|

시장보고서

상품코드

1913421

폴리이소부틸렌 시장 : 기회, 성장 요인, 산업 동향 분석 및 예측(2026-2035년)Polyisobutylene Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

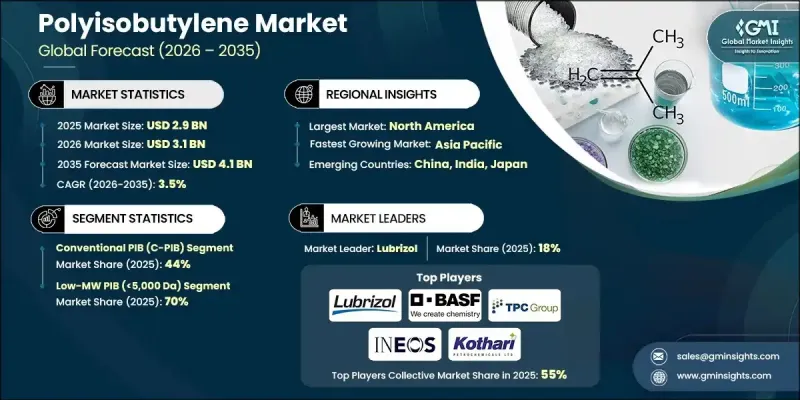

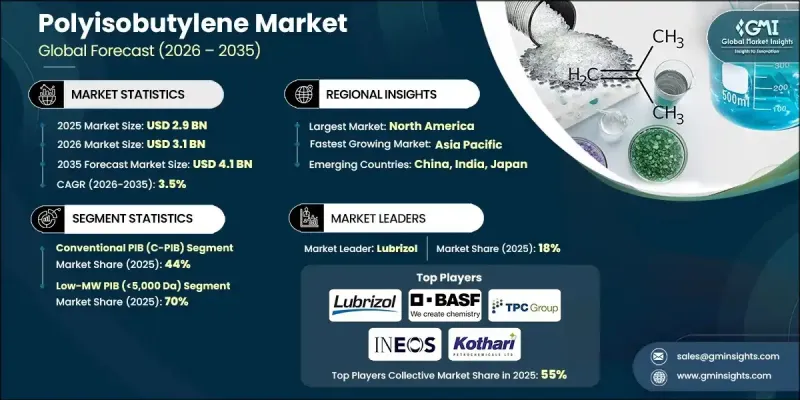

세계의 폴리이소부틸렌 시장은 2025년 29억 달러로 평가되었으며, 2035년까지 연평균 복합 성장률(CAGR) 3.5%로 성장하여 41억 달러에 이를 것으로 예측됩니다.

이 성장은 식품 접촉 용도 및 퍼스널케어 산업 등의 안전 및 품질 기준 강화에 의해 추진되고 있으며, 이들은 적합성이 있는 폴리이소부틸렌(PIB) 등급의 채용을 촉진하고 있습니다. 미국 식품의약국(FDA)을 포함한 규제 당국의 승인에 의해 식품접촉용 접착제나 코팅에 PIB 사용이 가능해졌으며, 안전성을 확보하기 위해 특정 최소 수평균 분자량 기준이 설정되어 있습니다. 화장품 및 수소화 PIB 등급은 피부 연화제 및 필름 형성 응용 분야에서 안정성과 피부 적합성을 제공하며 틈새 시장에서 프리미엄 가격 설정을 지원합니다. 신흥 지역의 인프라 확장은 접착제, 실란트 및 유리 코팅 솔루션에 대한 수요를 추진하고 있으며 PIB의 점착성, 유연성, 내화학성 및 매우 낮은 수증기 투과성이 높게 평가되고 있습니다. 게다가, 지속가능성의 동향과 규제 강화는 바이오 PIB와 깨끗한 제조 공정의 개발을 촉진함과 동시에 진화하는 컴플라이언스 틀이 환경 부하가 낮은 촉매 및 친환경 원료에 대한 연구 개발을 이끌고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 연도 | 2026-2035년 |

| 시작 규모 | 29억 달러 |

| 예측 금액 | 41억 달러 |

| CAGR | 3.5% |

기존 PIB(C-PIB) 부문은 접착제, 실란트, 산업용 오일, 츄잉껌 베이스, 코팅제 등의 광범위한 용도로 2025년 44%의 점유율을 차지했습니다. C-PIB 수요는 유연성, 끈끈함, 방습성에 의존하는 건설 및 포장 부문과 밀접하게 연동되어 있습니다. C-PIB 시장 가격은 분자량과 순도에 따라 일반적으로 1Kg당 0.8-1.5달러의 범위로 추이하고 있으며, TPC Group, BASF, INEOS 등 주요 제조업체가 강력한 공급 기반을 유지하고 있습니다.

고분자량 PIB(100,000 Da 초과) 부문은 2025년 10%의 점유율을 차지했으며, 무미, 비독성 및 고차단성을 필요로 하는 츄잉껌 베이스, 의료기기, 특수 실란트 등의 틈새 용도에 제공되고 있습니다. 제조 공정의 진보에 의해 수율이 향상되어 내열성이 확대됨으로써 의료용 및 식품 등급 용도의 적용 범위가 넓어지고 있습니다.

북미 폴리이소부틸렌 시장은 2025년 33%의 점유율을 차지했습니다. 이것은 자동차 산업의 집적, 고반응성 PIB의 강력한 공급 체제, 첨가제 배합 제조업체의 견고한 네트워크에 의해 지원되었습니다. 미국은 통합 석유화학 콤비나트와 풍부한 원료 공급으로 생산능력의 주요 담당자로 지속되고 캐나다는 자동차 및 윤활유 섹터가 지역 공급망과 다운스트림 용도를 보완하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 요인

- 업계의 잠재적 위험 및 과제

- 시장 기회

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 가격 동향

- 지역별

- 미래 시장 동향

- 기술과 혁신 동향

- 현재의 기술 동향

- 신흥기술

- 특허 상황

- 무역 통계(HS코드)(참고 : 무역 통계는 주요 국가에서만 제공됨)

- 주요 수입국

- 주요 수출국

- 지속가능성과 환경면

- 지속가능한 대처

- 폐기물 감축 전략

- 생산에서의 에너지 효율

- 환경에 배려한 대처

- 탄소발자국에 관한 고려 사항

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 인수합병

- 제휴 및 협업

- 신제품 발매

- 확대 계획

제5장 시장 규모와 예측 : 제품 유형별, 2022-2035년

- 기존 폴리이소부틸렌(C-PIB)

- 고반응성 폴리이소부틸렌(HR-PIB)

제6장 시장 규모와 예측 : 분자량별, 2022-2035년

- 저분자량 PIB(5,000 Da 미만)

- 중분자량 PIB(40,000-100,000 Da)

- 고분자량 PIB(100,000 Da 초과)

제7장 시장 규모와 예측 : 용도별, 2022-2035년

- 윤활유 첨가제

- 연료 첨가제

- 접착제 및 실란트

- 타이어 및 고무 제품

- 전기 절연

- 퍼스널케어 및 화장품

- 식품 접촉 용도

- 스트레치 필름 및 포장

- 기타

제8장 시장 규모와 예측 : 등급별, 2022-2035년

- 식품 등급 PIB

- 화장품 등급 PIB

- 의약품 등급 PIB

- 기타

제9장 시장 규모와 예측 : 지역별, 2022-2035년

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 기타 라틴아메리카

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

제10장 기업 프로파일

- Braskem

- RB Products

- TPC Group

- Lanxess

- Infineum International

- Kothari Petrochemicals

- Janex

- ExxonMobil Corporation

- Berkshire Hathaway

- Lubrizol

- Chevron Oronite Company

- Mayzo

The Global Polyisobutylene Market was valued at USD 2.9 billion in 2025 and is estimated to grow at a CAGR of 3.5% to reach USD 4.1 billion by 2035.

The growth is driven by increasing safety and quality standards in industries such as food contact and personal care, which encourage the adoption of compliant PIB grades. Regulatory approvals, including those by the U.S. FDA, allow PIB in food-contact adhesives and coatings, with specific minimum number-average molecular weight thresholds to ensure safety. Cosmetic and hydrogenated PIB grades provide stability and skin compatibility for emollients and film-forming applications, supporting premium pricing in niche markets. The expansion of infrastructure in emerging regions fuels demand for adhesives, sealants, and glazing solutions, where PIB's tack, flexibility, chemical resistance, and extremely low moisture vapor transmission are highly valued. Additionally, sustainability trends and regulatory tightening are encouraging the development of bio-based PIB and cleaner production processes, while evolving compliance frameworks are directing R&D toward lower-impact catalysts and environmentally friendly feedstocks.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.9 Billion |

| Forecast Value | $4.1 Billion |

| CAGR | 3.5% |

The conventional PIB (C-PIB) segment held 44% share in 2025, owing to its extensive use in adhesives, sealants, industrial oils, chewing gum bases, and coatings. Demand for C-PIB closely follows construction and packaging sectors that rely on its flexibility, tack, and moisture barrier properties. Market prices for C-PIB typically range from USD 0.8-1.5 per kilogram, depending on molecular weight and purity, with major producers such as TPC Group, BASF, and INEOS maintaining strong supply positions.

The high-molecular-weight PIB (>100,000 Da) segment accounted for 10% share in 2025, serving niche applications like chewing gum bases, medical devices, and specialized sealants that require tastelessness, non-toxicity, and high barrier strength. Advances in production processes have increased yields and expanded temperature tolerance, broadening the application spectrum for medical and food-grade uses.

North America Polyisobutylene Market held 33% share in 2025, driven by a concentration of automotive hubs, strong merchant high-reactivity PIB supply, and a robust network of additive formulators. The U.S. remains a key contributor to production capacity, supported by integrated petrochemical complexes and abundant feedstocks, while Canada's automotive and lubricant sectors complement regional supply and downstream applications.

Key players in the Global Polyisobutylene Market include TPC Group, Braskem SA, Lanxess, RB Products, Infineum International Ltd, Kothari Petrochemicals, Janex, ExxonMobil Corporation, Berkshire Hathaway, Lubrizol, Chevron Oronite Company, and Mayzo. To strengthen their presence, companies in the Polyisobutylene Market focus on several strategic approaches. They invest heavily in process optimization and R&D to enhance product quality, expand molecular weight ranges, and develop bio-based and sustainable grades. Strategic collaborations and partnerships allow for technology sharing, faster commercialization, and access to new regional markets. Firms also pursue capacity expansions in key geographies, particularly near high-demand industrial hubs, ensuring reliable supply chains. Additionally, regulatory compliance and certifications are emphasized to support entry into food, cosmetic, and medical applications.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Product type

- 2.2.2 Molecular weight

- 2.2.3 Grade

- 2.2.4 Application

- 2.3 TAM analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Size and Forecast, By Product Type, 2022-2035 (USD Billion, Kilo Tons)

- 5.1 Key trends

- 5.2 Conventional polyisobutylene (C-PIB)

- 5.3 Highly reactive polyisobutylene (HR-PIB)

Chapter 6 Market Size and Forecast, By Molecular Weight, 2022-2035 (USD Billion, Kilo Tons)

- 6.1 Key trends

- 6.2 Low molecular weight PIB (Mn < 5,000 Da)

- 6.3 Medium molecular weight PIB (Mn 40,000-100,000 Da)

- 6.4 High molecular weight PIB (Mn > 100,000 Da)

Chapter 7 Market Size and Forecast, By Application, 2022-2035 (USD Billion, Kilo Tons)

- 7.1 Key trends

- 7.2 Lubricant additives

- 7.3 Fuel additives

- 7.4 Adhesives & sealants

- 7.5 Tires & rubber products

- 7.6 Electrical insulation

- 7.7 Personal care & cosmetics

- 7.8 Food contact applications

- 7.9 Stretch films & packaging

- 7.10 Others

Chapter 8 Market Size and Forecast, By Grade, 2022-2035 (USD Billion, Kilo Tons)

- 8.1 Key trends

- 8.2 Food-grade PIB

- 8.3 Cosmetic-grade PIB

- 8.4 Pharmaceutical-grade PIB

- 8.5 Others

Chapter 9 Market Size and Forecast, By Region, 2022-2035 (USD Billion, Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East & Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

- 9.6.4 Rest of Middle East & Africa

Chapter 10 Company Profiles

- 10.1 Braskem

- 10.2 RB Products

- 10.3 TPC Group

- 10.4 Lanxess

- 10.5 Infineum International

- 10.6 Kothari Petrochemicals

- 10.7 Janex

- 10.8 ExxonMobil Corporation

- 10.9 Berkshire Hathaway

- 10.10 Lubrizol

- 10.11 Chevron Oronite Company

- 10.12 Mayzo