|

시장보고서

상품코드

1928902

금속 가공유 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Metalworking Fluids Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

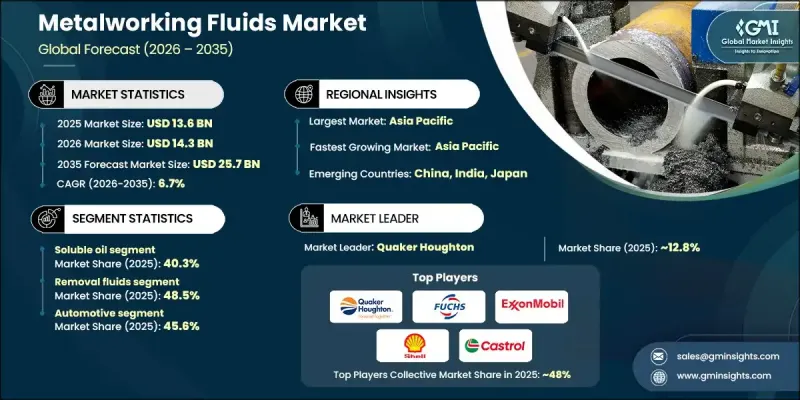

세계의 금속 가공유 시장은 2025년에 136억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 6.7%로 성장하여 257억 달러에 이를 것으로 예측됩니다.

금속 가공유는 가공, 연삭, 성형, 표면처리 공정에 필수적인 특수 윤활제 및 냉각제로 정의됩니다. 이들 제품은 순수 오일, 수용성 오일, 반합성 오일, 완전 합성 오일로 제공되며, 마찰 감소, 방열, 칩 제거, 부식 방지, 공구 수명 연장 등의 중요한 기능을 수행합니다. 용해성 유제는 비용 효율성, 에멀젼 안정성, 다양한 가공 공정에 대한 적응성으로 인해 널리 채택되어 시장을 선도하고 있습니다. 시장 성장은 자동차 및 항공우주 제조의 확대, 고정밀 부품에 대한 수요 증가, 가공 기술의 발전에 의해 촉진되고 있습니다. 바이오 및 지속 가능한 배합에 대한 관심 증가와 고속 및 복잡한 금속 가공을 위한 성능 특성 향상도 세계 수요를 더욱 견인하고 있습니다. 열 안정성, 윤활성, 표면 마감 품질에 대한 지속적인 혁신을 통해 금속 가공유는 현대 제조에 없어서는 안 될 필수 요소로 자리매김하고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 연도 | 2026-2035년 |

| 개시 연도 가치 | 136억 달러 |

| 예측 금액 | 257억 달러 |

| CAGR | 6.7% |

수용성 오일 부문은 2025년 40.3%의 점유율을 차지할 것으로 예상되며, 2026년부터 2035년까지 연평균 복합 성장률(CAGR) 6.5%를 나타낼 것으로 예측됩니다. 수용성 오일은 냉각 효율, 윤활 성능, 비용 효율의 균형이 우수하여 선호되고 있습니다. 이 유체는 우수한 유화 안정성과 다용도성으로 밀링, 드릴링, 터닝, 연삭 등 다양한 가공에 사용할 수 있습니다. 수성 배합은 중간 부하 작업에서 충분한 윤활성을 유지하면서 효율적인 열 방출을 실현하기 때문에 일반적인 가공 요건에서 선호되는 선택이 되었습니다.

제거 유체 부문은 2025년 48.5%의 점유율을 차지할 것으로 예상되며, 2026년부터 2035년까지 연평균 복합 성장률(CAGR) 7.2%를 나타낼 것으로 예측됩니다. 그 우위는 자동차, 항공우주, 일반 엔지니어링 분야의 절삭, 연삭, 밀링, 드릴링, 터닝 작업에 대한 기본적인 수요에 의해 뒷받침됩니다. 절삭유는 금속 제거 공정에서 중요한 윤활, 냉각, 칩 관리 및 공구 보호 기능을 제공하여 일관된 생산성을 보장합니다. 다양한 금속과 작업 조건에 폭넓게 적용할 수 있기 때문에 가공의 기초로서 중요한 역할을 하고 있습니다.

미국 금속 가공유 시장은 2025년 26억 달러 규모에 달했습니다. 북미, 특히 미국의 성장은 자동차 제조, 항공우주 부품 제조, 기계 생산 등 강력한 산업 기반에 의해 뒷받침되고 있습니다. 엔진, 변속기, 구조 부품 제조의 정확성, 효율성, 신뢰성에 대한 요구로 절삭유, 반합성유, 성형유 등 고성능 유체에 대한 수요가 지속되고 있습니다. 선진적인 인프라, 확립된 생산 시설, 엄격한 품질 기준은 지역 시장의 채택을 지속적으로 촉진하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급업체 상황

- 이익률

- 각 단계 부가가치

- 밸류체인에 영향을 미치는 요인

- 파괴적 변화

- 업계에 대한 영향요인

- 성장 촉진요인

- 업계의 잠재적 리스크&과제

- 시장 기회

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter의 Five Forces 분석

- PESTEL 분석

- 기술과 혁신 동향

- 현재 기술 동향

- 신기술

- 가격 동향

- 지역별

- 제품별

- 향후 시장 동향

- 기술과 혁신 동향

- 현재 기술 동향

- 신기술

- 특허 상황

- 무역 통계(HS코드)

(주 : 무역 통계는 주요 국가에 한해 제공됩니다)

- 주요 수입국

- 주요 수출국

- 지속가능성과 환경면

- 지속가능한 대처

- 폐기물 감축 전략

- 생산 에너지 효율

- 친환경 이니셔티브

- 탄소발자국 고려

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 인수합병(M&A)

- 제휴 및 협업

- 신제품 발매

- 확대 계획

제5장 시장 추산·예측 : 제품별, 2022-2035

- 순유

- 가용성유

- 반합성 유체

- 합성 유체

제6장 시장 추산·예측 : 용도별, 2022-2035

- 제거액

- 성형용 유체

- 보호액

- 처리액

제7장 시장 추산·예측 : 최종 용도별, 2022-2035

- 자동차

- 항공우주

- 건설

- 전기 및 전력

- 농업

- 선박

- 헬스케어

- 기타

제8장 시장 추산·예측 : 지역별, 2022-2035

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 기타 라틴아메리카

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카공화국

- 아랍에미리트

- 기타 중동 및 아프리카

제9장 기업 개요

- Quaker Houghton

- FUCHS Petrolub SE

- ExxonMobil

- Shell(Shell Lubricants)

- BP Castrol

- Chevron(Caltex)

- TotalEnergies

- Idemitsu Kosan

- Yushiro Chemical

- Blaser Swisslube

- Master Fluid Solutions

- Milacron(Cimcool)

- Oemeta Chemische Werke

- Petron Corporation

- Phoenix Petroleum Philippines

The Global Metalworking Fluids Market was valued at USD 13.6 billion in 2025 and is estimated to grow at a CAGR of 6.7% to reach USD 25.7 billion by 2035.

Metalworking fluids are described as specialized lubricants and coolants essential for machining, grinding, forming, and surface treatment processes. These products, available as neat oils, soluble oils, semi-synthetic, and fully synthetic fluids, provide vital functions such as friction reduction, heat dissipation, chip removal, corrosion protection, and tool life enhancement. Soluble oils dominate the market with broad adoption due to their cost-effectiveness, emulsion stability, and suitability across diverse machining operations. Market growth is propelled by expanding automotive and aerospace manufacturing, rising demand for high-precision components, and advances in machining technologies. Increasing focus on bio-based and sustainable formulations, along with enhanced performance characteristics for high-speed and complex metalworking, is further driving global demand. Continuous innovation in thermal stability, lubricity, and surface finish quality ensures that metalworking fluids remain indispensable in modern manufacturing.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $13.6 billion |

| Forecast Value | $25.7 billion |

| CAGR | 6.7% |

The soluble oil segment accounted for 40.3% share in 2025 and is expected to grow at a CAGR of 6.5% from 2026 to 2035. Soluble oils are favored due to their ability to provide a balanced combination of cooling efficiency, lubrication performance, and cost-effectiveness. These fluids offer excellent emulsion stability and versatility, supporting applications like milling, drilling, turning, and grinding. Their water-based formulation ensures efficient heat dissipation while maintaining sufficient lubrication for moderate-duty operations, making them a preferred choice for general machining requirements.

The removal fluids segment held a 48.5% share in 2025 and is projected to grow at a CAGR of 7.2% from 2026 to 2035. Their dominance is driven by the fundamental need for cutting, grinding, milling, drilling, and turning operations across automotive, aerospace, and general engineering sectors. Removal fluids provide critical lubrication, cooling, chip management, and tool protection, ensuring consistent productivity in metal removal processes. They remain the backbone of machining operations due to their wide applicability across various metals and operational conditions.

U.S. Metalworking Fluids Market generated USD 2.6 billion in 2025. Growth in North America, particularly in the United States, is supported by a strong industrial base encompassing automotive manufacturing, aerospace component fabrication, and machinery production. The demand for high-performance fluids, including removal, semi-synthetic, and forming fluids, is sustained by the requirement for precision, efficiency, and reliability in engine, transmission, and structural component manufacturing. Advanced infrastructure, established production facilities, and stringent quality standards continue to drive regional market adoption.

Key players operating in the Global Metalworking Fluids Market include Quaker Houghton, ExxonMobil, FUCHS Petrolub SE, Blaser Swisslube, Chevron (Caltex), TotalEnergies, Idemitsu Kosan, Shell (Shell Lubricants), Milacron (Cimcool), Master Fluid Solutions, Yushiro Chemical, Petron Corporation, Oemeta Chemische Werke, Phoenix Petroleum Philippines, and BP Castrol. Companies in the Global Metalworking Fluids Market are strengthening their positions by focusing on product innovation, sustainability, and technical support. Leading manufacturers are developing high-performance synthetic and semi-synthetic fluids with improved thermal stability, lubricity, and emulsion life to meet the demands of modern machining operations. Strategic collaborations with OEMs and industrial partners enable customized solutions tailored to specific metalworking processes. Expansion into emerging regions, coupled with efficient supply chain management, allows companies to widen their global footprint.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Product

- 2.2.2 Application

- 2.2.3 End Use

- 2.2.4 Regional

- 2.3 TAM Analysis, 2025-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter';s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Future market trends

- 3.10 Technology and innovation landscape

- 3.10.1 Current technological trends

- 3.10.2 Emerging technologies

- 3.11 Patent landscape

- 3.12 Trade statistics (HS code)

( Note: the trade statistics will be provided for key countries only)

- 3.12.1 Major importing countries

- 3.12.2 Major exporting countries

- 3.13 Sustainability and environmental aspects

- 3.13.1 Sustainable practices

- 3.13.2 Waste reduction strategies

- 3.13.3 Energy efficiency in production

- 3.13.4 Eco-friendly initiatives

- 3.14 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2022-2035 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Neat oil

- 5.3 Soluble oil

- 5.4 Semi-synthetic fluid

- 5.5 Synthetic fluid

Chapter 6 Market Estimates and Forecast, By Application, 2022-2035 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Removal fluids

- 6.3 Forming fluids

- 6.4 Protecting fluids

- 6.5 Treating fluids

Chapter 7 Market Estimates and Forecast, By End Use, 2022-2035 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Automotive

- 7.3 Aerospace

- 7.4 Construction

- 7.5 Electrical & power

- 7.6 Agriculture

- 7.7 Marine

- 7.8 Healthcare

- 7.9 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022-2035 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Quaker Houghton

- 9.2 FUCHS Petrolub SE

- 9.3 ExxonMobil

- 9.4 Shell (Shell Lubricants)

- 9.5 BP Castrol

- 9.6 Chevron (Caltex)

- 9.7 TotalEnergies

- 9.8 Idemitsu Kosan

- 9.9 Yushiro Chemical

- 9.10 Blaser Swisslube

- 9.11 Master Fluid Solutions

- 9.12 Milacron (Cimcool)

- 9.13 Oemeta Chemische Werke

- 9.14 Petron Corporation

- 9.15 Phoenix Petroleum Philippines