|

시장보고서

상품코드

1928912

자율주행차 시장 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2026-2035년)Self-driving Cars Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

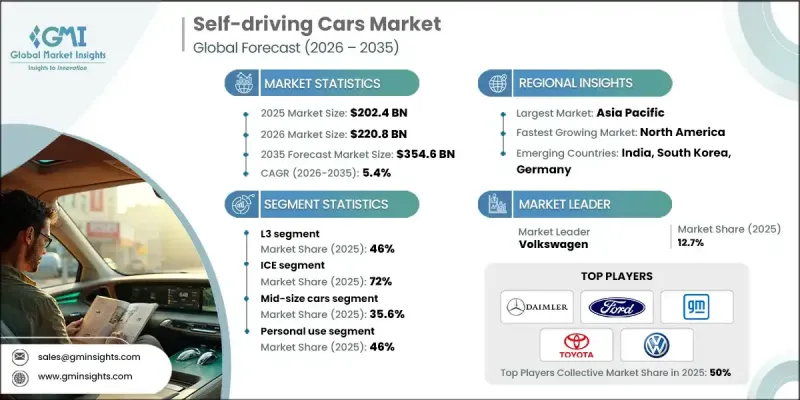

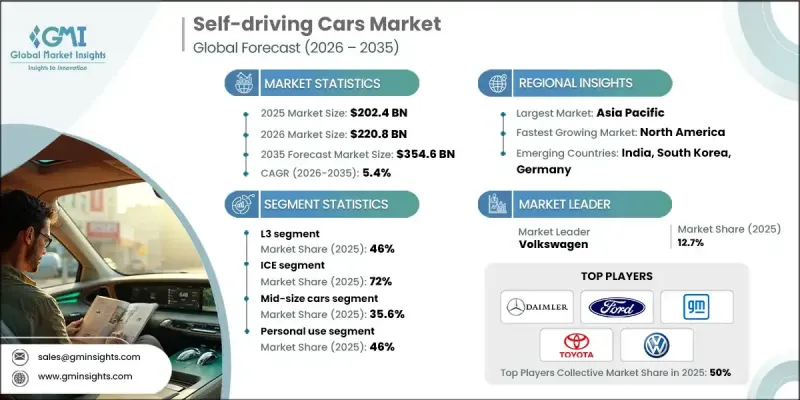

세계의 자율주행차 시장은 2025년에 2,024억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 5.4%로 성장하여 3,546억 달러에 이를 것으로 예측됩니다.

교통 관련 위험 최소화 및 이동 효율성 향상에 대한 관심이 높아지면서 도입이 가속화되고 있습니다. 통제된 테스트와 조기 도입을 지원하는 규제 프레임워크는 자율기술의 새로운 상용화 기회를 열어주고 있습니다. 인공지능, 센싱 시스템, 고성능 컴퓨팅의 발전으로 시스템의 신뢰성과 실제 환경에서의 성능이 향상되고 있습니다. 자율주행차와 지능형 도시 인프라의 통합은 커넥티드 교통 플랫폼, 차량과 인프라 간 통신, 적응형 경로 설정 기능을 통해 시장의 모멘텀을 강화하고 있습니다. 이러한 기술은 교통 흐름을 개선하고, 교통 체증 수준을 낮추며, 에너지 소비를 줄이는 데 도움을 줍니다. 자율 이동 플랫폼의 확장은 도시 교통의 경제성을 재구축하고 차량군의 효율성을 향상시키는 동시에 확장 가능한 자동화 운송 모델을 실현함으로써 추가적인 성장을 뒷받침하고 있습니다. 자율 이동 서비스 플랫폼 시장은 자동화에 초점을 맞춘 시스템 도입 후 차량 그룹 운영자가 최소 30% 이상의 운영 비용 절감 효과를 보고함에 따라 지속적으로 확대되고 있습니다. 이러한 플랫폼은 상업적으로 실행 가능하고 확장 가능한 것으로 입증되어 자동화 운송 서비스에 대한 장기적인 신뢰를 강화하고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 연도 | 2026-2035년 |

| 개시 연도 가치 | 2,024억 달러 |

| 예측 금액 | 3,546억 달러 |

| CAGR | 5.4% |

레벨 3 자율주행 부문은 2025년 46%의 점유율을 차지할 것으로 예상되며, 2026년부터 2035년까지 연평균 5.2%의 성장률을 보일 것으로 전망됩니다. 레벨 3 차량은 운전자가 운전 작업에서 부분적으로 해방될 수 있도록 하면서도 운전자의 준비 태세를 보장하기 위해 여러 차량 카테고리에서 널리 채택되고 있습니다. 자율주행 개발 프로그램의 상당 부분이 레벨3 기능에 초점을 맞추고 있기 때문에 지속적인 수요가 예상됩니다.

내연기관 차량 부문은 2025년 72%의 점유율을 차지할 것으로 예상되며, 2035년까지 연평균 4.8%의 성장률을 보일 것으로 전망됩니다. 이러한 차량은 기존 제조 플랫폼의 이점을 활용하고 자동화 통합을 단순화합니다. 전기 자율주행차는 소프트웨어 기반 아키텍처, 첨단 센서 어레이, 중앙집중식 컴퓨팅 시스템과의 호환성으로 인해 2위를 차지하고 있지만, 내연기관 플랫폼은 기계적 성능 특성에 크게 의존하고 있습니다.

미국 자율주행차 시장은 2025년 83%의 점유율을 차지하며 336억 달러 시장 규모를 형성할 것으로 예측됩니다. 활발한 투자 활동, 유리한 정책 이니셔티브, 가속화되는 상용화로 인해 중국은 자율주행차 개발과 장기적인 시장 성장의 핵심 거점으로서의 지위를 계속 유지하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급업체 상황

- 이익률 분석

- 비용 구조

- 각 단계 부가가치

- 밸류체인에 영향을 미치는 요인

- 파괴적 변화

- 업계에 대한 영향요인

- 업계의 잠재적 리스크&과제

- 시장 기회

- 성장 가능성 분석

- 규제 상황

- 북미

- 미국 국가 도로 교통안전 국(NHTSA) 자율주행차용 FMVSS 갱신

- 미국 운송 성(DOT) 자율주행차 양포괄 계획(AVCP)

- 주 레벨 자율주행 시험 허가(캘리포니아주 DMV 및 네바다주 DMV 가이드라인)

- 캐나다 운송 성 자율주행 시스템(ADS) 시험 가이드라인

- 유럽

- 자동차 섬유지시스템(ALKS)에 관한 유엔 유럽 경제 위원회 규칙 제 157호

- 유럽연합(EU) 자율주행 시스템(ADS) 형 식 인증에 관한 일반 안전 규제(GSR)

- 독일 연방 자동차 운송 국(KBA) 레벨 4 운전 허가

- 영국 자율주행차 법 및 책임 프레임워크

- 아시아태평양

- 중화 인민 공화국 산업 정보화부(MIIT) ICV 시장 참여 가이드

- 국토 교통성(MLIT) 레벨 4라이선싱

- 한국 국토 교통성(MOLIT) 자율주행차 상용 화 안전기준

- 자율주행차에 관한 싱가포르 기술 기준 68(TR 68)

- 인도 도로 운송·고속도로성(MoRTH) 신흥 ADAS 가이드라인

- 라틴아메리카

- 브라질 국가 교통 평의회(CONTRAN)에 의한 운전 지원에 관한 결의

- 멕시코 이동·도로 안전 기본법(LGMSV)이 자동화에 미치는 영향

- 칠레 운송 성에 의한 자율주행 파일럿 시험에 관한 규제

- 유엔 자동차 규제 조화 세계 포럼(WP.29)와의 지역 제휴

- 중동 및 아프리카

- 아랍에미리트(UAE) 도로 교통국(RTA) 자율주행 운송 규제

- 사우디아라비아 SASO 전기자동차 및 자율주행차용 기술 기준

- 이스라엘 운송 성 자율주행차 양시험 시행 가이드라인

- 남아프리카공화국 지능형 교통시스템(ITS)(ITS) 도입 기준

- 북미

- Porter의 Five Forces 분석

- PESTEL 분석

- 기술과 혁신 동향

- 현재 기술 동향

- 신기술

- 가격 동향

- 지역별

- 제품별

- 생산 통계

- 생산 거점

- 소비 거점

- 수출과 수입

- 비용 내역 분석

- 특허 분석

- 지속가능성과 환경면

- 지속가능한 실천

- 폐기물 감축 전략

- 생산 에너지 효율

- 친환경 이니셔티브

- 탄소발자국에 관한 고려사항

- 자율주행 시스템 아키텍처와 소프트웨어 스택

- 자율주행 시스템 아키텍처와 스택 분석

- 컴퓨팅, 센서, 소프트웨어 오케스트레이션 모델

- 자율주행 소프트웨어, AI 및 데이터·플라이휠

- 검증, 테스트 및 안전성 보증 프레임워크

- 자율주행차 비즈니스 모델과 수익화

- 고정도 지도제작, V2X 및 인프라 의존성

- 소비자 신뢰와 보급 장벽

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

- 주요 발전

- 인수합병(M&A)

- 제휴 및 협업

- 신제품 발매

- 사업 확대 계획과 자금조달

제5장 시장 추산·예측 : 자율성 레벨별, 2022-2035

- 레벨 1

- 레벨 2

- 레벨 3

- 레벨 4

- 레벨 5

제6장 시장 추산·예측 : 추진별, 2022-2035

- 내연기관(ICE)

- 전기식

- 하이브리드차

제7장 시장 추산·예측 : 기술별, 2022-2035

- 카메라 기반 시스템

- 레이더 기반 시스템

- LiDAR 기반 시스템

- 센서 퓨전 시스템

제8장 시장 추산·예측 : 차량별, 2022-2035

- 콤팩트 카

- 중형차

- SUV 및 고급차

제9장 시장 추산·예측 : 용도별, 2022-2035

- 개인 이용

- 공유 모빌리티

- 물류·배송

- 공공 운송

- 기타

제10장 시장 추산·예측 : 지역별, 2022-2035

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 북유럽 국가

- 네덜란드

- 스웨덴

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 싱가포르

- 태국

- 인도네시아

- 베트남

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카공화국

- 사우디아라비아

- 아랍에미리트

- 튀르키예

제11장 기업 개요

- 세계 기업

- BMW

- Daimler(Mercedes-Benz)

- Ford Motor Company

- General Motors(GM)

- Honda Motor

- Hyundai Motor

- Stellantis

- Tesla

- Toyota Motor

- Volkswagen

- 지역 기업

- BYD

- Geely

- Renault-Nissan-Mitsubishi Alliance

- SAIC Motor

- Tata Motors

- 신흥 기업/디스럽터

- Aurora Innovation

- Baidu

- NIO

- Waymo

- XPeng Motors

The Global Self-driving Cars Market was valued at USD 202.4 billion in 2025 and is estimated to grow at a CAGR of 5.4% to reach USD 354.6 billion by 2035.

Increased focus on minimizing traffic-related risks and improving travel efficiency continues to accelerate adoption. Regulatory frameworks that support controlled testing and early deployment are opening new commercialization opportunities for autonomous technologies. Advancements in artificial intelligence, sensing systems, and high-performance computing are improving system reliability and real-world performance. Integration of autonomous vehicles with intelligent urban infrastructure is strengthening market momentum through connected traffic platforms, vehicle-to-infrastructure communication, and adaptive routing capabilities. These technologies are improving traffic flow, lowering congestion levels, and supporting reduced energy consumption. Growth is further supported by the expansion of autonomous mobility platforms, which are reshaping urban transportation economics and improving fleet efficiency while enabling scalable automated transport models. The autonomous mobility as a service platform market continues to expand as fleet operators report operational cost reductions of at least 30% following the adoption of automation-focused systems. These platforms are proving commercially viable and scalable, reinforcing long-term confidence in automated transportation services.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $202.4 Billion |

| Forecast Value | $354.6 Billion |

| CAGR | 5.4% |

The Level 3 automation segment held a 46% share in 2025 and is forecast to grow at a CAGR of 5.2% from 2026 to 2035. Level 3 vehicles allow partial disengagement from driving tasks while ensuring driver readiness, making them widely adopted across multiple vehicle categories. A significant portion of autonomous development programs continues to focus on Level 3 functionality, supporting sustained demand.

The internal combustion engine vehicles segment accounted for 72% share in 2025 and is expected to grow at a CAGR of 4.8% through 2035. These vehicles benefit from established manufacturing platforms that simplify automation integration. Electric autonomous vehicles represent the second-largest segment due to their compatibility with software-driven architectures, advanced sensor arrays, and centralized computing systems, while ICE platforms rely more heavily on mechanical performance characteristics.

United States Self-driving Cars Market held an 83% share and generated USD 33.6 billion in 2025. Strong investment activity, favorable policy initiatives, and accelerating commercial deployment continue to position the country as a central hub for autonomous vehicle development and long-term market growth.

Key companies active in the Global Self-driving Cars Market include Tesla, Toyota Motor, Hyundai Motor, Volkswagen, General Motors, BMW, Ford Motor Company, Daimler (Mercedes-Benz), Honda Motor, and BYD. Companies in the Global Self-driving Cars Market are strengthening their market position through aggressive investment in artificial intelligence, advanced driver assistance software, and proprietary autonomous platforms. Strategic partnerships with technology providers are enabling faster innovation cycles and improved system integration. Automakers are prioritizing scalable architectures that support multiple autonomy levels across vehicle portfolios. Continuous real-world testing and data-driven optimization remain central to product refinement. Firms are also focusing on regulatory alignment and safety validation to accelerate approvals. Expansion into fleet-based and mobility service models is helping companies diversify revenue streams.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Level of Autonomy

- 2.2.3 Propulsion

- 2.2.4 Technology

- 2.2.5 Vehicle

- 2.2.6 Application

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1.1 Growth drivers

- 3.2.1.2 Road safety and accident reduction

- 3.2.1.3 Advancements in artificial intelligence and sensors

- 3.2.1.4 Government testing approvals and regulations

- 3.2.1.5 Growth of autonomous mobility services

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High development and validation costs

- 3.2.2.2 Regulatory uncertainty across regions

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of robotaxi and autonomous fleet services

- 3.2.3.2 Autonomous logistics and freight transport

- 3.2.3.3 Integration with smart city infrastructure

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 US National Highway Traffic Safety Administration (NHTSA) FMVSS Updates for Automated Vehicles

- 3.4.1.2 US Department of Transportation (DOT) Automated Vehicles Comprehensive Plan (AVCP)

- 3.4.1.3 State-Level Autonomous Testing Permits (California DMV & Nevada DMV Guidelines)

- 3.4.1.4 Transport Canada Guidelines for Testing Automated Driving Systems (ADS)

- 3.4.2 Europe

- 3.4.2.1 UNECE Regulation No. 157 on Automated Lane Keeping Systems (ALKS)

- 3.4.2.2 European Union General Safety Regulation (GSR) for Type Approval of ADS

- 3.4.2.3 Germany Federal Motor Transport Authority (KBA) Level 4 Operating Permits

- 3.4.2.4 UK Automated Vehicles Act and Liability Frameworks

- 3.4.3 Asia Pacific

- 3.4.3.1 China Ministry of Industry and Information Technology (MIIT) ICV Market Access Guide

- 3.4.3.2 Japan Ministry of Land, Infrastructure, Transport and Tourism (MLIT) Level 4 Licensing

- 3.4.3.3 South Korea MOLIT Safety Standards for Autonomous Vehicle Commercialization

- 3.4.3.4 Singapore Technical Reference 68 (TR 68) for Autonomous Vehicles

- 3.4.3.5 India Ministry of Road Transport and Highways (MoRTH) Emerging ADAS Guidelines

- 3.4.4 Latin America

- 3.4.4.1 Brazil National Traffic Council (CONTRAN) Resolutions on Assisted Driving

- 3.4.4.2 Mexico Mobility & Road Safety General Law (LGMSV) Implications for Automation

- 3.4.4.3 Chile Ministry of Transport Regulations on Autonomous Pilot Testing

- 3.4.4.4 Regional Alignment with UN World Forum for Harmonization of Vehicle Regulations (WP.29)

- 3.4.5 Middle East & Africa

- 3.4.5.1 UAE Roads and Transport Authority (RTA) Regulations for Autonomous Transport

- 3.4.5.2 Saudi Arabia SASO Technical Standards for Electric and Autonomous Vehicles

- 3.4.5.3 Israel Ministry of Transport Guidelines for Driverless Vehicle Trials

- 3.4.5.4 South Africa Standards for Intelligent Transport Systems (ITS) Deployment

- 3.4.1 North America

- 3.5 Porter';s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Production statistics

- 3.9.1 Production hubs

- 3.9.2 Consumption hubs

- 3.9.3 Export and import

- 3.10 Cost breakdown analysis

- 3.11 Patent analysis

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly Initiatives

- 3.12.5 Carbon footprint considerations

- 3.13 AV System Architecture & Software Stack

- 3.13.1 Autonomous driving system architecture & stack analysis

- 3.13.2 Compute, sensor, and software orchestration models

- 3.14 Autonomous Software, AI & Data Flywheel

- 3.15 Validation, Testing & Safety Assurance Framework

- 3.16 AV Business Models & Monetization

- 3.17 HD Mapping, V2X & Infrastructure Dependency

- 3.18 Consumer Trust & Adoption Barriers

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Level of Autonomy, 2022 - 2035 (USD Mn, Units)

- 5.1 Key trends

- 5.2 L1

- 5.3 L2

- 5.4 L3

- 5.5 L4

- 5.6 L5

Chapter 6 Market Estimates & Forecast, By Propulsion, 2022 - 2035 (USD Mn, Units)

- 6.1 Key trends

- 6.2 ICE

- 6.3 Electric

- 6.4 Hybrid vehicle

Chapter 7 Market Estimates & Forecast, By Technology, 2022 - 2035 (USD Mn, Units)

- 7.1 Key trends

- 7.2 Camera-Based Systems

- 7.3 Radar-Based Systems

- 7.4 LiDAR-Based Systems

- 7.5 Sensor Fusion Systems

Chapter 8 Market Estimates & Forecast, By Vehicle, 2022 - 2035 (USD Mn, Units)

- 8.1 Key trends

- 8.2 Compact cars

- 8.3 Mid-size cars

- 8.4 SUVs & luxury cars

Chapter 9 Market Estimates & Forecast, By Application, 2022 - 2035 (USD Mn, Units)

- 9.1 Key trends

- 9.2 Personal use

- 9.3 Shared mobility

- 9.4 Logistics & delivery

- 9.5 Public transport

- 9.6 Others

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 (USD Mn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.3.8 Netherlands

- 10.3.9 Sweden

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Singapore

- 10.4.7 Thailand

- 10.4.8 Indonesia

- 10.4.9 Vietnam

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

- 10.6.4 Turkey

Chapter 11 Company Profiles

- 11.1 Global Players

- 11.1.1 BMW

- 11.1.2 Daimler (Mercedes-Benz)

- 11.1.3 Ford Motor Company

- 11.1.4 General Motors (GM)

- 11.1.5 Honda Motor

- 11.1.6 Hyundai Motor

- 11.1.7 Stellantis

- 11.1.8 Tesla

- 11.1.9 Toyota Motor

- 11.1.10 Volkswagen

- 11.2 Regional Players

- 11.2.1 BYD

- 11.2.2 Geely

- 11.2.3 Renault-Nissan-Mitsubishi Alliance

- 11.2.4 SAIC Motor

- 11.2.5 Tata Motors

- 11.3 Emerging Players / Disruptors

- 11.3.1 Aurora Innovation

- 11.3.2 Baidu

- 11.3.3 NIO

- 11.3.4 Waymo

- 11.3.5 XPeng Motors