|

시장보고서

상품코드

1928994

픽앤플레이스 머신 시장의 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2026-2035년)Pick and Place Machine Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

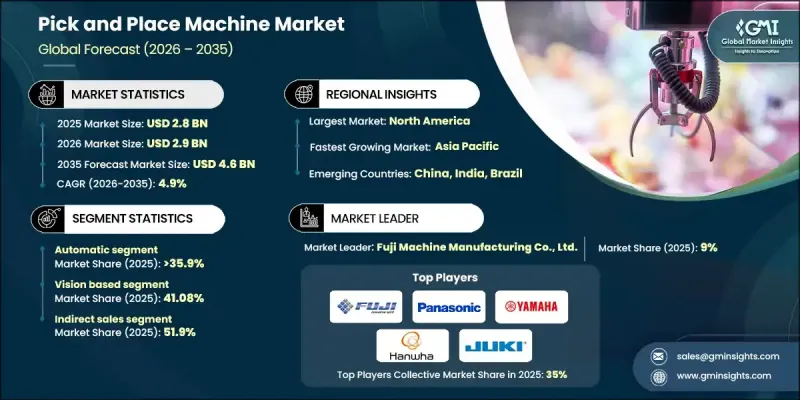

세계의 픽앤플레이스 머신 시장은 2025년에 28억 달러로 평가되었으며, 2035년까지 CAGR 4.9%로 성장하여 46억 달러에 달할 것으로 예측됩니다.

시장 확대는 현대 전자제품 제조에 필수적인 고속, 고정밀 표면 실장 기술(SMT) 배치 시스템에 대한 수요 증가에 의해 주도되고 있습니다. 효율성 향상, 정확성, 일관된 품질에 대한 요구가 높아지면서 업계 재편이 진행되고 있으며, 주요 기업들이 경쟁업체를 인수 합병하여 역량을 확장하고 있습니다. 이번 조직개편을 통해 제품 포트폴리오 확대, R&D 투자 확대, 세계 시장에서의 입지를 강화할 수 있게 되었습니다. 기존의 수동 부품 실장 및 반자동 기계로는 특히 5G, 자동차, EV 분야에서 소형화된 전자기기의 정밀도와 속도 요건을 충족시키기가 점점 더 어려워지고 있습니다. 에너지 효율이 높은 서보 모터와 열 안정성을 갖춘 완전 자동화 시스템은 작동 시 전력 손실을 줄이고, 지속가능한 첨단 기술 제조 방식에 부합합니다. 이러한 첨단 기계의 도입으로 제조업체는 정밀도와 운영 효율성을 유지하면서 대량 생산 목표를 달성할 수 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 연도 | 2026-2035 |

| 개시시 가치 | 28억 달러 |

| 예측 금액 | 46억 달러 |

| CAGR | 4.9% |

자동 픽앤플레이스 분야는 2025년 35.9%의 점유율을 차지하며 10억 달러의 수익을 창출할 것으로 예상됩니다. 자동화 기계가 주류가 된 이유는 현대 전자제품 제조에 필요한 서브마이크론 단위의 배치 정확도, 고속 동작, 확장성을 제공하기 때문입니다. 이러한 시스템은 인더스트리 4.0 도입에 필수적이며, 로봇 공학, 스마트 팩토리 네트워크, 예지보전 플랫폼과의 원활한 통합을 가능하게 합니다. 스마트폰, 전기자동차(EV), 자동차 및 항공우주 산업에서 전자제어장치(ECU)의 생산 증가는 고성능 자동 실장 시스템에 대한 수요를 더욱 촉진하고 있습니다. 인적 오류 감소, 처리량 최적화, 일관된 품질 보증을 실현할 수 있는 능력으로 대량 생산에 필수적인 존재가 되었습니다.

비전 기반 픽앤플레이스 시스템은 41.08%의 점유율을 차지하며 2025년 12억 달러의 시장 규모를 형성할 것으로 예상됩니다. 비전 시스템은 소형 및 고밀도 부품에 대한 실시간 광학 인식, 정렬 및 결함 감지를 제공하여 매우 높은 수율을 보장합니다. 이 기술은 미세 피치 부품의 배치와 복잡한 어셈블리를 뛰어난 정밀도로 처리하는 데 필수적인 기술입니다. 검사와 배치를 동시에 통합할 수 있는 능력은 재작업과 낭비를 줄이고 전체 생산 효율을 향상시킵니다. 제조업체들은 항공우주, 의료기기 조립, 자동차 전장 분야에서 요구되는 엄격한 품질 기준 충족, 사이클 타임 단축, 오류율 감소를 위해 비전 기반 시스템에 대한 의존도를 높이고 있습니다.

2025년 기준 미국 픽앤플레이스 장비 시장은 84.5%의 점유율을 차지했습니다. 이러한 우위는 첨단 로봇공학, AI 통합 조립 시스템, 고정밀 제조 기술의 조기 도입으로 뒷받침되고 있습니다. 자동차 및 항공우주 분야의 강력한 수요가 시장을 주도하고 있으며, 이들 분야에서는 복잡한 전자 제어 장치, 센서, 고밀도 기판 조립에 픽앤플레이스 장비가 필수적입니다. 또한, 클린룸 환경에서의 가동과 극도의 정밀도가 요구되는 의료기기 분야도 성장에 기여하고 있습니다. 북미의 경우, 잘 구축된 전자제품 제조 생태계에 더해 높은 R&D 투자와 스마트 팩토리 개념의 도입이 결합되어 시장을 지속적으로 견인하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급업체 상황

- 이익률

- 각 단계의 부가가치

- 밸류체인에 영향을 미치는 요인

- 업계에 대한 영향요인

- 성장 촉진요인

- 전자부품 소형화

- 인더스트리 4.0 및 스마트 공장으로의 전환

- 전기자동차(EV)용 전자기기 수요 증가

- 업계의 잠재적 리스크와 과제

- 높은 초기 투자액

- 다품종소량생산의 프로그래밍의 복잡성

- 기회

- AI를 활용한 예지보전

- 5G 및 위성통신 확대

- 성장 촉진요인

- 성장 가능성 분석

- 향후 시장 동향

- 기술과 혁신 동향

- 현재 기술 동향

- 신기술

- 가격 동향

- 지역별

- 유형별

- 규제 상황

- 규격 및 컴플라이언스 요건

- 지역별 규제 프레임워크

- 인증 기준

- Porters 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 인수합병

- 제휴·협업

- 신제품 발매

- 확대 계획

제5장 시장 추정 및 예측 : 유형별, 2022-2035

- 수동식

- 반자동

- 자동식

제6장 시장 추정 및 예측 : 기술별, 2022-2035

- 비전 기반

- 힘 기반

- 레이저 방식

- 하이브리드

제7장 시장 추정 및 예측 : 용량별, 2022-2035

- 주요 동향

- 10,000 CPH 이하

- 10,000-20,000 CPH

- 20,000 CPH 이상

제8장 시장 추정 및 예측 : 용도별, 2022-2035

- 소비자 전자제품

- 자동차

- 포장 업계

- 제약

- 물류

- 기타

제9장 시장 추정 및 예측 : 유통 채널별, 2022-2035

- 직접

- 간접

제10장 시장 추정 및 예측 : 지역별, 2022-2035

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카공화국

- 사우디아라비아

- 아랍에미리트

제11장 기업 개요

- ASM Assembly Systems GmbH & Co. KG

- Fuji Machine Manufacturing Co., Ltd.

- Juki Corporation

- Panasonic Corporation

- Yamaha Motor Co., Ltd.

- Hanwha Corporation

- Mycronic AB

- Nordson Corporation

- Hanwha Techwin

- ASM Pacific Technology Ltd.

- Universal Instruments Corporation

- Europlacer Group

- Essemtec AG

- Viscom AG

- Speedline Technologies, Inc.

The Global Pick and Place Machine Market was valued at USD 2.8 billion in 2025 and is estimated to grow at a CAGR of 4.9% to reach USD 4.6 billion by 2035.

The market's expansion is driven by the increasing demand for high-speed, precise surface-mount technology (SMT) placement systems, which are essential for modern electronics manufacturing. Efficiency gains, accuracy, and the need for consistent quality have encouraged industry consolidation, as leading companies merge or acquire competitors to expand their capabilities. This consolidation has resulted in broader product portfolios, increased R&D investments, and stronger global market presence. Traditional manual component placement or semi-automatic machines are increasingly unable to meet the precision and speed requirements of miniaturized electronics, especially in the 5G, automotive, and EV sectors. Fully automated systems with energy-efficient servo motors and thermally stable materials offer reduced operational power loss and align with sustainable, high-tech manufacturing practices. Adoption of these advanced machines allows manufacturers to meet high-volume production targets while maintaining precision and operational efficiency.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.8 Billion |

| Forecast Value | $4.6 Billion |

| CAGR | 4.9% |

The automatic pick and place segment accounted for 35.9% share in 2025, generating USD 1 billion. Automatic machines dominate because they provide sub-micron placement accuracy, high-speed operation, and scalability required by modern electronics manufacturing. These systems are integral to Industry 4.0 implementations, enabling seamless integration with robotics, smart factory networks, and predictive maintenance platforms. The increasing production of smartphones, EVs, and electronic control units in the automotive and aerospace industries further drives the demand for high-performance automated placement systems. Their ability to reduce human error, optimize throughput, and ensure consistent quality makes them essential for high-volume manufacturing.

Vision-based pick and place systems held 41.08% share, generating USD 1.2 billion in 2025. Vision systems provide real-time optical recognition, alignment, and defect detection for small, high-density components, ensuring extremely high yield rates. This technology is critical for placing fine-pitch components and handling complex assemblies with exceptional accuracy. Its ability to integrate inspection and placement simultaneously reduces rework and waste, improving overall production efficiency. Manufacturers increasingly rely on vision-based systems to achieve faster cycle times, lower error rates, and compliance with stringent quality standards required in aerospace, medical device assembly, and automotive electronics.

U.S. Pick and Place Machine Market held 84.5% share in 2025. This dominance is fueled by early adoption of advanced robotics, AI-integrated assembly systems, and high-precision manufacturing technologies. Strong demand comes from the automotive and aerospace sectors, where pick and place machines are essential for assembling complex electronic control units, sensors, and high-density boards. Additionally, the medical device segment is contributing to growth, requiring specialized machines capable of cleanroom operation and extreme precision. North America's well-established electronics manufacturing ecosystem, combined with high R&D investment and adoption of smart factory concepts, continues to propel the market forward.

Major players operating in the Global Pick and Place Machine Market include ASM Pacific Technology Ltd., Yamaha Motor Co., Ltd., ASM Assembly Systems GmbH & Co. KG, Juki Corporation, Panasonic Corporation, Hanwha Techwin, Mycronic AB, Nordson Corporation, Universal Instruments Corporation, Speedline Technologies, Inc., Europlacer Group, Essemtec AG, Viscom AG, Hanwha Corporation, and others. These companies lead through continuous innovation, global expansion, and the development of automated, vision-integrated systems that meet evolving electronics manufacturing needs. Companies in the Pick and Place Machine Market are adopting multiple strategies to strengthen their market position. They focus heavily on mergers and acquisitions to consolidate technological expertise and expand regional reach. Product innovation, including AI-assisted placement, vision-based defect detection, and energy-efficient servo motors, enhances performance and sustainability. Firms invest in Industry 4.0 solutions to integrate machines into smart factories and provide connected, data-driven platforms for predictive maintenance.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Technology

- 2.2.4 Capacity

- 2.2.5 Application

- 2.2.6 Distribution Channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Miniaturization of electronic components

- 3.2.1.2 Transition to industry 4.0 and smart factories

- 3.2.1.3 Rise in electric vehicle (EV) electronics

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High initial capital expenditure

- 3.2.2.2 Complexity of programming for high-mix production

- 3.2.3 Opportunities

- 3.2.3.1 Ai-driven predictive maintenance

- 3.2.3.2 Expansion of 5G and satellite communication

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter';s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Type, 2022 - 2035 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Manual

- 5.3 Semi-automatic

- 5.4 Automatic

Chapter 6 Market Estimates and Forecast, By Technology, 2022 - 2035 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Vision based

- 6.3 Force based

- 6.4 Laser based

- 6.5 Hybrid

Chapter 7 Market Estimates and Forecast, By Capacity, 2022 - 2035 (USD Billion) (Thousand Units)

- 7.1 Key trend

- 7.2 Upto 10,000 CPH

- 7.3 10,000-20,000 CPH

- 7.4 Above 20,000 CPH

Chapter 8 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Consumer electronics

- 8.3 Automotive

- 8.4 Packaging industry

- 8.5 Pharmaceutical

- 8.6 Logistics

- 8.7 Others

Chapter 9 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Direct

- 9.3 Indirect

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 ASM Assembly Systems GmbH & Co. KG

- 11.2 Fuji Machine Manufacturing Co., Ltd.

- 11.3 Juki Corporation

- 11.4 Panasonic Corporation

- 11.5 Yamaha Motor Co., Ltd.

- 11.6 Hanwha Corporation

- 11.7 Mycronic AB

- 11.8 Nordson Corporation

- 11.9 Hanwha Techwin

- 11.10 ASM Pacific Technology Ltd.

- 11.11 Universal Instruments Corporation

- 11.12 Europlacer Group

- 11.13 Essemtec AG

- 11.14 Viscom AG

- 11.15 Speedline Technologies, Inc.