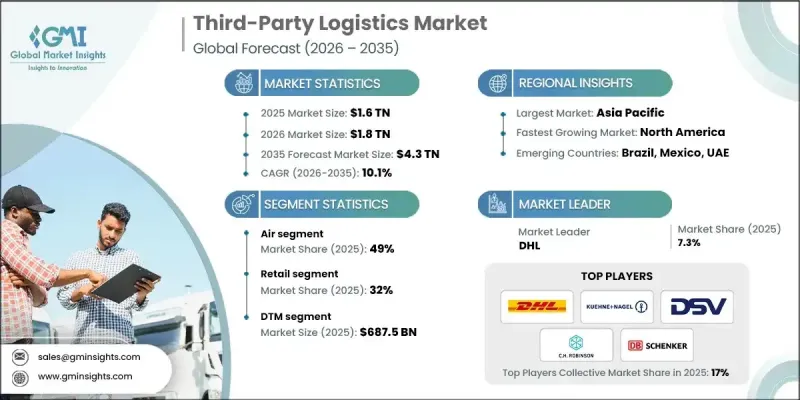

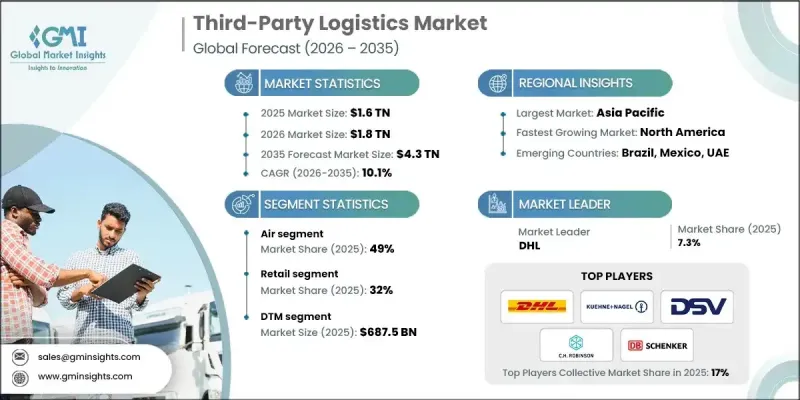

세계의 제3자물류(3PL) 시장은 2025년 1조 6,000억 달러로 평가되었으며, 2035년까지 연평균 복합 성장률(CAGR) 10.1%로 성장하여 4조 3,000억 달러에 이를 것으로 예측됩니다.

이 시장의 성장은 전자상거래의 급속한 확대, 공급망의 세계화 진전, 고객의 신속한 배송에 대한 수요 증가, 물류 및 유통 네트워크의 복잡화에 의해 추진되고 있습니다. 기업은 비용 효율성, 업무 유연성, 실시간 가시성 및 확장성을 갖춘 공급망 운영을 실현하기 위해 전문 3PL 공급자에게 물류 기능의 아웃소싱을 증가시키고 있습니다. 클라우드 기반의 운송 관리 시스템(TMS), 창고 관리 시스템(WMS), AI 및 머신러닝을 활용한 경로 최적화, IoT 대응의 화물 추적, 로보틱스, 창고 자동화, 고도의 데이터 분석 등의 기술 혁신이 기존의 물류를 변혁하고 있습니다. 이러한 솔루션은 재고 정확도를 높이고 운송을 최적화하고 운송 시간을 단축하며 수요 예측을 개선합니다. 옴니채널 소매, 크로스 보더 무역, 라스트 마일 배송 솔루션의 도입 확대는 통합적이고 유연하며 기술 주도형 3PL 서비스에 대한 세계 수요를 더욱 가속화하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 연도 | 2026-2035년 |

| 시작 규모 | 1조 6,000억 달러 |

| 예측 금액 | 4조 3,000억 달러 |

| CAGR | 10.1% |

항공화물 부문은 2025년 49%의 점유율을 차지했으며, 2026년부터 2035년까지 연평균 복합 성장률(CAGR) 11.2%를 보일 것으로 예측됩니다. 항공 물류는 시간 엄수, 고가치 및 긴급 운송을 실현하는데 있어서 필수적인 역할을 담당하고 있기 때문에 주도적인 지위를 차지하고 있습니다. 신속한 배송을 필요로 하는 업계의 강한 수요로 인해 국경을 넘어서는 배송, 저스트 인 타임 재고 관리, 프리미엄 물류 수요에서 항공화물의 채용이 증가하고 있습니다. 고급 화물 취급, 실시간 추적, 우선 배송, 통합 익스프레스 네트워크는 속도, 신뢰성, 서비스 품질을 보장하며, 항공 운송은 긴급하고 긴급 화물에 최적의 솔루션으로 자리를 잡고 있습니다.

국내 운송 관리(DTM) 부문은 2025년 6,875억 달러에 달했습니다. DTM 솔루션은 높은 빈도, 시간 엄수, 비용 효율성이 필요한 국내 운송에서 매우 중요합니다. 최적화된 경로 계획, 운송업체 선정, 화물 추적, 라스트 마일 배송 관리를 제공합니다. 이 기능은 EC, 소매, FMCG 및 제조 공급망에서 신속한 완성, 저스트 인 타임 배송 및 확장 가능한 운영을 실현하는 데 필수적입니다. 효율성과 신뢰성을 추구하는 화물주와 물류 서비스 제공업체 모두에게 DTM은 여전히 중점적 영역입니다.

중국의 제3자물류(3PL) 시장은 2025년 3,749억 달러를 창출해 57%의 점유율을 차지했습니다. 이 지역의 성장은 전자상거래의 확대, 높은 제조 생산량, 기술 주도형 물류 솔루션의 보급 확대에 의해 견인되고 있습니다. AI 기반 루트 최적화, 클라우드 기반 TMS/WMS, 실시간 추적, 자동화 완성 시스템에 대한 투자가 이 지역의 물류 능력을 가속화하고 있습니다. 첨단 인프라, 엄청난 화물량 및 진화하는 규제 기준은 세계 제3자 물류(3PL) 시장에서 아시아태평양의 입지를 더욱 강화하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 비용 구조

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 요인

- 전자상거래와 옴니채널 소매의 급속한 성장

- 공급망 복잡화와 세계 무역의 진전

- 기술 도입과 디지털 전환

- 비용 최적화 및 자산 경량형 비즈니스 모델

- 업계의 잠재적 위험 및 과제

- 상승하는 운영비와 인건비

- 규제 및 컴플라이언스의 복잡성

- 시장 기회

- 라스트 마일 배송 및 부가가치 물류 서비스

- 디지털 및 지속 가능한 물류 솔루션

- AI, 머신러닝, IoT 기술의 채용 상황

- 지속가능성과 녹색 물류 서비스

- 성장 요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 미국 교통부(DOT) 및 연방 자동차 운송 안전국(FMCSA)의 규제

- EPA 배출 기준

- 캐나다 교통부 기준

- 유럽

- 독일 TUV 및 BaFin 준수

- 프랑스 DGCCRF 및 CNIT 가이드라인

- 영국 DVSA 및 FCA 규정

- 이탈리아 교통부 적합성

- 아시아태평양

- 중국공업정보화부(MIIT) 가이드라인

- 일본 금융청 자동차 컴플라이언스

- 한국국토교통성(MOT) 및 금융위원회(FSC)의 규제

- 인도 BIS(인도 규격 협회) 및 자동차 연구 협회 가이드라인

- 라틴아메리카

- 브라질 ANTT 및 DENATRAN 규제

- 멕시코 환경 천연 자원성(SEMARNAT) 및 통신 교통부(SCT) 가이드라인

- 중동 및 아프리카

- 아랍에미리트(UAE) 도로 교통국 가이드라인

- 사우디아라비아 교통 총국(GAT)의 규제

- 북미

- Porter's Five Forces 분석

- PESTEL 분석

- 기술과 혁신 동향

- 현재의 기술 동향

- 자동화 및 로보틱스

- 인공지능(AI) 및 머신러닝

- 사물인터넷(IoT)

- 클라우드 기반 공급망 플랫폼

- 신흥기술

- 하이퍼커넥티드 서플라이 체인

- Robotics-as-a-service(RAAS)

- AI를 활용한 동적 가격 설정과 용량 관리

- 증강현실(AR)과 웨어러블 디바이스

- 현재의 기술 동향

- 가격 동향

- 지역별

- 제품별

- 비용 내역 분석

- 특허 분석

- 지속가능성과 환경적 측면

- 지속가능한 실천

- 폐기물 감축 전략

- 생산에서의 에너지 효율

- 환경에 배려한 대처

- 탄소발자국에 관한 고려 사항

- 이용 사례 시나리오

- 지역별 인프라와 전개 동향

- 운송 및 물류 인프라 평가

- 디지털 및 접속성에 대한 대응 상황

- 항만, 철도 및 복합 수송의 용량 동향

- 스마트 물류 허브 및 프리존

- 수요 및 공급측의 평가

- 공급측 분석

- 공급자의 용량, 인프라 및 능력

- 기술 도입과 운용 효율

- 비용 구조와 수익성

- 수요측 분석

- 최종 사용자 산업의 요건

- 수량, 빈도, 서비스 수준의 기대치

- 가격 감응도와 도입 동향

- 공급측 분석

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

- 주요 발전

- 인수합병

- 제휴 및 협업

- 신제품 발매

- 사업 확대 계획과 자금 조달

제5장 시장 추계 및 예측 : 솔루션별, 2022-2035년

- 전용 계약 운송(DCC)

- 전용 운송 관리(DTM)

- 국제 운송 관리(ITM)

- 창고 보관 및 유통

- 물류 소프트웨어

제6장 시장 추계 및 예측 : 모드별, 2022-2035년

- 항공

- 해상 운송

- 철도 및 도로

제7장 시장 추계 및 예측 : 용도별, 2022-2035년

- 식품 및음료

- 헬스케어

- 소매

- 자동차

- 제조업

- 전자상거래 및 물류

- 화학제품 및 석유화학제품

- 의약품

- 기타

제8장 시장 추계 및 예측 : 지역별, 2022-2035년

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 벨기에

- 네덜란드

- 스웨덴

- 스위스

- 오스트리아

- 노르웨이

- 덴마크

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 싱가포르

- 한국

- 베트남

- 인도네시아

- 말레이시아

- 태국

- 필리핀

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 칠레

- 콜롬비아

- 페루

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 이집트

- 이스라엘

- 카타르

제9장 기업 프로파일

- 글로벌 기업

- CH Robinson Worldwide

- Ceva Logistics

- DB Schenker Logistics

- DHL Supply Chain &Global Forwarding

- DSV A/S

- Expeditors International of Washington

- FedEx Supply Chain

- Kuehne Nagel International AG

- Nippon Express

- XPO Logistics

- 지역 기업

- Agility Logistics

- APL Logistics

- Bollore Logistics

- Geodis

- Hellmann Worldwide Logistics

- Hitachi Transport System

- Kerry Logistics

- Panalpina

- Toll Group

- Yusen Logistics

- 신흥기업

- eBike Diagnostic Solutions

- MotoTech Diagnostics

- NeoMotor Diagnostics

- RideScan Electronics

- SmartMoto Diagnostics

The Global Third-Party Logistics (3PL) Market was valued at USD 1.6 trillion in 2025 and is estimated to grow at a CAGR of 10.1% to reach USD 4.3 trillion by 2035.

The market is propelled by the rapid expansion of e-commerce, increasing globalization of supply chains, rising customer demand for faster deliveries, and the growing complexity of logistics and distribution networks. Businesses are increasingly outsourcing logistics functions to specialized 3PL providers to achieve cost efficiency, operational flexibility, real-time visibility, and scalable supply chain operations. Technological innovations such as cloud-based transportation management systems (TMS), warehouse management systems (WMS), AI- and ML-powered route optimization, IoT-enabled shipment tracking, robotics, warehouse automation, and advanced data analytics are transforming traditional logistics. These solutions enhance inventory accuracy, optimize transportation, reduce transit times, and improve demand forecasting. Rising adoption of omnichannel retail, cross-border trade, and last-mile delivery solutions further accelerates the demand for integrated, flexible, and technology-driven 3PL services globally.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.6 Trillion |

| Forecast Value | $4.3 Trillion |

| CAGR | 10.1% |

The air freight segment held 49% share in 2025 and is anticipated to grow at a CAGR of 11.2% from 2026 to 2035. Air logistics dominates due to its essential role in enabling time-sensitive, high-value, and express shipments. Strong demand from industries requiring rapid delivery has increased the adoption of air freight for cross-border deliveries, just-in-time inventory, and premium logistics needs. Advanced cargo handling, real-time tracking, priority shipping, and integrated express networks ensure speed, reliability, and service quality, positioning air transport as the preferred solution for urgent and high-value goods.

The domestic transportation management (DTM) segment reached USD 687.5 billion in 2025. DTM solutions are crucial for handling high-frequency, time-sensitive, and cost-efficient domestic shipments. They provide optimized route planning, carrier selection, shipment tracking, and last-mile delivery management. This functionality is critical for e-commerce, retail, FMCG, and manufacturing supply chains, enabling rapid fulfillment, just-in-time delivery, and scalable operations. DTM remains a key focus area for both shippers and logistics service providers seeking efficiency and reliability.

China Third-Party Logistics (3PL) Market held a 57% share, generating USD 374.9 billion in 2025. The region's growth is driven by the expansion of e-commerce, high manufacturing output, and increasing adoption of technology-driven logistics solutions. Investments in AI-based route optimization, cloud-based TMS/WMS, real-time tracking, and automated fulfillment systems are accelerating the region's logistics capabilities. Advanced infrastructure, large freight volumes, and evolving regulatory standards further strengthen Asia-Pacific's position in the Global Third-Party Logistics (3PL) Market.

Key players operating in the Global Third-Party Logistics (3PL) Market include DB Schenker Logistics, DHL, DSV A/S (UTi Worldwide, Inc.), C.H. Robinson Worldwide, Expeditors International of Washington, Ceva Logistics, Nippon Express, Kuehne + Nagel International AG, XPO Logistics, and SinoTrans (HK) Logistics Limited. Companies in the Global Third-Party Logistics (3PL) Market strengthen their presence through technology adoption, investing heavily in AI- and ML-powered logistics platforms, cloud-based TMS/WMS, IoT-enabled real-time tracking, and warehouse automation to enhance efficiency. Strategic partnerships with e-commerce firms, retailers, and manufacturers expand service reach. Firms focus on offering integrated end-to-end logistics solutions, optimizing last-mile delivery, and providing scalable operations to meet diverse client needs.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Solution

- 2.2.3 Mode

- 2.2.4 Application

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rapid Growth of E-commerce & Omnichannel Retail

- 3.2.1.2 Rising Supply Chain Complexity & Global Trade

- 3.2.1.3 Technology Adoption & Digital Transformation

- 3.2.1.4 Cost Optimization & Asset-Light Business Models

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Rising Operational & Labor Costs

- 3.2.2.2 Regulatory & Compliance Complexity

- 3.2.3 Market opportunities

- 3.2.3.1 Last-Mile Delivery & Value-Added Logistics Services

- 3.2.3.2 Digital & Sustainable Logistics Solutions

- 3.2.3.3 Adoption of AI, ML, and IoT Technologies

- 3.2.3.4 Sustainability and Green Logistics Services

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 U.S. DOT & FMCSA Regulations

- 3.4.1.2 EPA Emission Standards

- 3.4.1.3 Transport Canada Standards

- 3.4.2 Europe

- 3.4.2.1 Germany TUV & BaFin Compliance

- 3.4.2.2 France DGCCRF & CNIT Guidelines

- 3.4.2.3 United Kingdom DVSA & FCA Regulations

- 3.4.2.4 Italy Ministry of Infrastructure & Transport Compliance

- 3.4.3 Asia Pacific

- 3.4.3.1 China MIIT Guidelines

- 3.4.3.2 Japan FSA Automotive Compliance

- 3.4.3.3 South Korea MOT & FSC Regulations

- 3.4.3.4 India BIS & Automotive Research Association Guidelines

- 3.4.4 Latin America

- 3.4.4.1 Brazil ANTT & DENATRAN Regulations

- 3.4.4.2 Mexico SEMARNAT & SCT Guidelines

- 3.4.5 Middle East and Africa

- 3.4.5.1 UAE Roads & Transport Authority Guidelines

- 3.4.5.2 Saudi Arabia General Authority for Transport (GAT) Regulations

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation Landscape

- 3.7.1 Current technological trends

- 3.7.1.1 Automation & robotics

- 3.7.1.2 Ai & machine learning

- 3.7.1.3 Internet of things (IOT)

- 3.7.1.4 Cloud-based supply chain platforms

- 3.7.2 Emerging technologies

- 3.7.2.1 Hyper-connected supply chains

- 3.7.2.2 Robotics-as-a-service (RAAS)

- 3.7.2.3 AI-driven dynamic pricing & capacity management

- 3.7.2.4 Augmented reality (AR) & wearables

- 3.7.1 Current technological trends

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Cost breakdown analysis

- 3.10 Patent analysis

- 3.11 Sustainability and Environmental Aspects

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly initiatives

- 3.11.5 Carbon footprint considerations

- 3.12 Use case scenarios

- 3.13 Regional Infrastructure & Deployment Trends

- 3.13.1 Transportation & logistics infrastructure scoring

- 3.13.2 Digital & connectivity readiness

- 3.13.3 Port, rail & intermodal capacity trends

- 3.13.4 Smart logistics hubs & free zones

- 3.14 Demand and Supply-Side Assessment

- 3.14.1 Supply-Side Analysis

- 3.14.1.1 Provider capacity, infrastructure, and capabilities

- 3.14.1.2 Technology adoption & operational efficiency

- 3.14.1.3 Cost structures and profitability

- 3.14.2 Demand-Side Analysis

- 3.14.2.1 End-user industry requirements

- 3.14.2.2 Volume, frequency, and service-level expectations

- 3.14.2.3 Pricing sensitivity and adoption trends

- 3.14.1 Supply-Side Analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Solution, 2022 - 2035 ($ Bn)

- 5.1 Key trends

- 5.2 Dedicated contract carriage (DCC)

- 5.3 Dedicated transportation management (DTM)

- 5.4 International transportation management (ITM)

- 5.5 Warehousing & distribution

- 5.6 Logistics software

Chapter 6 Market Estimates & Forecast, By Mode, 2022 - 2035 ($ Bn)

- 6.1 Key trends

- 6.2 Air

- 6.3 Sea

- 6.4 Rail & Road

Chapter 7 Market Estimates & Forecast, By Application, 2022 - 2035 ($ Bn)

- 7.1 Key trends

- 7.2 Food & beverages

- 7.3 Healthcare

- 7.4 Retail

- 7.5 Automotive

- 7.6 Manufacturing

- 7.7 E-commerce & Logistics

- 7.8 Chemicals & Petrochemicals

- 7.9 Pharmaceuticals

- 7.10 Others

Chapter 8 Market Estimates & Forecast, By Region, 2022 - 2035 ($ Bn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 US

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Belgium

- 8.3.7 Netherlands

- 8.3.8 Sweden

- 8.3.9 Switzerland

- 8.3.10 Austria

- 8.3.11 Norway

- 8.3.12 Denmark

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 Singapore

- 8.4.6 South Korea

- 8.4.7 Vietnam

- 8.4.8 Indonesia

- 8.4.9 Malaysia

- 8.4.10 Thailand

- 8.4.11 Philippines

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Chile

- 8.5.5 Colombia

- 8.5.6 Peru

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

- 8.6.4 Egypt

- 8.6.5 Israel

- 8.6.6 Qatar

Chapter 9 Company Profiles

- 9.1 Global Player

- 9.1.1 C.H. Robinson Worldwide

- 9.1.2 Ceva Logistics

- 9.1.3 DB Schenker Logistics

- 9.1.4 DHL Supply Chain & Global Forwarding

- 9.1.5 DSV A/S

- 9.1.6 Expeditors International of Washington

- 9.1.7 FedEx Supply Chain

- 9.1.8 Kuehne + Nagel International AG

- 9.1.9 Nippon Express

- 9.1.10 XPO Logistics

- 9.2 Regional Player

- 9.2.1 Agility Logistics

- 9.2.2 APL Logistics

- 9.2.3 Bollore Logistics

- 9.2.4 Geodis

- 9.2.5 Hellmann Worldwide Logistics

- 9.2.6 Hitachi Transport System

- 9.2.7 Kerry Logistics

- 9.2.8 Panalpina

- 9.2.9 Toll Group

- 9.2.10 Yusen Logistics

- 9.3 Emerging Players

- 9.3.1 eBike Diagnostic Solutions

- 9.3.2 MotoTech Diagnostics

- 9.3.3 NeoMotor Diagnostics

- 9.3.4 RideScan Electronics

- 9.3.5 SmartMoto Diagnostics