|

시장보고서

상품코드

1913411

동물 사료용 단백질 원료 시장 : 기회, 성장 요인, 산업 동향 분석 및 예측(2026-2035년)Animal Feed Protein Ingredients Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

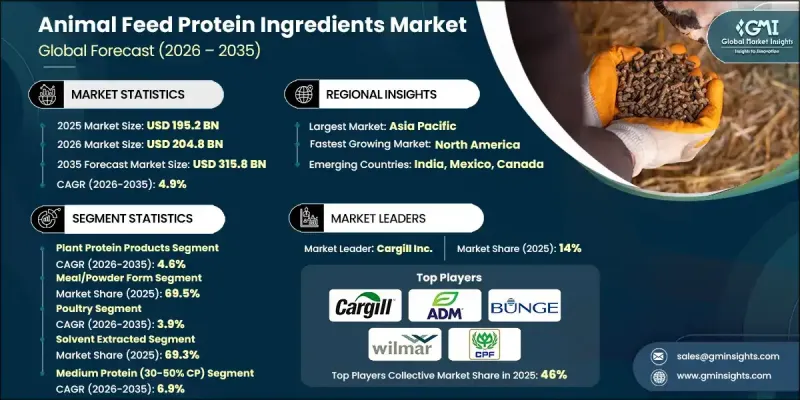

세계의 동물 사료용 단백질 원료 시장은 2025년 1,952억 달러로 평가되었으며, 2035년까지 연평균 복합 성장률(CAGR) 4.9%로 성장하여 3,158억 달러에 이를 것으로 예측됩니다.

이 시장의 성장은 사료 효율, 동물 건강, 육류, 유제품 및 수산물 생산에서 고품질 단백질 함유에 대한 수요 증가로 인한 것입니다. 식물성 단백질, 곤충 유래 단백질, 기능성 첨가물을 포함한 동물 사료용 단백질 원료는 소화율과 영양 흡수를 향상시켜 생산성과 지속가능성을 모두 지원합니다. 세계 환경 규제와 저탄소 생산 기법에 대한 추진이 업계를 보다 지속 가능한 실천으로 이끌고 있습니다. 지역마다의 동향은 다르며 아시아태평양은 축산 및 수산 양식 부문 확대에 의해 성장을 견인하고, 유럽은 추적 가능성와 지속가능성에 주력하고, 북미는 동물의 퍼포먼스와 건강을 위한 특수 배합 사료를 중시하고 있습니다. 자원을 최적화하고 폐기물을 줄이기 위해 순환 경제의 원칙과 통합 생산 모델을 채택하는 기업은 장기적인 경쟁 우위를 수립하는 입장에 있습니다. 혁신적이고 책임있는 조달을 통해 단백질 솔루션에 대한 관심이 증가함에 따라 시장은 계속 진화하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 연도 | 2026-2035년 |

| 시작 규모 | 1,952억 달러 |

| 예측 금액 | 3,158억 달러 |

| CAGR | 4.9% |

식물성 단백질 제품 부문은 2025년 71.2%의 점유율을 차지했고, 2035년까지 연평균 복합 성장률(CAGR) 4.6%를 보일 것으로 예측됩니다. 콩, 캐놀라 및 기타 작물에서 얻은 식물성 단백질은 가축과 수산 양식에 균형 잡힌 아미노산을 공급하는 비용 효율성과 지속가능성이 뛰어난 선택이며 자원 효율성과 환경 책임에 관한 세계의 목표에 부합합니다.

물리적 형태별로는 식사 및 분말 부문이 2025년에 69.5%의 점유율을 차지했고, 2026년부터 2035년까지 CAGR 4.7%를 보일 것으로 예측됩니다. 이러한 형태는 다양성, 배합 사료에 대한 혼합의 용이성, 균일한 영양 분포, 자동 공급 시스템과의 호환성에서 선호됩니다. 펠렛이나 압출 성형품 등의 건조 형태는 영양소의 방출 제어, 사료 효율의 향상, 집약적인 축산 및 수산 양식에서 폐기물 감축의 관점에서 주목을 끌고 있습니다.

유럽 동물 사료용 단백질 원료 시장은 2025년 339억 달러 규모에 이르렀으며 예측 기간 동안 견조한 성장이 예상됩니다. 엄격한 품질 기준과 책임있는 조달 규정은 환경 목표와 영양 목표를 충족시키는 단백질 블렌드의 혁신을 추진하고 있습니다. 독일은 첨단 축산업과 진보적인 사료 정책을 통해 시장에 크게 기여하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 요인

- 세계의 육류 및 유제품 소비량 증가

- 양식산업 확대

- 반려동물 사육률 상승과 프리미엄 반려동물 먹이 수요 증가

- 업계의 잠재적 위험 및 과제

- 변동하는 원재료 가격

- 환경 및 지속가능성에 관한 우려 사항

- 시장 기회

- 곤충 단백질 시장의 상승

- 미생물 및 발효 단백질 성장

- 성장 요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 가격 동향

- 지역별

- 제품 유형별

- 향후 시장 동향

- 기술과 혁신 동향

- 현재의 기술 동향

- 신흥기술

- 특허 상황

- 무역 통계(HS코드)

(참고 : 무역 통계는 주요 국가에서만 제공됩니다)

- 주요 수입국

- 주요 수출국

- 지속가능성과 환경면

- 지속가능한 대처

- 폐기물 감축 전략

- 생산에서의 에너지 효율

- 환경에 배려한 대처

- 탄소발자국 고려

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 인수합병

- 제휴 및 협업

- 신제품 발매

- 사업 확대 계획

제5장 시장 추계 및 예측 : 제품 유형별, 2022-2035년

- 식물성 단백질 제품

- 지방종자 사료

- 대두 단백질 농축물 및 분리물

- 콩류 단백질(완두콩, 루핀, 잠두)

- 옥수수 단백질(글루텐 밀, 글루텐 피드)

- 밀 단백질 제품

- 감자 단백질

- 기타 식물성 단백질(알팔파, 쌀)

- 동물성 단백질 제품(ABP)

- 육류 및 골분

- 육분

- 혈액분

- 우모분

- 가금류 육분

- 유제품 단백질(카제인, 우유 단백질, 락토알부민)

- 해양성 단백질 제품

- 어분(흰살 생선, 검은 생선)

- 생선 단백질 농축물

- 생선 용해물

- 갑각류 단백질(새우, 게, 조개류)

- 연체동물 단백질(오징어, 조개)

- 미생물 및 발효 유래 단백질

- 건조 발효 바이오매스

- 효모 단백질(1차 배양, 양조용, 톨라)

- 효모 배양물

- 조류 단백질

- 곤충 단백질

- 블랙솔저플라이 유충

- 귀뚜라미 가루

- 밀웜 가루

- 기타

제6장 시장 추계 및 예측 : 물리적 형태별, 2022-2035년

- 밀 및 분말

- 케이크

- 펠렛 및 압출

- 액체 농축

- 매쉬

제7장 시장 추계 및 예측 : 축산별, 2022-2035년

- 가금류

- 브로일러

- 레이어

- 터키

- 기타(오리, 거위)

- 돼지

- 새끼 돼지

- 육성돈

- 비육돈

- 암퇘지

- 소 (반추동물)

- 젖소

- 육용소

- 송아지, 송아지 고기

- 기타(물소, 들소)

- 양식

- 연어

- 송어

- 새우

- 잉어

- 틸라피아

- 메기(채널 메기, 노란 메기)

- 바닷물고기(농어, 병어, 가물치, 청어, 장어)

- 기타(거북, 게, 연체 동물)

- 반려동물 식품

- 개

- 고양이

- 조류

- 관상용 어류

- 소형 포유류

- 말

- 기타 가축(양, 염소, 토끼)

제8장 시장 추계 및 예측 : 제조 및 가공 방법별, 2022-2035년

- 렌더링 제품

- 용매 추출법

- 기계적 추출 및 압착 방식

- 발효 유래

- 가수분해

- 농축 및 분리

제9장 시장 추계 및 예측 : 단백질 함유량별, 2022-2035년

- 고단백질(CP 50% 초과)

- 중단백질(30-50% CP)

- 저-중단백질(20-30% CP)

제10장 시장 추계 및 예측 : 지역별, 2022-2035년

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 기타 라틴아메리카

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

제11장 기업 프로파일

- Cargill Inc.

- Archer Daniels Midland Company(ADM)

- Bunge Limited

- Wilmar International Limited

- Charoen Pokphand Foods PCL

- Evonik Industries AG

- DSM-Firmenich

- Nutreco NV

- TASA(Tecnologica de Alimentos SA)

- Copeinca(Cooke Aquaculture)

- De Heus Animal Nutrition

- Alltech Inc.

- Protix BV

- InnovaFeed

- Calysta Inc.

The Global Animal Feed Protein Ingredients Market was valued at USD 195.2 billion in 2025 and is estimated to grow at a CAGR of 4.9% to reach USD 315.8 billion by 2035.

The market is fueled by rising demand for feed efficiency, animal health, and high-quality protein content in meat, dairy, and seafood production. Animal feed protein ingredients, including plant proteins, insect proteins, and functional additives, enhance digestibility and nutrient absorption, supporting both productivity and sustainability. Global environmental regulations and the push for low-carbon production methods are shaping the industry toward more sustainable practices. Regional dynamics vary, with Asia-Pacific driving growth due to expanding livestock and aquaculture sectors, Europe focusing on traceability and sustainability, and North America emphasizing specialty blends for animal performance and health. Companies adopting circular economy principles and integrated production models to optimize resources and reduce waste are positioned for long-term competitive advantage. The market is evolving with increasing interest in innovative, responsibly sourced protein solutions.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $195.2 Billion |

| Forecast Value | $315.8 Billion |

| CAGR | 4.9% |

The plant protein products segment held 71.2% share in 2025 and is expected to grow at a CAGR of 4.6% through 2035. Plant-based proteins, sourced from soy, canola, and other crops, remain cost-effective and sustainable options for supplying balanced amino acids to livestock and aquaculture, aligning with global goals for resource efficiency and environmental responsibility.

By physical form, the meal and powder segment held a 69.5% share in 2025 and is forecast to grow at a CAGR of 4.7% during 2026-2035. These forms are preferred for their versatility, ease of blending into compound feeds, uniform nutrient distribution, and compatibility with automated feeding systems. Dry forms such as pellets and extrudates are gaining attention for controlled nutrient release, improved feed efficiency, and reduced wastage in intensive farming and aquaculture applications.

Europe Animal Feed Protein Ingredients Market accounted for USD 33.9 billion in 2025 and is expected to show strong growth throughout the forecast period. Stringent quality standards and responsible sourcing regulations are driving innovation in protein blends that meet environmental and nutritional goals. Germany contributes significantly due to its advanced livestock industry and progressive feed policies.

Key players operating in the Animal Feed Protein Ingredients Market include Cargill Inc., Archer Daniels Midland Company (ADM), Bunge Limited, Wilmar International Limited, Charoen Pokphand Foods PCL, Evonik Industries AG, DSM-Firmenich, Nutreco N.V., TASA (Tecnologica de Alimentos S.A.), Copeinca (Cooke Aquaculture), De Heus Animal Nutrition, Alltech Inc., Protix B.V., InnovaFeed, and Calysta Inc. Companies in the Animal Feed Protein Ingredients Market are adopting strategies to strengthen their presence and competitive positioning. They are investing in R&D to develop innovative protein blends and functional additives that improve animal performance while supporting sustainability. Expansion into emerging markets with growing livestock and aquaculture industries is a priority. Firms are enhancing processing technologies and product quality to meet regulatory standards and consumer demands. Collaborations, mergers, and acquisitions are being used to consolidate supply chains and access new distribution channels.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Physical form

- 2.2.4 Livestock

- 2.2.5 Production/processing method

- 2.2.6 Protein content

- 2.3 TAM Analysis, 2025-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing global meat & dairy consumption

- 3.2.1.2 Expansion of aquaculture industry

- 3.2.1.3 Rising pet ownership & premium pet food demand

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Volatile raw material prices

- 3.2.2.2 Environmental & sustainability concerns

- 3.2.3 Market opportunities

- 3.2.3.1 Insect protein market emergence

- 3.2.3.2 Microbial & fermentation protein growth

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

( Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Plant protein products

- 5.2.1 Oilseed meals

- 5.2.2 Soy protein concentrate & isolate

- 5.2.3 Pulse proteins (pea, lupin, fava bean)

- 5.2.4 Corn protein (gluten meal, gluten feed)

- 5.2.5 Wheat protein products

- 5.2.6 Potato protein

- 5.2.7 Other plant proteins (alfalfa, rice)

- 5.3 Animal protein products (ABP)

- 5.3.1 Meat & bone meal

- 5.3.2 Meat meal

- 5.3.3 Blood meal

- 5.3.4 Feather meal

- 5.3.5 Poultry meal

- 5.3.6 Dairy proteins (casein, milk protein, lactalbumin)

- 5.4 Marine protein products

- 5.4.1 Fishmeal (white fish, dark fish)

- 5.4.2 Fish protein concentrate

- 5.4.3 Fish solubles

- 5.4.4 Crustacean proteins (shrimp, crab, shellfish)

- 5.4.5 Mollusk proteins (squid, clam)

- 5.5 Microbial & fermentation proteins

- 5.5.1 Dried fermentation biomass

- 5.5.2 Yeast proteins (primary, brewers, torula)

- 5.5.3 Yeast culture

- 5.5.4 Algae proteins

- 5.6 Insect proteins

- 5.6.1 Black soldier fly larvae

- 5.6.2 Cricket meal

- 5.6.3 Mealworm meal

- 5.7 Others

Chapter 6 Market Estimates and Forecast, By Physical Form, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Meal/Powder Form

- 6.3 Cake Form

- 6.4 Pellet/Extruded Form

- 6.5 Liquid/Condensed Form

- 6.6 Mash Form

Chapter 7 Market Estimates and Forecast, By Livestock, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Poultry

- 7.2.1 Broiler

- 7.2.2 Layer

- 7.2.3 Turkey

- 7.2.4 Others (duck, geese)

- 7.3 Swine

- 7.3.1 Starter

- 7.3.2 Grower

- 7.3.3 Finisher

- 7.3.4 Sow

- 7.4 Cattle (ruminants)

- 7.4.1 Dairy cattle

- 7.4.2 Beef cattle

- 7.4.3 Calf/veal

- 7.4.4 Others (buffalo, bison)

- 7.5 Aquaculture

- 7.5.1 Salmon

- 7.5.2 Trout

- 7.5.3 Shrimp

- 7.5.4 Carp

- 7.5.5 Tilapia

- 7.5.6 Catfish (channel, yellow)

- 7.5.7 Marine fish (seabass, pomfret, snakehead, herring, eel)

- 7.5.8 Others (turtle, crab, mollusks)

- 7.6 Petfood

- 7.6.1 Dogs

- 7.6.2 Cats

- 7.6.3 Birds

- 7.6.4 Fish (ornamental)

- 7.6.5 Small mammals

- 7.7 Equine

- 7.8 Other livestock (sheep, goats, rabbits)

Chapter 8 Market Estimates and Forecast, By Production/Processing Method, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Rendered Products

- 8.3 Solvent Extracted

- 8.4 Mechanically Extracted/Expeller Pressed

- 8.5 Fermentation-Derived

- 8.6 Hydrolyzed

- 8.7 Concentrated/Isolated

Chapter 9 Market Estimates and Forecast, By Protein Content, 2022-2035 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 High Protein (>50% Crude Protein)

- 9.3 Medium Protein (30-50% CP)

- 9.4 Low-Medium Protein (20-30% CP)

Chapter 10 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Rest of Europe

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Rest of Asia Pacific

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Rest of Latin America

- 10.6 Middle East and Africa

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

- 10.6.4 Rest of Middle East and Africa

Chapter 11 Company Profiles

- 11.1 Cargill Inc.

- 11.2 Archer Daniels Midland Company (ADM)

- 11.3 Bunge Limited

- 11.4 Wilmar International Limited

- 11.5 Charoen Pokphand Foods PCL

- 11.6 Evonik Industries AG

- 11.7 DSM-Firmenich

- 11.8 Nutreco N.V.

- 11.9 TASA (Tecnologica de Alimentos S.A.)

- 11.10 Copeinca (Cooke Aquaculture)

- 11.11 De Heus Animal Nutrition

- 11.12 Alltech Inc.

- 11.13 Protix B.V.

- 11.14 InnovaFeed

- 11.15 Calysta Inc.